- Transportation & Logistics

- Asphalt Pavers Market

Asphalt Pavers Market Size, Share, and Growth Forecast 2026 - 2033

Asphalt Pavers Market by Product Type (Screeds; Tracked Asphalt Pavers; Wheeled Asphalt Pavers; Compact Asphalt Pavers; Specialized / Hybrid Pavers), by Technology (Mechanical Pavers, Hydraulic Pavers, Semi-Autonomous Pavers), by Application, by End-User, by Regional Analysis, 2026 - 2033

Asphalt Pavers Market Size and Trend Analysis

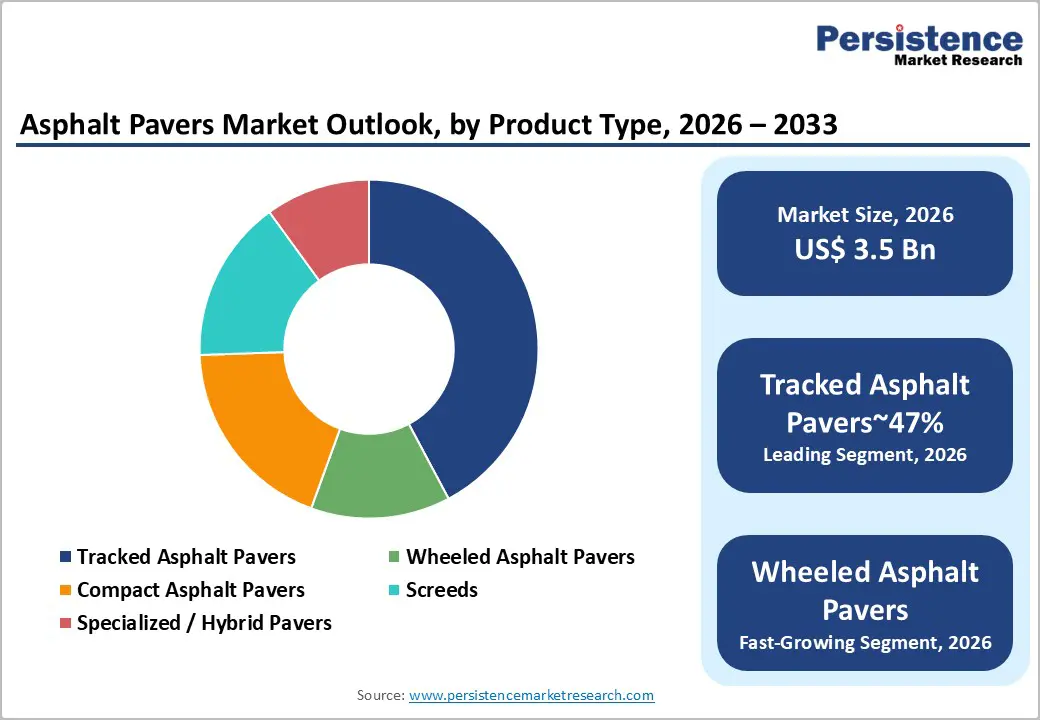

The global asphalt pavers market size is likely to be valued at US$ 3.5 billion in 2026 and is expected to reach US$ 5.2 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033.

Accelerating global infrastructure investment, rising government allocations toward highway modernization and urban road rehabilitation, and the rapid adoption of hydraulic and semi-autonomous paving technologies are the primary forces propelling market growth.

Key Industry Highlights:

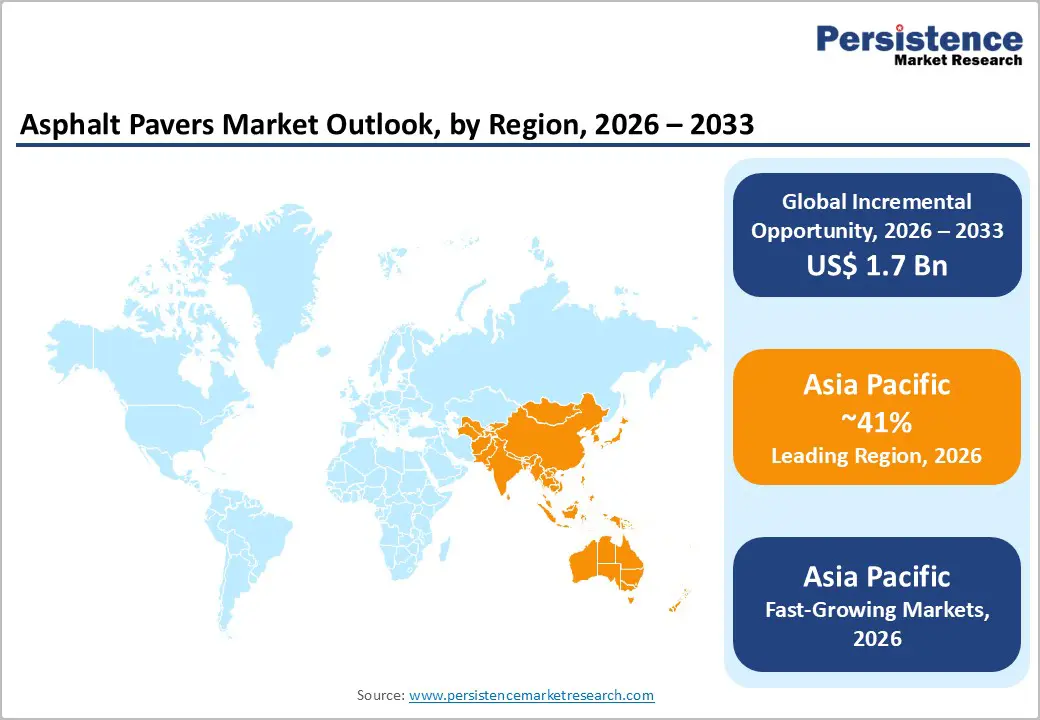

- Leading Region: Asia Pacific leads the global market, accounting for a 41% share, anchored by China's expressway network expansion to 461,000 km by 2035, India's Bharatmala highway program, and Japan's ongoing expressway rehabilitation investment maintaining dominant regional demand.

- Dominant Product Segment: Tracked asphalt pavers dominate with approximately 47% product type revenue share, preferred for high-volume highway and expressway construction due to superior traction, wide screed capability, and the ability to maintain consistent paving speed under heavy load conditions.

- Fastest Growing Segment: Semi-Autonomous pavers represent the fastest growing technology sub-segment, as GPS-guided 3D machine control and intelligent screed systems deliver superior mat quality, reduced operator dependency, and compliance with quality management documentation mandates in public tender specifications.

- Key Opportunity: Airport runway expansion and rehabilitation programs represent a high-value niche opportunity, with FAA's Airport Improvement Program allocating over US$ 3 billion annually and IATA projecting 7.8 billion air passengers by 2036 driving sustained global runway pavement investment.

| Key Insights | Details |

|---|---|

| Asphalt Pavers Market Size (2026E) | US$ 3.5 Billion |

| Market Value Forecast (2033F) | US$ 5.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 4.6% CAGR |

DRO Analysis

Drivers - Unprecedented Public Infrastructure Investment Driving Global Road Construction Activity

Government spending on road and highway infrastructure is currently at record levels, creating strong and sustained demand for asphalt pavers across major regions. In the United States, the Infrastructure Investment and Jobs Act (IIJA) allocated nearly US$ 110 billion for roads, bridges, and large infrastructure projects over five years starting in 2022, marking the largest federal investment in decades.

The European Union’s Cohesion Fund and Trans-European Transport Network program are directing hundreds of billions of euros toward transport development through 2030. In Asia, China’s 14th Five-Year Plan aims to build over 300,000 km of highways and rural roads. These large-scale investments are significantly boosting demand for both tracked and wheeled asphalt pavers, ensuring consistent equipment utilization and long-term growth opportunities for manufacturers across global markets.

Accelerating Road Rehabilitation and Maintenance of Aging Infrastructure Networks

In addition to new road construction, the growing need to repair and upgrade aging infrastructure in North America and Europe is creating steady demand for asphalt pavers. The American Society of Civil Engineers (ASCE) rated U.S. road infrastructure as “D” in its 2021 report, noting that 43% of roads are in poor or mediocre condition, with a maintenance backlog exceeding US$ 786 billion.

The European Road Federation (ERF) emphasizes the urgent need for increased investment in road maintenance to meet safety and quality standards. Rehabilitation projects often require compact and wheeled pavers that can operate efficiently in urban areas and deliver precise paving results. This trend is driving demand for specialized resurfacing equipment and ensuring a continuous replacement cycle, making maintenance activities a stable and recurring revenue source for asphalt paver manufacturers.

Restraints - High Capital Cost and Financing Barriers for Equipment Acquisition

Asphalt pavers, especially advanced tracked models equipped with extendable screeds, GPS-based grade control, and telematics systems, require substantial capital investment. Premium machines from leading manufacturers such as Caterpillar Inc., Volvo Construction Equipment, and Wirtgen Group typically range between US$ 250,000 and US$ 800,000 per unit.

These high costs create a significant barrier for small and medium-sized contractors, particularly in markets where project availability is inconsistent and equipment utilization varies seasonally. Additionally, rising interest rates have increased financing costs, making it more difficult for contractors to invest in new machinery. As a result, many companies delay purchases, rely on rentals, or extend the life of existing equipment, which directly affects new equipment sales and slows overall market growth in certain regions and customer segments.

Volatility in Bitumen and Raw Material Prices Impacting Pavement Laying Activity

The usage of asphalt pavers is closely linked to the availability and cost of asphalt mix, which largely depends on bitumen prices derived from crude oil. These prices are highly volatile, as shown by fluctuations of over 50% between 2020 and 2023 according to the International Energy Agency (IEA).

When bitumen prices rise sharply, the cost of road construction projects increases, leading governments and contractors to delay or reduce project volumes. This directly impacts the utilization rates of asphalt pavers and reduces demand for new equipment. In addition, uncertainty in raw material costs makes project planning more challenging for contractors, often leading to cautious investment decisions. Such volatility not only affects short-term equipment demand but also slows fleet expansion and replacement cycles across the industry.

Opportunities - Semi-Autonomous and GPS-Integrated Paving Technology Creating Premium Equipment Demand

The shift toward semi-autonomous and intelligent paving systems is creating a major growth opportunity in the asphalt pavers market. Modern pavers now use advanced 3D machine control systems powered by GPS and Total Station technology to automatically adjust screed height, slope, and layer thickness. This reduces dependence on operator skill while improving paving accuracy, surface quality, and fuel efficiency.

Leading companies like Wirtgen Group and Caterpillar Inc. are actively developing such technologies through platforms like WITOS PaveDocs and Cat Grade. As governments increasingly require digital quality tracking and precise construction standards, contractors are adopting these advanced systems to stay competitive in tenders. This trend is driving demand for high-value, technologically advanced pavers and is expected to support premium segment growth over the coming years.

Airport Runway Expansion and Rehabilitation Programs Driving Specialized Paver Demand

The rapid growth of global air travel is creating strong demand for specialized asphalt pavers used in airport runway and taxiway construction. The International Air Transport Association (IATA) expects global passenger traffic to reach 7.8 billion by 2036, requiring expansion of airport infrastructure worldwide. Runway construction demands highly precise paving equipment capable of delivering smooth, durable, and high-density surfaces that meet strict aviation standards set by authorities such as the FAA and ICAO. These projects require pavers with wide screeds, advanced grade control systems, and consistent material handling capabilities. In the United States, the Federal Aviation Administration’s Airport Improvement Program (AIP) invests over US$ 3 billion annually in airport infrastructure. This creates a strong and consistent demand for specialized pavers, making the aviation sector an important niche growth area for manufacturers.

Category-wise Analysis

By Product Type Insights

Tracked asphalt pavers are the leading product type in the global market, accounting for approximately 47% of total revenue. These machines are widely used in large-scale highway and expressway construction due to their strong traction on uneven or soft surfaces. They also offer better paving width capabilities and maintain consistent speed even under heavy loads.

Their lower ground pressure minimizes damage to freshly prepared road bases, making them ideal for high-quality construction projects such as highways and airport runways. Major manufacturers including Caterpillar Inc., Volvo Construction Equipment, and Wirtgen Group (Vögele brand) dominate this segment by offering advanced and reliable tracked pavers. Their strong presence in government and large infrastructure projects further strengthens this segment’s leadership, ensuring continued demand across global markets.

By Technology Insights

Hydraulic pavers dominate the technology segment, accounting for around 58% of total revenue. These systems provide better control, smoother power transmission, and greater flexibility compared to traditional mechanical systems. Hydraulic technology allows precise control of paving speed in relation to material flow, which is essential for maintaining consistent surface quality and preventing defects such as material segregation.

This makes hydraulic pavers highly suitable for a wide range of applications, from highways to urban roads. Leading manufacturers such as Dynapac, Bomag GmbH, and Ammann Group have largely transitioned to hydraulic systems across their product lines. Additionally, hydraulic platforms support integration with advanced technologies such as automation and telematics, further strengthening their dominance. Semi-autonomous hydraulic pavers are emerging as the fastest-growing sub-segment within this category.

By Application Insights

Highways and expressways represent the largest application segment, contributing approximately 43% of total market revenue. These projects involve long-distance paving, high material volumes, and strict quality requirements, making them ideal for large, high-capacity tracked pavers with extendable screeds. Government infrastructure programs across the world are heavily focused on expanding and maintaining national highway networks.

In the United States, the Federal Highway Administration (FHWA) directs a significant portion of its funding toward interstate and national highways. These projects require consistent paving quality, high productivity, and reliable equipment performance. As a result, contractors prefer premium asphalt pavers for such applications. The continuous investment in highway infrastructure ensures steady demand for advanced paving equipment in this segment.

By End-user Insights

Government and public infrastructure agencies are the largest end users in the asphalt pavers market, accounting for around 51% of total demand. These agencies include national highway authorities, state and local road departments, and municipal public works organizations. They play a key role in issuing contracts for road construction and maintenance, often specifying equipment standards, paving requirements, and quality benchmarks in tender documents.

Procurement is carried out through direct purchases, framework agreements, or public-private partnership (PPP) models. According to the World Bank, developing countries alone require around US$ 1 trillion annually for transport infrastructure investment. This highlights the strong and ongoing dependence on public sector spending. As a result, government agencies continue to act as the primary demand drivers, ensuring long-term market stability.

Regional Insights

North America Asphalt Pavers Market Trends

North America is a major market for asphalt pavers, driven primarily by large-scale infrastructure investments in the United States. The Infrastructure Investment and Jobs Act (IIJA) has allocated US$ 110 billion for road and bridge development, creating a strong pipeline of construction and maintenance projects across all states. This has significantly increased demand for both new equipment and rental fleets.

Domestic manufacturers such as Caterpillar Inc., LeeBoy, and Roadtec Inc. benefit from favorable policies like Buy America provisions. In addition, agencies like the Federal Highway Administration (FHWA) promote the use of advanced paving technologies to improve quality and efficiency. Canada’s Investing in Canada Plan also supports infrastructure development at provincial and municipal levels. A strong rental market, supported by companies like United Rentals and Sunbelt Rentals, further enhances equipment availability and aftermarket services.

Europe Asphalt Pavers Market Trends

Europe represents a mature but highly innovative market for asphalt pavers, with Germany serving as a key hub for advanced equipment manufacturing. Leading companies such as Wirtgen Group and Bomag GmbH are based in the region and drive technological advancements. The European Union’s TEN-T program supports the development of major transport corridors, ensuring consistent demand for paving equipment.

Countries like France and Spain invest heavily in maintaining and upgrading their motorway networks. In the United Kingdom, the Road Investment Strategy (RIS2) has committed over £27 billion for road improvements. Environmental regulations in Europe are also encouraging the adoption of low-emission and electric paving equipment. Companies like Dynapac and Ammann Group are introducing electric and hybrid models, especially for urban applications, supporting the region’s focus on sustainability and innovation.

Asia Pacific Asphalt Pavers Market Trends

Asia Pacific is the largest and fastest-growing market for asphalt pavers, driven by rapid infrastructure development in countries like China, India, and Southeast Asia. China’s National Highway Network Plan aims to expand its expressway network to 461,000 km by 2035, creating long-term demand for paving equipment. India’s Bharatmala Pariyojana program is also significantly boosting highway construction activity.

Government initiatives and consistent project pipelines are supporting strong equipment demand. Domestic manufacturers such as SANY, XCMG, and Zoomlion are becoming increasingly competitive by offering cost-effective solutions and improving product quality. In addition, countries like Japan continue to invest in road maintenance and resilience upgrades, while ASEAN nations such as Vietnam, Indonesia, and the Philippines are expanding their transport infrastructure. This makes Asia Pacific a key growth engine for the global asphalt pavers market.

Competitive Landscape

The global asphalt pavers market is moderately consolidated, particularly in the premium segment. Leading companies such as Wirtgen Group, Caterpillar Inc., Volvo Construction Equipment, Dynapac, and Bomag GmbH hold a significant share due to their strong product portfolios and global presence. These companies compete based on advanced technology, including screed systems, telematics, and machine control solutions, along with strong dealer and service networks. Their established relationships with government agencies also strengthen their market position.

In contrast, the mid-range and value segments are more fragmented, with Chinese manufacturers like SANY, XCMG, and Zoomlion expanding rapidly in international markets. Key industry trends include the adoption of electric screed heating, integration of telematics services, and a growing focus on aftermarket support and service offerings, which are becoming important revenue streams for manufacturers.

Key Developments:

- In February 2025, Wirtgen Group showcased multiple innovations at bauma 2025, highlighting advanced paving technologies, automation systems, and digital solutions. These developments focused on improving paving precision, efficiency, and sustainability through smart automation and integrated performance tracking systems.

- In October 2024, Caterpillar Inc. expanded the availability of its Cat Grade 3D paving control system across its AP Series pavers, enabling automated grade and slope adjustments. This enhances paving accuracy, reduces operator dependency, and improves productivity in highway resurfacing applications.

- In April 2023, Dynapac advanced its paving technology portfolio with innovations in screed systems and efficient machine design, including options for electric heating and improved fuel efficiency. These developments support compliance with emission standards while enhancing operational performance in road construction.

Companies Covered in Asphalt Pavers Market

- Caterpillar Inc.

- Volvo Construction Equipment

- Wirtgen Group (Vögele)

- Dynapac

- Bomag GmbH

- Ammann Group

- Fayat Group

- SANY Group

- XCMG Group

- Zoomlion Heavy Industry Science and Technology Co., Ltd.

- Sumitomo Construction Machinery

- LeeBoy

- Roadtec Inc.

- Sakai Heavy Industries, Ltd.

- Weiler

- Terex Corporation

- Hanta Machinery Co., Ltd.

- Shantui Construction Machinery Co., Ltd.

Frequently Asked Questions

The global Asphalt Pavers Market is valued at US$ 3.5 Billion in 2026 and is projected to reach US$ 5.2 Billion by 2033, growing at a CAGR of 5.9% over the forecast period from 2026 to 2033.

The primary growth drivers are unprecedented public infrastructure investment, most notably the U.S. Infrastructure Investment and Jobs Act (IIJA) allocating US$ 110 billion for roads and bridges, and the critical need to rehabilitate aging road networks, with the ASCE estimating a U.S. road maintenance backlog exceeding US$ 786 billion.

Tracked Asphalt Pavers lead the product type segment with approximately 47% market share, driven by their superior traction, high-output paving capability, and suitability for large-scale highway and expressway construction, the dominant application category globally.

Asia Pacific is the leading region, driven by China's expressway network expansion targeting 461,000 km by 2035, India's Bharatmala Pariyojana highway program, and ASEAN nations' rapidly expanding road infrastructure investment pipelines.

The most significant opportunity is the transition to semi-autonomous and GPS-integrated paving systems. As public agencies mandate digital quality documentation and mat quality standards, contractors equipped with intelligent 3D machine control pavers gain competitive advantages, driving sustained premium equipment demand through 2033.

Leading companies include Wirtgen Group (Vögele), Caterpillar Inc., Volvo Construction Equipment, Dynapac, Bomag GmbH, Ammann Group, SANY Group, XCMG Group, LeeBoy, Roadtec Inc., and Sumitomo Construction Machinery, among others.