- Medical Devices

- Artificial Pancreas Systems Market

Artificial Pancreas Systems Market Size, Share, and Growth Forecast 2026 - 2033

Artificial Pancreas Systems Market by Device Type (Threshold Suspend Systems, Control-to-Range (CTR) Systems, Control-to-Target (CTT) Systems), by Component (Continuous Glucose Monitoring (CGM) Systems, Insulin Pumps, Others), End-user (Hospitals, Clinics, Homecare Settings), and Regional Analysis, 2026 - 2033

Artificial Pancreas Systems Market Share and Trends Analysis

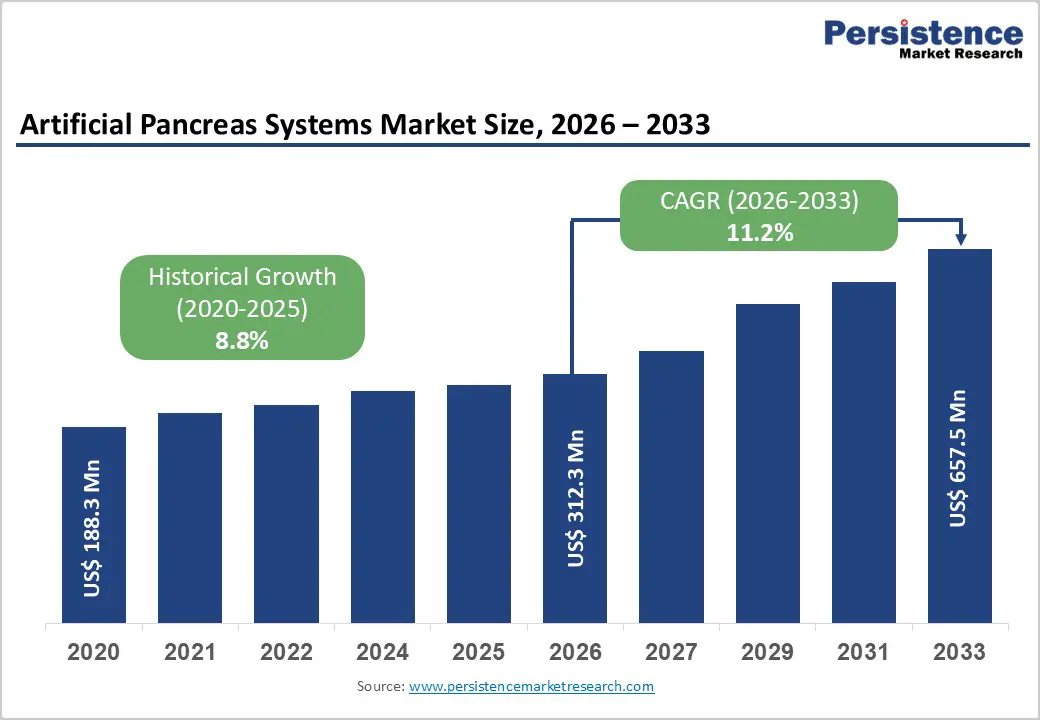

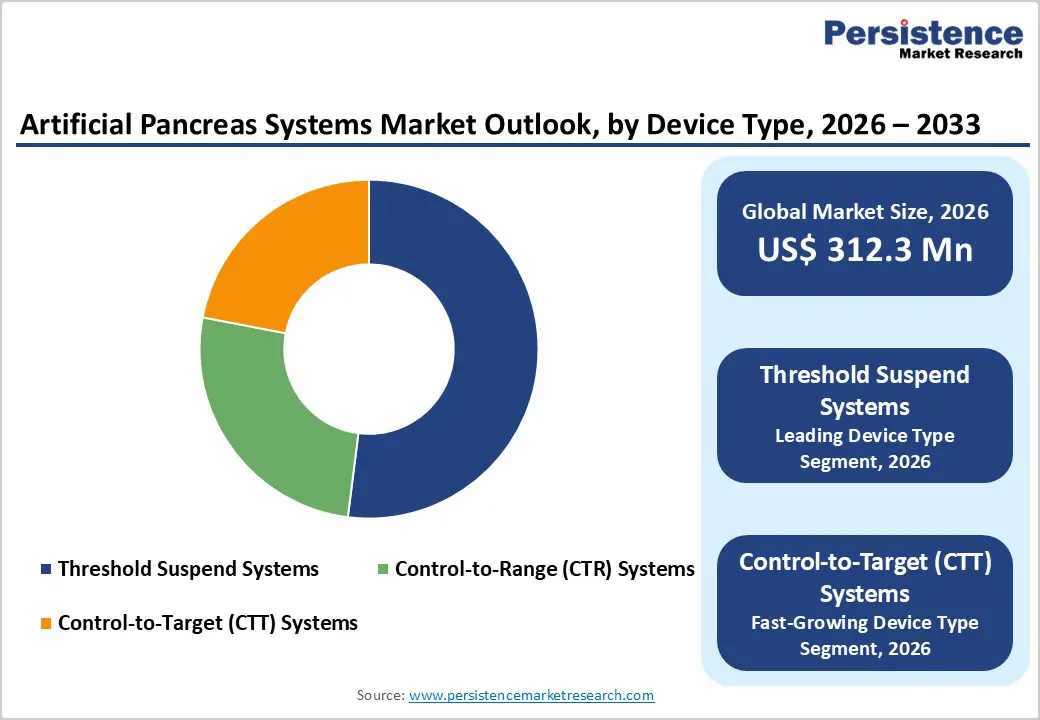

The global artificial pancreas systems market size is expected to be valued at US$ 312.3 million in 2026 and projected to reach US$ 657.5 million by 2033, growing at a CAGR of 11.2% between 2026 and 2033.

The market expansion is driven by the rising global diabetes burden, with the IDF Diabetes Atlas estimating that 589 million adults live with diabetes in 2024, projected to reach 853 million by 2050. Regulatory approvals for advanced hybrid closed-loop systems from Medtronic, Tandem, Insulet, and Beta Bionics have accelerated adoption, demonstrating significant improvements in time-in-range and HbA1c reduction across clinical trials and real-world use.

Key Industry Highlights:

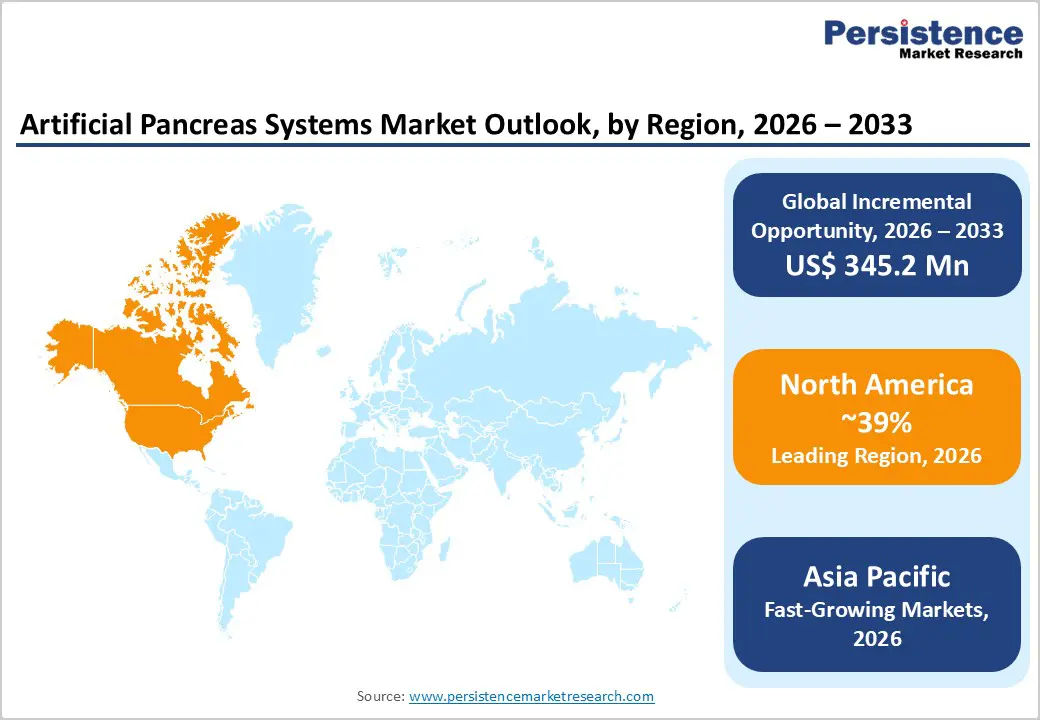

- North America dominated the Artificial Pancreas Systems Market with around 39% share in 2025, supported by strong regulatory leadership from the U.S. Food and Drug Administration, early approvals of automated insulin delivery technologies, and high insurance coverage. The region also has about 68.1 million diabetes cases, driving strong demand for advanced diabetes management devices.

- Asia Pacific is the fastest-growing region, driven by the rising diabetes burden, including nearly 106.9 million cases in South-East Asia. Expanding healthcare infrastructure, regulatory reforms, and cost-efficient device manufacturing are supporting market expansion.

- Threshold Suspend Systems lead the device segment with 52% market share, as they effectively prevent hypoglycemia by automatically stopping insulin delivery when glucose levels fall below a preset threshold.

- Continuous Glucose Monitoring (CGM) Systems dominate the component segment with 58% share, as they provide real-time glucose data essential for closed-loop artificial pancreas operation.

| Key Insights | Details |

|---|---|

| Artificial Pancreas Systems Market Size (2026E) | US$ 312.3 million |

| Market Value Forecast (2033F) | US$ 657.5 million |

| Projected Growth CAGR (2026 - 2033) | 11.2% |

| Historical Market Growth (2020 - 2025) | 8.8% |

Market Dynamics

Drivers - Rise in Global Diabetes Burden and Need for Tight Glycemic Control

The artificial pancreas systems market is primarily driven by the steep rise in diabetes prevalence worldwide, particularly type 1 diabetes requiring lifelong intensive insulin therapy. The IDF Diabetes Atlas (11th Edition) estimates 589 million adults had diabetes in 2024, projected to reach 853 million by 2050, with rapid increases in South-East Asia and Africa. Artificial pancreas systems integrating CGM, insulin pumps, and algorithms improve time-in-range above 70% and reduce hypoglycemia, meeting stringent glycemic targets and reducing complications. Clinical guidelines increasingly emphasize time-in-range metrics over HbA1c alone, positioning automated insulin delivery as essential for optimal diabetes management.

Demonstrated Clinical Benefits of Hybrid and Fully Closed-Loop Systems

Hybrid closed-loop systems like Medtronic MiniMed 780G, Tandem Control-IQ, and Insulet Omnipod 5 have shown 15% increases in time-in-range (3.6 hours/day) and HbA1c reductions of 0.3-0.5% without increased hypoglycemia. Real-world data validates these outcomes across diverse populations, supporting payer acceptance and guideline endorsements. FDA approvals expanding age indications to children as young as 2 years and investigational bihormonal systems further validate the technology's maturity and broad applicability.

Restraints - High Upfront Device Costs and Reimbursement Barriers

The high upfront cost of artificial pancreas systems remains one of the major restraints to market growth. These systems integrate multiple components such as continuous glucose monitoring (CGM) sensors, insulin pumps, control algorithms, and disposable consumables, which significantly increases the overall treatment cost. Patients must also regularly replace sensors, infusion sets, and reservoirs, adding recurring expenses that can become burdensome over time. In many developing and low-income regions where diabetes prevalence is rising rapidly, healthcare infrastructure and reimbursement support for advanced diabetes technologies remain limited, restricting patient access. Even in developed healthcare markets, insurance coverage for CGM devices and automated insulin delivery systems is often limited to specific patient populations, such as individuals with severe hypoglycemia or Type 1 diabetes. In addition, complicated reimbursement procedures, prior authorization requirements, and extensive clinical documentation can delay patient access to therapy, discouraging wider adoption of artificial pancreas technologies.

Technical Complexity, Training Requirements, and Data Security Concerns

Artificial pancreas systems involve sophisticated technologies that require proper understanding and management by both patients and healthcare providers. Users must learn how to operate insulin pumps, calibrate CGM sensors, manage infusion sites, and respond to device alerts or system malfunctions. This learning curve can be challenging, particularly for elderly patients or individuals who are not familiar with digital health devices. In the early stages of adoption, frequent alarms and notifications from glucose monitoring systems can lead to alarm fatigue, causing frustration and reduced adherence among users. Additionally, these systems continuously generate large volumes of sensitive health data that are stored or transmitted through cloud-based platforms for remote monitoring and analysis. Ensuring compliance with data protection regulations such as the Health Insurance Portability and Accountability Act (HIPAA) and the General Data Protection Regulation (GDPR) requires strong cybersecurity infrastructure. Any potential data breaches or cybersecurity vulnerabilities may reduce patient confidence and limit the widespread adoption of connected artificial pancreas systems.

Opportunity - Next-Generation Control-to-Target Systems and Bihormonal Artificial Pancreas

Next-generation control-to-target (CTT) systems are creating significant growth opportunities in the Artificial Pancreas Systems Market by improving automation, accuracy, and patient convenience. These advanced closed-loop systems continuously analyze glucose readings and automatically adjust insulin delivery to maintain glucose levels near a predefined target without constant user input. Innovations such as automated correction boluses and adaptive learning algorithms have improved glycemic control while reducing episodes of hyperglycemia and hypoglycemia. Additionally, the development of bihormonal artificial pancreas systems that deliver both insulin and glucagon represents a major technological advancement. By mimicking the natural functions of the pancreas more closely, these systems can stabilize glucose levels more effectively and reduce the risk of severe hypoglycemia. Clinical studies have shown that bihormonal systems can improve glucose management outcomes and provide greater safety for patients with complex diabetes conditions. As technology advances and regulatory approvals increase, these systems are expected to attract premium healthcare segments and drive market expansion.

Expansion into Broader Patient Populations and Care Settings

The expansion of artificial pancreas systems into broader patient populations and diverse care settings presents a major opportunity for market growth. Traditionally, these systems have been primarily used by individuals with Type 1 diabetes, but technological improvements are enabling their adoption among insulin-dependent Type 2 diabetes patients, significantly increasing the potential user base. Since Type 2 diabetes accounts for the majority of diabetes cases worldwide, expanding artificial pancreas applications to this group can greatly increase market demand. In addition, the growing shift toward home-based healthcare is supporting wider adoption of automated insulin delivery systems, as patients can manage their glucose levels more effectively outside hospital environments. These systems also enable remote monitoring by healthcare professionals, reducing the need for frequent clinic visits and improving long-term disease management. Furthermore, increasing adoption in hospital settings for perioperative glucose control and critical care management is opening new clinical applications, while expanding healthcare infrastructure and regulatory support in emerging regions are further accelerating market opportunities.

Category-wise Analysis

Device Type Insights

Threshold Suspend Systems held around 52% of the Artificial Pancreas Systems Market share in 2025, largely due to their early regulatory approvals and strong clinical adoption. Early products such as the MiniMed 530G and MiniMed 630G introduced automated insulin suspension when glucose levels fall below a preset threshold, helping prevent severe hypoglycemia. This feature is particularly beneficial during nighttime when patients may not recognize falling glucose levels. Clinical studies and real-world data have demonstrated that these systems can reduce nocturnal hypoglycemia episodes by approximately 50-70%, improving patient safety and confidence in automated insulin delivery technologies. Their relatively simple architecture, proven safety profile, and established reimbursement pathways have strengthened adoption across diabetes care centers. Although advanced hybrid closed-loop and control-to-target systems are emerging, Threshold Suspend Systems continue to maintain leadership due to their reliability and widespread clinical familiarity.

End-user Insights

Homecare settings accounted for approximately 65% of the Artificial Pancreas Systems Market share in 2025, reflecting the increasing shift toward patient-centered diabetes management outside traditional hospital environments. Artificial pancreas systems are designed for continuous daily use, making them highly suitable for home-based monitoring and insulin delivery. These systems combine insulin pumps with continuous glucose monitoring sensors that automatically adjust insulin dosing, allowing patients to maintain stable glucose levels with minimal manual intervention. Remote connectivity and cloud-based data platforms enable healthcare providers, including endocrinologists and diabetes specialists, to monitor patient glucose trends and therapy performance from a distance. This capability allows clinicians to review patient data remotely and make therapy adjustments without frequent in-person consultations. As a result, artificial pancreas technologies can reduce routine clinic visits by nearly 40%, supporting improved patient convenience, better treatment adherence, and more efficient long-term diabetes management.

Regional Insights

North America Artificial Pancreas Systems Market Trends and Insights

North America leads the Artificial Pancreas Systems Market, driven by advanced healthcare infrastructure, strong adoption of digital diabetes management technologies, and supportive regulatory frameworks. The region benefits from early regulatory approvals for automated insulin delivery systems from authorities such as the U.S. Food and Drug Administration, which has accelerated the commercialization of hybrid closed-loop and next-generation artificial pancreas technologies. High awareness among patients and clinicians regarding continuous glucose monitoring and automated insulin delivery solutions further supports market expansion. In addition, favorable reimbursement coverage for insulin pumps and CGM devices across the United States and Canada has improved patient access to these advanced systems. The growing prevalence of Type 1 Diabetes and increasing adoption of connected health platforms that allow remote glucose monitoring are also contributing to demand. Furthermore, the presence of major medical device manufacturers, strong clinical research activity, and continuous product innovation are strengthening regional leadership, enabling North America to remain the most mature and technologically advanced market for artificial pancreas systems globally.

Asia Pacific Artificial Pancreas Systems Market Trends and Insights

The Asia Pacific Artificial Pancreas Systems Market is emerging as a high-growth region due to the rapidly increasing prevalence of diabetes, improving healthcare infrastructure, and rising adoption of advanced diabetes management technologies. Countries such as China, India, Japan, and South Korea are witnessing growing demand for continuous glucose monitoring and automated insulin delivery systems as awareness of modern diabetes care improves. Government initiatives aimed at strengthening chronic disease management and expanding digital healthcare solutions are also supporting the adoption of artificial pancreas technologies. In addition, increasing healthcare investments, a rising middle-class population, and expanding private healthcare facilities are enabling greater access to advanced medical devices. Several multinational medical device manufacturers are strengthening their presence in the region through partnerships, product launches, and distribution expansions. Furthermore, growing telehealth adoption and remote patient monitoring capabilities are encouraging patients and healthcare providers to adopt automated insulin delivery solutions, positioning Asia Pacific as one of the fastest growing markets for artificial pancreas systems.

Competitive Landscape

The artificial pancreas systems market is moderately competitive, driven by continuous technological advancements and increasing demand for automated diabetes management solutions. Market participants are focusing on developing advanced closed-loop insulin delivery systems that integrate continuous glucose monitoring, insulin pumps, and intelligent control algorithms to improve glycemic control and patient convenience. Companies are investing significantly in research and development to introduce more accurate, user-friendly, and fully automated systems. Strategic initiatives such as regulatory approvals, product innovations, technology collaborations, and expansion into emerging markets are common approaches used to strengthen market presence.

Key Developments:

- In September 2025, NHS England launched a new initiative to provide a pregnancy-specific hybrid closed-loop artificial pancreas system to women with Type 1 Diabetes who are pregnant or planning pregnancy. The system integrates an insulin pump, a continuous glucose sensor, and a smartphone-based algorithm that automatically monitors glucose levels and adjusts insulin delivery throughout the day.

- In September 2024, Abbott Laboratories announced a strategic partnership with Beta Bionics to integrate Abbott’s FreeStyle Libre 3 Plus sensor with the iLet Bionic Pancreas. The collaboration aimed to combine real-time glucose monitoring with automated insulin dosing, enabling the iLet system to calculate and deliver insulin using glucose data from the sensor.

Companies Covered in Artificial Pancreas Systems Market

- Medtronic

- Tandem Diabetes Care

- Insulet Corporation

- Dexcom, Abbott Laboratories

- Beta Bionics

- Bigfoot Biomedical

- Diabeloop

- Pancreum

- Inreda Diabetic

- Admetsys

- TypeZero Technologies

- Roche Diabetes Care

- Ypsomed

- SOOIL Development

Frequently Asked Questions

US$ 312.3 million, driven by 589 million global diabetes cases and FDA approvals expanding hybrid closed-loop access.

853 million projected diabetes cases by 2050, 15% time-in-range improvements, 70% hypoglycemia reduction validate clinical superiority.

North America (39% share 2025) via FDA leadership (12 approvals), 68.1 million cases, 95% insurance coverage.

Control-to-target systems, type 2 diabetes expansion, Asia Pacific growth (106.9 million cases) offer 3x market expansion.

Medtronic (780G), Tandem (Control-IQ), Insulet (Omnipod 5), Dexcom, Beta Bionics (iLet) lead innovation.