- Automotive Components & Materials

- AdBlue Market

AdBlue Market Size, Share, and Growth Forecast, 2026 - 2033

AdBlue Market by Vehicle Type (Commercial Vehicles, Passenger Cars, Others), Packaging Type (Bulk Storage/IBC Containers, Drums, Others), Formulation Type, Technology Type, and Regional Analysis 2026 - 2033

AdBlue Market Size and Trends Analysis

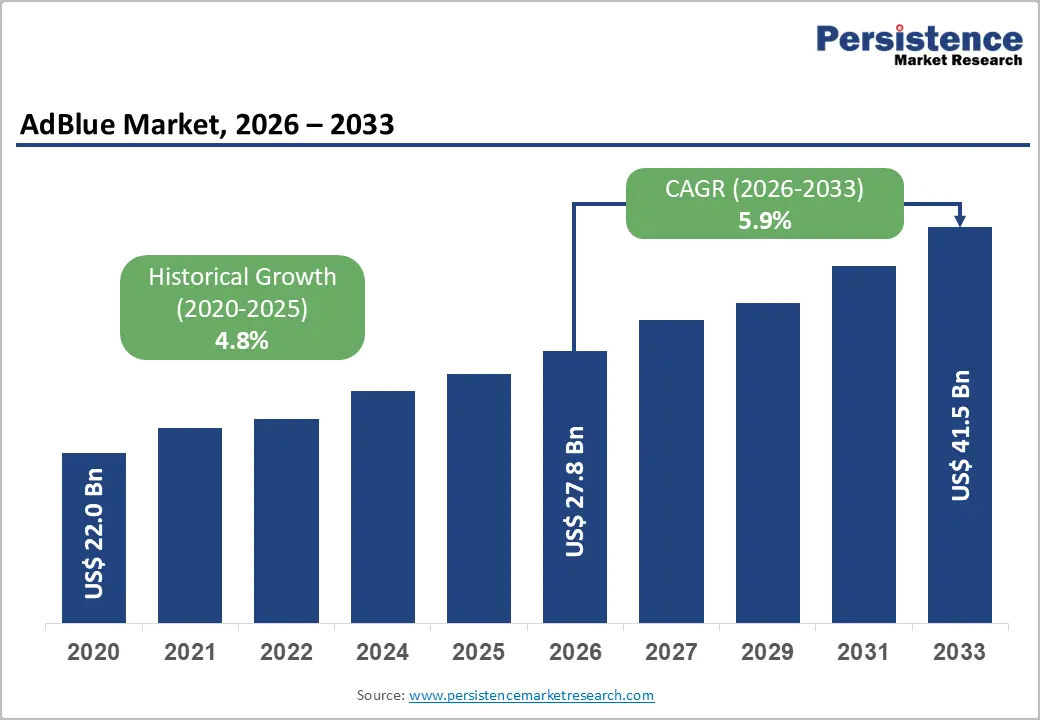

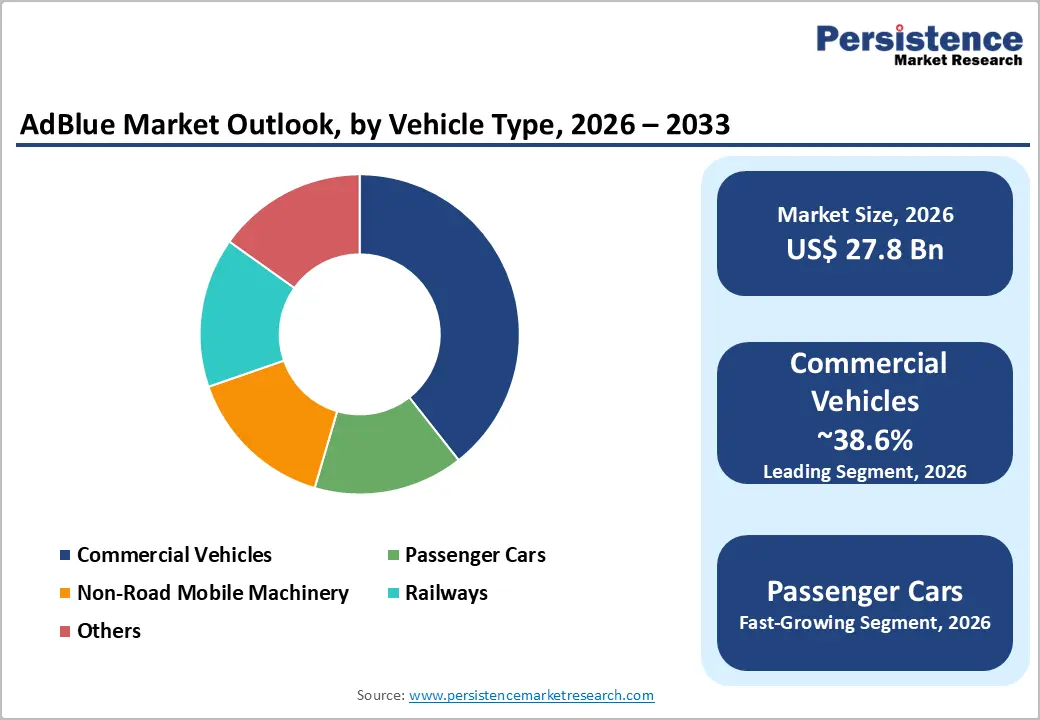

The global AdBlue market size is likely to be valued at US$ 27.8 billion in 2026 and is expected to reach US$41.5 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033, driven by the continued reliance on diesel-powered commercial transport and the enforcement of stringent NOx emission standards across major economies.

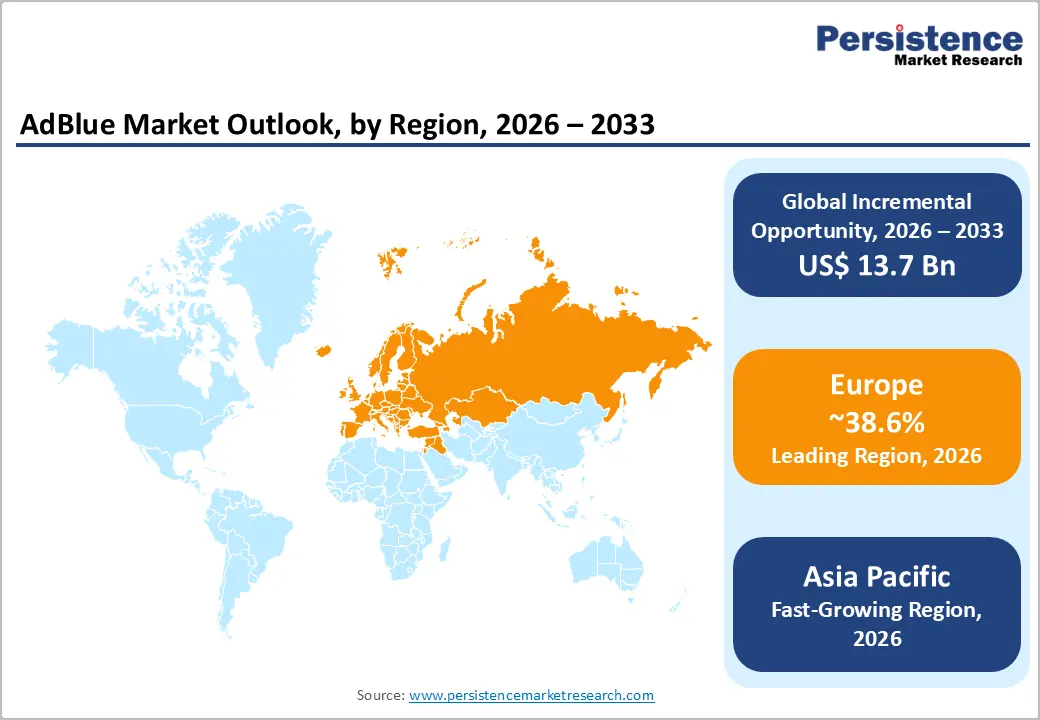

Regulatory compliance requirements are sustaining steady demand for Selective Catalytic Reduction (SCR) systems and associated fluids. Europe leads in market share, while Asia Pacific represents the fastest-growing region, driven by regulatory convergence and expanding logistics infrastructure.

Key Industry Highlights:

- Leading Region: Europe remains the leading region, accounting for 38.6% of the market share, supported by a mature diesel fleet, strict emission regulations, and well-established bulk distribution infrastructure.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, driven by regulatory frameworks such as China VI and BS VI, along with rising freight activity and industrialization.

- Investment Plans: Industry investments are increasingly focused on low-carbon AdBlue production, bulk storage infrastructure, and digital supply chain systems, with leading players allocating capital toward renewable-based ammonia production and telemetry-enabled distribution networks.

- Dominant Vehicle Type: The commercial vehicles segment is expected to dominate with an anticipated 62.7% market share, driven by high diesel use in trucks, buses, and heavy-duty transport applications that require continuous AdBlue consumption.

- Leading Packaging Type: Bulk storage and IBC containers are projected to lead with an anticipated 56.3% share, as they offer cost efficiency, operational scalability, and reliability for large fleet operators and industrial users.

DRO Analysis

Driver - Regulatory Pressure is Sustaining Mandatory SCR/DEF Consumption

AdBlue demand is fundamentally driven by emissions regulations that mandate the use of SCR systems in diesel vehicles. In the United States, environmental regulations require DEF-equipped vehicles to comply with strict NOx emission thresholds, supported by onboard diagnostics and anti-tampering systems. In Europe, the transition from Euro 6 to Euro 7 standards is tightening permissible limits for NOx, particulate matter, carbon monoxide, and ammonia emissions.

Similarly, China VI and India’s Bharat Stage VI (BS VI) standards are reinforcing SCR adoption across both commercial and passenger diesel vehicles. These regulatory frameworks create a non-discretionary demand environment in which AdBlue consumption is directly linked to compliance. As vehicle fleets modernize to meet evolving standards, suppliers benefit from consistent demand tied to regulatory cycles rather than economic volatility, ensuring long-term market stability.

Diesel Fleet Persistence in Commercial Transport Keeps Volume Demand Structurally High

Despite advancements in electrification, diesel engines remain dominant in heavy-duty and long-haul transportation segments. Trucks, buses, construction equipment, and agricultural machinery continue to rely on diesel due to energy density, cost efficiency, and infrastructure readiness. A significant majority of heavy-duty vehicles globally still operate on diesel, reinforcing the need for SCR systems and AdBlue consumption. Since AdBlue is a consumable fluid, its demand is recurring and directly proportional to vehicle usage intensity.

High mileage, extended operational cycles, and fleet-based logistics models amplify consumption volumes in commercial segments. Even moderate growth in freight activity or infrastructure development translates into sustained demand for AdBlue. This structural dependence on diesel in commercial applications ensures that AdBlue remains a critical component of emissions compliance across mature and emerging markets.

Restraint - Electrification, Alternative Powertrains, and Feedstock Risk Constrain Long-Run Upside

The primary long-term constraint for the AdBlue market is the gradual transition toward battery-electric vehicles and alternative fuel technologies such as hydrogen and natural gas. While this transition is uneven across regions and vehicle classes, it progressively reduces the total addressable market for diesel-based solutions, particularly in light-duty and urban mobility segments. In parallel, AdBlue production depends on high-purity urea derived from ammonia, exposing manufacturers to fluctuations in natural gas and energy prices.

Supply chain disruptions or input cost volatility can directly impact production economics and pricing stability. Furthermore, strict quality standards and anti-tampering requirements increase operational complexity for suppliers. These factors collectively limit margin expansion and introduce cost pressures, especially in a market where pricing is relatively commoditized.

Opportunity - Low-Carbon AdBlue Can Create A Premium Lane within a Compliance Market

A key growth opportunity lies in developing low-carbon or reduced-emission AdBlue formulations. Manufacturers are increasingly investing in production processes that utilize renewable energy, carbon capture technologies, and sustainable feedstocks to reduce the overall carbon footprint of AdBlue. This shift aligns with the growing emphasis on Scope 3 emissions reporting among logistics providers and industrial operators. Fleet operators are beginning to consider not only tailpipe emissions but also the embedded emissions of consumables used in operations.

Suppliers that can offer certified low-carbon AdBlue while maintaining compliance with ISO quality standards can differentiate themselves in a traditionally commoditized market. This trend is particularly relevant in Europe, where sustainability reporting requirements are more advanced, creating a premium pricing opportunity and stronger customer retention.

Packaging, Dispensing, and Telemetry are Becoming Commercial Differentiators

The AdBlue market is evolving beyond product supply into an integrated distribution and service model. Innovations in packaging, storage, and dispensing systems are enabling suppliers to optimize logistics efficiency and reduce operational costs for end users. Bulk storage solutions with telemetry-enabled monitoring systems allow real-time tracking of inventory levels, minimizing downtime and preventing stockouts for fleet operators.

Lightweight and sustainable packaging formats are also reducing material usage and transportation costs. These advancements are particularly valuable in high-consumption environments such as logistics hubs and industrial fleets. As a result, value creation is shifting toward service integration, where suppliers combine product delivery with digital monitoring, automated refilling, and customized packaging solutions to enhance customer experience and operational efficiency.

Category-wise Analysis

Vehicle Type Insights

Commercial vehicles are expected to dominate, accounting for an anticipated 62.7% share of the market in 2026. This leadership is driven by the high diesel penetration in heavy-duty trucks, buses, and logistics fleets, where SCR systems are standard for emissions compliance. For example, long-haul trucking fleets operated by companies such as DHL Group and FedEx Corporation rely extensively on diesel-powered vehicles, creating continuous AdBlue consumption due to high mileage and operational intensity.

AdBlue usage in this segment is significantly higher because of longer driving distances, heavier loads, and round-the-clock operations. Fleet-based procurement models further strengthen this segment, as bulk purchasing and centralized refilling systems improve cost efficiency and supply reliability. Regulatory enforcement is also stricter for heavy-duty vehicles, ensuring consistent and non-discretionary AdBlue usage.

Passenger cars are likely to be the fastest-growing segment, particularly in regions where diesel passenger vehicles continue to operate under stringent emission standards. Growth is supported by regulatory mandates in Asia Pacific and parts of Europe, where diesel passenger vehicles from manufacturers such as Volkswagen AG and Hyundai Motor Company still incorporate SCR systems to meet emission norms.

While electrification is gradually reducing diesel penetration in this segment, SCR adoption in compliant diesel vehicles continues to drive incremental demand. Other segments, including non-road mobile machinery and railways, contribute to steady but moderate growth. For instance, construction equipment from Caterpillar Inc. and diesel locomotives used by Indian Railways depend on SCR systems, sustaining AdBlue demand in heavy-duty, non-road applications.

Packaging Type Insights

Bulk storage and IBC containers lead the packaging segment, holding an anticipated 56.3% market share of the market. This dominance is attributed to their cost efficiency and suitability for large-scale fleet operations. Bulk systems reduce per-unit distribution costs, streamline refilling processes, and ensure consistent supply for high-volume users such as logistics companies and industrial operators.

For example, large fleet operators often deploy on-site bulk storage solutions supplied by companies like Yara International ASA and GreenChem Holding B.V., which integrate telemetry systems for real-time monitoring and automated replenishment. Centralized storage also enhances quality control, which is critical for maintaining compliance with ISO standards and preventing contamination.

Drums are the fastest-growing packaging type, driven by increasing demand from small and medium-sized fleet operators and service centers. These users require flexible and portable solutions that do not justify investment in bulk storage infrastructure. For instance, regional transport operators and automotive workshops often rely on drum-based supply distributed through networks such as Brenntag AG. Portable containers and dispensers also play a crucial role in retail and rural markets, where accessibility and convenience are key factors.

The market is witnessing a gradual diversification of packaging formats, with suppliers introducing lightweight, recyclable containers and user-friendly dispensing systems. This shift highlights a growing emphasis on flexibility, sustainability, and operational convenience to address varying customer needs across different end-user segments.

Regional Insights

North America AdBlue Market Trends

North America represents a mature and compliance-driven market, characterized by strong regulatory enforcement and a well-established logistics infrastructure.

U.S. AdBlue Market Trends

The U.S. is expected to lead the region, supported by stringent emission standards that mandate the use of SCR systems in diesel vehicles. Demand is heavily concentrated in the commercial vehicle segment, particularly in long-haul trucking and freight distribution. This is reinforced by OEM-level integration, where engine manufacturers such as Cummins Inc. and Paccar Inc. have standardized SCR systems across their heavy-duty vehicle platforms, ensuring consistent AdBlue consumption across fleets.

On the supply side, energy and chemical players such as CF Industries Holdings, Inc. have continued to expand low-carbon ammonia initiatives, strengthening feedstock security for AdBlue production. Fuel retailers like Pilot Company have also expanded DEF dispensing infrastructure across interstate trucking corridors, improving accessibility for fleet operators. These developments collectively enhance supply reliability and distribution efficiency. While electrification is gaining traction in urban delivery fleets, particularly with companies such as Amazon deploying electric delivery vans, the dominance of diesel in long-haul transport ensures sustained AdBlue demand in the medium term, supported by infrastructure depth and regulatory continuity.

Europe AdBlue Market Trends

Europe is expected to be the largest AdBlue market, accounting for 38.6% of market share in 2026, driven by a mature diesel vehicle base and stringent emission regulations. The transition toward Euro 7 standards is further strengthening the regulatory framework, ensuring continued reliance on SCR systems. Countries such as Germany, the U.K., France, and Spain play a critical role in regional demand, supported by extensive freight networks and industrial activity. Major chemical producers like BASF SE have introduced low-carbon AdBlue variants such as ZeroPCF and renewable electricity-based formulations, directly influencing the shift toward sustainable product offerings in the region.

At the distribution level, Yara International ASA and GreenChem Holding B.V. have expanded bulk storage networks and telemetry-enabled supply systems across Western Europe, improving operational efficiency for fleet operators. Logistics providers such as DB Schenker are integrating sustainability targets into procurement, increasing demand for low-carbon consumables like AdBlue. These developments reinforce Europe’s position not only as the largest market but also as the innovation hub for sustainable and high-efficiency AdBlue solutions, with strong alignment between regulatory pressure and corporate decarbonization strategies.

Asia Pacific AdBlue Market Trends

Asia Pacific is expected to be the fastest-growing regional market, with a CAGR of 6.1%, driven by rapid industrialization, expanding transportation networks, and tightening emission regulations. China and India are the primary growth engines, supported by the implementation of China VI and BS VI standards, respectively.

China AdBlue Market Trends

In China, large state-owned enterprises such as China Petroleum & Chemical Corporation (Sinopec) have expanded AdBlue production and retail distribution across fuel stations, improving product accessibility nationwide.

India AdBlue Market Trends

Indian Oil Corporation Limited has scaled up its DEF brand distribution network, ensuring availability across highways and urban centers. Automotive manufacturers such as Tata Motors Limited and Isuzu Motors Limited have incorporated SCR systems across commercial vehicle portfolios to comply with emission standards, directly increasing AdBlue consumption.

The region also benefits from cost advantages in urea and ammonia production, supported by strong domestic chemical industries. Rising freight demand, infrastructure investments, and urbanization further amplify consumption levels. These combined factors position Asia Pacific as the primary growth engine for the global AdBlue market, with strong opportunities in localized production, fleet services, and distribution network expansion.

Competitive Landscape

networks, to maintain a competitive advantage. Market leaders focus on capacity expansion, product innovation, and strategic partnerships to strengthen their position. Smaller regional players compete primarily on pricing and localized supply, contributing to overall market fragmentation.

Key players are prioritizing low-carbon innovation, supply chain integration, and distribution efficiency. Strategies include expanding bulk supply networks, investing in sustainable production technologies, and enhancing customer engagement through digital monitoring solutions. The market is transitioning toward integrated service models that combine product supply with logistics and technology-driven solutions.

Key Industry Developments:

- In February 2026, BASF SE announced the launch of AdBlue® GE (Green Electricity), a new product manufactured entirely using renewable electricity, aimed at reducing CO2 emissions across the mobility value chain while maintaining identical performance to conventional AdBlue. This development will strengthen the shift toward low-carbon AdBlue solutions and support fleet operators in reducing Scope 3 emissions.

Companies Covered in AdBlue Market

- Yara International ASA

- BASF SE

- CF Industries Holdings, Inc.

- OCI N.V.

- GreenChem Holding B.V.

- Shell plc

- TotalEnergies SE

- Eni S.p.A.

- Brenntag AG

- Cummins Inc.

- Indian Oil Corporation Limited

- China Petroleum & Chemical Corporation (Sinopec)

- Mitsui Chemicals, Inc.

- Petronas Chemicals Group Berhad

- Kruse Automotive GmbH & Co. KG

- BlueDEF (Old World Industries)

Frequently Asked Questions

The global AdBlue market is valued at US$27.8 billion in 2026.

The market is projected to reach US$41.5 billion by 2033.

Key trends include the shift toward low-carbon AdBlue formulations, expansion of bulk storage and telemetry-enabled distribution systems, and increasing focus on supply chain integration and sustainability-driven procurement.

The commercial vehicles segment leads the market, accounting for an anticipated 62.7% share, due to high diesel usage in freight, buses, and heavy-duty transport.

The AdBlue market is expected to grow at a CAGR of 5.9% between 2026 and 2033.

Major players include Yara International ASA, BASF SE, Shell plc, CF Industries Holdings, Inc., and TotalEnergies SE.