- Automotive

- Automotive Blind Spot Detection System Market

Automotive Blind Spot Detection System Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Blind Spot Detection System Market by Technology (Radar Sensor, Camera, Ultrasonic Sensor), Vehicle Type (Passenger Cars, Commercial Vehicles), Propulsion Type (ICE, Electric), and Regional Analysis for 2026 - 2033

Automotive Blind Spot Detection System Market Size and Trend Analysis

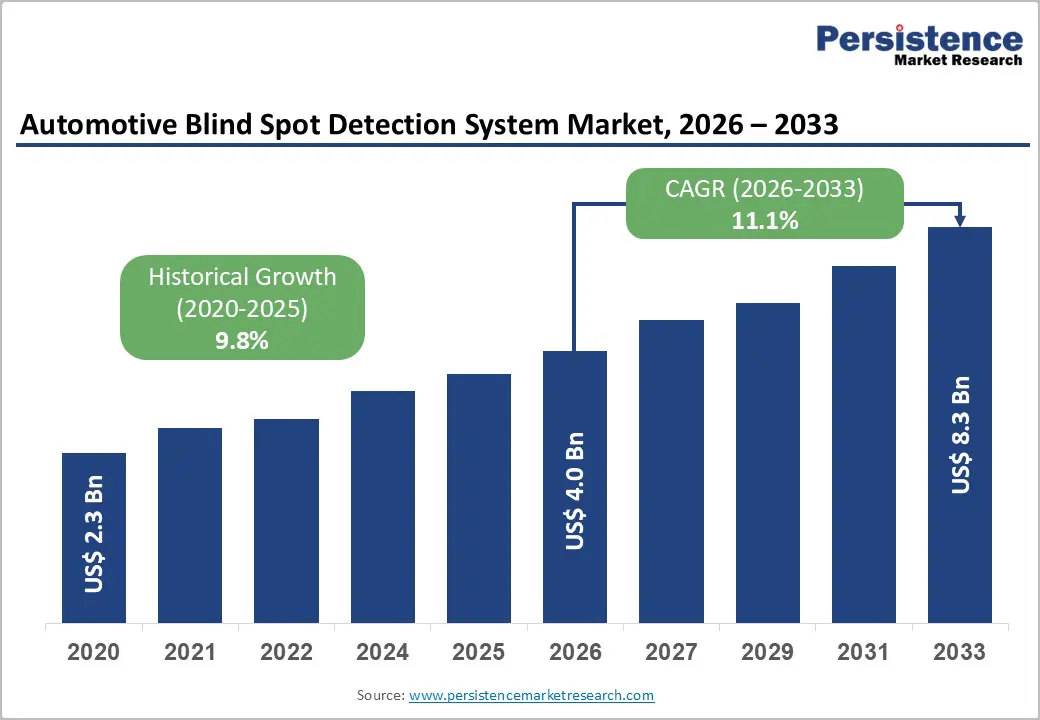

The global automotive blind spot detection system market size is valued at US$ 4.0 billion in 2026 and is projected to reach US$ 8.4 billion by 2033, growing at a CAGR of 11.1% between 2026 and 2033.

This accelerated growth trajectory reflects the compounding effect of tightening global vehicle safety mandates, the rapid mainstreaming of Advanced Driver Assistance Systems (ADAS) across mid-range and premium vehicle segments, and the technology-led transition toward sensor fusion architectures.

Key Industry Highlights:

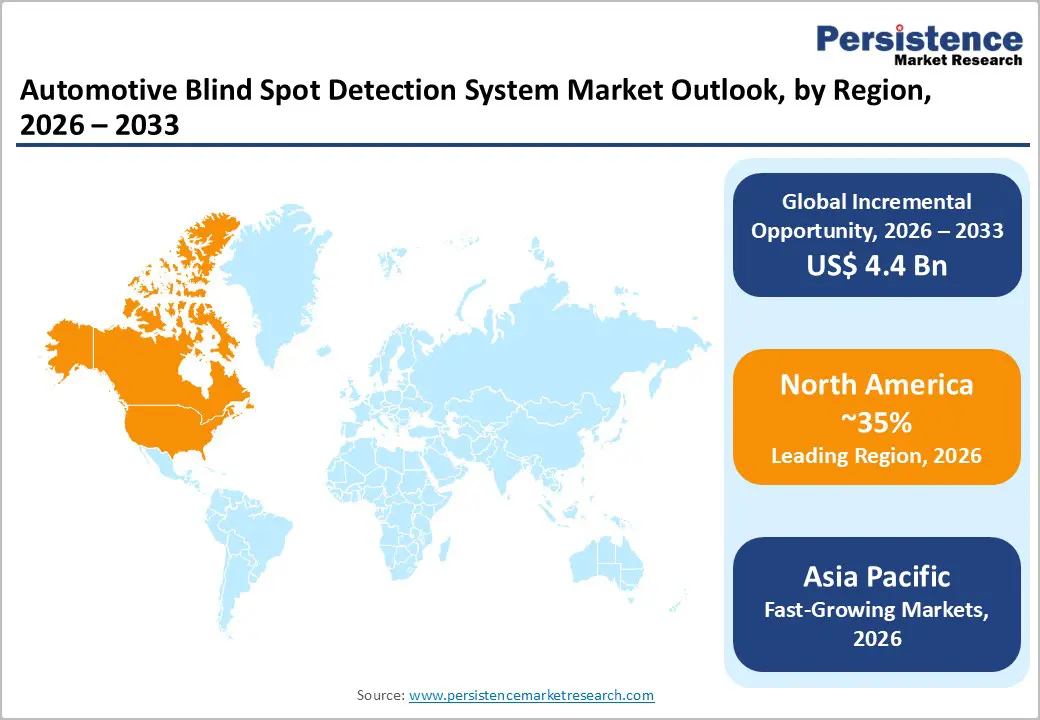

- Leading Region: North America leads the global Automotive Blind Spot Detection System Market, underpinned by NHTSA's December 2024 NCAP update formally incorporating Blind Spot Warning and Blind Spot Intervention into consumer vehicle safety ratings, driving near-universal OEM adoption across all new passenger car programs through 2033.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, expanding at approximately 10.8% CAGR through 2031, driven by China's massive vehicle production base, India's BSD market growing at 11.5% CAGR, and escalating road safety mandates across ASEAN nations compelling accelerated ADAS deployment.

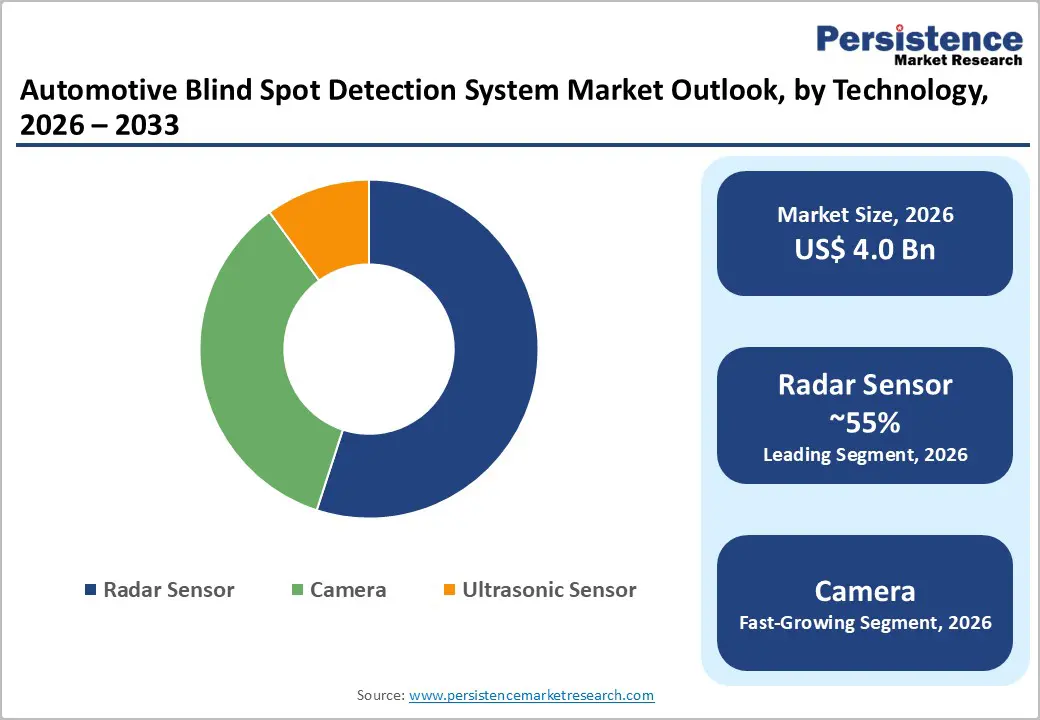

- Dominant Segment: The Radar Sensor technology segment leads with approximately 55% market share in the Automotive Blind Spot Detection System Market, driven by its all-weather operational reliability, superior long-range detection, FMCW precision, and seamless integration with broader ADAS and autonomous vehicle sensor fusion architectures.

- Fastest Growing Segment: The Electric propulsion type segment is the fastest-growing category in the Automotive Blind Spot Detection System Market, as EV manufacturers prioritize comprehensive ADAS feature sets and the compact electronic architectures of EVs facilitate easier BSD sensor integration, with BEVs commanding over 45% of electric vehicle BSD adoption.

- Key Opportunity: Commercial vehicle fleets represent the highest-growth underserved opportunity, with the EU General Safety Regulation mandating BSD technologies for trucks and buses from July 2024 and fleet operators facing mounting liability exposure from blind spot-related accidents, driving both regulatory-compelled and proactive system procurement globally.

| Key Insight | Details |

|---|---|

| Automotive Blind Spot Detection System Market Size (2026E) | US$ 4.0 Bn |

| Market Value Forecast (2033F) | US$ 8.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.8% |

Market Dynamics

Drivers - Mandatory ADAS Regulations Across the U.S. and EU Creating Sustained Procurement Demand

The most consequential structural driver of the Automotive Blind Spot Detection System Market is the escalating wave of binding regulatory mandates requiring blind spot detection as standard equipment on new vehicles across major global automotive markets. In December 2024, the U.S. National Highway Traffic Safety Administration (NHTSA) finalized its decision to incorporate Blind Spot Warning (BSW) and Blind Spot Intervention (BSI) into the updated New Car Assessment Program (NCAP), with a 10-year performance evaluation roadmap spanning 2024 through 2033. In the European Union, Regulation (EU) 2019/2144 the General Safety Regulation mandated blind spot recognition technologies and collision warning systems for all new trucks and buses from July 2024, with further expansion phases planned through 2029. These overlapping regulatory frameworks across two of the world's largest automotive markets create a durable, policy-reinforced demand base for blind spot detection hardware and software suppliers throughout the forecast period, structurally embedding the technology into vehicle design requirements.

Rising Road Accident Statistics and Consumer Safety Awareness Accelerating ADAS Adoption

Escalating road fatality and injury data across global markets is reinforcing both regulatory and consumer-driven demand for blind spot detection technologies. In the Asia Pacific region alone, road accidents resulted in 1,68,491 fatalities and 4,43,366 injuries in a recent reporting year representing an 11.9% increase in accidents, a 9.4% increase in fatalities, and a 15.3% increase in injuries compared to the prior year directly motivating government mandates for advanced driver assistance systems adoption in both passenger and commercial vehicles. Connected vehicle penetration which grew from 94% to 97% between 2020 and 2022 according to Fleet News is further amplifying demand for integrated, data-sharing blind spot monitoring solutions that can communicate with vehicle-to-infrastructure networks, enhancing the value proposition of modern blind spot detection systems in urban traffic environments.

Restraints - High System Integration Costs Limiting Adoption in Entry-Level Vehicle Segments

Despite robust demand at the premium and mid-range tires, the high cost of multi-sensor blind spot detection systems remains a meaningful barrier to universal adoption, particularly in price-sensitive entry-level passenger car and commercial vehicle segments in emerging markets. Full radar-based blind spot detection systems especially those incorporating Frequency Modulated Continuous Wave (FMCW) radar and sensor fusion with cameras involve significant bill-of-materials and integration engineering costs. In markets such as India and Southeast Asia, where many vehicle sales are concentrated in sub-compact and entry-level segments, these cost barriers slow the penetration rate of standard ADAS equipment and limit market volume growth in the near term.

Sensor Performance Limitations in Adverse Weather and Complex Urban Environments

While radar sensors demonstrate superior all-weather detection capability, camera-based blind spot systems remain susceptible to performance degradation in conditions of heavy rain, fog, glare, and low-light environments. Ultrasonic sensors, though cost-effective, are limited to short-range detection, constraining their applicability for highway-speed blind spot monitoring scenarios. Sensor fusion architectures combining radar, camera, and ultrasonic inputs effectively mitigate these limitations, but add system complexity and cost. False alarm rates in complex urban traffic scenarios can undermine driver trust in blind spot systems, potentially reducing consumer willingness to rely on and pay for the technology, particularly in aftermarket retrofit applications. These technical reliability challenges represent ongoing hurdles for system developers in the automotive blind spot detection system market.

Opportunity - Commercial Vehicle Fleet Safety Regulations Opening a Structurally Underserved Segment

The commercial vehicles segment represents a high-growth, structurally underserved opportunity within the Automotive Blind Spot Detection System Market, driven by the convergence of mandatory regulatory requirements, fleet operator safety obligations, and the physical blind spot challenges inherent to trucks, buses, and heavy freight vehicles. The EU General Safety Regulation (EU) 2019/2144 specifically mandated blind spot recognition technologies for trucks and buses from July 2024 and will continue expanding scope requirements through 2029, directly driving OEM specification of BSD systems across commercial vehicle production lines.

Fleet operators managing large vehicle pools face mounting liability exposure from blind spot-related accidents, creating a compelling economic case for proactive system installation beyond regulatory minimums. The International Trade Administration (ITA) projects that partial and conditional automation vehicles will account for over 50% of new vehicle sales in China by 2025, many of which are commercial and logistics platforms, underscoring the scale of demand building in this category.

EV Platform Integration Driving Next-Generation Blind Spot Detection System Demand

Electric vehicles represent the fastest-growing propulsion-type opportunity for Automotive Blind Spot Detection System suppliers, as EV platforms are architecturally optimized for seamless ADAS integration and are disproportionately equipped with advanced safety features by design. Battery Electric Vehicles (BEVs) lead the electric vehicle segment with over 45% share within the electric vehicle blind spot monitoring category, as EV manufacturers position ADAS comprehensiveness as a core competitive differentiator.

The global EV transition, with EVs accounting for approximately 18% of global car sales in 2024 is creating a rapidly expanding addressable market for premium blind spot detection systems. As automakers such as Tesla, BYD, and Volkswagen compete on ADAS feature depth, blind spot detection integration becomes a standard expectation rather than a premium option, expanding the market across an ever-broader range of EV price segments throughout the forecast period.

Category-wise Analysis

Technology Insights

Radar Sensor is the leading technology segment in the Automotive Blind Spot Detection System Market, commanding an estimated market share of approximately 55% in 2026. Radar technology's dominance is underpinned by its all-weather operational reliability, functioning accurately in rain, fog, dust, and low-visibility conditions, where camera and ultrasonic sensors experience significant performance degradation. Radar systems, particularly those utilizing Frequency Modulated Continuous Wave (FMCW) architectures, deliver precise range, speed, and directional measurements of objects in blind zones, enabling both Blind Spot Warning (BSW) and active Blind Spot Intervention (BSI) functionalities. In January 2023, NXP Semiconductors released an advanced 28nm RFCMOS radar-on-chip family for next-generation ADAS and autonomous driving applications, directly targeting blind spot detection and automatic emergency braking use cases.

Vehicle Type Insights

Passenger cars represent the dominant vehicle type segment in the automotive blind detection system market, accounting for an estimated 54% of total market share in 2025. This leadership reflects passenger cars' overwhelming share of total global vehicle production volumes, combined with strong consumer demand for ADAS safety features in daily commuting vehicles and intensifying OEM competition to differentiate on safety technology breadth. NHTSA's December 2024 decision to incorporate blind spot warning and intervention assessments into NCAP ratings which directly influence consumer purchasing decisions is further accelerating OEM integration of blind spot detection systems across passenger car product lines, from entry-level vehicles to premium segments. The Persistence Market Research analysis of the Automotive Blind Spot Detection System Market affirms that passenger car penetration of blind spot technology is deepening across all global regions, supported by both regulatory compliance and consumer preference convergence.

Propulsion Type Insights

The ICE (Internal Combustion Engine) segment currently leads the Automotive Blind Spot Detection System Market's propulsion type category, reflecting the still-dominant share of ICE vehicles in the global total vehicle parc. The ICE segment is estimated to hold approximately 72% of the total market share in 2026, underpinned by the massive installed base of ICE passenger cars and commercial vehicles globally and the growing OEM-standard integration of blind spot detection in mid-range and premium ICE vehicle platforms. The Electric propulsion segment, while smaller in current absolute terms, is unambiguously the fastest-growing propulsion type segment in the Automotive Blind Spot Detection System Market. Electric vehicle manufacturers inherently position advanced ADAS as a core product differentiator, and the compact electronic architectures of EVs facilitate easier BSD sensor integration compared to traditional ICE platforms.

Regional Insights

North America Automotive Blind Spot Detection System Market Trends

North America is the leading regional market for automotive blind spot detection systems, driven by the United States' combination of a large vehicle parc, high consumer willingness-to-pay for safety technology, and the most comprehensive regulatory evolution underway in the ADAS space. The U.S. Department of Transportation's NHTSA finalized its NCAP update in December 2024, formally embedding Blind Spot Warning (BSW) and Blind Spot Intervention (BSI) performance evaluations into the consumer-facing five-star safety rating system, with a 10-year roadmap through 2033 ensuring sustained market demand.

The North American aftermarket for blind spot detection retrofits also represents a growing commercial channel, particularly among fleet operators and independent commercial vehicle owners subject to escalating liability exposure. The presence of leading technology suppliers, including Sensata Technologies, Inc. and VOXX Electronics Corp. both headquartered in the U.S., alongside global tier-1 suppliers with major North American operations, reinforces the region's innovation ecosystem for BSD technology development and commercialization.

Europe Automotive Blind Spot Detection System Market Trends

Europe represents the second-largest and one of the most regulatory-driven regional markets for automotive blind spot detection systems, with a comprehensive mandatory ADAS framework already in force. Regulation (EU) 2019/2144 the General Safety Regulation (GSR2) mandated blind spot recognition technologies for trucks and buses from July 2024 and includes expanding scope requirements through 2029, covering additional vehicle categories.

Germany leads European innovation in BSD technology, with premium automakers including BMW, Mercedes-Benz, Audi, and Volkswagen consistently specifying advanced sensor fusion BSD systems in new model launches. Robert Bosch GmbH and Continental AG both headquartered in Germany, are global leaders in radar-based blind spot detection hardware, deploying cutting-edge FMCW radar and sensor fusion architectures across OEM programs worldwide. Germany is projected to grow at a CAGR of 7.4% in adaptive highway driving features incorporating BSD technology through the forecast period.

Asia Pacific Automotive Blind Spot Detection System Market Trends

Asia Pacific is the fastest-growing regional market for automotive blind spot detection systems, expanding at an estimated CAGR of 10.8% through 2031. China is the dominant country market, driven by the world's largest automotive production volumes, the rapid adoption of autonomous and semi-autonomous vehicles with partial and conditional automation vehicles expected to account for over 50% of new vehicle sales in China by 2025, according to the International Trade Administration (ITA) and escalating government mandates for vehicle safety systems. India is the fastest-growing country market within Asia Pacific, with the Automotive Blind Spot Detection System Market in India projected to grow at a CAGR of 11.5% through 2031, driven by the government's Bharat New Car Assessment Programme (Bharat NCAP) and rising consumer safety awareness following a sustained increase in road accident casualties.

Japan continues to be a technically sophisticated BSD market, with Toyota, Honda, and Nissan consistently integrating premium ADAS capabilities, including multi-sensor blind spot detection across a broad range of vehicle model lines, supported by Japan's strong focus on autonomous driving safety standards.

Competitive Landscape

The global automotive blind spot detection system market is moderately consolidated at the tier-1 supplier level, with Robert Bosch GmbH, Continental AG, Valeo, and Sensata Technologies commanding significant market influence through deep OEM integration contracts, proprietary radar sensor portfolios, and global engineering footprints. Competition is primarily driven by sensor technology performance, sensor fusion architecture capability, ADAS integration breadth, and cost optimization for volume OEM programs.

Emerging competitive dynamics include the rise of semiconductor-led players such as NXP Semiconductors and Infineon Technologies AG challenging traditional Tier-1 integrators with chip-level system solutions. Investment in AI-powered object classification, multi-sensor fusion, and vehicle-to-everything (V2X) connectivity represents the most prominent R&D frontier, with leading players filing increasing numbers of ADAS-related patents across radar and imaging technologies.

Key Developments:

- In December, 2024, The U.S. Department of Transportation's NHTSA finalized its decision to add Blind Spot Warning (BSW) and Blind Spot Intervention (BSI) to the updated New Car Assessment Program (NCAP), establishing a 10-year performance roadmap through 2033 that directly embeds BSD evaluation into consumer vehicle safety ratings.

- In October 2023, Sensata Technologies introduced PreView Sentry79, a radar system for blind spot detection, designed for front and rear detection, intended to enhance driver awareness and mitigate the danger of blind spot collisions.

Companies Covered in Automotive Blind Spot Detection System Market

- Sensata Technologies, Inc.

- Robert Bosch GmbH

- Continental AG

- Rear View Safety, Inc.

- Valeo Service

- NXP Semiconductors

- Infineon Technologies AG

- VOXX Electronics Corp.

- Exeros Technologies Ltd.

- Quanzhou Minpn Electronic Co., Ltd.

- Other Key Players

Frequently Asked Questions

The global Automotive Blind Spot Detection System Market is valued at approximately US$ 4.0 Billion in 2026 and is projected to reach US$ 8.4 Billion by 2033, growing at a forecast CAGR of 11.1% between 2026 and 2033.

Growth is primarily driven by binding regulatory mandates including NHTSA's December 2024 NCAP update adding Blind Spot Warning and Blind Spot Intervention assessments, and the EU General Safety Regulation (EU) 2019/2144 mandating BSD systems for trucks and buses from July 2024 alongside escalating road safety awareness, connected vehicle proliferation, and the mainstreaming of ADAS across passenger and commercial vehicle platforms globally.

The Radar Sensor technology segment leads the Automotive Blind Spot Detection System Market with an estimated 55% market share, driven by radar's all-weather reliability, superior long-range detection capability, and performance in FMCW precision ranging qualities that cameras and ultrasonic sensors cannot match in adverse weather or high-speed highway detection scenarios.

North America holds the largest regional share in the Automotive Blind Spot Detection System Market, supported by NHTSA's comprehensive NCAP blind spot evaluation framework, a large high-ADAS-penetration vehicle parc, and the presence of leading technology suppliers.

The leading companies operating in the global Automotive Blind Spot Detection System Market include Robert Bosch GmbH, Continental AG, NXP Semiconductors, Valeo Service, Sensata Technologies, Inc., Infineon Technologies AG, ZF Friedrichshafen AG, Denso Corporation, Aptiv PLC, and VOXX Electronics Corp., among others.