- Automotive Components & Materials

- Automotive Acoustic Engineering Services Market

Automotive Acoustic Engineering Services Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Acoustic Engineering Services Market by System (Physical Testing and Virtual Testing), By Application (Interior, Powertrain, Drivetrain, and Others), and Regional Analysis for 2026 - 2033

Automotive Acoustic Engineering Services Market Size and Trends Analysis

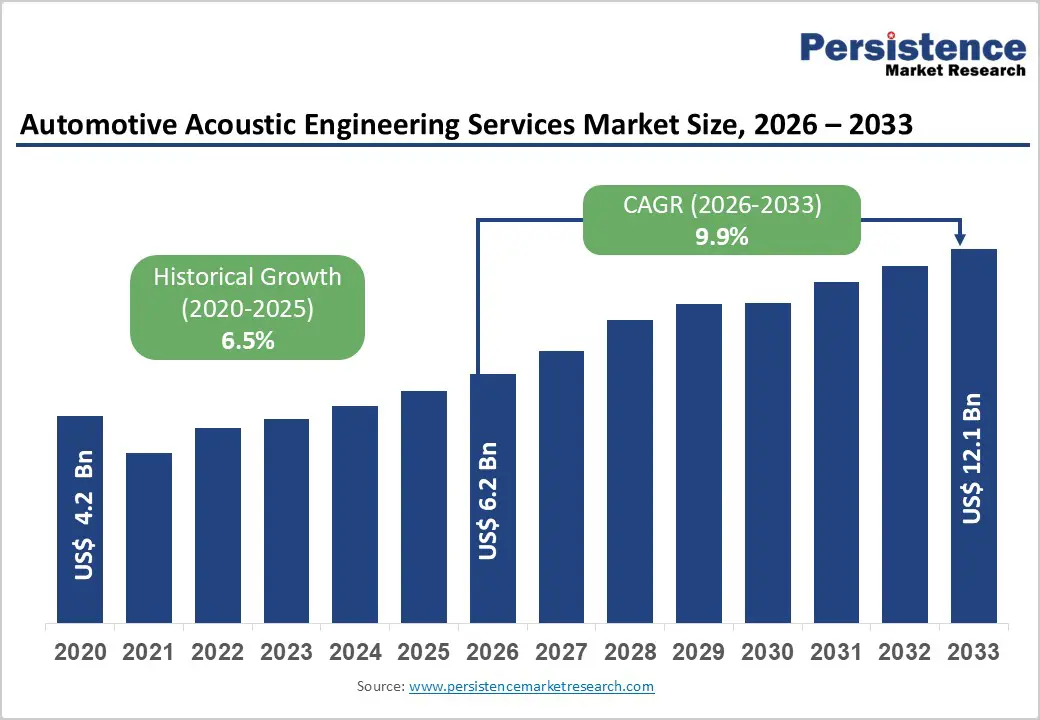

The global automotive acoustic engineering services market was valued at US$ 4.2 Billion in 2020 and reached US$ 6.2 Billion in 2026, with projections to reach US$ 12.1 Billion by 2033, growing at a CAGR of 9.9% between 2026 and 2033 (Historical CAGR 2020 - 2026: 6.5%).

This market expansion reflects the automotive industry's escalating focus on vehicle noise reduction, enhanced passenger comfort, and stringent regulatory requirements across major automotive markets. The acceleration in growth rate from 6.5% to 9.9% indicates intensifying demand driven by electric vehicle adoption, technological advancements in acoustic simulation, and consumer expectations for premium driving experiences globally.

Key Industry Highlights:

- Physical testing dominance with virtual testing momentum: Physical testing maintains 65%+ market share with moderate 7.5-8.5% growth; virtual testing emerging as fastest-growing segment with 11.2% CAGR, gradually expanding responsibility for acoustic development activities beyond compliance-critical functions

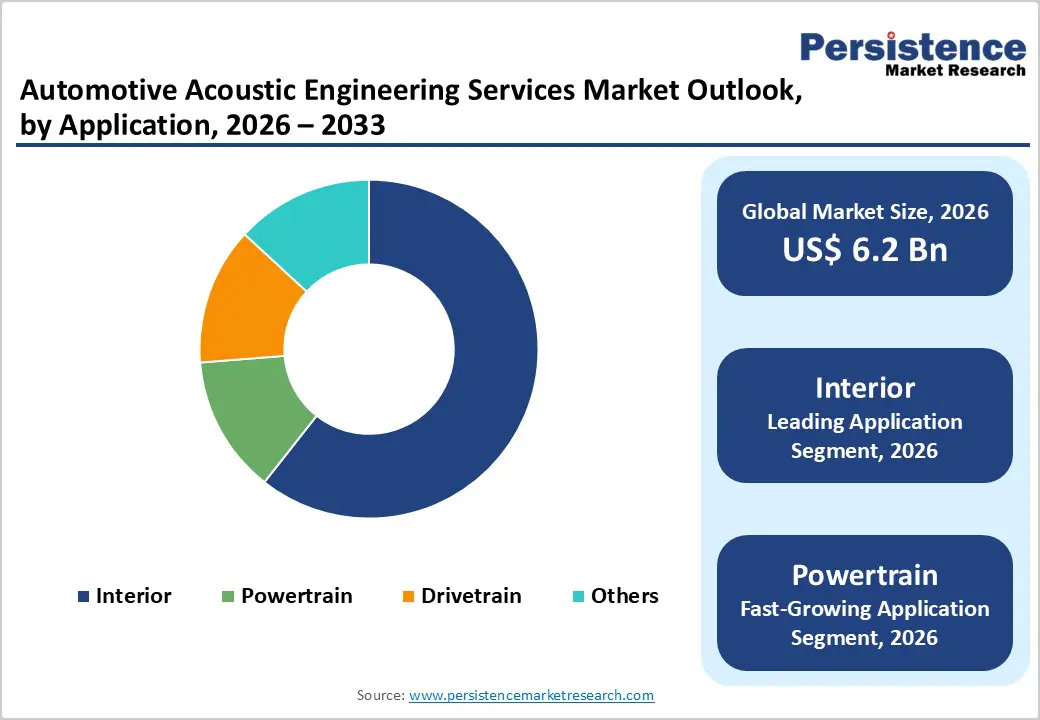

- Powertrain acoustic expansion leading applications: Interior applications retain dominant 35%+ revenue share; powertrain acoustic services achieving 11.5% CAGR driven by electric vehicle production acceleration and acoustic complexity elevation in EV propulsion systems

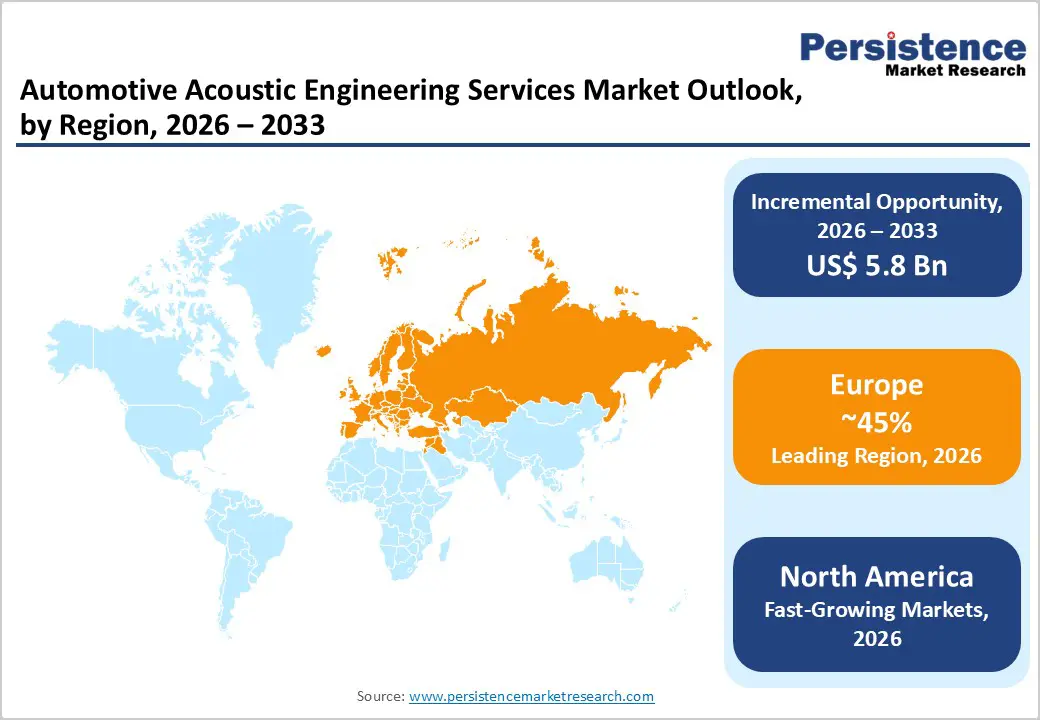

- Europe market leadership with Asia-Pacific growth acceleration: Europe commanding 45%+ global market share with mature market characteristics; North America with 11.3% CAGR fastest-growing established market; Asia-Pacific expanding at 11.3% CAGR driven by manufacturing expansion and emerging market OEM development

- Market consolidation trajectory: Moderate market consolidation with 5-8 largest players commanding 22-28% combined market share; mid-sized independent firms progressively merging with diversified engineering service providers; emerging indigenous providers in Asia-Pacific rapidly developing local capabilities

- Strategic imperatives: Digital transformation acceleration through cloud-based simulation platforms, sustainability-focused service differentiation supporting regulatory and ESG mandates, geographic expansion into high-growth emerging markets, and technology partnerships supporting integrated acoustic-vehicle development ecosystem evolution

| Global Market Attributes | Key Insights |

|---|---|

| Automotive Acoustic Engineering Services Market Size (2026E) | US$ 6.2 Bn |

| Market Value Forecast (2033F) | US$ 12.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.5% |

Market Dynamics

Key Growth Drivers

Stringent Noise Emission Regulations and Compliance Requirements

Regulatory frameworks across North America, Europe, and Asia-Pacific have implemented increasingly strict noise emission standards that directly mandate automotive manufacturers' investment in acoustic engineering services. The European Union's Stage V regulations and Euro 6 standards require manufacturers to reduce vehicle noise emissions to specific decibel levels, with non-compliance penalties reaching 5-10% of annual revenue. Similarly, the United States Environmental Protection Agency (EPA) enforces the Noise Control Act, requiring comprehensive acoustic testing before vehicle launch.

These regulatory pressures account for approximately 40-45% of acoustic engineering service adoption, forcing OEMs to invest in both physical testing facilities and virtual simulation capabilities. The International Organization for Standardization (ISO) standards, particularly ISO 3744 and ISO 3745 for sound pressure level measurement, establish baseline compliance requirements that manufacturers cannot bypass. This regulatory-driven demand creates a stable, predictable revenue stream for acoustic engineering service providers, with manufacturers budgeting acoustic compliance costs as non-discretionary expenditures during vehicle development cycles.

Market Restraining Factors

Complexity of Virtual Testing Validation and Simulation Accuracy Limitations

While virtual acoustic testing (CAE simulation) continues advancing rapidly, persistent validation challenges limit widespread adoption and delay market expansion. Acoustic simulation models require extensive experimental validation against physical test data, with correlation errors of 3-8 dB remaining common in complex vehicle structures, necessitating hybrid physical-virtual testing approaches that increase overall project costs and timelines. Automotive manufacturers express hesitation regarding exclusive reliance on virtual testing for regulatory compliance decisions, as regulatory agencies frequently require corroborating physical test data before certification approval.

Advanced simulation software demonstrates capability limitations in predicting nonlinear acoustic phenomena in complex geometries, particularly regarding transmission loss prediction in multi-layer composite structures utilized in modern vehicles. This validation requirement sustains demand for expensive physical testing facilities despite virtual testing advancement, creating a market structure where service providers must maintain dual capabilities, both physical and virtual, increasing operational complexity and requiring higher service pricing to offset infrastructure costs. The extended learning curve for CAE acoustic simulation, typically 12-24 months for engineers to achieve competency, creates talent availability constraints that limit service provider expansion and restrain market scaling.

Automotive Acoustic Engineering Services Market Trends and Opportunities

Autonomous Vehicle Development and Advanced Acoustic System Integration

The autonomous vehicle market, projected to encompass 60-70 million annual unit sales by 2040, represents a substantial growth opportunity for acoustic engineering service providers. Autonomous vehicles require fundamentally different acoustic engineering approaches, as absent human driver focus on road sounds creates requirements for enhanced cabin communication systems, warning sound design, and occupant comfort optimization in controlled acoustic environments. SAE Level 3-5 autonomous vehicles necessitate specialized acoustic engineering for passenger communication systems, external warning sounds for pedestrians, and premium cabin experiences that differentiate autonomous vehicle offerings.

Early autonomous vehicle development programs indicate that acoustic engineering and sound design services comprise 8-12% of total development costs, substantially higher than conventional vehicle programs. Market opportunities exist in specialized domains including synthetic sound design for autonomous vehicles, acoustic optimization of advanced driver assistance systems (ADAS) notifications, and human-machine interface acoustic engineering. Technology partnerships between major OEMs and acoustic engineering firms targeting autonomous vehicle platforms indicate growing service demand in this segment, with consulting revenue estimates of $180-220 million annually by 2030 within the autonomous vehicle acoustic engineering niche.

Automotive Acoustic Engineering Services Market Insights and Trends

System Insights

PEM Automotive Acoustic Engineering Servicess Dominate Revenue While SOFCs Drive Fastest Market Growth

Within the acoustic engineering services market, physical testing continues to hold a dominant position, accounting for more than 65% of total revenue. This leadership is supported by a well-established global testing infrastructure that includes anechoic and semi-anechoic chambers, reverberation rooms, and field-based acoustic measurement systems used for regulatory compliance and product validation. Regulatory authorities and automotive OEMs strongly favor experimental validation, relying on internationally recognized standards such as ISO 3744 and SAE J1169. Significant capital investments-typically ranging from US$3-8 million per facility-create high entry barriers, reinforcing the position of established service providers. Revenues are sustained through recurring demand for testing services, technician expertise, equipment calibration, and certification activities. While demand remains stable due to mandatory physical testing for vehicle approval, growth is moderating, with a projected CAGR of 7.5-8.5% through 2033.

In contrast, virtual testing represents the fastest-growing segment, expanding at an estimated CAGR of 11.2%. Advances in CAE software, computational power, and machine learning have enhanced simulation accuracy and reduced development timelines. Virtual acoustic analysis enables parallel engineering workflows, delivering measurable cost savings and schedule acceleration. However, regulatory validation requirements continue to necessitate physical testing confirmation, positioning virtual testing as a complementary, high-growth solution rather than a complete replacement.

Application Insights

Interior and Powertrain Acoustic Engineering Drive Market Leadership and Future Growth

Interior acoustic engineering represents the largest application segment, accounting for more than 35% of total revenue and maintaining a premium positioning across global vehicle programs. This dominance is driven by OEM focus on in-cabin comfort as a key differentiator, particularly in luxury and electric vehicles. Interior applications include cabin noise optimization, acoustic material selection, vibration isolation, and overall passenger compartment sound quality enhancement. As electrification reduces engine noise masking, manufacturers increasingly invest in advanced interior solutions such as active noise cancellation, EV-specific noise control, and premium cabin materials. These projects typically span four to eight months and require significant investment in advanced measurement tools and multidisciplinary expertise.

Powertrain acoustic engineering is the fastest-growing application, expanding at an estimated CAGR of 11.5%. Growth is fueled by rising EV penetration and the increasing acoustic complexity of electric motors, hybrid systems, and transmissions. Unlike conventional engines, electric powertrains generate high-frequency noise, demanding specialized expertise in motor acoustics, bearing noise, and thermal system optimization. Powertrain projects are longer and more complex, reflecting rising OEM budgets and the strategic importance of acoustic refinement in premium and electrified vehicles.

Regional Insights and Trends

Europe Leads Automotive Acoustic Engineering Through Regulation, Premium OEM Concentration, And Innovation

Europe holds a dominant position in the global automotive acoustic engineering services market, accounting for more than 45% of total revenue. This leadership is underpinned by harmonized regulatory frameworks such as EU Stage V and Euro 6 standards, alongside a dense concentration of premium automotive manufacturers. Decades of stringent noise-emission compliance have fostered deep-rooted acoustic engineering expertise, positioning Europe as the global benchmark for noise, vibration, and harshness (NVH) solutions.

Germany anchors regional activity, supported by extensive OEM research and development centers and a strong ecosystem of specialized acoustic consulting firms. Its engineering-driven culture and advanced technical education system enable highly sophisticated service offerings. The United Kingdom contributes around 12-15% of regional revenue, with specialization in niche areas such as aerospace-automotive acoustic crossover and advanced material acoustics. France and Spain account for roughly 8-12% and 6-10% respectively, driven by manufacturing hubs requiring compliance-oriented acoustic validation.

Strict exterior noise limits of 80 dB for passenger vehicles necessitate comprehensive pre-market acoustic testing across Europe. Simultaneously, EU sustainability and circular economy directives are accelerating investment in bio-based acoustic materials and lifecycle assessment methodologies. Harmonized regulations across member states allow service providers to scale efficiently through multinational delivery models, reinforcing competitive depth while supporting premium vehicle differentiation strategies across global luxury markets.

North America’s Automotive Acoustic Engineering Market Driven by Regulation, EV Innovation, and OEM Investment

North America represents a mature and well-established market for automotive acoustic engineering services. The United States dominates regional demand, supported by stringent noise emission regulations enforced by the Environmental Protection Agency and vehicle development and reporting requirements mandated by the National Highway Traffic Safety Administration. The strong concentration of global OEM headquarters, including General Motors, Ford Motor Company, Stellantis, and Tesla, further reinforces sustained investment in advanced acoustic engineering capabilities.

North American OEMs typically operate vertically integrated acoustic testing infrastructure, including anechoic chambers and advanced simulation labs, while also engaging specialized service providers to access niche expertise, advanced testing protocols, and additional capacity during peak development cycles. A predictable regulatory framework creates steady demand for compliance testing and documentation, while close technology partnerships between OEMs and engineering firms accelerate innovation in electric vehicle acoustics, autonomous vehicle sound design, and high-fidelity digital simulation. Increasing investment in cloud-based modeling, machine learning-enabled acoustic prediction, and vehicle-level optimization platforms highlights the region’s focus on digital transformation. Market growth is further supported by rising EV penetration, intensifying competition in premium vehicle segments, and stricter state-level standards-particularly in California-that exceed federal requirements and drive higher acoustic performance expectations.

Competitive Landscape

The automotive acoustic engineering services market demonstrates moderate consolidation characteristics, with significant presence of both large diversified engineering service firms and specialized acoustic consulting providers. Market concentration reflects capital-intensive business model requiring substantial infrastructure investment (testing facilities, simulation software, specialized expertise) creating barriers to market entry favoring established players. Five largest market players (Siemens PLM Software, Hexagon AB's MSC Nastran division, Ansys, Head Acoustics, EOSINT) collectively command approximately 22-28% market share, while remaining market share distributed among 50-70 regional and specialized service providers. This structure indicates moderately fragmented competitive landscape with declining trend toward consolidation, as mid-sized independent acoustic firms increasingly merge with larger engineering services organizations or specialize in niche domains insufficient for long-term independence.

Leading players distinguish themselves through integrated service delivery combining physical testing, virtual simulation, and consulting expertise; proprietary measurement methodologies and software solutions; and geographic reach supporting multinational OEM client relationships. Regional market leaders maintain competitive advantages through established relationships with local OEMs, regulatory familiarity, and language/cultural capabilities supporting customer engagement.

Key Industry Developments

- June 2024, Harman launched its advanced Car Acoustic Experience Lab in India, which focuses on various car audio needs, including engineering, research, and customer demonstrations, aimed at enhancing the overall automotive acoustic experience?.

- September 2023, EDAG Engineering expanded its service offerings by collaborating with major automotive manufacturers to develop customized acoustic solutions, focusing on improving interior sound quality.

Companies Covered in Automotive Acoustic Engineering Services Market

- Schaeffler Engineering GmbH

- Continental AG

- Robert Bosch GmbH

- AVL List GmbH

- FEV Group GmbH

- Adler Pelzer Holding GmbH

- Head acoustic GmbH

- Autoneum

- Bertrandt AG

- EDAG Engineering GmbH

- Harman International

- Other Market Players

Frequently Asked Questions

The Automotive Acoustic Engineering Services market is estimated to be valued at US$ 6.2 Bn in 2026.

The primary demand driver for the Automotive Acoustic Engineering Services market is the combined impact of increasingly stringent noise, vibration, and harshness (NVH) regulations and the rapid global transition toward electrified and software-defined vehicles.

In 2026, the Europe region will dominate the market with an exceeding 45% revenue share in the global Automotive Acoustic Engineering Services market.

Among applications, Interior has the highest preference, capturing beyond 35% of the market revenue share in 2026, surpassing other applications.

Schaeffler Engineering GmbH, Continental AG, Robert Bosch GmbH, AVL List GmbH FEV Group GmbH, Adler Pelzer Holding GmbH, and Head acoustic GmbH. There are a few leading players in the Automotive Acoustic Engineering Services market.