- Metals & Minerals

- Aluminium Scrap Market

Aluminium Scrap Market Size, Share, and Growth Forecast 2026 - 2033

Aluminium Scrap Market by Scrap Type (Post-Consumer Scrap, Post-Industrial Scrap, Mixed Scrap), Alloy Type (Wrought Aluminium Scrap, Cast Aluminium Scrap), Grade (Casting Scrap, Extrusion Scrap, Sheet Scrap), End-user (Automotive, Building & Construction, Packaging, Electrical & Electronics, Industrial Machinery, Consumer Goods), and Regional Analysis, 2026 - 2033

Aluminium Scrap Market Size and Trend Analysis

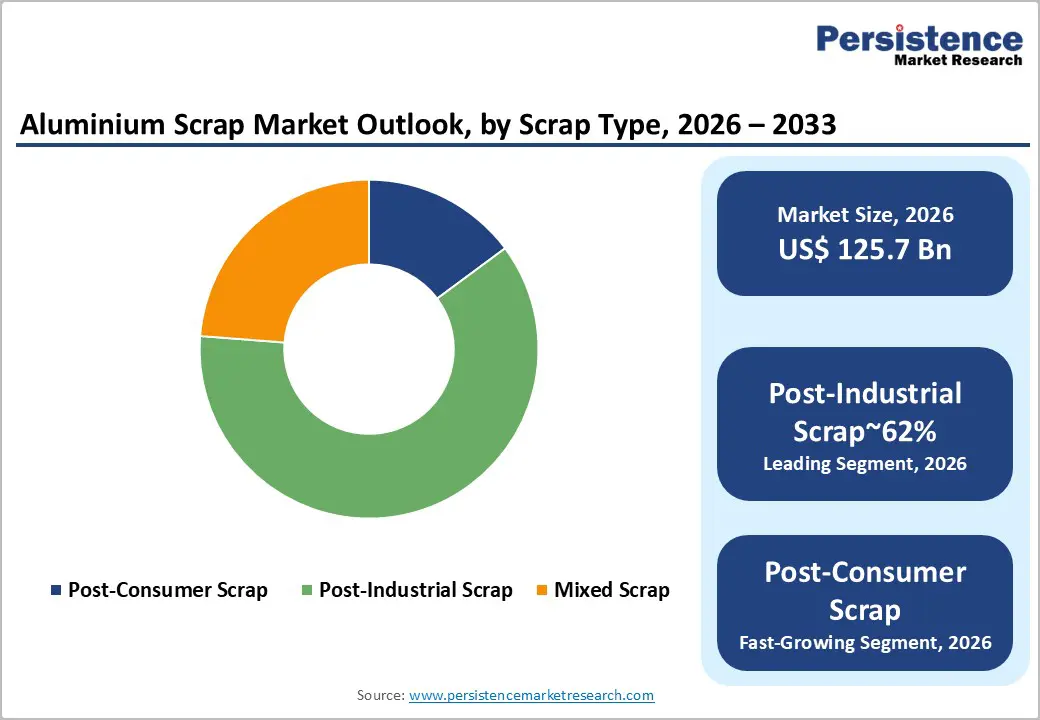

The global aluminium scrap market size is likely to be valued at US$ 125.7 Billion in 2026 and is expected to reach US$ 172.2 Billion by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 and 2033. Circular economy mandates and primary aluminium production constraints are fueling this expansion.

Key Industry Highlights:

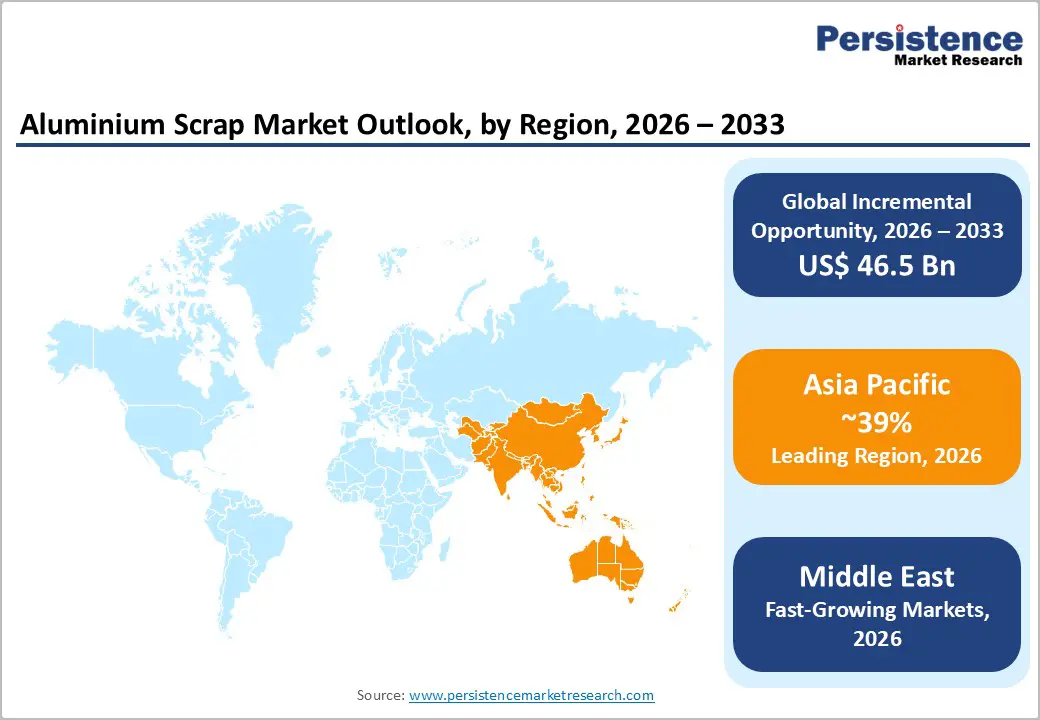

- Leading region: Asia Pacific dominates the aluminium scrap market with 39% share, driven by strong secondary capacity expansion in China and India, supported by government policies, rising domestic consumption, and increasing investments in organized recycling infrastructure.

- Fastest Growing Region: The Middle East is emerging as the fastest-growing region with rising CAGR of 6.1%, led by UAE smelter modernizations, increasing focus on sustainable aluminium production, and rising construction and infrastructure projects generating significant recyclable scrap volumes.

- Dominant Scrap Type: Post-industrial scrap leads the market with 62% share, supported by high purity levels, consistent quality from manufacturing processes, premium pricing advantages, and strong demand from automotive and packaging industries.

- Fastest Growing Segment: EV battery casings are the fastest-growing segment, generating clean ADC12 aluminium scrap, driven by rapid electric vehicle adoption, increasing end-of-life battery recycling, and rising demand for sustainable material sourcing.

- Key Opportunity: Construction demolition scrap presents a key opportunity, as facade and extrusion materials provide high-quality recyclable aluminium, enabling premium billet production, energy savings, and supporting sustainability requirements in global construction markets.

| Key Insights | Details |

|---|---|

| Aluminium Scrap Market Size (2026E) | US$ 125.7 Billion |

| Market Value Forecast (2033F) | US$ 172.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 4.6% |

| Historical Market Growth (2020 - 2025) | 3.8% |

DRO Analysis

Drivers - Strong policy push and carbon reduction targets accelerate global demand for recycled aluminium supply chains

Rising pressure to reduce carbon emissions is significantly reshaping aluminium supply chains. Scope 3 emission reporting is pushing OEMs to increasingly adopt recycled aluminium, which reduces carbon emissions by nearly 95% compared to bauxite-based production. According to industry data, secondary aluminium production emits only about 0.5 tCO2 per ton versus 14 tCO2 for primary aluminium. Regulatory support is further accelerating this shift, with policies such as the EU Battery Regulation mandating 12% recycled aluminium in EV casings by 2030.

Incentives under the U.S. Inflation Reduction Act are favoring scrap-based smelting operations. As a result, scrap premiums have surged by around US$ 200 per ton above LME levels in 2025. This evolving policy and pricing environment is creating strong profit opportunities for scrap collectors and processors who can efficiently optimize ISRI-grade segregation and supply high-quality recycled material.

Rising EV production and lightweighting needs significantly boost demand for high-quality aluminium scrap materials

The rapid shift toward electric vehicles is driving strong demand for aluminium scrap, particularly for lightweight and high-strength applications. EV battery enclosures and structural components require large volumes of ADC12-grade scrap, supporting cost efficiency and sustainability goals. For example, aluminium-intensive platforms such as Tesla’s 4680 battery cells incorporate around 20 kg of recycled aluminium per vehicle.

With global EV production projected to reach 65 million units annually by 2030, the demand for clean wrought scrap is expected to exceed 2 million tons per year. In parallel, end-of-life vehicle (ELV) regulations are boosting scrap recovery rates, particularly for components such as bumpers and rims, with collection volumes rising by nearly 30%. Leading players like Novelis are already using up to 40% scrap in automotive sheet production, reducing melting costs by approximately US$ 800 per ton while meeting sustainability certifications.

Restraints - Contamination challenges in aluminium scrap reduce recovery efficiency and increase processing costs for recyclers

Quality inconsistency remains a major challenge in the aluminium scrap market, directly impacting recovery rates and profitability. Even small levels of contamination, such as iron or steel exceeding 0.5%, can downgrade high-value scrap like A356 cast material into lower-grade remelt categories. This results in up to a 15% reduction in recovery efficiency. Mixed scrap streams, such as used beverage cans (UBC), often contain 2-5% organic and metallic impurities, requiring advanced sorting and cleaning processes.

The adoption of modern technologies like Laser-Induced Breakdown Spectroscopy (LIBS) is still limited, with nearly 70% of processing facilities yet to upgrade. As a result, scrap processors continue to face purity penalties of around US$ 50 per ton, which erode the cost advantage of secondary aluminium. Addressing contamination challenges through better segregation and technology adoption remains critical for improving overall market efficiency.

Trade restrictions and geopolitical tensions disrupt global aluminium scrap flows and constrain supply availability

Global aluminium scrap flows have been significantly impacted by geopolitical developments and trade restrictions. China’s ban on solid waste imports since 2018 disrupted approximately 4 million tons of global scrap movement, leading to sharp price volatility and increased LME premiums by nearly 50%. Additionally, ongoing geopolitical tensions, such as the Russia-Ukraine conflict, have disrupted key export routes through the Black Sea region, further tightening supply chains.

Trade barriers, including U.S.-China tariffs of up to 25%, have also increased costs and limited cross-border scrap movement. At the same time, collection inefficiencies persist in several regions, with Europe achieving only about 30% collection rates in certain segments. These factors collectively constrain secondary aluminium production capacity, keeping utilization levels below 75%. Addressing these structural and geopolitical challenges is essential to ensure stable supply and support long-term market growth.

Opportunities - Growing EV adoption creates lucrative opportunities for high-purity battery-grade aluminium scrap processing technologies

The growing adoption of electric vehicles is creating a strong opportunity for battery-grade aluminium scrap processing. Materials derived from EV battery casings, particularly those using NMC chemistries, generate high-quality scrap similar to ADC12, which can be reused in next-generation battery systems such as LFP cells. As early EV models like Nissan Leaf and Toyota Prius reach end-of-life stages, the availability of recyclable aluminium is expected to rise significantly, with projections indicating nearly 3 million tons of EV-related aluminium scrap by 2030.

Advanced processing methods, including black mass pre-sorting, can deliver up to 99% pure A380-grade aluminium at just 20% of the cost of primary material. Innovative facilities, such as Hydro’s r∞D unit, demonstrate near-complete recovery rates of 99.9%. With regulatory mandates requiring 16% recycled content in batteries, this segment offers premium pricing potential of up to US$ 2,500 per ton.

Urban mining and demolition activities unlock large volumes of high-quality recyclable aluminium construction scrap

Urban mining is emerging as a major opportunity in the aluminium scrap market, particularly from construction and demolition activities. Large-scale infrastructure replacement and redevelopment projects are unlocking significant volumes of high-quality aluminium scrap from building facades, cladding, and window systems. Alloys such as AA3003 and AA5005 are especially valuable due to their high recyclability and consistent quality.

The demolition projects in regions like the Middle East are generating substantial scrap volumes, with Dubai’s Sustainable City alone producing around 10,000 tons annually. Overall, Gulf region projects are expected to contribute nearly 500,000 tons of scrap through 2030. This scrap offers up to 95% energy savings compared to primary production and commands premium prices of approximately US$ 1,800 per ton due to traceability and sustainability certifications. Advanced mobile technologies like XRF units are further improving recovery rates by capturing previously overlooked materials.

Category-wise Analysis

Scrap Type Insights

Post-industrial scrap holds a dominant position in the aluminium scrap market, accounting for approximately 62% of total share due to its superior quality and consistency. This type of scrap, generated from manufacturing processes such as trimming and stamping, typically offers purity levels as high as 98%, significantly higher than post-consumer scrap at around 85%. As a result, it commands a price premium of nearly US$ 150 per ton over standard LME rates.

In the automotive sector, manufacturing processes generate about 1.5 kg of clean AA6016 scrap per car door, which can be directly recycled with minimal processing. Companies like Novelis utilize up to 70% post-industrial scrap in can production lines, improving efficiency and reducing costs. Industry data indicates that nearly 75% of global secondary aluminium billet production relies on industrial scrap streams, highlighting their critical role in ensuring supply reliability and maintaining high-quality output.

Alloy Type Insights

Wrought aluminium scrap represents the largest share within alloy types, accounting for approximately 58% of the market due to its superior recyclability and performance characteristics. Commonly sourced from packaging and transportation applications, alloys in the 3xxx and 5xxx series are highly suitable for extrusion and remelting processes. These materials offer excellent conductivity levels of up to 99.5%, significantly outperforming cast aluminium, which typically contains higher impurity levels.

The wrought aluminium recycling is up to three times more energy-efficient than cast recycling, making it a preferred choice for sustainability-focused manufacturers. This efficiency advantage is particularly evident in Europe, where secondary extrusion markets account for nearly 75% of total production. The strong demand for lightweight, high-performance materials in industries such as automotive and construction continues to drive the adoption of wrought aluminium scrap across global markets.

Grade Insights

Extrusion scrap leads the grade segment with approximately 45% share, driven by its high recyclability and consistent material properties. Commonly derived from construction applications such as window frames and structural profiles, alloys like AA6063 are particularly valuable due to their low iron content, typically below 0.2%. This makes them ideal for seamless re-extrusion without compromising quality. Construction activities generate nearly 2 million tons of aluminium scrap annually in Europe alone, according to industry estimates.

In emerging markets like India, rapid urbanization and infrastructure development are contributing an additional 500,000 tons of window and extrusion scrap each year. The predictable composition and high recovery rates of extrusion scrap make it a preferred input material for recyclers. As construction activities continue to expand globally, the availability and importance of extrusion-grade scrap are expected to increase further.

End-user Insights

The building and construction sector accounts for approximately 38% of total aluminium scrap demand, making it the largest end-use segment. This dominance is driven by ongoing demolition and renovation cycles, which generate significant volumes of recyclable aluminium from roofing, cladding, and structural components. Alloys such as AA3004 are widely used in these applications and offer near 100% recyclability, enabling efficient closed-loop systems.

In regions like China, large-scale urban developments and underutilized infrastructure, often referred to as “ghost cities,” are creating substantial scrap supply, estimated at around 1 million tons of clean sheet aluminium. Additionally, green building standards such as LEED certification require at least 20% recycled material content, further boosting demand for aluminium scrap. As sustainability becomes a key focus in construction, the reliance on recycled aluminium is expected to grow significantly.

Regional Insights

North America Aluminium Scrap Market Trends

North America, led by the United States, remains a key market for aluminium scrap, supported by well-established collection and processing infrastructure. Major networks such as OmniSource and Sims handle approximately 4 million tons of used beverage cans annually, ensuring a steady supply of recyclable material. Government initiatives, including funding from the Department of Energy, are promoting advanced sorting technologies like spectroscopic systems for EV-grade alloys. Regulatory frameworks such as EPA’s End-of-Life Vehicle rules mandate up to 95% material recovery, further strengthening scrap availability.

Leading manufacturers like Novelis are investing in large-scale facilities such as the Bay Minette plant, which focuses on producing automotive sheet entirely from recycled aluminium. Additionally, regional trade agreements like USMCA encourage the use of locally sourced scrap, reducing dependence on imports and supporting domestic recycling industries. Secondary aluminium production in the Rust Belt has reached utilization levels of around 85%.

Europe Aluminium Scrap Market Trends

Europe continues to lead in sustainable aluminium recycling practices, driven by strong regulatory frameworks and advanced infrastructure. Countries like Germany have implemented strict policies such as the Circular Economy Act, targeting 75% secondary aluminium usage by 2030. Major players like Constellium operate fully scrap-based facilities, including the Voerde plant, which relies entirely on recycled input material.

The region also plays a key role in global scrap trade, with the UK exporting nearly 1 million tons of processed scrap to markets like Turkey. Innovative processes such as Waelz kiln technology are being used in countries like France and Spain to recover valuable materials from aluminium salt slag. Additionally, EU Taxonomy regulations provide financial incentives for scrap-based production, offering up to double the green premium compared to primary aluminium. Companies like Hydro are achieving near carbon-neutral production through high recycled content and advanced technologies.

Asia Pacific Aluminium Scrap Market Trends

The Asia Pacific region is experiencing rapid growth in aluminium scrap processing, driven by industrial expansion and increasing sustainability initiatives. India is emerging as a key market, with secondary aluminium capacity expected to reach 3 million tons by 2030, supported by government policies and rising domestic consumption. China, despite its import ban, continues to hold large stockpiles of scrap, estimated at around 5 million tons, which are gradually being utilized for domestic production.

Japan remains a major exporter of high-quality scrap, particularly A356-grade material, supplying markets like South Korea. Meanwhile, Southeast Asian countries such as Vietnam are developing into key sorting and redistribution hubs for global scrap flows, especially from Europe. Large-scale producers like Vedanta are also increasing scrap utilization, with facilities such as Jharsuguda operating at up to 70% scrap input for EV component manufacturing. This regional shift is strengthening global recycling supply chains.

Competitive Landscape

The aluminium scrap market is characterized by a fragmented collection network combined with a relatively consolidated secondary smelting sector. Leading companies such as Novelis, Hydro, and Constellium collectively control around 40% of the processing market through advanced technologies like LIBS and eddy current sorting systems. Industry players are increasingly focusing on vertical integration strategies, with companies like Arconic acquiring scrap collection yards to secure consistent raw material supply.

Digital platforms such as ScrapWare are also gaining traction, improving logistics efficiency and enabling better price discovery. Differentiation in the market is largely driven by sustainability credentials, with Aluminium Stewardship Initiative (ASI) certification becoming a key competitive factor. Additionally, tolling models are becoming more common, allowing OEMs to supply their own scrap while processors handle recycling operations. These evolving strategies are helping companies improve margins, enhance traceability, and strengthen long-term customer relationships.

Key Developments:

- In February, 2026: Hydro Aluminium expanded its recycling capabilities by launching a new RTA line in Grevenbroich, Germany, designed to process 110,000 tons of low-carbon aluminium scrap annually, strengthening its closed-loop supply for automotive clients like Audi’s e-tron EV platform.

- In October, 2025: Novelis strengthened its automotive recycling supply chain by acquiring Gränges Americas, securing approximately 50,000 tons per annum of AA6xxx aluminium scrap, enhancing its position in high-strength automotive sheet production and supporting growing EV demand globally.

- In June, 2025: Real Alloy introduced advanced AI-powered Vision sorting technology to improve scrap quality, achieving up to 99.5% iron removal from mixed used beverage cans, significantly enhancing recycling efficiency, reducing contamination, and improving the value of secondary aluminium outputs.

Companies Covered in Aluminium Scrap Market

- Novelis Inc.

- Hydro Aluminium AS

- Constellium SE

- Arconic Corporation

- Real Alloy Holding GmbH

- RUSAL

- OmniSource Corporation

- Sims Metal Management

- Century Aluminium Company

- Kaiser Aluminium

- Alcoa Corporation

- Sapa Group

- Hindalco Industries Limited

- Kaiser Aluminium Corporation

- Matalco Inc

- Norsk Hydro

Frequently Asked Questions

The market will reach US$ 172.2 Billion by 2033 at 4.6% CAGR, driven by circular economy mandates.

EV lightweighting and 95% CO2 savings versus primary production accelerate secondary.

Post-Industrial Scrap at 62% share offers 98% purity for premium remelt applications.

Asia Pacific dominates via China/India secondary capacity and domestic collection growth.

EV battery casing scrap processing for LFP cell manufacturing with US$ 2,500/t premiums.

Novelis, Hydro, Constellium, Real Alloy, and Hindalco lead via integrate d recycling platforms.