- Sensors & Controls

- GaN Chargers Market

GaN Chargers Market Size, Share, and Growth Forecast 2026 - 2033

GaN Chargers Market by Product Type (Wall Chargers, Desktop Chargers, Car Chargers, Power Banks, Travel Adapters, Industrial/Embedded Chargers), by Charging Type (Wired Chargers, Wireless Chargers, Hybrid Chargers), by Port Configuration (Single-Port, Dual-Port, Multi-Port), by Power Output (Below 30W, 30W-65W, 66W-100W, Above 100W), by End-User, by Regional Analysis, 2026 - 2033

GaN Chargers Market Size and Trend Analysis

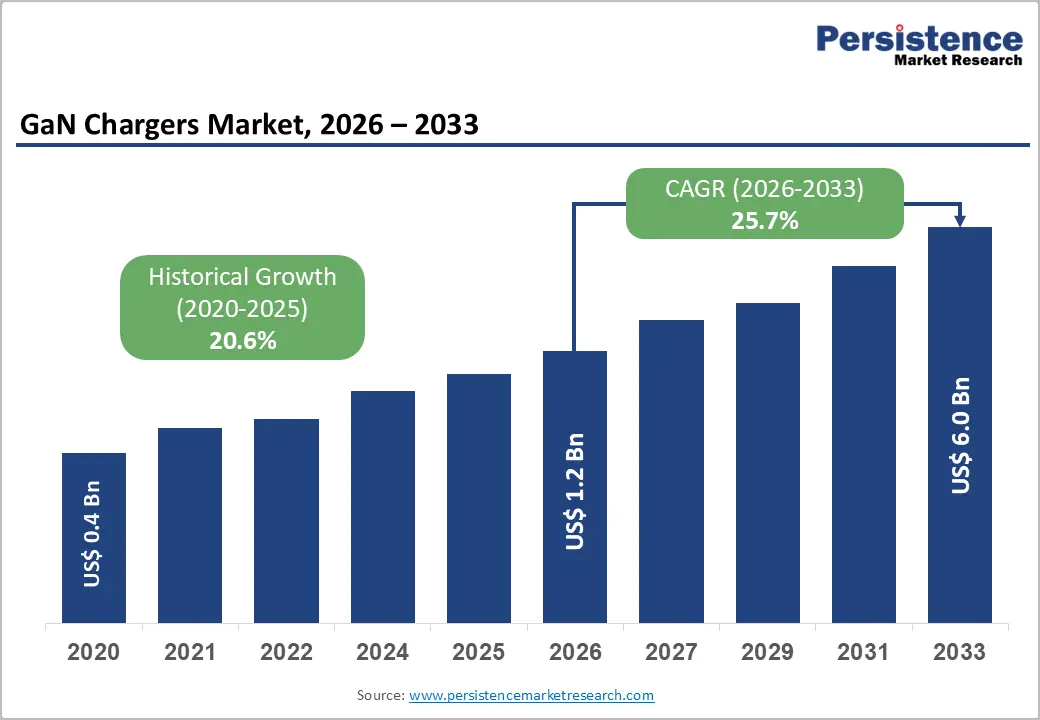

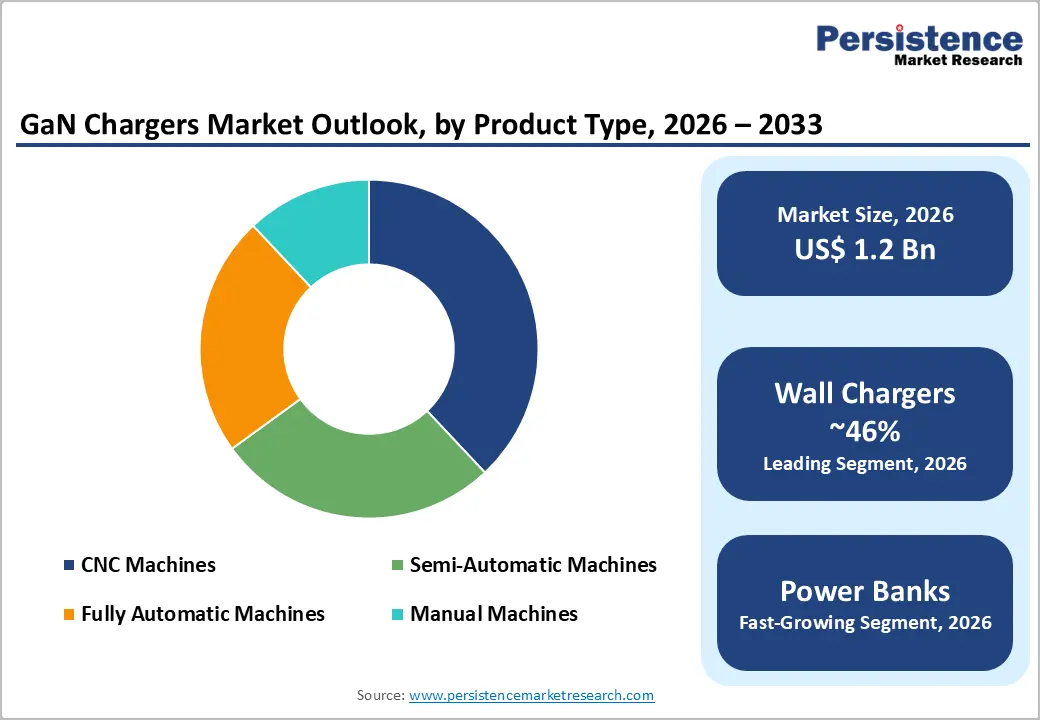

The global GaN chargers market size is likely to be valued at US$1.2 billion in 2026 and is expected to reach US$6.0 billion by 2033, growing at a CAGR of 25.7% during the forecast period from 2026 to 2033.

The market's exceptional growth trajectory is anchored in Gallium Nitride's (GaN) decisive technical superiority over traditional silicon-based charging solutions, delivering up to 40% smaller form factors, 3x higher switching frequencies, and efficiency ratings exceeding 95% at full load.

Key Market Highlights

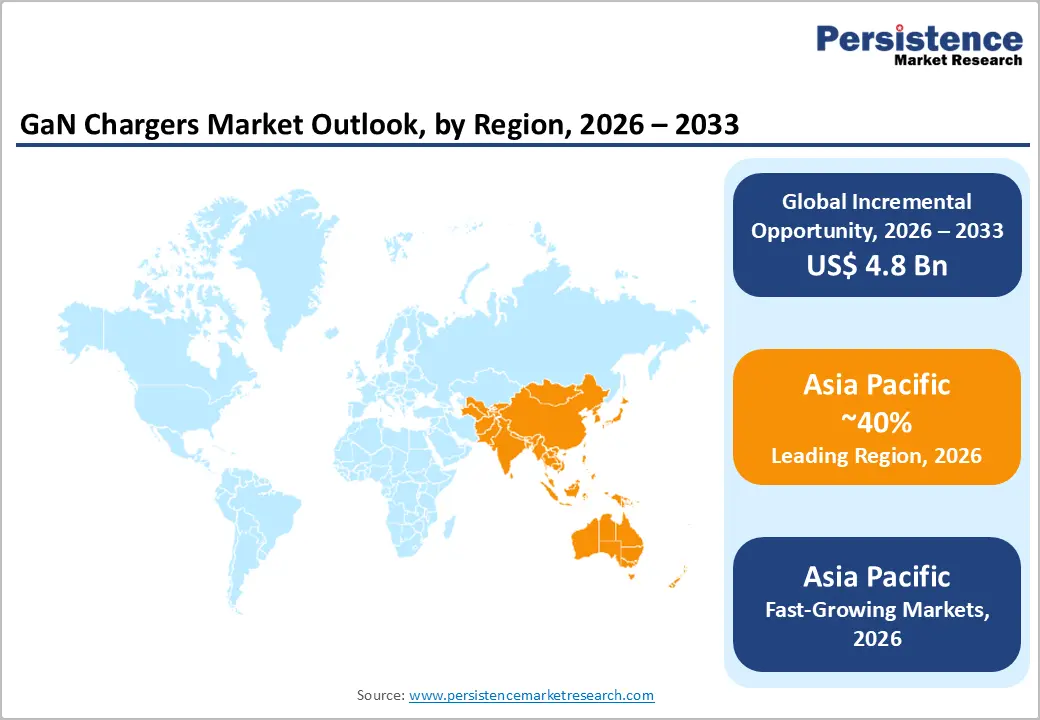

- Leading Region: Asia Pacific leads the global GaN Chargers market holding 40% share, driven by China's dominant GaN wafer manufacturing, including Innoscience's 8-inch GaN-on-Si foundry, alongside major consumer charger brands Anker, Baseus, and UGREEN commanding significant global market share.

- Fastest Growing Region: Europe is the fastest growing regional market with a rising CAGR of 30.0%, catalyzed by the EU Common Charger Directive mandating USB-C standardization from December 2024, triggering a continent-wide charger replacement cycle that disproportionately benefits compact, high-efficiency GaN-based USB-PD products.

- Dominant Segment: Wall Chargers dominate the product type category with approximately 46% market share, driven by universal fixed-location device charging demand and the EU Common Charger Directive-led replacement cycle favoring compact, high-wattage GaN wall adapter upgrades.

- Fastest Growing Segment: Above 100W GaN chargers are the fastest growing power output segment, fueled by expanding adoption in laptop multi-device charging, EV on-board charging components, and data center power supply applications demanding maximum power density and thermal efficiency.

- Key Market Opportunity: Electric vehicle on-board charger adoption represents a high-growth opportunity, with IEA reporting 14 million EV sales in 2023 and automotive-grade AEC-Q101 certified GaN devices from Navitas and GaN Systems enabling compact, high-efficiency EV charging system integration globally.

Market Dynamics

Market Growth Drivers

Proliferation of Multi-Device Ecosystems and Fast-Charging Standards

The explosion of connected personal devices, smartphones, laptops, tablets, wireless earbuds, and smartwatches has fundamentally altered consumer charging behavior, driving strong demand for compact, high-wattage multi-port GaN chargers. According to Ericsson's Mobility Report, global smartphone subscriptions are projected to reach 7.7 billion by 2028, while laptop shipments remain at historically elevated levels following the pandemic-driven shift to remote work.

Concurrently, the adoption of fast-charging protocols, including USB Power Delivery (USB-PD) and Qualcomm Quick Charge, which require power delivery circuits operating at higher voltages and switching frequencies, creates a natural technological home for GaN transistors. The USB Implementers Forum (USB-IF) certification ecosystem for USB-PD chargers has effectively standardized GaN-enabling power architectures, directly accelerating market penetration across consumer and enterprise device charging segments.

Regulatory Push for Energy-Efficient Power Adapters and Universal Charging Mandates

Global regulatory mandates for energy-efficient and standardized chargers are powerfully accelerating GaN adoption across consumer electronics and commercial infrastructure segments. The European Union's Common Charger Directive (2022/2380/EU), which mandates USB-C port standardization for consumer electronics sold in the EU by 2024-2026, has created an urgent product refresh cycle favoring GaN-based USB-PD chargers.

The U.S. Department of Energy (DOE)'s Level VI external power supply efficiency standards impose minimum efficiency requirements that silicon chargers increasingly struggle to meet at compact form factors. Additionally, China's GB 4943.1 and CQC charger certification standards are being updated to reflect USB-PD compatibility, aligning the world's largest consumer electronics market with GaN-enabling architectural requirements. These converging regulatory frameworks collectively mandate hardware transitions that benefit GaN charger manufacturers globally.

Market Restraints

Higher Manufacturing Cost Compared to Silicon Counterparts

The higher cost of GaN semiconductor wafers and the more complex manufacturing processes involved in GaN power device fabrication result in retail pricing for GaN chargers that typically commands a 40% premium over comparable silicon-based chargers.

Gallium metal, a primary GaN precursor, is subject to supply concentration risk, with China accounting for over 80% of global gallium production, according to the U.S. Geological Survey (USGS). This pricing disadvantage limits mass-market penetration in price-sensitive emerging market geographies and commodity consumer electronics segments where cost parity with silicon alternatives is a prerequisite for broad adoption.

Supply Chain Concentration Risk for Gallium and GaN Wafers

Gallium nitride wafer supply is concentrated among a small number of specialized substrate manufacturers, creating structural supply chain fragility. In July 2023, China's Ministry of Commerce announced export restrictions on gallium and germanium, two critical materials used in the production of wide-bandgap semiconductors.

This geopolitical supply risk, acknowledged by the European Commission's Critical Raw Materials Act, which lists gallium as a strategic raw material, introduces pricing volatility and procurement uncertainty for GaN charger manufacturers globally, potentially constraining production scaling and compressing margins during periods of tightened export controls or elevated geopolitical tension.

Market Opportunities

Electric Vehicle On-Board and Portable GaN Charging Solutions

The global electric vehicle (EV) revolution represents a transformative growth opportunity for high-power GaN charging technology. The International Energy Agency (IEA) reported that global EV sales surpassed 14 million units in 2023, with the global EV fleet approaching 40 million vehicles. EV on-board chargers (OBCs) operating at 6.6 kW to 22 kW are increasingly adopting GaN transistors to achieve the higher power densities and efficiency levels demanded by automakers targeting vehicle range optimization and compact powertrain packaging.

Companies, including Navitas Semiconductor and GaN Systems, have specifically developed automotive-grade GaN devices certified under AEC-Q101 standards. As EV adoption continues to accelerate under government mandates, including the EU's 2035 ICE vehicle sales ban, demand for automotive-grade GaN charging components and portable EV travel adapters is set to grow exponentially over the forecast period.

Data Center and Industrial Power Infrastructure Adoption of High-Power GaN

Data centers and industrial power infrastructure represent an emerging, high-value opportunity for GaN charger and power supply manufacturers targeting the above-100W segment. The U.S. Department of Energy (DOE) estimates that U.S. data centers consumed approximately 200 billion kWh of electricity in 2023, with power supply efficiency being a critical operational lever for total cost of ownership.

GaN-based server power supply units (PSUs) and rack-mounted chargers deliver measurably higher efficiency, approaching 98% under 80 PLUS Titanium benchmarks, compared to 94% for best-in-class silicon alternatives. Innoscience and Navitas Semiconductor are actively expanding their GaN IC portfolios targeting server and telecom rectifier applications. As AI-driven data center buildouts intensify global demand for power-dense, thermally efficient charging and power-conversion infrastructure, GaN solution providers are positioned to capture significant incremental revenue in this premium-priced industrial segment.

Category-wise Insights

Product Type Analysis

Wall Chargers dominate the product type segment, accounting for approximately 46% of total GaN charger market revenues. The segment's primacy reflects the universal consumer need for primary device charging at fixed locations, homes, offices, and hotels, where compact, high-wattage GaN wall chargers delivering 45W-140W through USB-PD protocols have become the preferred replacement for bulky legacy adapters.

The EU Common Charger Directive and widespread adoption of USB-C across smartphones and laptops have created a direct procurement tailwind for GaN wall charger upgrades. Premium offerings from Anker's Nano and Prime series and Belkin's BoostCharge Pro range have demonstrated strong consumer willingness to pay for the size and speed advantages GaN wall chargers deliver over silicon alternatives.

Charging Type Analysis

Wired Chargers are the dominant charging type segment, commanding approximately 71% of total segment revenues. Despite the growth of wireless charging standards, including Qi2 and MagSafe, wired GaN chargers maintain decisive advantages in charging speed, cost efficiency, and energy transfer reliability.

USB-PD wired charging enables power delivery up to 240W under the USB-PD 3.1 specification, a benchmark that wireless technologies cannot currently approach. The USB Implementers Forum (USB-IF) reports that USB-PD-certified product certifications have grown at double-digit rates annually, reflecting deep market entrenchment of the wired fast-charging architecture across consumer and professional device ecosystems globally.

Port Configuration Analysis

Multi-Port GaN chargers lead the port configuration segment with an estimated 44% revenue share, driven by consumers' and professionals' growing need to charge multiple devices from a single, compact power unit. The average consumer now owns 5 chargeable devices according to Consumer Technology Association (CTA) surveys, creating persistent demand for multi-port solutions that eliminate the need for multiple wall outlets and adapters.

GaN's efficiency advantages at high power densities make it uniquely capable of delivering full wattage across multiple ports simultaneously without thermal throttling, a critical differentiator over silicon multi-port chargers that typically derate individual port output under concurrent charging loads.

Power Output Analysis

The 30W-65W power output segment leads the market, accounting for approximately 38% of revenue. This power range optimally serves the largest addressable consumer device category, laptops, tablets, and premium smartphones, which represent the primary use case driving GaN charger upgrades from legacy silicon adapters.

MacBook Air (30W-67W) and a broad range of USB-C laptops from Dell, HP, and Lenovo fall precisely within this power delivery range. The USB-IF's USB-PD certification data confirms this segment accounts for the highest certification volume, reflecting both consumer demand concentration and OEM compliance requirements within the 30W-65W power window.

End-User Analysis

Consumer Electronics is the dominant end-user segment, accounting for approximately 54% of the total GaN Chargers market revenue. This dominance reflects the segment's massive addressable base of smartphones, laptops, tablets, gaming handhelds, and wearables, all of which are actively transitioning to USB-C and USB-PD fast charging, requiring GaN-optimized power delivery architectures.

According to the Consumer Technology Association (CTA), U.S. consumer electronics spending exceeded US$ 505 billion in 2023, with portable device chargers and accessories representing a high-velocity aftermarket category. The EU Common Charger Directive is catalyzing a continent-wide consumer charger replacement cycle, while rising consumer awareness of GaN's compact and efficient benefits is further intensifying aftermarket procurement volumes globally.

Regional Insights

North America GaN Chargers Market Trends & Analysis

North America remains a technology-driven market for GaN chargers, supported by high penetration of premium consumer electronics and strong adoption of USB-PD fast charging ecosystems. Regulatory frameworks promoting energy efficiency and domestic semiconductor innovation are accelerating GaN integration across consumer and enterprise charging solutions.

- U.S. GaN Chargers Market Size

The U.S. GaN chargers market is estimated at ~US$ 950 million in 2026, driven by strong demand for multi-device fast chargers, high laptop penetration, and enterprise IT upgrades. Growth is supported by DOE efficiency standards, widespread USB-C adoption, and increasing availability of compact, high-wattage GaN chargers across retail and e-commerce channels.

Europe GaN Chargers Market Trends, Drivers & Insights

Europe’s GaN charger market is primarily driven by regulatory mandates and sustainability goals. The EU’s universal USB-C directive has triggered a large-scale replacement cycle, while strict energy efficiency regulations are encouraging OEMs to shift toward GaN-based designs. Strong enterprise IT demand and the development of the EV ecosystem further reinforce market growth.

- Germany GaN Chargers Market Size

Germany leads the European GaN charger market with an estimated size of ~US$ 250 million in 2026. Growth is driven by its advanced industrial base, high purchasing power, and strong demand for efficient charging solutions across enterprise IT, automotive electronics, and premium consumer segments.

- U.K. GaN Chargers Market Size

The U.K. GaN charger market is projected to reach ~US$ 150 million in 2026, supported by high e-commerce penetration and the increasing adoption of USB-C charging standards. Post-Brexit regulatory alignment with EU directives and growing demand for compact, high-speed chargers are key growth contributors.

- France GaN Chargers Market Size

France’s GaN chargers market is estimated at ~US$ 120 million in 2026, driven by strong retail distribution networks and rising consumer awareness of energy-efficient electronics. Government-backed sustainability initiatives and EU compliance requirements are accelerating the transition toward GaN-based charging solutions.

Asia Pacific GaN Chargers Market Drivers & Analysis

Asia Pacific dominates the global GaN chargers market, supported by large-scale electronics manufacturing, strong supply chain integration, and rapid smartphone adoption. The region benefits from cost-efficient production, increasing USB-C standardization, and rising demand for fast-charging accessories across emerging and developed economies.

- China GaN Chargers Market Size

China accounts for the largest share, with a market size of ~US$ 1.9 billion in 2026. The country’s dominance is driven by vertically integrated manufacturing, strong domestic demand, and the presence of leading GaN component suppliers and charger brands catering to both local and global markets.

- India GaN Chargers Market Size

India’s GaN chargers market is estimated at ~US$ 280 million in 2026, fueled by a rapidly expanding smartphone user base and increasing demand for affordable fast-charging solutions. Government-led standardization initiatives and rising e-commerce penetration are accelerating adoption across urban and semi-urban consumers.

- Japan GaN Chargers Market Size

Japan’s GaN charger market is projected to reach ~US$ 200 million in 2026, supported by strong expertise in power electronics and high demand for compact, high-efficiency devices. Premium consumer electronics and industrial applications are key contributors to steady market expansion.

Competitive Landscape

The global GaN Chargers market is moderately fragmented, featuring consumer accessory brands, semiconductor IP companies, and contract electronics manufacturers operating across distinct value chain layers. Consumer-facing leaders Anker, Baseus, and UGREEN compete on industrial design, multi-port functionality, and brand trust. Semiconductor enablers Navitas Semiconductor and Innoscience differentiate through GaN IC performance and wafer cost competitiveness.

Strategic drivers include USB-PD 3.1 compliance roadmaps, eco-certification (USB-IF, Energy Star), and direct-to-consumer e-commerce channel investment. Emerging business models include OEM white-labeling partnerships with consumer electronics brands replacing bundled silicon chargers with GaN alternatives across flagship product lines.

Key Market Developments

- January 2025: Anker launched its Prime 240W GaN Desktop Charging Station at CES 2025, featuring six ports and a companion smartphone app for real-time power monitoring, targeting power users and professionals managing multiple high-wattage devices simultaneously.

- October 2024: Navitas Semiconductor announced mass production of its third-generation GaNFast NV6177 power IC, achieving 98% peak efficiency for 65W-140W charger applications, with design wins at leading Chinese and European charger OEMs targeting EU Common Charger Directive compliance product refreshes.

- April 2024: Innoscience began commercial shipment of its 8-inch GaN-on-Si wafers at volume, reducing GaN device production costs by an estimated 30-40% versus 6-inch wafer baselines, enabling broader price-competitive GaN charger rollouts by downstream consumer electronics accessory manufacturers globally.

GaN Chargers Market- Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 0.4 Bn |

| Current Market Value (2026) | US$ 1.2 Bn |

| Projected Market Value (2033) | US$ 6.0 Bn |

| CAGR (2026 - 2033) | 25.7% |

| Leading Region | Asia Pacific, 40% share |

| Dominant Product Type | Wall Chargers, 46% share |

| Top-ranking Charging Type | Wired Chargers, 71% |

| Incremental Opportunity | US$ 4.8 Bn |

Companies Covered in GaN Chargers Market

- Anker Innovations Technology Co., Ltd.

- Baseus

- UGREEN Group Limited

- Belkin International, Inc.

- Zendure

- Mophie

- AUKEY

- RAVPower

- CHOETECH

- Spigen Inc.

- Nekteck

- HyperJuice

- Navitas Semiconductor

- GaN Systems

- Innoscience Technology Co., Ltd.

- Infineon Technologies AG

- STMicroelectronics N.V.

- EFM Technologies

- Ugreen Group

- Xiaomi Corporation

Frequently Asked Questions

The global GaN Chargers market is projected to reach US$ 6.0 Billion by 2033, growing from US$ 1.2 Billion in 2026 at an exceptional CAGR of 25.7%, driven by proliferating multi-device ecosystems, USB-PD fast charging adoption, stringent global energy efficiency regulations, and accelerating EV on-board charger integration of GaN semiconductor technology.

Primary demand drivers include the proliferation of multi-device consumer ecosystems, with global smartphone subscriptions projected at 7.7 billion by 2028 per Ericsson, and the EU's Common Charger Directive mandating USB-C standardization from December 2024. GaN's 40% smaller form factor and 95%+ efficiency ratings versus silicon alternatives compel OEM product refreshes globally.

Wall Chargers lead the product type segment with approximately 46% revenue share. Their dominance is driven by universal fixed-location device charging demand, USB-PD compatibility with the EU Common Charger Directive, and strong consumer adoption of premium GaN wall adapter lines from brands including Anker's Nano and Prime series and Belkin's BoostCharge Pro range.

Asia Pacific leads the global GaN Chargers market, anchored by China's dominant GaN wafer manufacturing through Innoscience's 8-inch GaN-on-Si foundry and globally significant consumer brand presence from Anker, Baseus, UGREEN, and AUKEY. South Korea, Japan, and India further strengthen the region's combined production capacity and consumer demand base.

The foremost opportunities are EV on-board charger integration, with IEA reporting 14 million EV sales in 2023 and AEC-Q101-certified GaN devices from Navitas and GaN Systems enabling compact EV charging, and data center high-efficiency GaN power supplies approaching 98% efficiency under 80 PLUS Titanium benchmarks, targeting DOE Level VI and EU Ecodesign compliance requirements.

Key market participants include consumer brands Anker, Baseus, UGREEN, Belkin, Zendure, Mophie, AUKEY, RAVPower, CHOETECH, Spigen, Nekteck, and HyperJuice, alongside GaN semiconductor leaders Navitas Semiconductor, GaN Systems (Infineon Technologies), Innoscience, STMicroelectronics, and Infineon Technologies AG serving the charger IC and wafer supply chain.