- Industrial Goods & Service

- Atmospheric Water Generator Market

Atmospheric Water Generator Market Size, Share, and Growth Forecast 2026 - 2033

Atmospheric Water Generator Market by Product Type (Static, Mobile), by Technology (Cooling Condensation, Wet/Liquid Desiccation), by Capacity (1L-500L, 500L-1000L, 1000L-5000L, 5000L-10,000L), Distribution Channel (Direct, Indirect), End-user (Residential, Commercial, Industrial), and Regional Analysis, 2026 - 2033

Atmospheric Water Generator Market Size and Trend Analysis

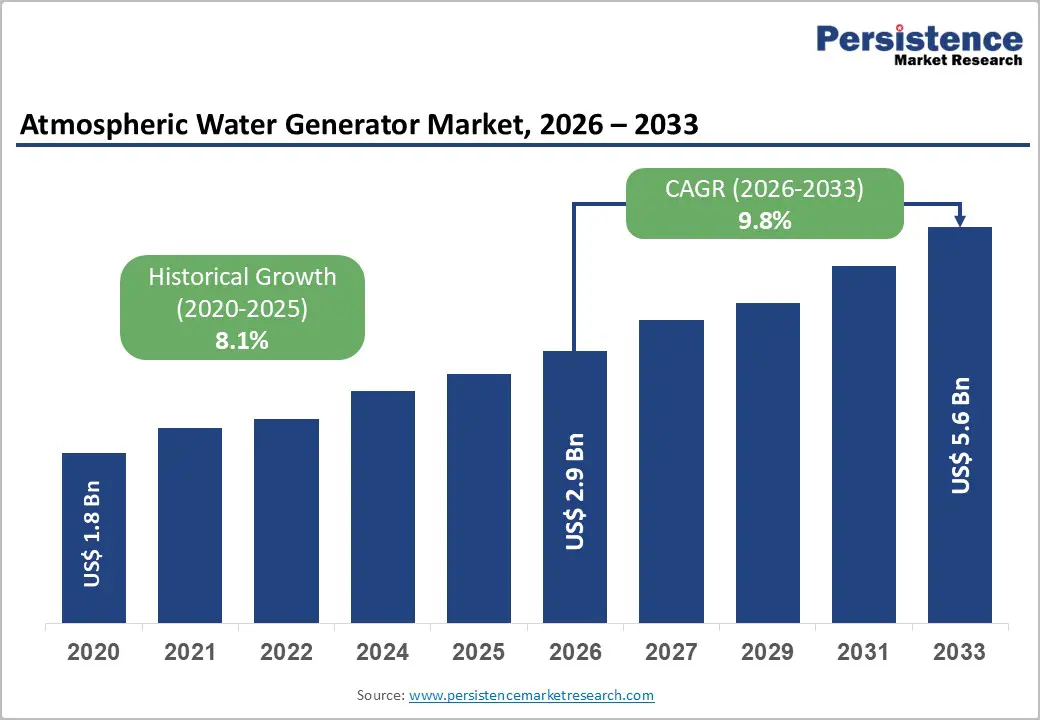

The global atmospheric water generator market size is likely to be valued at US$ 2.9 Billion in 2026 and is expected to reach US$ 5.6 Billion by 2033, growing at a CAGR of 9.8% during the forecast period from 2026 to 2033.

This robust growth is fundamentally underpinned by an accelerating global freshwater crisis, escalating demand for decentralized off-grid water solutions, and advancing energy efficiency in atmospheric water harvesting technologies.

Key Market Highlights

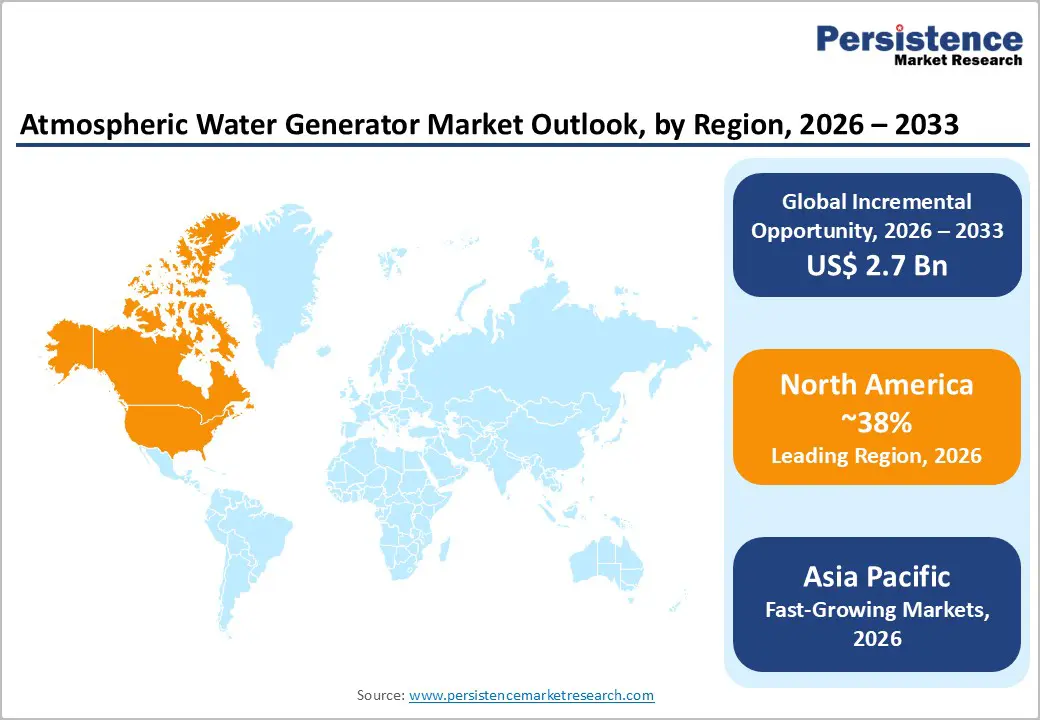

- Leading Region: North America leads the global Atmospheric Water Generator Market holding 38% share, driven by U.S. EPA documented water shortage risks across 40+ states, strong DoD institutional procurement, and an advanced innovation ecosystem anchored by EcoloBlue, Inc., Drinkable Air, and Air 2 Water Solutions.

- Asia Pacific is the fastest-growing region with rising CAGR of 11.2%, propelled by India's Jal Jeevan Mission, China's AWG materials research, high-humidity ASEAN island markets, and over 600 million people in the region lacking reliable access to safe drinking water per WHO/UNICEF JMP data.

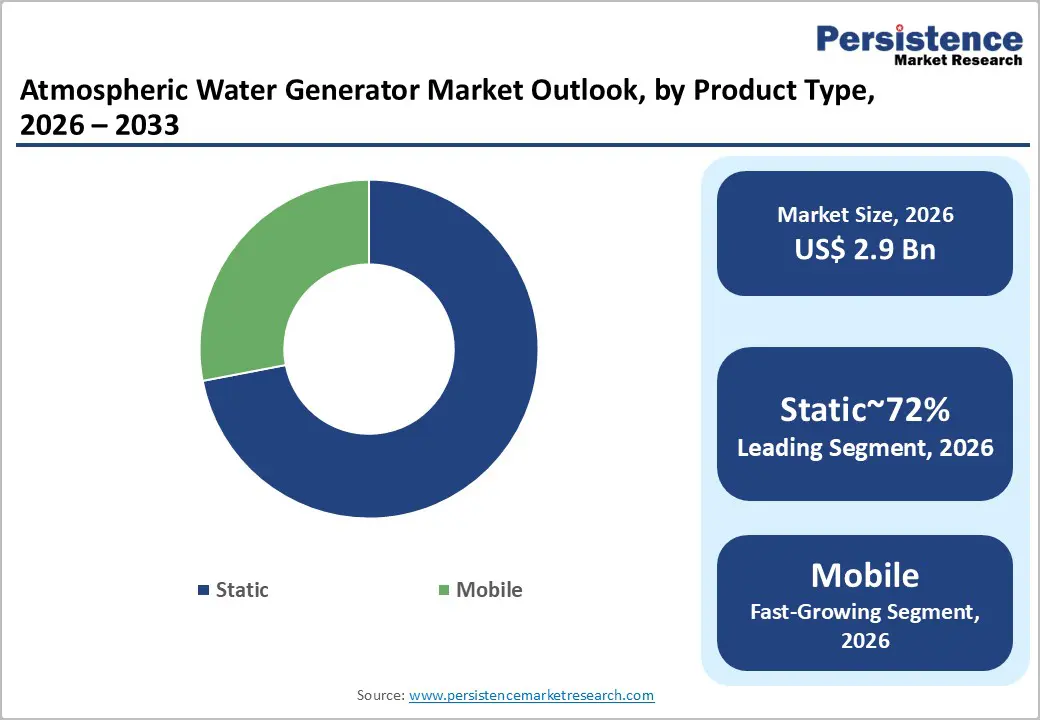

- Static atmospheric water generators dominate with approximately 72% product type market share, preferred for residential and commercial fixed installations due to superior energy efficiency, higher daily water output, and compatibility with multi-stage WHO-compliant water purification architectures.

- The Industrial end-use segment is the fastest-growing category, driven by remote mining, oil & gas, and manufacturing operations in water-scarce regions requiring self-sufficient potable water supply independent of municipal infrastructure, supported by solar-integrated large-capacity AWG deployments.

- The key market opportunity lies in solar-powered AWG systems for off-grid communities, with IRENA reporting a 90%+ decline in solar PV costs since 2010, making solar-integrated AWG increasingly viable for World Bank and ADB-funded rural water access programs targeting SDG 6 by 2030.

| Key Insights | Details |

|---|---|

| Atmospheric Water Generator Market Size (2026E) | US$ 2.9 Billion |

| Market Value Forecast (2033F) | US$ 5.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 9.8% |

| Historical Market Growth (2020 - 2025) | 8.1% |

Market Dynamics

Drivers - Worsening Global Water Scarcity and Deteriorating Groundwater Resources

The rapid depletion and contamination of traditional freshwater sources are making atmospheric water generation an increasingly important alternative water supply solution. According to the Joint Monitoring Programme (JMP) of the World Health Organization and UNICEF, nearly 785 million people worldwide still lack access to basic drinking water services. At the same time, climate-driven changes in rainfall patterns are intensifying water stress even in regions that historically had reliable water resources.

The Intergovernmental Panel on Climate Change projects that global warming of 1.5°C above pre-industrial levels could significantly reduce freshwater availability across Southern Europe, Sub-Saharan Africa, and South Asia. In addition, the Food and Agriculture Organization has highlighted the accelerating depletion of major aquifers that support agriculture and urban water supply. Atmospheric water generators capture humidity directly from the air, providing a pipeline-independent and drought-resilient water source. As a result, they are becoming an attractive solution for residential, commercial, and humanitarian applications in regions facing increasing water scarcity.

Rising Military, Disaster Relief, and Remote Industrial Applications Driving Mobile Unit Demand

Beyond residential and commercial applications, government procurement for military operations, disaster relief efforts, and remote industrial installations is creating strong demand for atmospheric water generator systems, particularly mobile units. The United States Department of Defense has identified atmospheric water harvesting as a strategic capability for ensuring water independence at forward operating bases, helping reduce reliance on vulnerable supply chains in conflict zones.

After major disasters such as floods, cyclones, and earthquakes, organizations like the United Nations Office for the Coordination of Humanitarian Affairs and other international relief agencies deploy mobile atmospheric water units to restore access to safe drinking water when infrastructure collapses. According to the World Meteorological Organization, the number of climate-related disasters has increased fivefold over the past 50 years. This rising frequency of extreme weather events is encouraging governments and humanitarian organizations to allocate larger budgets for portable and self-sufficient water generation systems capable of supporting emergency and remote operations.

Restraints - High Energy Consumption Limiting Cost Competitiveness in Price-Sensitive Markets

One of the major challenges limiting the widespread adoption of atmospheric water generators is their relatively high energy consumption, especially for cooling condensation-based systems. A typical residential cooling condensation AWG that produces around 30 liters of water per day generally consumes between 0.3 and 0.5 kilowatt-hours of electricity per liter of water generated. This energy requirement is significantly higher than the energy cost associated with conventional centralized water treatment and distribution systems.

In regions where electricity tariffs are high or power supply is unreliable, the operational cost of atmospheric water generation can exceed the cost of other water sources such as bottled water, desalinated water, or rainwater harvesting systems. This cost challenge often discourages price-sensitive residential consumers and small commercial users from adopting the technology. As a result, although AWG technology offers long-term benefits, its higher operating costs remain a major barrier to large-scale adoption in developing and electricity-constrained markets.

Dependence on Ambient Humidity Levels Restricts Deployment

Another key limitation of atmospheric water generators is their dependence on ambient humidity levels for efficient operation. Cooling condensation-based AWG systems, which represent the most widely used technology, typically require a minimum relative humidity of around 40% to function effectively, while optimal performance is usually achieved when humidity levels exceed 60%.

This natural limitation restricts the deployment of AWG systems in extremely dry or hyper-arid regions such as the Sahara Desert, the Arabian Peninsula, and certain inland continental areas. Ironically, these are often the regions where water scarcity is most severe. In addition, seasonal fluctuations in humidity levels can lead to inconsistent water production throughout the year. This variability creates uncertainty in output forecasts and makes it difficult for institutions and investors to calculate reliable returns on investment. As a result, financing and large-scale deployment of AWG systems in climatically challenging regions can become more complicated.

Opportunities - Solar-Powered Atmospheric Water Generation for Off-Grid and Rural Communities

The combination of falling solar photovoltaic costs and improving atmospheric water generation technology is creating significant opportunities for energy-independent water production in remote and underserved regions. According to the International Renewable Energy Agency, the global average cost of solar PV electricity has declined by more than 90% between 2010 and 2023. This dramatic cost reduction makes solar-integrated atmospheric water generators increasingly viable for off-grid communities.

The United Nations Sustainable Development Goal 6 aims to ensure universal access to safe and affordable drinking water by 2030, which has encouraged funding from institutions such as the World Bank and the Asian Development Bank for innovative water solutions. Companies developing solar-powered AWG systems capable of operating in lower humidity conditions, particularly through advanced desiccant or hybrid technologies, are well positioned to secure contracts from rural water access programs across Sub-Saharan Africa, South Asia, and ASEAN island regions where both electricity grids and piped water infrastructure remain limited.

Growing Demand from Commercial Real Estate and Smart Building Integration

The commercial sector, including hotels, office complexes, airports, hospitals, and educational institutions, is emerging as one of the fastest-growing end-use segments for atmospheric water generators. This growth is largely driven by sustainability initiatives, green building certification requirements, and corporate commitments toward responsible water management. Certification systems such as U.S. Green Building Council’s LEED standards and the Building Research Establishment’s BREEAM framework encourage the use of innovative water efficiency technologies, including atmospheric water generation.

According to the World Green Building Council, the global green building market is valued in hundreds of billions of dollars and continues to expand rapidly. Large-capacity AWG installations, typically producing between 500 and 5,000 liters per day, are well-suited for commercial building water requirements. These systems allow property owners to reduce dependence on municipal water supply, lower operational costs, and strengthen environmental, social, and governance (ESG) reporting, making them attractive for modern sustainable building projects.

Category-wise Analysis

Product Type Insights

Static atmospheric water generators lead the product type segment, accounting for an estimated 72% of total market revenue. These systems are designed for fixed installation in residential buildings, commercial facilities, and industrial locations. Static units benefit from stable grid power, larger storage tanks, and optimized humidity intake systems, allowing them to generate consistent and high volumes of water. Their long-term installation capability and lower cost per liter of water, especially at higher capacities, make them a preferred option for organizations seeking alternatives or supplements to municipal water supply.

The static systems can easily integrate with existing building plumbing and filtration infrastructure, making them suitable for large commercial and institutional environments. Compliance with WHO-recommended multi-stage filtration, including UV purification and reverse osmosis, is also easier to implement in these fixed systems. This advantage strengthens buyer confidence and further increases the demand for static atmospheric water generator installations.

Technology Insights

Cooling condensation technology dominates the technology segment, accounting for approximately 78% of the global market share. This technology works by cooling incoming air below its dew point using a refrigeration cycle. When the air cools, moisture condenses on cold surfaces and is collected as liquid water. The technology is widely used because it is mature, reliable, and supported by well-established manufacturing supply chains. Cooling condensation systems can operate across a wide humidity range, typically performing effectively from around 35% relative humidity, which makes them suitable for diverse climatic conditions.

Another important advantage is the lower capital cost compared with alternative technologies such as liquid or wet desiccation systems. Technical guidelines from the American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) help standardize the design and testing of condensation-based air treatment equipment. These standards improve product reliability and increase buyer confidence, making cooling condensation the most widely adopted technology globally.

Capacity Analysis

The 1L-500L per day capacity segment leads the market, representing around 45% of total capacity-segment revenue. This dominance is mainly driven by the large number of residential and small commercial installations in urban and semi-urban regions. Atmospheric water generators in this capacity range are designed to meet the needs of households, small offices, and small retail establishments. They offer affordable price points, compact sizes, and water output levels that match typical daily water consumption patterns.

According to the World Health Organization (WHO), average household water consumption ranges between 50 and 100 liters per person per day, which aligns well with the production capacity of these systems. Increasing awareness of safe drinking water, especially across Asia Pacific and the Middle East, is encouraging more households to adopt atmospheric water generation technology. At the same time, falling costs of key components such as refrigeration compressors and filtration materials are making residential AWG units more affordable, further expanding demand in emerging economies.

Distribution Channel Analysis

The direct distribution channel dominates the Atmospheric Water Generator Market, accounting for approximately 62% of total revenue. Direct sales include manufacturer-to-end-user transactions, B2B procurement agreements, government tenders, and turnkey project installations. This channel is widely used by commercial, industrial, and institutional customers who require customized system configurations, on-site installation, regulatory documentation, and long-term maintenance services. Atmospheric water generators, particularly mid- and large-capacity systems producing more than 1,000 liters per day, involve significant capital investment and technical specifications.

As a result, buyers typically prefer direct engagement with manufacturers to negotiate system design, warranty terms, water quality certifications, and service agreements. Direct distribution also allows companies to provide tailored solutions based on site conditions and water demand. Leading companies such as Watergen and Water Technologies International, Inc. maintain dedicated B2B and B2G sales teams to work with municipal authorities, defense organizations, and large commercial infrastructure developers.

End-user Insights

The commercial segment holds the largest share in the Atmospheric Water Generator Market, accounting for approximately 41% of total demand. Commercial users include hotels, resorts, corporate offices, shopping complexes, hospitals, schools, and food service establishments. These organizations require a reliable and safe source of drinking water to support daily operations and maintain service quality. Atmospheric water generators allow commercial facilities to produce clean drinking water on-site, reducing dependence on bottled water deliveries and lowering municipal water expenses.

Many companies are also adopting AWG systems to support their environmental, social, and governance (ESG) sustainability goals. According to the World Health Organization (WHO), access to safe drinking water is a basic human right, which has encouraged regulators to push commercial organizations to ensure dependable water access. In water-stressed tourism regions such as the Middle East and parts of the Mediterranean, hotels are increasingly installing AWG systems as part of sustainability certification programs to reduce environmental impact and strengthen water security.

Regional Insights

North America Atmospheric Water Generator Market Trends

The United States leads the North American Atmospheric Water Generator Market, driven by growing awareness about water supply vulnerabilities and infrastructure challenges. Events such as the Flint, Michigan water contamination crisis have increased public and government attention on water quality and supply reliability. At the same time, severe drought conditions across the western United States have accelerated interest in alternative water generation technologies.

According to the U.S. Environmental Protection Agency (EPA), more than 40 states could experience water shortages in the coming decade under moderate drought scenarios. This outlook has encouraged both private and public sector organizations to explore atmospheric water generation systems. California’s drought management programs and incentives supporting water recycling and alternative supply technologies also support AWG adoption. The U.S. Department of Defense (DoD) is among the largest institutional buyers of mobile AWG systems, using them for military logistics and disaster response. Canada is also exploring AWG solutions to improve drinking water access in remote Indigenous communities.

Europe Atmospheric Water Generator Market Trends

Europe’s Atmospheric Water Generator Market is expanding steadily, supported by sustainability initiatives and climate resilience policies across the region. The European Green Deal promotes water conservation, circular water use, and climate adaptation infrastructure, which creates favorable conditions for alternative water technologies such as AWGs. Countries including Spain and southern France are facing increasing water stress due to shifting Mediterranean climate patterns.

According to the European Environment Agency (EEA), southern Europe experiences the most severe water shortages on the continent, driving demand for new water supply solutions in tourism, agriculture, and municipal infrastructure. Germany is also exploring AWG integration within smart building frameworks as part of its broader Energiewende sustainability strategy. Additionally, policies such as the EU Water Framework Directive and the EU Strategy on Adaptation to Climate Change (2021) encourage investment in diversified water sources. These regulatory initiatives are helping increase the adoption of atmospheric water generators across public infrastructure and commercial facilities.

Asia Pacific Atmospheric Water Generator Market Trends

Asia Pacific is the fastest-growing regional market for atmospheric water generators. The region has the largest population lacking reliable access to safe drinking water, which creates strong demand for decentralized water generation technologies. Rapid urbanization across developing economies is also placing pressure on existing water infrastructure systems. India represents a particularly promising market due to government initiatives such as the Jal Jeevan Mission, which aims to provide piped drinking water to every rural household.

In regions where pipeline infrastructure is difficult or expensive to install, atmospheric water generators are emerging as a practical alternative. Domestic companies such as WaterMaker India Pvt. Ltd. and Akvo Atmospheric Water Systems Pvt. Ltd. are expanding production to serve institutional and government buyers. Meanwhile, China is investing heavily in advanced atmospheric water harvesting research. Universities such as Tsinghua University are developing innovative materials that can improve moisture capture efficiency, even in lower humidity environments.

Competitive Landscape

The global Atmospheric Water Generator Market has a highly fragmented competitive structure, with many small and medium-sized specialized manufacturers operating alongside a few globally recognized companies. Key industry players include Watergen and EcoloBlue, Inc., which have established strong international presence through advanced product portfolios and strategic partnerships. Companies compete based on several factors such as water generation capacity, energy efficiency, filtration system quality, and solar integration capabilities.

The availability of strong after-sales service networks is also an important competitive advantage, particularly for large institutional clients. Leading companies are expanding into water-stressed regions through government partnerships, humanitarian organization projects, and regional distributor networks. Emerging business models are also shaping the market, including water-as-a-service subscription models, leasing arrangements for institutional customers, and integrated solar-AWG project financing. At the same time, ongoing research and development efforts focus on reducing energy consumption, expanding operational humidity ranges, and developing more compact high-capacity systems.

Key Developments:

- In February 2025, Watergen secured a multi-unit supply agreement with a Middle Eastern government agency to deploy large-scale atmospheric water generation systems supporting municipal water resilience initiatives. The project strengthens Watergen’s presence in government infrastructure programs addressing drought and water scarcity challenges across arid regions.

- In August 2024: GENAQ Technologies S.L. introduced a next-generation solar-powered atmospheric water generator series designed for off-grid environments. The upgraded systems improved water production efficiency by nearly 20%, enabling more reliable clean water supply for rural communities in Africa and Latin America supported by development programs.

- In November 2023: Akvo Atmospheric Water Systems Pvt. Ltd. partnered with the Government of India under the Jal Jeevan Mission to pilot atmospheric water generation units in water-scarce districts of Rajasthan and Gujarat, demonstrating the technology’s potential to support decentralized rural drinking water supply infrastructure.

Companies Covered in Atmospheric Water Generator Market

- Akvo Atmospheric Water Systems Pvt. Ltd.

- Dew Point Manufacturing

- Mayaqwa. Diseño Web

- WaterMaker India Pvt. Ltd.

- PlanetsWater

- Water Technologies International, Inc.

- SkyWater Air Water Machines

- Drinkable Air

- Hendrx Water

- Energy and Water Development Corp.

- Atlantis Solar

- GENAQ Technologies S.L.

- Air 2 Water Solutions

- EcoloBlue, Inc.

- Watergen

- Tsunami Products Inc.

- SOURCE Global, PBC

- Kara Water

- Aqua Sciences Inc.

- Infinite Water Inc.

Frequently Asked Questions

The global Atmospheric Water Generator Market is estimated at US$ 2.9 Billion in 2026 and is projected to reach US$ 5.6 Billion by 2033, growing at a CAGR of 9.8% during the forecast period. The market recorded a historical CAGR of 8.1% between 2020 and 2025, reflecting sustained demand growth driven by global water scarcity intensification.

The primary growth drivers are the accelerating global freshwater scarcity crisis, with the UN estimating over 2 billion people lacking safe water access, combined with climate-driven drought intensification documented by the IPCC, increasing government and military procurement for mobile water generation, and growing commercial sustainability mandates requiring on-site alternative water supply solutions aligned with LEED and BREEAM green building standards.

Static atmospheric water generators lead the product type segment with approximately 72% market share. Their advantage in energy efficiency, higher sustained daily water output, compatibility with building infrastructure, and lower per-liter operational cost for fixed installations make them the preferred choice across commercial, industrial, and residential end-users seeking long-term, reliable atmospheric water supply systems.

North America leads the global market, anchored by the United States where the U.S. EPA has documented water shortage risks across more than 40 states. Strong institutional procurement by the U.S. Department of Defense for mobile AWG deployments, an advanced innovation ecosystem, and growing residential adoption in drought-affected western states collectively reinforce North America's regional market leadership position.

The highest-impact opportunity is the development and deployment of solar-powered AWG systems for off-grid rural communities. With IRENA reporting a greater than 90% decline in solar PV costs since 2010 and multilateral funding from the World Bank and Asian Development Bank targeting UN SDG 6 clean water goals, solar-integrated AWG systems represent a commercially scalable, policy-supported solution for the 2+ billion people globally lacking reliable safe water access.

Key companies operating in the global Atmospheric Water Generator Market include Watergen, EcoloBlue, Inc., GENAQ Technologies S.L., Akvo Atmospheric Water Systems Pvt. Ltd., WaterMaker India Pvt. Ltd., Water Technologies International, Inc., Air 2 Water Solutions, Drinkable Air, Energy and Water Development Corp. (EAWC), SkyWater Air Water Machines, SOURCE Global, PBC, Atlantis Solar, PlanetsWater, and Kara Water, among other regional specialists and innovators.