- Sensors & Controls

- Engineering Services Market

Engineering Services Market Size, Share, and Growth Forecast 2026 - 2033

Engineering Services Market by Service Type (Design and Development, Consulting), Engineering Discipline (Civil, Mechanical), Application (Infrastructure Development, Industrial Projects), End-user, and Regional Analysis, 2026 - 2033

Engineering Services Market Size and Trends Analysis

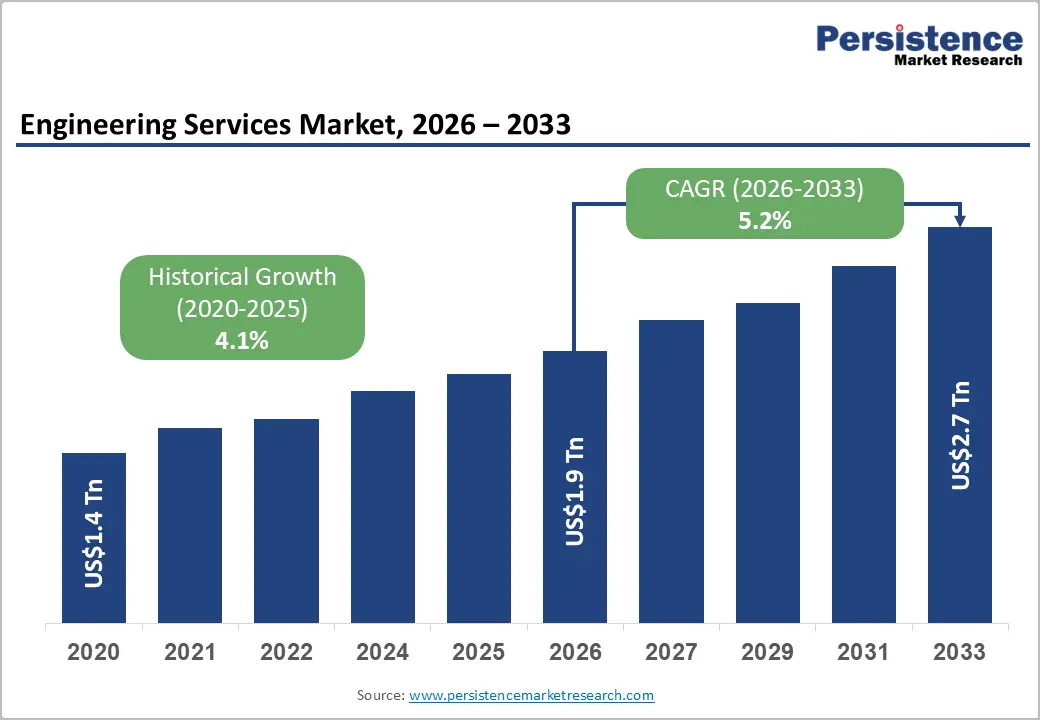

The global engineering services market size is likely to be valued at US$1.9 trillion in 2026 and is expected to reach US$2.7 trillion by 2033, growing at a CAGR of 5.2% during the forecast period from 2026 to 2033, driven by the rising adoption of AI-led product engineering and increasing demand for software-defined systems in automotive and electronics.

Ongoing expansion of semiconductor and advanced manufacturing networks, supported by government initiatives, is also expected to bolster the market.

Key Industry Highlights:

- Recent Acquisition: In August 2025, Wipro Limited announced an agreement to acquire HARMAN's Digital Transformation Solutions (DTS) business unit, a Samsung company. Wipro stated that DTS's strengths in embedded software, connected product engineering, and AI-native platforms would strengthen its position as a global leader in engineering research and development services.

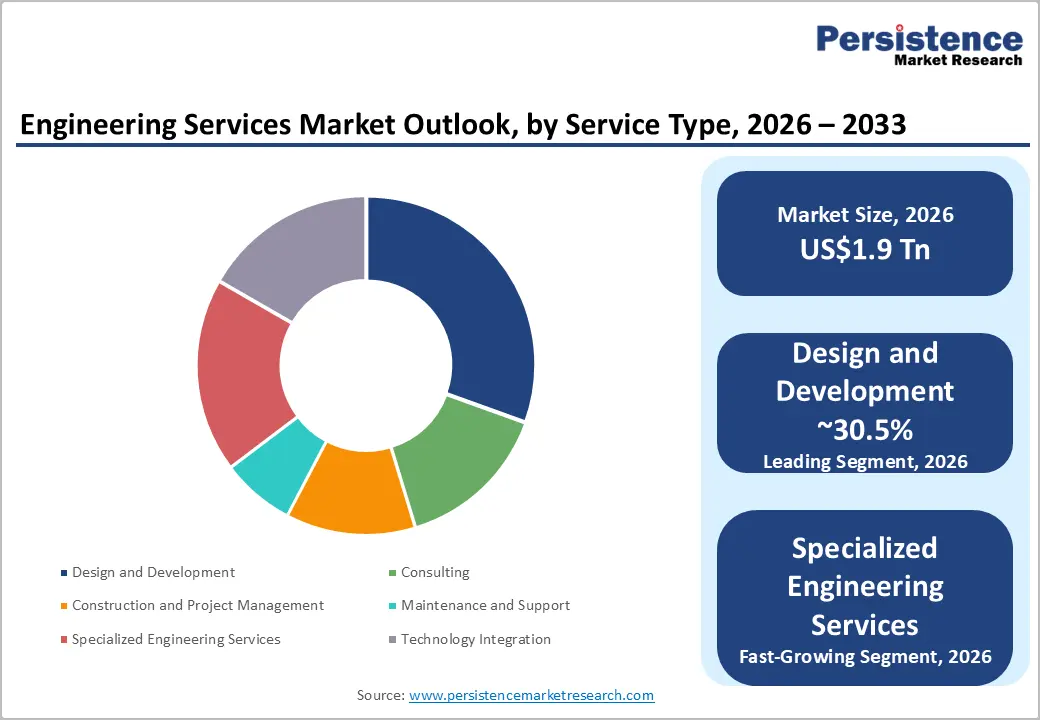

- Leading Service Type: Design and development, approximately 30.5% share in 2026, as companies are outsourcing core product engineering to reduce time-to-market.

- Dominant Application: Environmental projects, nearly 38.2% in 2026, owing to strict climate policies and large-scale government-backed investments in renewable energy.

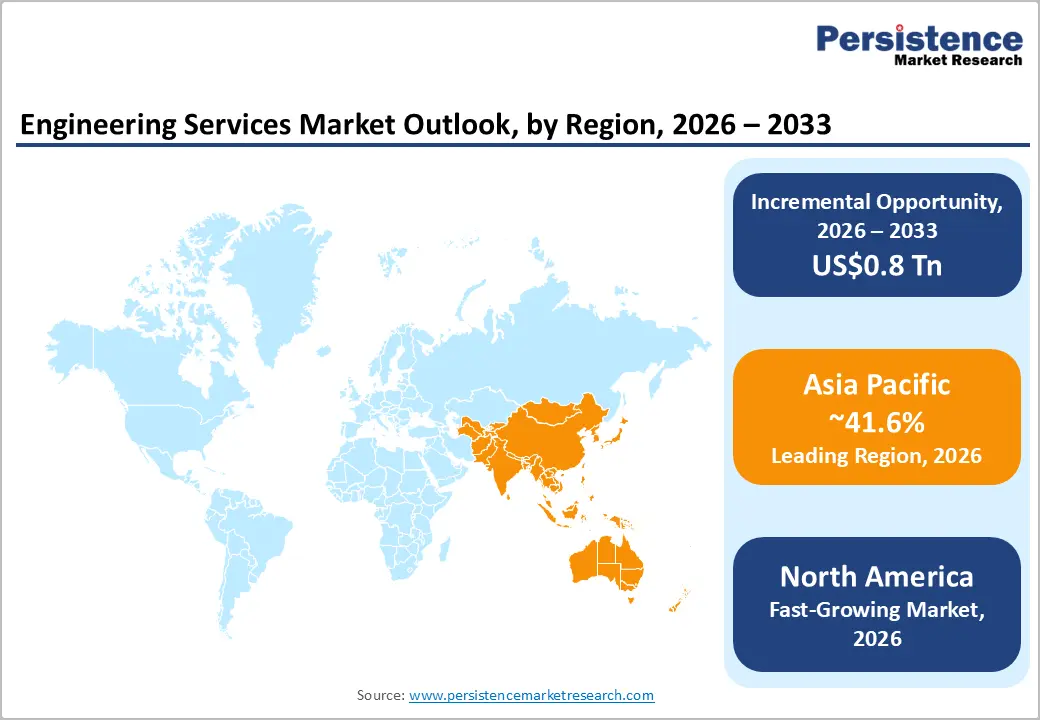

- Leading Region: Asia Pacific, with about a 41.6% share in 2026, as it blends low-cost engineering talent with large-scale manufacturing networks.

- Fast-growing Region: North America, backed by increasing investments in AI, semiconductor design, and defense engineering.

DRO Analysis

Driver - Emergence of Industrial IoT and Digital-Twin

Industrial IoT and digital twin technologies are pushing manufacturers to hire specialized engineering service providers. Plants require engineers who can build sensor networks, feed live data into virtual asset replicas, and run predictive diagnostics. At Hannover Messe 2025, EDAG Engineering demonstrated a multi-layered factory twin built on NVIDIA Omniverse, combining real-time data, simulation, and generative AI. It further enables AI-guided maintenance and virtual operator training.

Siemens also strengthened its position in this field by acquiring Altair Engineering for US$10 billion in March 2025. These moves show that digital-twin rollouts are no longer pilot projects. But they require full engineering teams for integration, calibration, and ongoing operations. A latest study found that 92% of businesses using digital twins reported returns above 10%, making the ROI case strong enough to unlock sustained outsourcing demand.

Expansion of Cities to Fuel Civil Engineering Demand

Rapid urban population growth is compelling governments to commission large-scale infrastructure projects, including roads, transit networks, water systems, and smart city grids, that require extensive civil engineering services. The U.S. Infrastructure Investment and Jobs Act has already announced over 66,000 projects across all 50 states, spanning highways, bridges, transit systems, ports, and pipelines. Emerging economies are equally active.

India's National Investment Pipeline earmarks US$1.4 trillion for infrastructure covering renewable energy, roads, urban development, and railways. In China, urbanization is boosting projects such as Xiong'an New Area and the Greater Bay Area, creating sustained demand for construction and public works. These projects require niche engineering expertise, right from geotechnical analysis to smart grid design, which local governments mainly source from specialized service firms.

Restraint - Data Security Barriers to Hamper Defense Work Outsourcing

Defense agencies are reluctant to outsource engineering tasks when sensitive intellectual property is at stake. The core problem is regulatory overlap. The International Traffic in Arms Regulations (ITAR) rules explicitly prohibit foreign support personnel from accessing in-scope data. Outsourcing IT to foreign nations risks ITAR violations if it allows system administrator access to protected technical information. Compliance requirements have also become strict.

The CMMC 2.0 final rule became effective in December 2024, and CMMC requirements began appearing in DoD contracts starting in November 2025. It raised the certification bar for any third-party engineering partner. In December 2025, the DOJ settled with Swiss Automation Inc., an Illinois-based machining firm, for inadequately protecting technical drawings for DoD parts. This shows that enforcement is now reaching subcontractors and small-scale suppliers. Until vendors can reliably demonstrate the protection of classified data, defense outsourcing will likely remain limited.

Opportunity - Launch of Autonomous and High-Speed Weapons Programs

Military investment in drone systems and hypersonic weapons is creating demand for engineering firms with expertise in aerodynamics, propulsion, and materials science- skills that are scarce inside government agencies. The Defense Advanced Research Projects Agency’s (DARPA) ANCILLARY drone program completed flight testing in summer 2025 and is being transitioned to U.S. military services by the end of 2025, demonstrating how quickly development cycles are moving.

On the hypersonic side, DARPA announced the NextRS program in February 2025 to develop a large and reusable hypersonic bomber prototype capable of multi-mission strike and ISR operations. DARPA also requested US$38 million for its Glide Breaker hypersonic intercept program in FY2025, while the Navy and Army are co-developing a common hypersonic glide body. These programs require test infrastructure, thermal protection engineering, and guidance system design. To complete these tasks, specialized engineering service providers are increasingly being contracted.

Clean Energy Mega-Projects to Create New Engineering Niches

The global push toward clean energy is generating complex and large-scale projects in hydrogen production and carbon capture. Both of these demand engineering services that go well beyond conventional plant design. The U.S. DOE's 2024 Hydrogen Program Plan outlines Regional Clean Hydrogen Hubs and a Hydrogen Shot goal. Clean hydrogen is producible via renewables, nuclear, and fossil fuels integrated with CCUS.

Private investment is following. The Abu Dhabi National Oil Company took a final investment decision on a 1.5 million metric ton per year CCUS project, while the Stratos direct air capture plant in Texas targeted operations in mid-2025. In June 2024, Baker Hughes was among six firms selected by the U.S. DOE to design hydrogen systems converting waste feedstock into clean energy. Each project involves electrolyzer sizing, CO2 pipeline routing, subsurface storage design, and process integration. These are specialized engineering scopes that are consistently outsourced to third-party service providers.

Category-wise Analysis

Service Type Insights

The design and development segment is predicted to lead with a share of approximately 30.5% in 2026, as it sits at the core of product development and innovation cycles. Every industry, right from automotive to semiconductors, now depends on continuous product upgrades, short development timelines, and digital-first engineering. Companies are outsourcing design work to reduce time-to-market and access advanced tools such as digital twins and simulation. For instance, the European Commission funded multiple digital twin initiatives under Horizon Europe to support product design in manufacturing and energy systems. It shows how design has moved from basic drafting to high-value and software-based engineering.

Specialized engineering services are projected to be the fastest-growing segment over the forecast period, as industries become more complex and regulated. Standard engineering support is no longer enough in sectors such as aerospace, healthcare devices, and semiconductors. These industries require deep expertise in areas such as certification, safety compliance, embedded systems, and chip design. For example, the U.S. Food and Drug Administration (FDA) requires strict validation for medical devices, which has increased demand for specialized engineering validation services.

Application Insights

The environmental projects segment is anticipated to dominate, with a share of nearly 38.2% in 2026, as governments enforce strict climate and sustainability targets. Engineering services are heavily used in renewable energy, water treatment, waste management, and carbon capture projects. Several countries have introduced large-scale programs that require engineering expertise. For example, the U.S. Department of Energy has invested billions in clean energy and carbon capture projects under the Bipartisan Infrastructure Law. Such initiatives are raising demand for engineering services in environmental applications more than in traditional sectors.

The technology implementation segment is expected to remain in second place in 2026, as companies shift from planning to executing digital transformation. Earlier, firms focused on consulting and strategy. Now, they are investing in actual deployment of technologies such as AI, IoT, cloud, and industrial automation. This requires engineering firms to integrate software with physical systems. For instance, the National Institute of Standards and Technology has highlighted the role of smart manufacturing and industrial IoT in improving productivity in the U.S. manufacturing sector.

It exhibits that companies are no longer experimenting with technology. They are expanding it, which augments demand for implementation services.

Regional Insights

Asia Pacific Engineering Services Market Trends

Asia Pacific is anticipated to dominate in 2026 with a share of nearly 41.6%, as it combines large-scale manufacturing with superior engineering talent and cost efficiency. Countries such as China, India, and Japan act as global production and engineering hubs. This creates constant demand for design, testing, and product engineering services. Governments are also investing in advanced industries. For example, China’s Made in China 2025 policy focuses on robotics, aerospace, and semiconductors.

India’s Production Linked Incentive schemes are boosting electronics and automotive manufacturing. According to Asian Development Bank, Asia accounts for over half of global manufacturing output, which supports engineering services demand across sectors.

China Engineering Services Market Trends

China’s growth outlook remains steady due to its push toward high-end manufacturing and technological self-reliance. The government is investing heavily in semiconductors, EVs, and industrial automation. For instance, the country produced over 9 million electric vehicles in 2023, as per data from the China Association of Automobile Manufacturers. This expansion requires continuous engineering support in battery systems, software, and design. At the same time, local firms are reducing their dependence on foreign technology, thereby increasing demand for domestic engineering capabilities.

India Engineering Services Market Trends

India is faring well as a global hub for engineering outsourcing and innovation. The country has a large pool of engineers and superior IT capabilities. This allows firms to deliver both traditional engineering and digital engineering services. Over 1,500 Global Capability Centers are operating in India, according to NASSCOM. Companies such as Airbus and Bosch have extended their engineering centers in cities, including Bengaluru. India is also gaining traction in semiconductor design and EV software, supported by government incentives and start-up activity.

North America Engineering Services Market Trends

North America will likely capture nearly 26.8% share in 2026 and become the fastest-growing market, spurred by significant investment in novel technologies and reshoring efforts. The region is focusing on AI, defense, clean energy, and semiconductor manufacturing. For instance, the U.S. Department of Commerce is supporting domestic chip production through the CHIPS and Science Act. This is augmenting demand for engineering services in plant design, automation, and equipment integration. Companies are also modernizing legacy systems, which increases the demand for engineering support.

U.S. Engineering Services Market Trends

The U.S. is faring steadily due to its leadership in innovation and research and development-driven industries. It hosts leading players in aerospace, defense, and digital engineering. Agencies such as NASA and the U.S. Department of Energy are funding advanced engineering projects in space systems, clean energy, and hydrogen technologies. Private firms are also investing in AI-supported engineering and software-defined products. This keeps demand high for both design and implementation services.

Europe Engineering Services Market Trends

In 2026, a share of approximately 18.4% is expected to be held by Europe, backed by its focus on sustainability, industrial automation, and regulatory compliance. The region is investing in green energy, smart manufacturing, and mobility transformation. The European Commission is funding projects under the Green Deal and Horizon Europe programs. These initiatives require engineering expertise in areas such as renewable energy systems, carbon reduction technologies, and smart infrastructure. Strict regulations also increase demand for compliance-driven engineering services.

U.K. Engineering Services Market Trends

The U.K. is seeing decent growth due to investments in clean energy, aerospace, and digital engineering. The government is promoting offshore wind, hydrogen, and net-zero infrastructure projects. For example, the U.K. Department for Energy Security and Net Zero is supporting large-scale renewable projects. The country also has a well-established aerospace hub, which propels demand for specialized engineering services. Growth in fintech and digital sectors is further increasing the demand for technology-backed engineering solutions.

Germany Engineering Services Market Trends

Germany’s growth is supported by its well-established industrial base and leadership in Industry 4.0. The country is modernizing factories with automation, IoT, and digital twins. According to Fraunhofer Society, local manufacturers are investing heavily in smart production systems to improve efficiency. The automotive sector is also shifting toward EVs and software-defined vehicles. It increases demand for engineering services in electronics and software integration.

Competitive Landscape

The global engineering services market is moderately fragmented. However, the top tier is becoming more consolidated through acquisitions, AI-led capability expansion, and domain-focused specialization. Companies such as Tata Consultancy Services, Infosys, HCLTech, Wipro, and Capgemini Engineering continue expanding as global manufacturers increasingly want integrated engineering plus software capabilities from a single vendor. India-based providers collectively control nearly 35 to 40% of offshore engineering outsourcing revenue due to their expandability, pricing flexibility, and superior engineering talent base.

The market is also seeing a wave of consolidation. Large-scale firms are acquiring specialized engineering companies to strengthen expertise in AI, mobility engineering, semiconductor design, industrial IoT, and autonomous systems. Another key competitive shift is the rise of Global Capability Centers (GCCs). Instead of fully outsourcing engineering work, multinational firms are building their own engineering hubs in India, Poland, and Eastern Europe. Companies with expertise in aerospace certification, semiconductor validation, industrial robotics, medical devices, or energy infrastructure are securing premium contracts.

Key Industry Developments:

- In January 2026, Parsons Corporation acquired Altamira Technologies Corporation in a transaction valued at up to US$375 million. The deal would extend Parsons’ capabilities in the U.S. Intelligence Community and Department of Defense, with Altamira projected to generate over US$200 million in revenue in 2026.

- In December 2025, WSP Global announced a US$3.3 billion acquisition of TRC Companies. WSP stated the deal would create the number one Power and Energy platform in the U.S. and make WSP the largest engineering and design firm in the country by revenue.

- In March 2025, Arcadis acquired WSP Infrastructure Engineering GmbH, a Germany-based engineering firm with 160 specialists in rail infrastructure, signaling, structural engineering, and software development. The acquisition would create new revenue opportunities through Deutsche Bahn framework agreements and support smooth project delivery backed by Arcadis's global engineering centers.

Companies Covered in Engineering Services Market

- STRABAG SE

- Jones Lang LaSalle Incorporated

- Balfour Beatty Inc.

- Kiewit Corporation

- AECOM Engineering company

- NV5 Global, Inc.

- Barton Malow

- Brasfield & Gorrie LLC

- Nearby Engineers

- RMF Engineering Inc.

- Bechtel Corporation

- Gilbane Building Company

- WSP Global Inc.

- Jacobs Engineering Group

Frequently Asked Questions

The global engineering services market is projected to be valued at US$1.9 trillion in 2026.

The market is expected to reach US$2.7 trillion by 2033.

Key market trends include AI-led engineering, rise of Global Capability Centers, and increasing demand for software-defined products.

Design and development is expected to be the leading service type with a share of nearly 30.5% in 2026, as firms increasingly co-create products with engineering partners.

The market is expected to grow at a CAGR of 5.2% from 2026 to 2033.

STRABAG SE, Jones Lang LaSalle Incorporated, Balfour Beatty Inc., and Kiewit Corporation are a few key market players.