- Automotive Components & Materials

- Automotive Gesture Recognition Systems Market

Automotive Gesture Recognition Systems Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Gesture Recognition Systems Market by Authentication (Hand/Fingerprint/Palm/Leg, Face, Vision/Iris), Vehicle Type (Passenger Cars, Light Commercial Vehicles, High Commercial Vehicles and Electric Vehicles), Application (Multimedia/Infotainment/Navigation, Lighting System, Other), By Component (Touch Based System, Touchless System), and Regional Analysis for 2026 - 2033

Automotive Gesture Recognition Systems Market Size and Trend Analysis

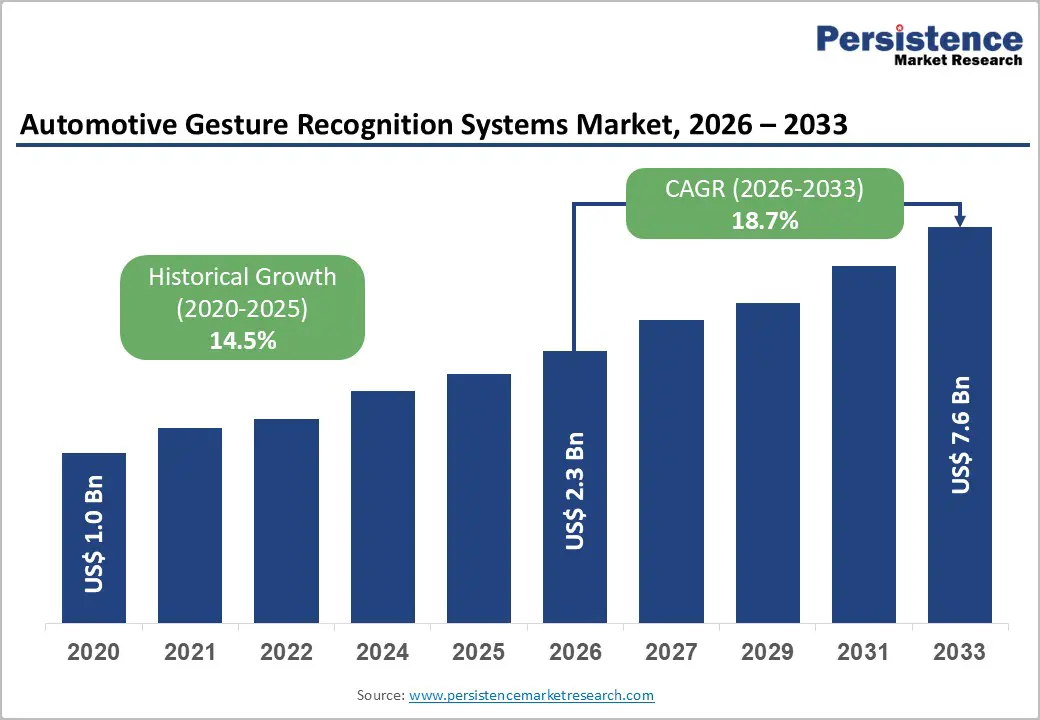

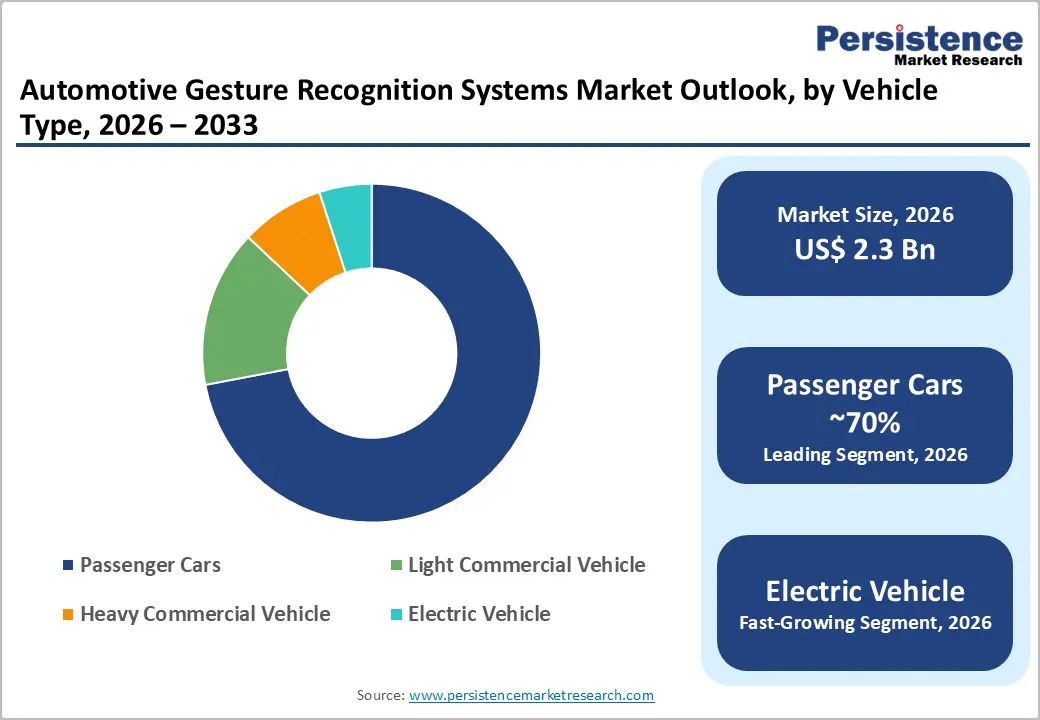

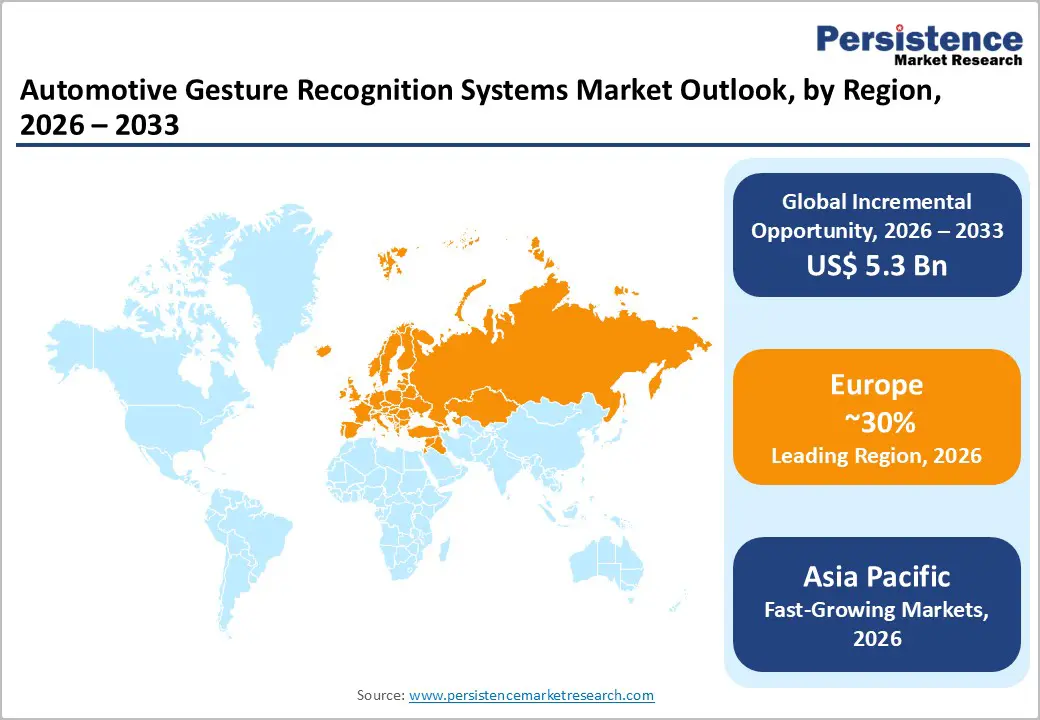

The global Automotive Gesture Recognition Systems Market is valued at US$ 2.3 Bn in 2026 and is projected to reach US$ 7.6 Bn by 2033, growing at a CAGR of 18.7% between 2026 and 2033.

The market is experiencing robust growth driven by a convergence of regulatory mandates, consumer demand for safer in-vehicle interfaces, and rapid advances in artificial intelligence. The European Union's General Safety Regulation (GSR), which made Advanced Driver Distraction Warning (ADDW) systems mandatory for all new vehicles by July 7, 2026, is structurally expanding addressable demand for in-cabin sensing and gesture recognition hardware and software.

Key Market Highlights

- Leading Region: Europe leads the global Automotive Gesture Recognition Systems Market, driven by mandatory EU General Safety Regulation (GSR) compliance deadlines requiring ADDW systems in all new vehicles by July 2026, supported by Tier-1 champions Continental AG, Bosch, and Valeo S.A. headquartered in the region.

- Fastest Growing Region: Asia Pacific is the fastest growing region, propelled by China's intelligent connected vehicle mandate, government tax incentives for driver monitoring in Beijing and Shanghai, Japan's Sony targeting 43% of global automotive image sensor supply, and rapidly expanding automotive production volumes across ASEAN markets.

- Dominant Segment: Touchless Systems dominate the By Component segmentation with approximately 62% market share, driven by the EU GSR distraction reduction mandates, post-pandemic hygiene preferences, and OEM deployments in BMW Panoramic iDrive and Mercedes-Benz MBUX Interior Assist demonstrating strong consumer acceptance of mid-air gesture controls.

- Fastest Growing Segment: The Face/Biometric Authentication sub-segment within the authentication category is the fastest growing, projected to expand at approximately 27% CAGR through 2033, catalyzed by Continental AG's Face Authentication Display launch in January 2024 and growing OEM demand for personalized, keyless vehicle access in software-defined electric vehicle platforms.

- Key Market Opportunity: convergence of gesture recognition with multimodal AI encompassing voice, eye-tracking, and behavioral inference as demonstrated by HARMAN's Luna system at CES 2025 represents the most significant long-term revenue expansion opportunity, enabling OEMs to monetize in-cabin personalization via over-the-air software upgrades throughout the vehicle lifecycle.

| Key Insights | Details |

|---|---|

|

Automotive Gesture Recognition Systems Market Size (2026E) |

US$ 2.3 Bn |

|

Market Value Forecast (2033F) |

US$ 7.6 Bn |

|

Projected Growth CAGR (2026-2033) |

18.7% |

|

Historical Market Growth (2020-2025) |

14.5% CAGR |

Market Dynamics

Market Growth Drivers

Mandatory Safety Regulations Driving In-Cabin Sensing Demand

Stringent government safety mandates are the single most powerful demand catalyst for the Automotive Gesture Recognition Systems Market. The European Union's Vehicle General Safety Regulation (GSR), phased in from July 2022 through July 2026, requires all new motor vehicles including passenger cars, trucks, and buses to be equipped with Driver Drowsiness and Attention Warning (DDAW) and Advanced Driver Distraction Warning (ADDW) systems. These regulations, which are expected to save over 25,000 lives and prevent at least 140,000 serious injuries by 2038 according to the European Commission, directly mandate the integration of interior-facing cameras and sensor technologies that form the hardware backbone of gesture recognition systems.

Accelerating EV and ADAS Adoption Creating New Interface Requirements

The global transition toward electric and semi-autonomous vehicles is profoundly reshaping requirements for in-vehicle human-machine interfaces, providing a powerful structural tailwind for gesture recognition adoption. According to the International Energy Agency (IEA), global electric vehicle sales exceeded 17 million units in 2024, representing approximately 20% of total global car sales a near 25% year-on-year increase. Electric vehicles inherently feature larger central display consoles and reduced physical controls, making touchless gesture interfaces a functionally superior alternative to traditional buttons. The integration of Advanced Driver Assistance Systems (ADAS) across vehicle classes further demands intuitive, distraction-minimizing control paradigms, as drivers in semi-automated vehicles must maintain situational awareness while managing infotainment and navigation.

Market Restraints

High Development and Integration Costs Limiting Mid-Market Penetration

Despite growing adoption in premium vehicle segments, the high cost of developing and integrating automotive-grade gesture recognition systems remains a significant restraint on mainstream market penetration. Automotive-grade 3D cameras, infrared sensors, time-of-flight modules, and the associated artificial intelligence processing hardware are considerably more expensive than conventional control interfaces. OEMs must additionally invest in multi-scenario training datasets, validation protocols, and over-the-air update infrastructure to maintain system accuracy across diverse lighting conditions and driver profiles. These cost structures create a price premium that constrains penetration in entry-level and mid-range vehicle segments, which represent most of the global automotive sales volume, particularly in high-growth emerging markets where vehicle affordability is a primary purchasing criterion.

Data Privacy Concerns and Biometric Regulation Complexity

The collection, processing, and storage of facial and biometric data inherent in advanced gesture and authentication systems creates material regulatory compliance risks for automotive manufacturers. The EU General Data Protection Regulation (GDPR) classifies biometric identification data as sensitive personal data requiring explicit user consent and stringent security obligations. Notably, the EU GSR's ADDW mandate explicitly requires that distraction warning systems must function without retaining biometric information. Navigating these overlapping regulatory frameworks particularly for OEMs operating across Europe, China, and the United States, each with distinct data localization and privacy regimes significantly increases development complexity, certification timelines, and ongoing compliance costs, creating friction that can delay market deployment and increase barriers to entry for smaller technology suppliers.

Market Opportunities

Biometric Authentication Integration as a Premium Differentiator

The integration of biometric gesture authentication encompassing facial recognition, iris scanning, and palm vein identification into vehicle access and personalization workflows represents a high-value growth opportunity within the Automotive Gesture Recognition Systems Market. In January 2024, Continental AG launched its Face Authentication Display, a two-tier biometric access control system embedded behind the driver's display console, using an OLED screen for discreet facial recognition for both in-cabin and external vehicle access. This development illustrates the commercial momentum behind biometric authentication as a premium feature that automakers can deploy as a distinct competitive differentiator. As electric vehicle platforms prioritize software-defined vehicle architectures enabling per-driver personalization of seat positions, ambient lighting, infotainment preferences, and climate settings via biometric identification the demand for integrated gesture and authentication systems is expected to expand substantially across luxury and progressively mid-tier vehicle segments through 2033.

Multimodal AI Integration Opening Next-Generation HMI Market Segment

The convergence of gesture recognition with voice recognition, eye-tracking, and AI-driven behavioral inference is creating a multimodal HMI segment with substantially greater functional scope and market value than standalone gesture systems. HARMAN International a subsidiary of Samsung Electronics Co., Ltd. demonstrated this trajectory in January 2025 when it announced new technology partnerships and unveiled Luna, an emotionally intelligent AI avatar integrated with its Ready Engage system, transforming in-cabin interaction into personalized, empathetic vehicle experiences. In March 2024, Synaptics Incorporated announced a strategic focus on edge AI for automotive in-cabin experiences, positioning itself as a platform for responsive, personalized gesture and sensing interfaces.

Category-wise Insights

Authentication Analysis

Within the authentication segmentation of the Automotive Gesture Recognition Systems Market, the Hand/Fingerprint/Palm/Leg authentication segment commands the leading position, accounting for approximately 36% of total market share. This dominance is rooted in the widespread commercial deployment of hand gesture control for infotainment, navigation, climate management, and lighting functions across luxury and semi-premium vehicle platforms. Purpose-designed hand gesture interfaces are embedded in flagship vehicle models from BMW with its air gesture controls in the iDrive system and Mercedes-Benz with its MBUX Interior Assist, both of which have demonstrated strong consumer acceptance and OEM replication across their vehicle portfolios. Hand gesture systems benefit from a relatively mature technology readiness level, broader sensor compatibility, and lower computational overhead compared to iris or full facial recognition, making them the preferred authentication modality for mass deployment at current price points.

Vehicle Type Analysis

Passenger Cars constitute the dominant vehicle type segment in the Automotive Gesture Recognition Systems Market, capturing approximately 72% of total market share. The pre-eminence of this segment is attributable to the intensive focus by passenger car OEMs on cockpit digitalization, personalized user experiences, and regulatory compliance with EU safety mandates targeting M1-category passenger vehicles. Premium passenger car brands including BMW, Mercedes-Benz, Audi, and Tesla have led commercial deployment of gesture recognition as standard or optional features, and the technology is progressively trickling down into mainstream mid-range models. The transition to electric vehicles, which substantially reduces interior physical controls and places greater emphasis on digital HMI, is particularly pronounced in the passenger car segment. Commercial Vehicles encompassing trucks, buses, and commercial vans represent the remaining market share and are expected to register proportionally stronger growth through 2033 as ADDW mandates extend to N2, N3, M2, and M3 vehicle categories under the EU GSR.

Application Analysis

The Multimedia/Infotainment/Navigation application segment leads the Automotive Gesture Recognition Systems Market with approximately 58% market share, driven by its central role in the modern automotive digital cockpit. The integration of gesture control into infotainment and navigation systems addresses a primary safety concern for regulators and OEMs alike: enabling drivers to interact with audio, navigation, phone connectivity, and climate controls without diverting visual attention from the road. According to a Deloitte consumer survey, approximately 68% of drivers express preference for gesture-based controls for infotainment and navigation tasks versus conventional touchscreens. The proliferation of large central display consoles particularly in electric vehicles and the OEM-mandated shift toward software-defined vehicle cockpits is anchoring infotainment as the primary application domain for gesture recognition adoption, with Continental AG, Visteon Corporation, and Harman International all centring their product roadmaps around this application.

By Component Analysis

Touchless Systems represent the leading component segment in the Automotive Gesture Recognition Systems Market, accounting for approximately 62% of market share, as documented by industry tracking data. Touchless gesture recognition enables drivers to control vehicle functions through mid-air hand movements, body gestures, and eye-tracking without requiring physical surface contact a capability that aligns precisely with the distraction-reduction objectives embedded in EU GSR safety legislation. The post-pandemic behavioral shift toward contactless interaction reinforced consumer preference for touchless interfaces, while advances in 3D depth cameras, infrared sensors, and time-of-flight technology have substantially improved gesture detection accuracy across diverse environmental conditions including low light and variable weather.

Regional Insights

North America

North America represents one of the most mature and innovation-intensive regions in the Automotive Gesture Recognition Systems Market, led by the United States where a convergence of robust automotive R&D investment, advanced semiconductor ecosystems, and progressive federal safety policy is driving market development. The U.S. Department of Transportation has allocated US$ 1.2 billion toward smart vehicle technologies including advanced HMI solutions as part of its road safety and connected vehicle strategy.

The region benefits from the concentrated presence of leading semiconductor companies including NXP Semiconductors, Qualcomm, and Texas Instruments, whose automotive-grade chipsets form the processing backbone of gesture recognition systems. Electric vehicle adoption in North America with approximately 1.7 million EVs sold in the United States in 2024 according to the IEA is expanding the addressable market for next-generation in-cabin gesture interfaces.

Europe

Europe commands the largest regional share of the Automotive Gesture Recognition Systems Market, anchored by Germany, France, the United Kingdom, and Spain home to both the world's most stringent automotive safety legislative framework and the headquarters of globally leading Tier-1 automotive suppliers. The EU Vehicle General Safety Regulation (GSR), which mandated Driver Drowsiness and Attention Warning (DDAW) systems for all new EU vehicle types from July 2022 and expanded these requirements to Advanced Driver Distraction Warning (ADDW) systems for all new vehicles by July 7, 2026, has created a structural compliance mandate that is directly stimulating investment in in-cabin camera, sensor, and gesture recognition hardware.

Germany anchors regional competitive strength through the vertically integrated presence of Continental AG, Robert Bosch GmbH, and Infineon Technologies AG, which collectively span sensor design, processing hardware, and systems integration. Valeo S.A. of France unveiled advanced cabin monitoring systems in July 2024, integrating infrared and RGB cameras in mirror housings for occupant detection and gesture recognition across front and rear seat passengers expanding the gesture recognition perimeter beyond driver-only applications.

Asia Pacific

Asia Pacific is the fastest growing region in the Automotive Gesture Recognition Systems Market, driven by China's mandatory intelligent connected vehicle framework, Japan's sensor technology pipeline, and India's rapidly expanding automobile sector. China's government-backed Intelligent Vehicle Innovation and Development Strategy, which targets full-scale commercial deployment of smart connected vehicles across major urban centers, has positioned the country as the primary growth engine for automotive in-cabin technology adoption.

Japan contributes precision sensor manufacturing capabilities, with Sony targeting 43% of the global automotive image sensor market by fiscal 2026, banking on demand from gesture and driver monitoring applications. Renesas Electronics Corporation strengthened its HMI portfolio through the acquisition of radar startup Steradian Semiconductors in August 2022, expanding its gesture recognition technology stack for automotive applications. In India, growing EV adoption supported by the FAME II policy and evolving safety norms is creating nascent but accelerating demand for advanced in-cabin technologies.

Competitive Landscape

The Automotive Gesture Recognition Systems Market exhibits a moderately consolidated competitive structure, dominated by established automotive Tier-1 suppliers principally Continental AG, Robert Bosch GmbH, and Valeo S.A. alongside specialized semiconductor and software companies including NXP Semiconductors, Synaptics Incorporated, and Eyesight Technology. Key competitive differentiators include proprietary sensor fusion algorithms, edge AI processing capability, biometric authentication accuracy, OEM design-win relationships, and certification to automotive safety standards such as ISO 26262. R&D investment is concentrated in multimodal AI platforms that fuse gesture, voice, and eye-tracking inputs.

Key Market Developments

- In January 2025, HARMAN International (a subsidiary of Samsung Electronics Co., Ltd.) announced a series of new technology partnerships and unveiled the Luna emotionally intelligent AI avatar system, expanding its advanced automotive solutions library encompassing in-car connectivity, infotainment, and gesture recognition technologies across a broad OEM ecosystem.

- In 2025, Valeo S.A. launched cloud-connected gesture systems, enabling adaptive personalization, multi-user recognition, and integration with ADAS and connected vehicle networks for enhanced safety and convenience.

- In October 2024, Sony Semiconductor Solutions launched the ISX038 automotive CMOS image sensor, the industry's first sensor capable of simultaneously processing and outputting RAW and YUV images via dual interfaces, enabling single cameras to serve both gesture recognition and visual display applications while reducing system cost and complexity.

Companies Covered in Automotive Gesture Recognition Systems Market

- Continental AG

- Robert Bosch GmbH

- Delphi Technologies

- Denso Corporation

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- Visteon Corporation

- Harman International

- Synaptics Incorporated

- Eyesight Technology

- Cognitec Systems GmbH

- Valeo S.A.

Frequently Asked Questions

The global Automotive Gesture Recognition Systems Market is valued at US$ 2.3 Bn in 2026 and is projected to reach US$ 7.6 Bn by 2033, growing at a CAGR of 18.7% during the forecast period.

The primary demand drivers include the European Union's General Safety Regulation (GSR) mandating ADDW and DDAW in-cabin systems for all new vehicles by July 2026 alongside global EV adoption, which exceeded 17 million units in 2024 according to the IEA, and growing OEM investment in software-defined vehicle cockpits.

Touchless Systems dominate the By Component segmentation of the Automotive Gesture Recognition Systems Market with approximately 62% market share. Touchless gesture recognition enables hands-free, surface-free vehicle control that directly supports distraction reduction objectives mandated by the EU GSR.

Europe commands the largest regional share of the Automotive Gesture Recognition Systems Market, underpinned by the EU's Vehicle General Safety Regulation (GSR) that mandated ADDW and DDAW compliance across all new vehicles with a final deadline of July 7, 2026.

The leading companies operating in the global Automotive Gesture Recognition Systems Market include Continental AG Visteon Corporation, Synaptics Incorporated, Eyesight Technology, Cognitec Systems GmbH, Valeo S.A., Denso Corporation, Renesas Electronics Corporation, and Delphi Technologies, among others.