- Automotive

- Auto Repair Software Market

Auto Repair Software Market Size, Share, and Growth Forecast 2026 - 2033

Auto Repair Software Market by Application (Appointment Scheduling & Calendar Management, Inventory & Parts Management, Customer Relationship Management (CRM), Billing & Invoicing, Estimates & Work Order Management, Accounting & Financial Reporting, Technician Management & Productivity Tracking, Others), Organization Size (Small-Sized Enterprises, Medium-Sized Enterprises, Large Enterprises), End-user (Independent Auto Repair Shops, Auto Dealerships, Fleet Maintenance Operators, Auto Service Chains), Pricing Model and Regional Analysis, 2026 - 2033

Auto Repair Software Market Size and Trend Analysis

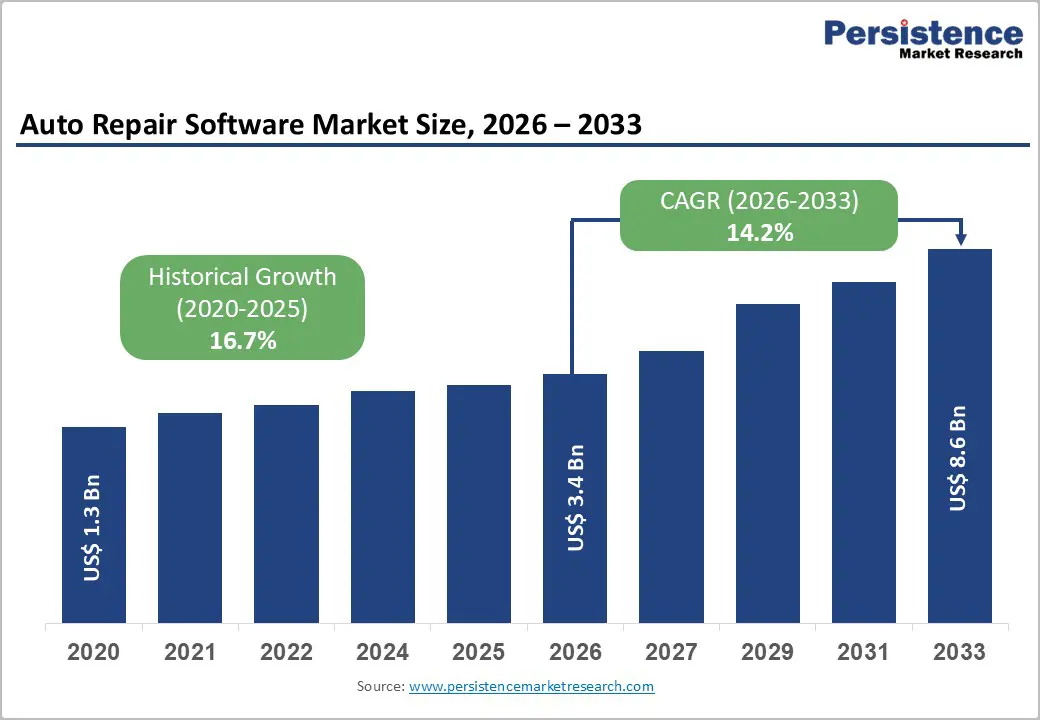

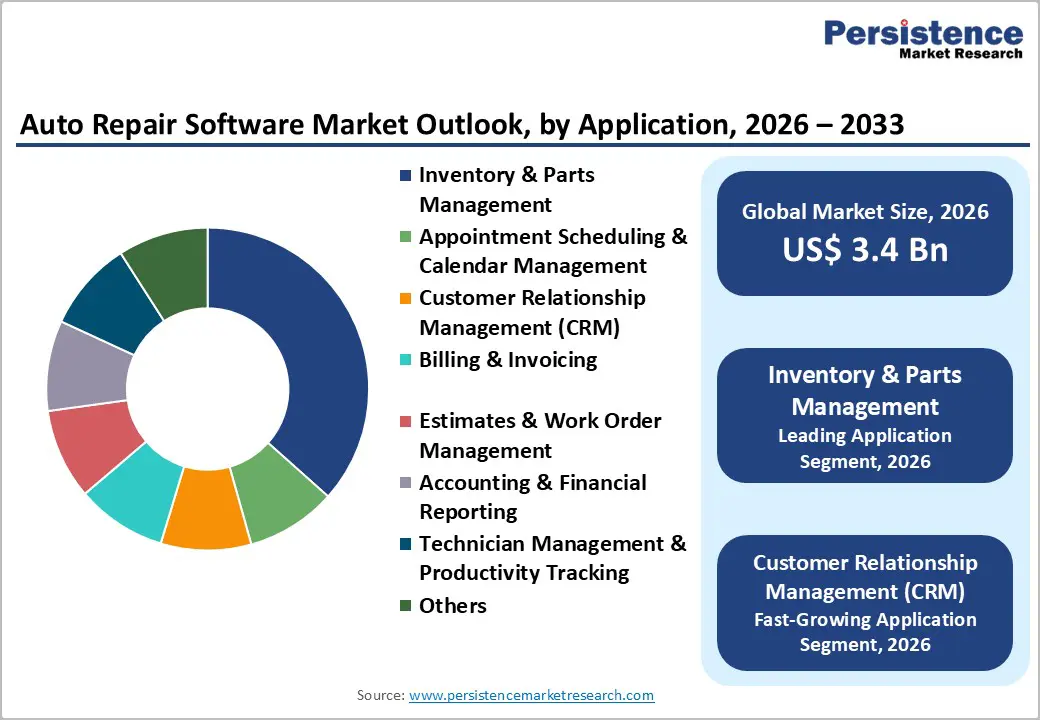

The global auto repair software market size is expected to be valued at US$ 3.4 billion in 2026 and projected to reach US$ 8.6 billion by 2033, growing at a CAGR of 14.2% between 2026 and 2033.

The market expansion is primarily driven by accelerating digital transformation in automotive service centers, with over 67% of small and medium-sized enterprises actively implementing automated workflow solutions to enhance operational efficiency. Additionally, cloud-based platforms account for approximately 63% of market demand in 2025, reflecting the industry’s decisive shift toward scalable, mobile-accessible repair management systems.

Key Industry Highlights:

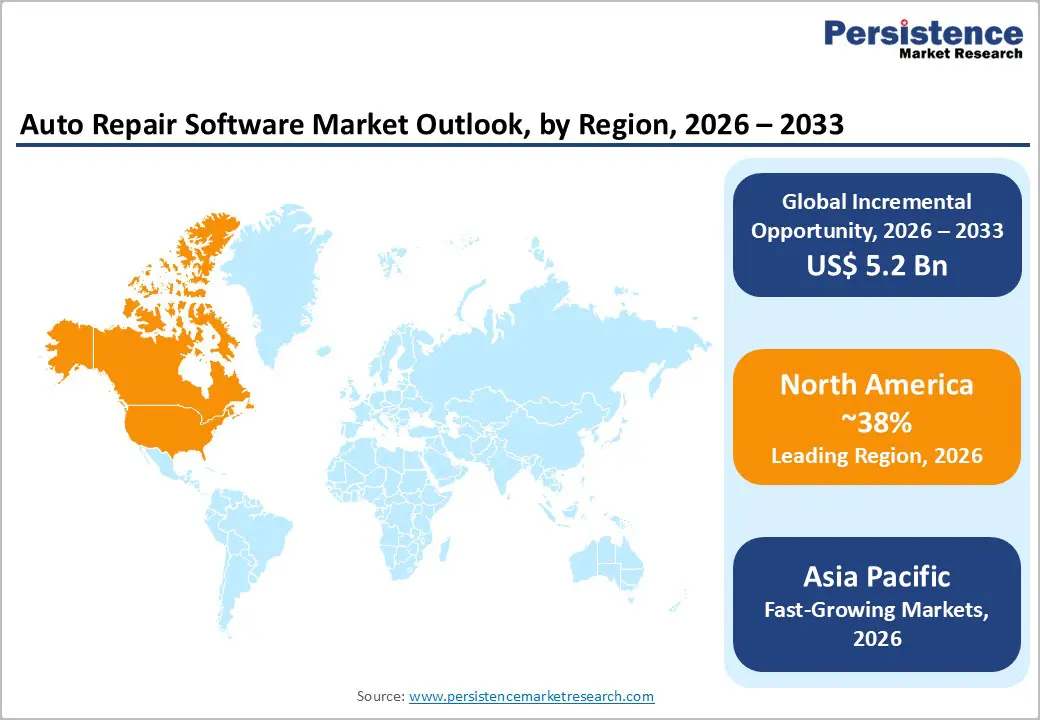

- Leading Region: North America leads global Auto Repair Software adoption with 38% market share in 2025, driven by high vehicle ownership rates exceeding 280 million vehicles, mature aftermarket infrastructure, and widespread digital transformation with over 71% of U.S. repair shops utilizing digital invoicing and service management tools.

- Fastest Growing Region: Asia Pacific represents fastest-growing regional market projected to expand at 15.4% CAGR through 2033, propelled by rapid urbanization, expanding middle-class vehicle ownership, aggressive EV adoption, with China reporting 45% sales increase, and government-supported digitalization initiatives across manufacturing and service sectors.

- Dominant Segment: Inventory & Parts Management application dominates market with approximately 38% share in 2025, reflecting critical importance of efficient parts procurement for shop profitability, with independent businesses performing 75% of aftermarket repairs requiring sophisticated real-time availability checking and automated reorder capabilities.

- Emerging Segment: Cloud-based Subscription Licensing emerges as the fastest-growing pricing model, commanding 68% share in 2025, accelerating at 17.1% CAGR driven by predictable monthly costs, continuous updates, flexible scaling, and elimination of large capital expenditures preferred by over 67% of implementing SMEs.

- Key Opportunity: Electric vehicle service specialization presents a transformative opportunity as EV fleet expands 47% annually in Europe and 45% in China, with each repair averaging 50% higher cost than conventional vehicles, creating demand for specialized software modules supporting battery diagnostics, thermal management, and high-voltage safety protocols.

| Key Insights | Details |

|---|---|

|

Auto Repair Software Market Size (2026E) |

US$ 3.4 billion |

|

Market Value Forecast (2033F) |

US$ 8.6 billion |

|

Projected Growth CAGR (2026-2033) |

14.2% |

|

Historical Market Growth (2020-2025) |

16.7% |

Market Dynamics

Drivers - Rapid Digital Transformation and Cloud Adoption Across Auto Repair Operations

Digital transformation has emerged as the cornerstone of modern auto repair operations, with cloud-based software platforms fundamentally reshaping shop management practices. According to industry data, over 71% of U.S. repair shops now rely on digital invoicing and service management tools, demonstrating widespread acceptance of software-driven workflows. The migration to cloud infrastructure offers substantial operational advantages, including real-time data synchronization across multiple locations, remote accessibility for shop owners and technicians, and elimination of costly on-premises hardware maintenance.

Cloud solutions enable repair shops to access critical diagnostic information, customer records, and inventory data from any internet-connected device, facilitating mobile mechanics and improving service response times. Furthermore, 59% adoption rate for cloud-based platforms indicates strong market momentum, with independent shops particularly benefiting from reduced upfront capital expenditure and seamless software updates that eliminate compatibility issues with evolving vehicle technologies.

Growing Vehicle Complexity and Aging Fleet Driving Demand for Advanced Diagnostic Tools

Modern vehicles incorporate increasingly sophisticated electronic systems, advanced driver assistance technologies, and complex software architectures that demand specialized diagnostic capabilities. The average vehicle age in the United States reached a record 12.8 years in 2025, extending a multi-year upward trend that amplifies maintenance requirements and repair frequency. According to the U.S. Department of Transportation, this aging fleet generates sustained demand for comprehensive repair management solutions capable of handling intricate fault diagnosis across diverse vehicle models and vintages.

The Bureau of Labor Statistics projects the automotive repair industry to grow by 6% from 2021 to 2031, underscoring robust structural demand. Auto repair software equipped with integrated diagnostic modules, manufacturer-specific repair procedures, and real-time technical service bulletins enables technicians to address complex electrical and mechanical issues efficiently. Additionally, the proliferation of electric and hybrid vehicles introduces novel service requirements such as high-voltage battery diagnostics and thermal management system maintenance, compelling repair facilities to adopt software platforms with specialized EV-specific modules and safety protocols.

Restraints - High Initial Investment and Implementation Costs for Small Independent Shops

Cost barriers represent a significant adoption challenge, particularly for small independent repair shops operating on tight profit margins. Approximately 56% of small repair facilities consider advanced software tools cost-prohibitive, with integrated artificial intelligence diagnostics, cloud-based analytics, and comprehensive parts management modules commanding premium subscription fees. Initial implementation expenses encompass not only software licensing fees but also hardware infrastructure upgrades, data migration services, and staff training programs required to achieve operational proficiency.

For establishments with limited capital budgets, monthly subscription costs ranging from $50 to $300 per technician can strain financial resources, especially when combined with other operational expenses. Additionally, hidden costs associated with third-party integrations, payment processing fees, and ongoing technical support services further elevate total cost of ownership. This economic pressure forces budget-constrained shops to either delay digitalization initiatives or settle for basic software packages lacking essential features, creating a competitive disadvantage relative to larger chains that can leverage economies of scale.

Shortage of Skilled Technicians and Digital Literacy Challenges

The automotive service industry confronts a persistent workforce shortage that directly impairs software adoption and utilization effectiveness. Data from TechForce Foundation indicates that retirements outpace new entrants, with a projected shortage of multiple unfilled positions by 2031. Compounding this scarcity, approximately 41% of shop owners cite training difficulties as major barriers, with 44% of technicians struggling to adapt to modern software platforms, including inventory automation, digital inspection reporting, and cloud-based diagnostic tools.

The aging workforce profile, with approximately 50% of car technicians around 40 years old, often correlates with resistance to new technology adoption and preference for traditional paper-based processes. Shop operators must allocate substantial resources to comprehensive training programs, yet even with investment, operational inefficiencies and user resistance can persist during transition periods. This skills gap creates particular challenges in effectively leveraging advanced features such as predictive maintenance algorithms, customer relationship management automation, and data-driven performance analytics, ultimately limiting return on software investment.

Opportunity - Electric Vehicle Service Market Expansion Creating Specialized Software Demand

The accelerating transition to electric mobility presents transformative growth opportunities for auto repair software providers capable of delivering EV-specific functionality. According to the European Commission, battery-only electric passenger cars increased by 47% between late 2022 and late 2023, approaching 4.5 million vehicles. In China, electric vehicle sales surged 45% according to the China Association of Automobile Manufacturers (CAAM), positioning Asia Pacific as a critical growth market.

While electric vehicles require fewer routine maintenance services compared to internal combustion engines, each repair averages almost 50% higher cost due to battery system complexity and specialized high-voltage safety requirements. This dynamic creates substantial demand for software platforms incorporating EV-specific modules such as battery health monitoring, thermal management diagnostics, charging system analysis, and over-the-air software update capabilities. Forward-thinking software developers can capture market share by offering integrated solutions that address both traditional mechanical repairs and emerging EV service needs, enabling multi-brand repair facilities to efficiently service mixed vehicle fleets without requiring separate software systems.

Fleet Management Integration and Commercial Vehicle Digitalization

Commercial fleet operations represent a high-value market segment experiencing rapid digital transformation, with fleet management software projected to grow at a 20% CAGR through 2033. Fleet operators face mounting pressure to minimize vehicle downtime, optimize maintenance scheduling, and ensure regulatory compliance across distributed vehicle populations. Auto repair software providers can capitalize on this opportunity by developing seamless integrations with leading fleet management platforms such as Verizon Connect, Trimble, and Geotab, enabling automated service scheduling based on telematics data, predictive maintenance alerts, and centralized repair history tracking.

Commercial fleet customers, representing 57% of fleet management market share in 2025, demand sophisticated features including multi-location service coordination, bulk parts procurement optimization, and compliance reporting for industries such as logistics, construction, and transportation. Software vendors that establish partnerships with fleet management providers and deliver specialized commercial vehicle modules can secure long-term enterprise contracts with recurring revenue streams substantially larger than individual shop subscriptions.

Category-wise Analysis

Application Insights

Inventory & Parts Management dominates the Auto Repair Software market, accounting for approximately 38% market share in 2025, due to its direct influence on shop efficiency and profitability. Repair operations depend heavily on timely parts availability to avoid service delays and revenue loss. Advanced inventory modules enable real-time stock visibility, automated reordering based on usage trends, supplier price comparison, and core return tracking, supporting tighter cost control. With parts margins typically ranging between 20% and 28%, accurate cost and markup management remains critical. Cloud-enabled inventory systems further support multi-location operations by allowing centralized procurement, inter-branch transfers, and improved purchasing leverage, making this application segment a core operational priority.

Organization Size Insights

Small-sized enterprises represent the largest organization-size segment, holding around 42% market share in 2025, reflecting the fragmented structure of the global auto repair industry. These businesses typically operate with limited staff and capital, prioritizing software solutions that are affordable, intuitive, and quick to deploy. Cloud-based SaaS platforms are particularly attractive due to low upfront costs, predictable monthly pricing, and minimal IT requirements. Small shops increasingly adopt digital tools to streamline scheduling, inspections, invoicing, and customer communication. By digitizing core workflows, small operators enhance productivity and customer experience, allowing them to compete more effectively with larger service chains and dealership service centers.

End-user Insights

Independent auto repair shops account for approximately 55% market share in 2024, making them the dominant end-user segment. These shops handle the majority of out-of-warranty repairs and routine maintenance, competing on pricing flexibility and personalized service. Software adoption enables independents to access standardized repair data, diagnostics, and service documentation, narrowing the technology gap with dealerships. Tools such as digital vehicle inspections, automated service reminders, and transparent estimates strengthen customer trust and retention. As consolidation intensifies and operating costs rise, independent shops increasingly rely on software-driven efficiency and differentiation to sustain margins and protect market position.

Pricing Model Analysis

Subscription licensing leads the pricing model landscape with around 68% market share in 2025, reflecting strong preference for software-as-a-service delivery. Subscription models offer predictable monthly expenses, continuous feature upgrades, and automatic compatibility with evolving vehicle technologies, reducing operational risk for repair shops. For multi-location operators and franchises, subscriptions scale easily across sites without large capital commitments. From the vendor perspective, recurring revenue supports sustained investment in innovation, including AI-driven diagnostics and workflow automation. This model also ensures consistent software updates and security compliance, reinforcing long-term adoption and customer retention.

Regional Insights

North America Auto Repair Software Market Trends and Insights

North America maintains market leadership with approximately 38% revenue share in 2025, propelled by high vehicle ownership rates, mature automotive aftermarket infrastructure, and early technology adoption among service providers. The United States specifically dominates regional demand, with the U.S. automotive service market expected to reach US$ 199.38 billion in 2025, creating substantial downstream demand for management software. Over 71% of U.S. repair shops utilize digital invoicing and service management tools, demonstrating widespread digital maturity.

Regulatory frameworks significantly shape market dynamics, with Federal Motor Carrier Safety Administration (FMCSA) electronic logging device mandates driving fleet management software adoption that integrates with repair scheduling systems. The average United States vehicle age reached 12.8 years in 2025, generating consistent maintenance demand that supports software investment returns. OEM dealerships retained 41.64% channel share in 2024 by leveraging connected car diagnostics and warranty coverage, compelling independent shops to adopt sophisticated software platforms to remain competitive. Major software providers including Mitchell 1, ALLDATA, and Tekmetric maintain strong market presence, with ALLDATA serving over 400,000 technicians across more than 115,000 shops globally, demonstrating deep market penetration.

Europe Auto Repair Software Market Trends and Insights

Europe represents the second-largest regional market with approximately 28% share in 2025, characterized by stringent emissions regulations, data privacy requirements, and diverse multi-country operational complexities. Germany, with 49.1 million vehicles on roads as of early 2024 representing the highest ever recorded, leads European demand for sophisticated repair management software capable of handling complex regulatory compliance reporting and manufacturer-specific service protocols across premium automotive brands.

The European Union’s Alternative Fuels Infrastructure Regulation passed in May 2025 mandates installation of electric vehicle charging infrastructure, accelerating EV adoption and creating demand for software platforms with specialized electric vehicle diagnostic modules. United Kingdom, France, and Spain constitute additional key markets, each exhibiting distinct characteristics in terms of independent shop versus dealership service market share. European repair facilities prioritize software features supporting General Data Protection Regulation (GDPR) compliance for customer data management, multi-language user interfaces accommodating diverse technician populations, and integration with regional parts distribution networks. The regulatory harmonization across EU member states facilitates software standardization opportunities while varying labor rate structures and parts pricing models across countries require flexible configuration capabilities.

Asia Pacific Auto Repair Software Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, projected to expand at 15.4% CAGR through 2033, driven by rapid urbanization, expanding middle-class vehicle ownership, and aggressive digitalization initiatives across manufacturing and service sectors. China accounts for over 60% of regional revenue, generating approximately US$ 139.2 billion in 2024, with electric vehicle sales increasing 45% according to CAAM, fundamentally reshaping service requirements and software feature priorities.

India and Southeast Asian economies demonstrate particularly strong growth momentum as automotive aftermarket services modernize and consolidate. Government initiatives supporting smart mobility and digital transformation, combined with substantial investments from domestic technology firms and automakers, accelerate software adoption across independent repair facilities and authorized service centers.

The region benefits from cost-competitive software development capabilities and growing domestic software providers tailoring solutions to local market requirements, including integration with regional payment systems, local language support, and adaptation to price-sensitive customer segments. Mobile repair services and on-demand automotive assistance platforms proliferate across densely populated urban centers, creating demand for mobile-optimized software applications enabling technicians to access diagnostic information, update repair status, and process payments from customer locations rather than fixed shop facilities.

Competitive Landscape

The auto repair software market is moderately fragmented, characterized by a large base of regional vendors and niche solution providers operating alongside a limited number of established platforms with broad user adoption. Market structure reflects low entry barriers for basic shop management tools, but increasing differentiation at the advanced functionality level. Competition is primarily driven by product depth, ease of use, and ecosystem integration, as repair shops seek unified platforms that streamline operations without adding complexity.

Business strategies increasingly emphasize cloud-native architectures, enabling faster feature deployment, scalability, and subscription-based monetization. Vendors are investing in intelligent capabilities such as AI-assisted diagnostics, data-driven service recommendations, and mobile-first workflows to enhance technician productivity and customer experience. Strategic alliances with parts distributors, diagnostic equipment providers, and fleet platforms are used to strengthen value propositions and increase switching costs. Additionally, providers are expanding beyond core repair management by integrating payments, customer engagement, and financing tools, positioning their platforms as end-to-end operating systems for repair businesses.

Key Developments

- November 2024: Collaboration Enhancement (ALLDATA and Mitchell ProDemand) ALLDATA announced collaboration with Mitchell ProDemand to enable synchronized access to repair information and parts pricing across repair workflows for participating shops, enhancing operational efficiency.

- May 2025: Platform Evolution (Shop-Ware) Shop-Ware unveiled Shop-Ware 2.0, delivering cloud-native architecture with expanded integrations to OEM data providers and redesigned mobile interface to improve technician efficiency and vehicle data accessibility.

- 2024: Artificial Intelligence Integration (Shopmonkey) Shopmonkey launched an AI-based smart scheduling tool, adopted by 63% of its client base, enabling automatic job assignments based on technician availability and job priority, significantly improving shop workflow optimization.

Companies Covered in Auto Repair Software Market

- Mitchell1 Manager SE

- ALLDATA

- Protractor

- Shop-Ware

- Tekmetric

- NAPA TRACS

- AutoFluent

- RepairShopr

- AutoVitals

- Bolt On Technology

- AutoLeap

- Shopmonkey

- Fullbay

- CalendX

- AutoRepair Pro

- GEM-CAR

- R.O. Writer

- Identifix

- Workshop Software

- Garage360

Frequently Asked Questions

The market is expected to reach US$ 3.4 billion in 2026 and grow to US$ 8.6 billion by 2033 at a 14.2% CAGR.

Demand is driven by rapid digital transformation, rising vehicle complexity and aging fleets, strong cloud adoption, and increasing electric vehicle servicing requirements.

North America leads the market with around 38% share in 2025, supported by high vehicle ownership and widespread use of digital service management tools.

The fastest-growing opportunity lies in electric vehicle service software, driven by rapid EV adoption and higher repair complexity and costs.

Leading market players include ALLDATA, Mitchell1 Manager SE, Tekmetric, Shopmonkey, AutoLeap, Shop-Ware, NAPA TRACS, AutoVitals, etc.