- Automotive Components & Materials

- Automotive Straps Market

Automotive Straps Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Straps Market by Product Type (Ratchet Straps, Cam Buckle Straps, Bungee Cords, Retractable Straps, Over-Center Lever Straps, Webbing Straps), by Material Type (Polyester, Polypropylene, Nylon, Rayon, Cotton, Metal), by Distribution Channel (OEM, Aftermarket), by Application (Seats & Seating Systems, Cargo Securing, Luggage Systems, Towing, Interior Fastening), by End-Use, by Regional Analysis, 2026 - 2033

Automotive Straps Market Size and Trend Analysis

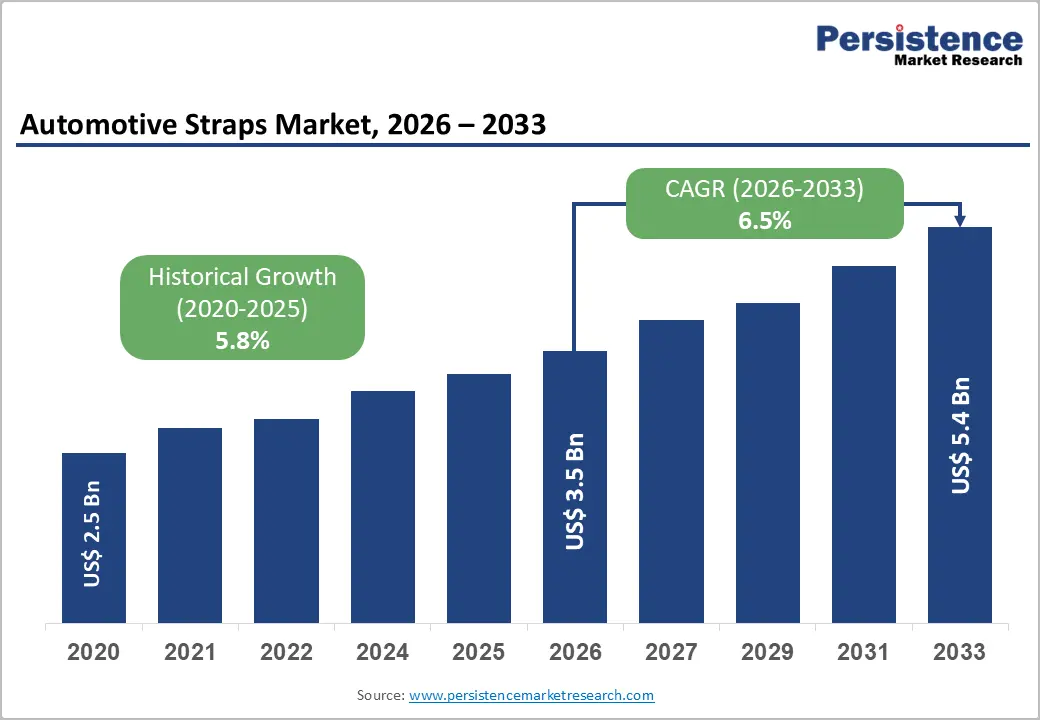

The global automotive straps market size is likely to be valued at US$ 3.5 Billion in 2026 and is expected to reach US$ 5.4 Billion by 2033, growing at a CAGR of 6.5% during the forecast period from 2026 to 2033.

The automotive straps market is experiencing accelerating growth, driven by the expansion of global e-commerce and logistics networks, which are creating surging demand for cargo securing solutions; the growth of the automotive OEM sector, which requires high-performance seat belt webbing and interior restraint systems; and increasingly stringent government regulations mandating the use of load-securing equipment in commercial transport.

Key Market Highlights

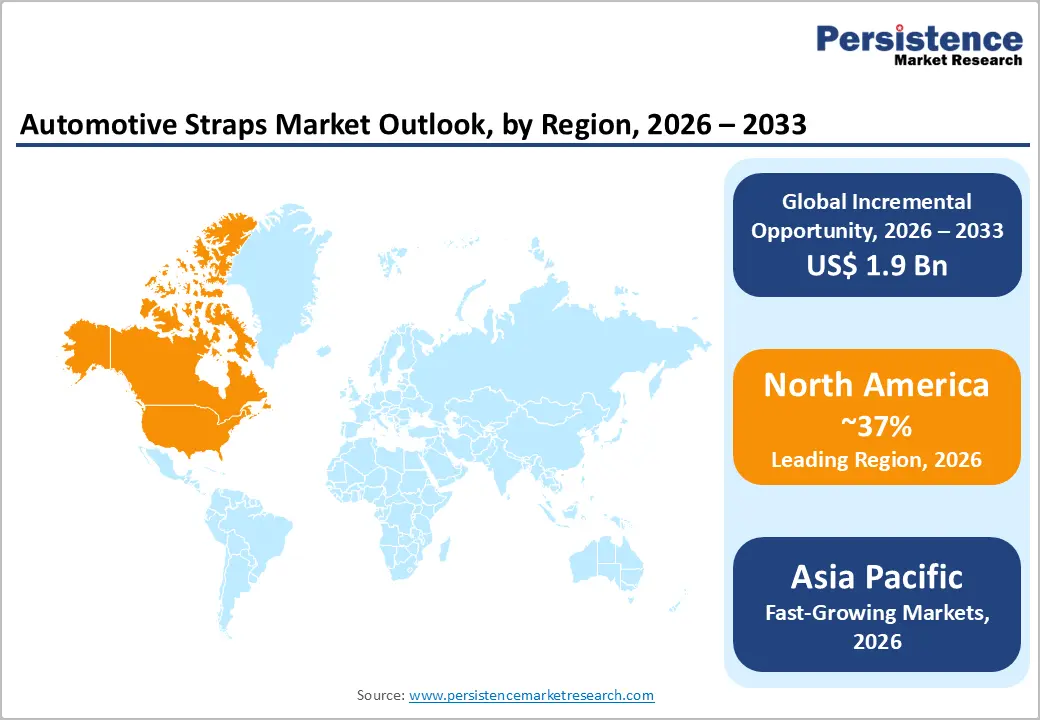

- Leading Region: North America leads the automotive straps market with 37% share, driven by FMCSA’s mandatory 49 CFR Part 393 cargo securing regulations, the U.S.’s 10+ billion tons of annual truck freight, and strong consumer aftermarket demand from the world’s highest per-capita pickup truck ownership base.

- Fastest Growing Region: Asia Pacific is the fastest growing region with a rising CAGR of 8.3%, propelled by China’s world-leading webbing manufacturing base and expanding logistics sector, India’s post-GST organized trucking growth, and ASEAN’s rapidly expanding manufacturing export logistics requiring cargo securing compliance.

- Dominant Segment: Ratchet Straps lead the By Product Type category with approximately 36% market share, as the industry-standard commercial cargo securing solution recognized by FMCSA and EN 12195-2 regulations for meeting required working load limits in professional transport applications.

- Fastest Growing Segment: EV-specific vehicle transport straps within the By Product Type category represent the fastest-growing niche, driven by IEA’s 14 million annual global EV sales, which require specialized wheel-claw and axle strap configurations designed for battery-electric vehicle tie-down point geometries.

- Key Market Opportunity: E-commerce fulfillment fleet cargo control, with ATA reporting 3.5+ million U.S. truck drivers and Amazon/FedEx/UPS/DHL operating millions of delivery vehicles globally, represents a high-volume, high-frequency replacement demand opportunity for fleet-grade strap procurement programs.

| Key Insights | Details |

|---|---|

| Automotive Straps Market Size (2026E) | US$ 3.5 Billion |

| Market Value Forecast (2033F) | US$ 5.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.5% |

| Historical Market Growth (2020 - 2025) | 5.8% |

Market Dynamics

Market Growth Drivers

Global E-Commerce and Logistics Expansion Driving Cargo Securing Demand

The explosive global expansion of e-commerce and organized logistics is generating unprecedented demand for cargo securing equipment, with ratchet straps, webbing straps, and cam buckle straps serving as essential load control tools for last-mile delivery vehicles, long-haul trucks, and intermodal freight operations. The International Transport Forum (ITF) reports that global freight transport volumes are projected to increase by more than 70% between 2015 and 2050, with road freight maintaining the dominant share.

The United Nations Conference on Trade and Development (UNCTAD) documented record global e-commerce sales exceeding US$ 5.5 trillion in 2022, with a significant proportion fulfilled through direct-to-consumer delivery requiring cargo-controlled last-mile vehicles. Regulatory requirements under EN 12195 (European Standard for load restraint) and equivalent national standards mandate specific minimum restraint forces that only certified strapping systems can provide, institutionalizing ratchet and webbing strap procurement throughout the commercial logistics sector globally.

Automotive OEM Seat Belt and Interior Restraint System Growth

Automotive OEMs represent a high-volume, technically demanding source of demand for precision-engineered webbing straps, retractable belt systems, and interior fastening components used in seat belt assemblies, child restraint mounting systems, and vehicle interior organizational systems. Global vehicle production of approximately 90 million units annually, per OICA data, generates consistent OEM strap procurement across passenger cars, commercial vehicles, and off-highway equipment.

Regulatory frameworks, including FMVSS 209 (Federal Motor Vehicle Safety Standard for Seat Belt Assemblies) in the U.S. and ECE R16 in Europe, mandate seat belt performance specifications that require certified high-tenacity polyester and nylon webbing meeting strict elongation, abrasion, and tensile strength requirements. Rising safety regulations for child safety seats and rear-seat passenger protection are expanding the per-vehicle strap content requirement in new vehicle designs.

Market Restraints

Commodity Raw Material Price Volatility

Automotive straps are predominantly manufactured from polyester, polypropylene, and nylon webbing, materials whose production costs are directly linked to petrochemical feedstock prices. The substantial volatility in crude oil and polymer prices, with polypropylene prices fluctuating by over 40% between 2020 and 2023 per ICIS Chemical Business data, creates significant margin pressure for strap manufacturers operating under fixed or semi-fixed OEM supply agreements.

These input cost fluctuations complicate pricing strategies, reduce operating margins, and can force manufacturers to cut product development investment during commodity price spikes, thereby moderating market growth.

Competition from Low-Cost Manufacturers and Quality Fragmentation

The automotive straps market, particularly the aftermarket consumer segment, faces intense price competition from low-cost manufacturers based in China and Southeast Asia, who can undercut established Western brands by 30-60% for comparable product specifications.

This price competition compresses margins for quality manufacturers, limits premium brand pricing power, and raises safety concerns from uncertified products entering the market. The U.S. Consumer Product Safety Commission (CPSC) has documented recalls of substandard load securing straps that fail to meet their rated working load limits, reflecting the quality risks associated with unregulated, low-cost alternatives.

Market Opportunities

Electric Vehicle Logistics and Specialized EV Transport Securing Systems

The rapid growth of the electric vehicle market is creating a specialized and high-value demand opportunity for automotive straps engineered specifically for EV transport, dealership delivery, and auction logistics applications. Electric vehicles, particularly those with large battery packs in skateboard chassis configurations, have different underbody geometry, weight distribution, and tie-down point specifications compared to conventional ICE vehicles, requiring purpose-designed tiedown strap systems.

The IEA reports that global EV sales exceeded 14 million units in 2023, generating growing demand for EV-specific vehicle transport straps from vehicle transporter OEMs and dealership delivery logistics operators. Companies developing EV-optimized strap systems with compatibility documentation for specific EV models, including wheel-claw designs and axle-strap configurations validated for BEV platform tie-down points, can capture premium pricing in this specialized, technically differentiated market segment.

E-Commerce Fulfillment and Last-Mile Delivery Fleet Cargo Control Market

The global expansion of last-mile delivery fleets, driven by e-commerce growth, is creating sustained, high-volume demand for cargo securing straps, bungee nets, and load retention systems purpose-built for parcel delivery vehicles. Amazon, FedEx, UPS, DHL, and their delivery service partner networks collectively operate millions of delivery vehicles globally, and the American Trucking Associations (ATA) reports over 3.5 million truck drivers employed in the U.S. alone.

Each delivery vehicle requires a set of cargo securing equipment that is subject to regular wear and replacement, generating a high-frequency recurring aftermarket demand cycle. Manufacturers that develop fleet-grade, high-durability cargo strap systems and offer branded fleet procurement programs with volume pricing, custom labeling, and online reorder platforms can establish significant recurring revenue relationships with major logistics operators and their delivery service partners globally.

Category-wise Insights

By Product Type Analysis

Ratchet Straps are the leading product type segment, commanding approximately 36% of total market share. Ratchet straps are the industry standard cargo securing solution for commercial trucking, vehicle transport, construction equipment hauling, and heavy industrial applications due to their superior tensile strength ratings, typically 3,333 to 10,000+ lbs working load limit, and their ability to generate and maintain precise, consistent load tension through the ratcheting mechanism.

FMCSA’s cargo securement regulations and EN 12195-2 specifically recognize ratchet lashing straps as compliant load restraint devices, institutionalizing their use across regulated commercial transport. The segment benefits from both strong OEM vehicle transport demand and a robust aftermarket replacement cycle as straps are subject to wear, UV degradation, and capacity testing that necessitates periodic replacement for safety and compliance.

By Material Type Analysis

Polyester is the dominant material type segment, representing approximately 51% of total market share. Polyester webbing is the preferred material for automotive straps across virtually all professional and commercial applications due to its exceptional combination of high tensile strength, minimal stretch under load (typically less than 3% elongation at working load), excellent UV and chemical resistance, and moisture non-absorption, properties that maintain strap integrity across the outdoor storage and transport conditions typical of cargo securing applications.

Polyester’s performance advantages are formally recognized in standards including ASTM D6651 and EN 12195-2, which specify polyester as the reference material for synthetic fiber lashing straps. The material’s competitive cost versus nylon and its dimensional stability in wet conditions have made it the universal default choice for professional-grade ratchet and cam buckle strap webbing.

By Distribution Channel Analysis

The Aftermarket channel is the leading distribution segment, accounting for approximately 57% of total market share. The aftermarket encompasses a wide range of consumer and commercial procurement channels including truck stops, automotive parts retailers (AutoZone, O’Reilly, NAPA), hardware stores (Home Depot, Lowe’s), e-commerce platforms (Amazon, eBay), and specialty cargo control distributors.

The aftermarket’s dominance reflects the replacement and consumable nature of cargo straps, particularly for commercial operators who must regularly inspect and retire straps that show wear, webbing damage, or hardware corrosion per FMCSA 393.104 standards. The rapid growth of direct-to-consumer e-commerce channels, where brands including Rhino USA, SmartStraps, and US Cargo Control have built substantial online customer bases, is further expanding aftermarket distribution reach and frequency.

By Application Analysis

Cargo Securing is the leading application segment, representing approximately 42% of total market share. This segment encompasses all commercial and consumer applications involving the restraint of cargo loads in trucks, trailers, flatbeds, pickups, and delivery vehicles. The scale of global road freight, with the American Trucking Associations (ATA) reporting that U.S. trucks moved over 10 billion tons of freight in 2022, creates a vast and sustained demand base for compliant cargo securing straps.

Regulatory mandates requiring specific minimum restraint forces per tonne of cargo weight under FMCSA 393.100-393.136 in the U.S. and EN 12195-1 in Europe make cargo securing straps non-discretionary equipment for all commercial transport operations, ensuring structural, compliance-driven demand regardless of economic cycles.

By End-Use Analysis

Logistics & Transportation is the dominant end-use segment, accounting for approximately 38% of total market share. The logistics and transportation sector’s demand for automotive straps is driven by regulatory requirements for load securing compliance, the high wear and replacement rates of straps in daily commercial use, and the sector’s enormous scale globally.

The International Road Transport Union (IRU) estimates that road transport carries approximately 75% of all inland freight in Europe, with similar proportions in North America and emerging markets. Each commercial truck and trailer requires multiple certified tie-down straps as standard operating equipment, and fleet operators must replace worn or damaged straps to maintain regulatory compliance under road transport authority inspections. This compliance-driven, high-frequency replacement cycle sustains the logistics segment’s dominant end-use position.

Regional Insights

North America Automotive Straps Market Trends

North America is the largest automotive straps market, anchored by the United States’ massive trucking and logistics industry, large pickup truck ownership base, and well-developed recreational vehicle and outdoor lifestyle culture. The FMCSA’s cargo securement regulations under 49 CFR Part 393 require that all cargo transported on public roads be properly secured, with specific working load limit requirements for different cargo types that effectively mandate the use of certified straps across commercial operations. The ATA’s reporting of 10 billion+ tons of U.S. truck freight annually reflects the enormous addressable market for cargo securing straps.

The U.S.’s large pickup truck and SUV ownership base, with full-size pickup trucks consistently ranking as the best-selling vehicles for over 40 consecutive years, generates strong aftermarket demand for consumer-grade ratchet straps, bungee cords, and tie-down systems from brands including Erickson Manufacturing, Ancra International, and Keeper Products. Canada’s resource extraction, construction, and agricultural sectors contribute additional demand for heavy-duty strap systems. The U.S. innovation ecosystem, with brands investing in patented buckle designs, high-visibility webbing materials, and e-commerce direct sales, continuously elevates product quality and distribution efficiency.

Europe Automotive Straps Market Trends

Europe is a major and highly regulated automotive straps market, with the EN 12195 standard series governing all aspects of cargo restraint, including working load limits, lashing capacity calculations, and material specifications for commercial transport. The European Commission’s directive on securing cargo in road transport and national road transport regulations in Germany, France, Spain, and the United Kingdom require documented compliance with EN 12195, creating a standards-driven market where certified strap manufacturers from established brands command significant competitive advantages.

Germany is the region’s largest national market, home to major strap manufacturers including Dolezych GmbH & Co. KG and JUMBO-Textil GmbH & Co., as well as a world-class automotive and logistics industry that generates strong OEM and aftermarket demand. The UK market, governed by Highway Code load securing requirements enforced by DVSA road safety inspections, is served by manufacturers including Maypole Ltd. Spain’s growing logistics sector and France’s large trucking industry provide additional regional demand, with the EU’s digital freight transport initiatives expanding trailer tracking that integrates with smart cargo securing monitoring systems.

Asia Pacific Automotive Straps Market Trends

Asia Pacific is the fastest-growing regional market for automotive straps, driven by expanding logistics infrastructure, rising e-commerce volumes, growing vehicle production, and strengthening road freight safety regulations across China, India, Japan, and ASEAN nations. China dominates the regional market as both the world’s largest producer of synthetic webbing-based automotive straps and a massive domestic consumer, with the country’s rapidly expanding express logistics sector, including JD Logistics, SF Express, and Cainiao (Alibaba), generating high-volume demand for cargo securing products.

India’s logistics sector is transforming rapidly following the implementation of GST (Goods and Services Tax), which rationalized national freight movements and stimulated organized trucking fleet investment. The Ministry of Road Transport and Highways (MoRTH) is progressively strengthening vehicle load securing regulations, creating growing compliance demand. ASEAN nations, particularly Thailand, Vietnam, and Indonesia, are expanding their manufacturing and export logistics sectors, with growing vehicle production and freight volumes driving automotive strap demand. Asia Pacific’s cost-competitive manufacturing base also positions the region as the world’s primary supplier of mid-range automotive straps for export markets globally.

Competitive Landscape

The global automotive straps market is highly fragmented, with hundreds of manufacturers ranging from large established brands to small regional producers and private-label suppliers. Leading companies including Erickson Manufacturing, Ancra International, Kinedyne LLC, Dolezych, and SmartStraps hold competitive positions through certified product portfolios, established distribution networks, and brand recognition in specific market segments.

Key competitive differentiators include working load limit certifications (FMCSA, EN 12195), webbing material quality, hardware corrosion resistance, and warranty programs. Emerging business model trends include direct-to-consumer e-commerce platforms, fleet procurement portal programs, custom branded OEM strap kits for vehicle manufacturers, and product bundling with cargo management accessories. Asian manufacturers compete aggressively on price in the consumer aftermarket, while European and North American brands defend premium positioning through certification and innovation.

Key Market Developments

- February 2025: Rhino USA launched a new EV-specific vehicle transport strap series with wheel claws and axle strap configurations validated for battery electric vehicle tie-down point specifications, targeting vehicle transporter fleets and dealership delivery operations.

- September 2024: Kinedyne LLC expanded its certified cargo control product line with a new series of EN 12195-2 compliant polyester ratchet straps featuring anti-corrosion zinc-plated hardware, targeting European commercial transport operators requiring regulatory-compliant load securing solutions.

- April 2024: US Cargo Control launched a dedicated fleet procurement e-commerce platform enabling logistics companies to manage standardized cargo strap inventory orders online, with bulk pricing, custom labeling options, and automated reorder triggers based on fleet size and usage metrics.

Companies Covered in Automotive Straps Market

- Erickson Manufacturing Ltd.

- Ancra International LLC

- Keeper Products, Inc.

- Kinedyne LLC

- Horizon Global Corporation

- Dolezych GmbH & Co. KG

- SmartStraps

- Rhino USA

- Quickloader

- US Cargo Control

- Master Lock Company LLC

- CargoBuckle

- Nite Ize Inc.

- Maypole Ltd

- JUMBO-Textil GmbH & Co.

- Cargoparts.com

- Boxer Tools Inc.

Frequently Asked Questions

The global Automotive Straps Market is projected to reach US$ 5.4 Billion by 2033, growing from US$ 3.5 Billion in 2026 at a CAGR of 6.5% during the 2026-2033 forecast period. This accelerates from a historical CAGR of 5.8% between 2020 and 2025, driven by e-commerce logistics expansion, cargo securing regulations, and growing automotive OEM seat belt and restraint system demand.

The primary drivers are global e-commerce and road freight expansion, with ITF projecting 70%+ growth in freight transport volumes through 2050 and UNCTAD documenting US$ 5.5T+ in e-commerce sales, and FMCSA and EN 12195 cargo securing regulations mandating certified strap use across all commercial road transport operations, creating a compliance-driven floor of recurring demand.

Ratchet Straps lead the By Product Type category with approximately 36% market share. Their status as the FMCSA and EN 12195-2 compliant industry standard for commercial cargo securing, providing superior tensile strength of 3,333-10,000+ lbs WLL and precise load tension control through the ratcheting mechanism, makes them non-negotiable equipment for regulated commercial transport operations globally.

North America leads the global Automotive Straps Market, anchored by the United States’ mandatory FMCSA 49 CFR Part 393 cargo securing compliance requirements, ATA-reported 10+ billion tons of annual truck freight generating high-frequency strap replacement demand, and strong consumer aftermarket driven by the world’s highest per-capita pickup truck ownership.

The highest-value opportunities are EV-specific vehicle transport strap systems for the 14M+ annual global EV sales market requiring specialized BEV tie-down configurations, and fleet cargo control procurement programs targeting Amazon, FedEx, UPS, DHL and their millions of last-mile delivery vehicles requiring high-frequency, compliance-driven ratchet and webbing strap replacement.

The key market participants include Erickson Manufacturing Ltd., Ancra International LLC, Keeper Products Inc., Kinedyne LLC, Horizon Global Corporation, Dolezych GmbH & Co. KG, SmartStraps, Rhino USA, US Cargo Control, Master Lock Company LLC, CargoBuckle, Nite Ize Inc., Maypole Ltd, and JUMBO-Textil GmbH & Co., spanning commercial, consumer, and OEM strap segments globally.