- Biotechnology

- Allergy and Autoimmune Disease Diagnostics Market

Allergy and Autoimmune Disease Diagnostics Market Size, Share, and Growth Forecast 2026 – 2033

Allergy and Autoimmune Disease Diagnostics Market by Product and Service (Instruments), Test Type (Allergy Diagnostics, Autoimmune Disease Diagnostics), Disease Type, End-user, and Regional Analysis, 2026 – 2033

Allergy and Autoimmune Disease Diagnostics Market Size and Trends Analysis

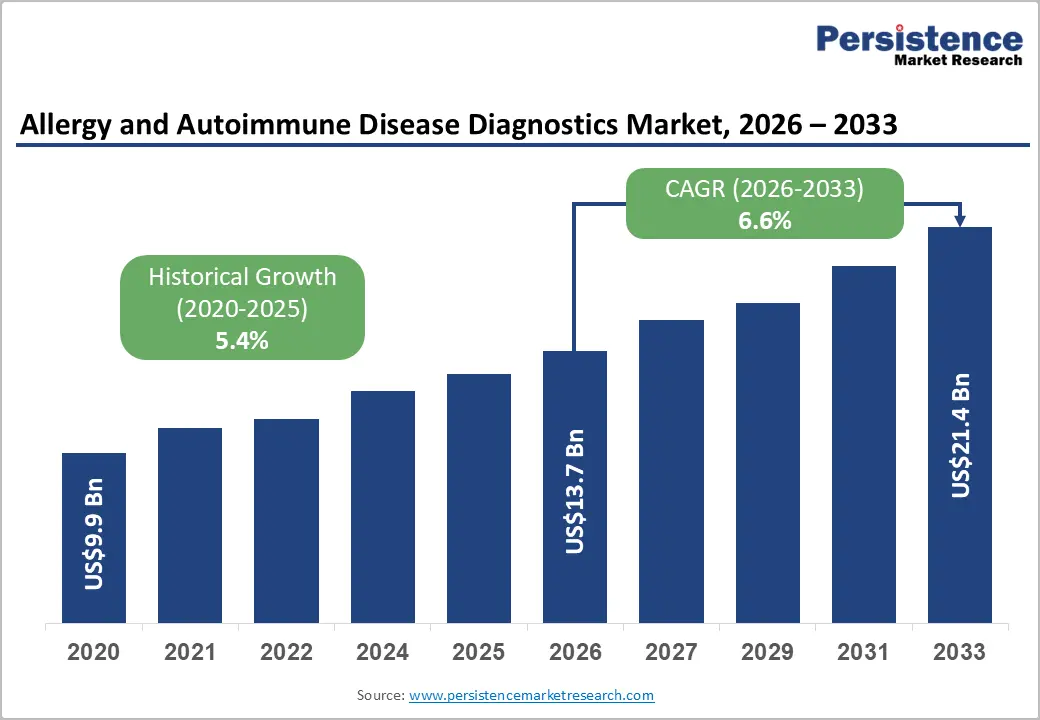

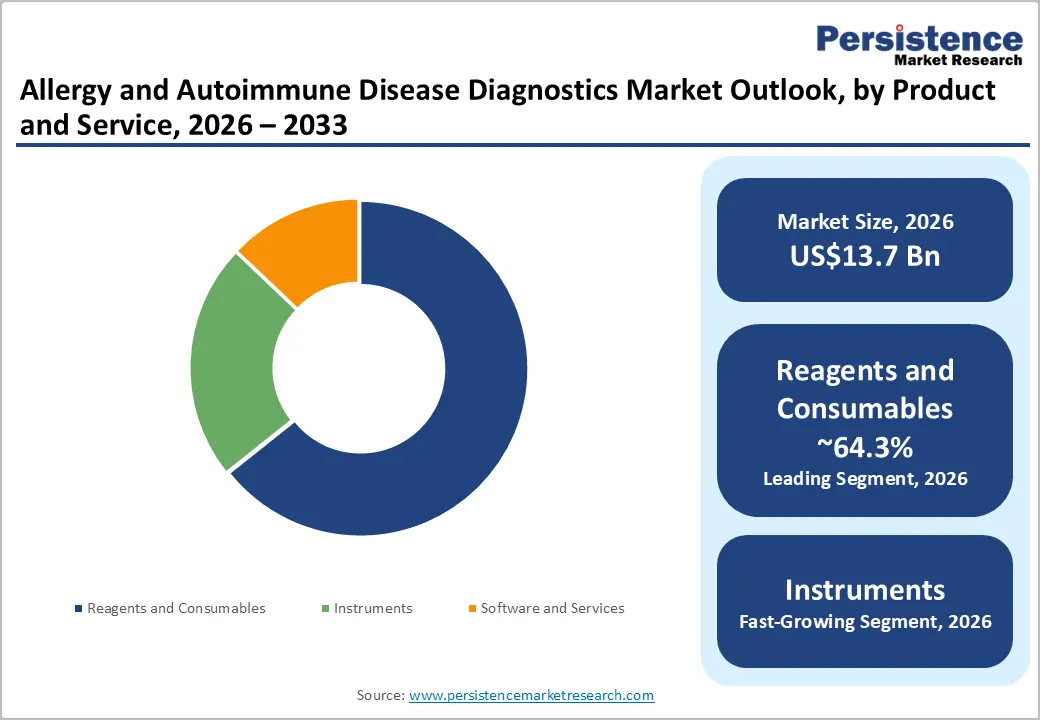

The global allergy and autoimmune disease diagnostics market size is likely to be valued at US$13.7 billion in 2026 and is expected to reach US$21.4 billion by 2033, growing at a CAGR of 6.6% during the forecast period from 2026 to 2033, driven by rising global burden of allergic and autoimmune conditions.

Increasing clinical preference for early and accurate diagnosis is boosting the adoption of advanced immunoassay and multiplex testing platforms across hospitals and diagnostic laboratories.

Key Industry Highlights:

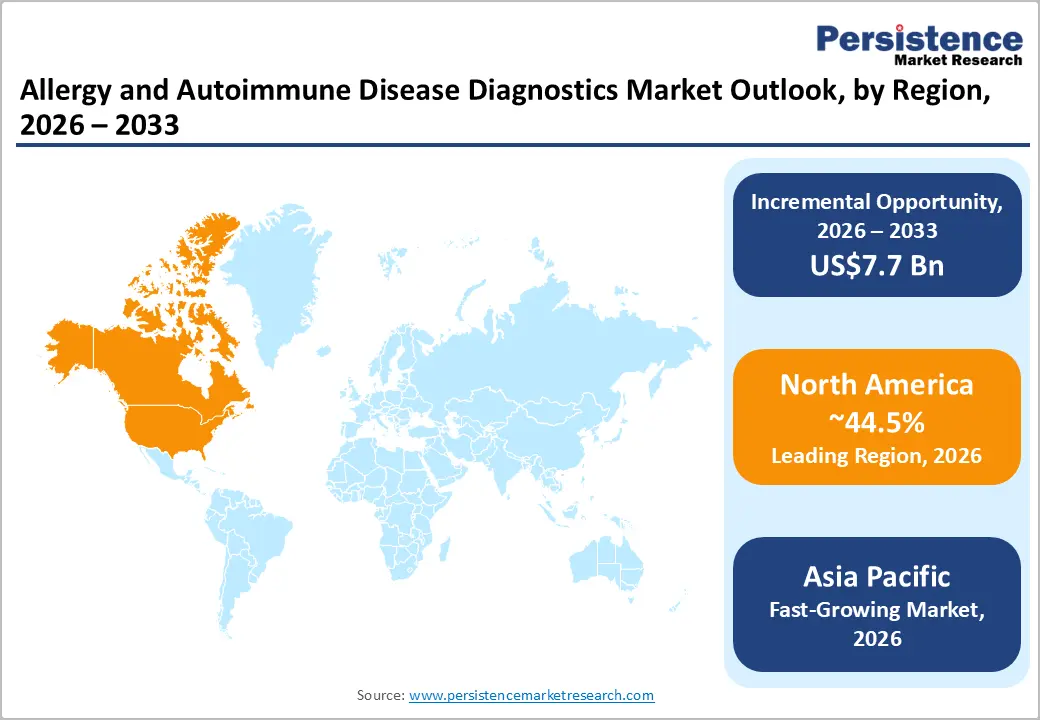

- Leading Region: North America, with about 44.5% share in 2026, backed by high adoption of advanced immunoassay platforms from leading companies.

- Fast-growing Region: Asia Pacific, backed by rising allergy prevalence and expanding diagnostic infrastructure.

- Latest Acquisition: In March 2026, Novartis agreed to acquire Excellergy, Inc., a Palo Alto-based private biotech developing next-generation anti-IgE therapies, for up to US$2 billion. The deal centers on Exl-111, a half-life extended, high-affinity anti-IgE antibody currently in Phase 1 trials.

- Leading Product and Service: Reagents and consumables, approximately 64.3% share in 2026, as every diagnostic test requires repeat usage, generating continuous revenue unlike one-time instrument purchases.

- Dominant Test Type: In vitro tests, with nearly 70.8% share in 2026, owing to their high accuracy and safety.

DRO Analysis

Driver - Rising Prevalence of Allergic and Autoimmune Conditions

The global load of allergic and autoimmune diseases is climbing sharply, and it is not just genetics driving this. Urbanization, dietary shifts, air pollution, and the hygiene hypothesis, where overly sanitized environments leave immune systems poorly calibrated, are all contributing factors. According to the Centers for Disease Control and Prevention’s (CDC) 2024 National Health Interview Survey, nearly one in three U.S. adults now carries a diagnosis of seasonal allergy, eczema, or food allergy.

On the autoimmune side, a 2024 study in the International Journal of Rheumatic Diseases noted that autoimmunity is rising globally, influenced by socioeconomic conditions, environmental exposures, diet, stress, and climate change. The COVID-19 pandemic further worsened outcomes, with unvaccinated individuals showing higher rates of post-infection autoimmune conditions. This surging patient pool is spurring demand for diagnostic tools.

Urgent Need to Detect Diseases Early

Several autoimmune diseases begin with vague complaints, including fatigue, joint pain, and dry eyes, that could fit dozens of other conditions. This overlap leads to prolonged diagnostic journeys. According to the National Health Council, autoimmune patients see an average of four different providers over 4.5 years before receiving a confirmed diagnosis. The consequences go beyond inconvenience.

A 2024 review in the Alqalam Journal of Medical and Applied Sciences noted that delayed diagnosis in autoimmune diseases often allows irreversible tissue and organ damage to progress unchecked. Advanced diagnostic platforms that can detect disease-specific biomarkers and autoantibody profiles earlier in the disease course are hence not just helpful. They are clinically essential for changing long-term patient outcomes.

Restraint - High Rates of False Positives and Negatives

One of the most persistent problems in this diagnostic field is the inconsistent reliability of widely used tests. A positive result does not always confirm disease and a negative result does not always rule it out. The University of North Carolina's Division of Rheumatology notes that antinuclear antibody (ANA) positivity can be seen in up to 20% of healthy adults, and up to 30% test positive at a dilution of 1:40 or greater, without any autoimmune disease present.

A study from Germany's Kerckhoff Clinic found that among asymptomatic individuals with ANAs, only 4% went on to develop an autoimmune disease within three years of follow-up. On the allergy side, MedlinePlus states that false positives in allergy blood tests can occur when the body reacts to substances in recently consumed foods or when IgE is elevated due to smoking or parasitic infections. These inaccuracies burden patients with unnecessary anxiety, trigger costly follow-up testing, and can lead to incorrect treatments.

Opportunity - Precision Allergy Testing at the Molecular Level

Traditional allergy tests use crude whole-allergen extracts, which can produce cross-reactive results that mask whether a patient truly has an allergy or is simply reacting to shared protein structures across unrelated allergens. Component-Resolved Diagnosis (CRD) solves this by testing IgE reactivity against individual purified allergen molecules. A January 2025 paper in the Journal of Allergy and Clinical Immunology confirmed that molecular allergy diagnosis has moved allergology into the era of precision medicine by establishing each patient's IgE reactivity profile at the molecular level.

CRD can specifically distinguish genuine sensitization from cross-reactive sensitization, a key clinical benefit that whole-extract testing cannot provide. For example, a patient reacting to both birch pollen and apples may only have pollen-food allergy syndrome, not a true apple allergy. A 2024 EAACI-commissioned meta-analysis of 149 studies and 24,489 patients found that component-specific IgE testing achieved specificities of 92 to 95%, far outperforming extract-based methods.

Functional Blood Testing to Replace Risky Oral Food Challenges

The Basophil Activation Test (BAT) measures how a patient's blood basophils respond when exposed to specific allergens, thereby simulating the allergic response in vitro, without putting the patient at risk. A 2024 review in Expert Review of Clinical Immunology confirmed that BAT has high sensitivity and specificity for IgE-mediated allergy, is reproducible under standardized protocols, and has been proposed as a tool to reduce the requirement for oral food challenges. The clinical evidence is strengthening.

A 2025 study in Allergy found that BAT had the largest area under the ROC curve for diagnosing both baked and fresh milk allergies compared to skin prick tests and specific IgE. Using BAT-guided cut-offs required the fewest oral food challenges to achieve 100% diagnostic accuracy. For drug allergies where IgE testing is limited by the sheer number of drugs on the market, BAT delivers superior specificity and has demonstrated clinical utility in diagnosing hypersensitivity to antibiotics and analgesics.

Category-wise Analysis

Product and Service Insights

Reagents and consumables are predicted to lead with a share of approximately 64.3% in 2026, owing to the recurring nature of diagnostic testing. Every allergy panel and autoimmune assay requires fresh reagents, controls, and calibrators. Large laboratories processing thousands of samples daily generate continuous demand. For instance, Thermo Fisher’s ImmunoCAP system processes millions of allergy tests annually, with most revenue associated with consumables rather than the analyzer itself, strengthening the segment’s dominance.

Instruments are estimated to be the fastest-growing segment in the forecast period. These include immunoassay analyzers and multiplex platforms from players such as Siemens Healthineers and Beckman Coulter. While they bring high upfront revenue, their share remains low as purchases are periodic and capital-intensive. Growth is still notable due to automation trends. Labs are upgrading to high-throughput systems capable of running both allergy and autoimmune panels on a single platform, but the installed base limits frequent replacement cycles.

Test Type Insights

In vitro tests are anticipated to dominate with a share of nearly 70.8% in 2026 under the allergy diagnostics segment. Blood-based testing is now the clinical preference due to safety, standardization, and expandability. Specific IgE blood tests, component-resolved diagnostics, and autoantibody assays (ANA, anti-CCP) are widely used as they eliminate risks associated with skin testing and enable large-scale lab processing.

In vivo tests are expected to remain in the second position in 2026. These include skin prick and patch tests, which are still widely used in clinical settings, owing to their low cost and immediate results. However, their share is declining as hospitals shift toward lab-based diagnostics. Limitations such as patient discomfort, contraindications in severe allergy cases, and variability in interpretation are pushing clinicians toward in vitro alternatives.

Regional Insights

North America Allergy and Autoimmune Disease Diagnostics Market Trends

North America is predicted to be the dominant region in 2026 with a global share of approximately 44.5%, and the U.S. leading the regional market. The foundation is a uniquely well-funded research network. NIAID, the U.S. government's primary immunology and allergy research body, operates under a US$6.6 billion budget that supports research in diagnostic development, immunologic diseases, and allergic conditions. This federal investment feeds into clinical adoption. A 2025 paper in the Journal of Allergy and Clinical Immunology: Global noted that 354 of 356 FDA-approved drugs between 2010 and 2019 originated from NIH-funded research, a pattern that extends to diagnostics.

U.S. Allergy and Autoimmune Disease Diagnostics Market Trends

The U.S. is expected to account for a share of nearly 53.6% in 2026, dominating North America’s market. According to the National Health Council, autoimmune diseases affect approximately 50 million Americans, with women accounting for 80% of that number. Several studies indicate annual growth rates in the range of 3% to 12% for these conditions. On the allergy side, the CDC puts the number of Americans with allergies at over 50 million each year.

A key structural advantage in the U.S. is its regulatory framework. The FDA's Breakthrough Devices Program has expedited approval for several allergy and autoimmune diagnostic platforms, while the 21st Century Cures Act has created speedy pathways for innovative diagnostics to reach clinical use. Medicare coverage decisions also influence how widely new tests get adopted. Together, these policies shorten the time from development to bedside.

Asia Pacific Allergy and Autoimmune Disease Diagnostics Market Trends

Asia Pacific is anticipated to be the fastest-growing market in 2026 with a global share of nearly 26.9%, owing to rising urbanization, environmental pollution, changing dietary habits, and expanding access to healthcare services. The scale of the opportunity is difficult to overstate. According to the 2025 United Nations Population Fund (UNFPA) report, approximately 60% of the global population or 4.3 billion people resides in Asia Pacific, with large proportions historically underserved by diagnostic infrastructure. India and China are seeing steady expansion in private diagnostic lab networks, while local firms are forming alliances with global players to bring advanced testing tools to market.

Japan Allergy and Autoimmune Disease Diagnostics Market Trends

Japan holds a dominant position in Asia Pacific, and the market is rapidly surging due to increasing prevalence of allergic rhinitis, asthma, and food allergies, mainly in children. The country has a uniquely well-documented allergy crisis boosted by a single allergen. More than one-third of all people have cedar pollinosis (sugi-pollinosis), and cases have increased significantly over the last two decades. This has created a large and diagnostically active population that regularly engages with allergy testing and immunotherapy. Owing to the aforementioned factors, the country is projected to account for a share of approximately 24.3% in 2026.

China Allergy and Autoimmune Disease Diagnostics Market Trends

In 2026, China is estimated to account for a share of nearly 10.8% in Asia Pacific, backed by rising allergy prevalence among children and government-led public health programs emphasizing early detection. Increasing air pollution in key cities, dietary transitions toward Western food patterns, and shifts away from rural living have all raised sensitization rates. China's National Health Commission has backed healthcare reform initiatives that include substantial investments in diagnostic capabilities, with the 14th Five-Year Plan dedicating approximately US$240 billion to healthcare infrastructure development.

Europe Allergy and Autoimmune Disease Diagnostics Market Trends

Europe will likely see steady growth over the forecast period with a share of nearly 17.6% in 2026. The continent’s growth is built on regulatory rigor, high disease burden, and the strength of its domestic diagnostics industry. According to the European Federation of Clinical Chemistry and Laboratory Medicine, over 60% of tertiary hospitals in Western Europe adopted multiplex bead-based or chemiluminescent platforms between 2020 and 2024, replacing the traditional indirect immunofluorescence for ANA detection. This technology upgrade cycle is a prominent growth catalyst.

Germany Allergy and Autoimmune Disease Diagnostics Market Trends

Germany will likely lead in Europe with a regional market share of approximately 22.4% in 2026. The German Society of Rheumatology confirms that over 95% of rheumatology centers use standardized autoantibody panels complied with EULAR recommendations. The country also hosts leading diagnostic manufacturers, including EUROIMMUN and Thermo Fisher Scientific's clinical diagnostics division. The national health insurance system reimburses comprehensive autoimmune panels, including anti-CCP, anti-dsDNA, and ENA profiles, without requiring prior stepwise testing. Hence, patients can access broad-panel testing from the first specialist visit, shortening the diagnostic journey and increasing test volumes.

U.K. Allergy and Autoimmune Disease Diagnostics Market Trends

The U.K. is anticipated to hold a share of approximately 15.7% in 2026 in Europe. Approximately 44% of the country’s adult population and up to 40% of children experience at least one allergy. The National Health Service’s (NHS) integration of allergy services in primary care and hospitals has strengthened demand for reliable testing platforms. In August 2025, London Allergy Care and Knowledge reported that around 20% of U.K. schoolchildren suffer from asthma, 15% from hay fever, 10 to 16% from eczema, and 6 to 8% from food allergies. The NHS has been moving toward AI-assisted and molecular testing, which is predicted to bolster diagnostic throughput.

Competitive Landscape

The global allergy and autoimmune disease diagnostics market is moderately consolidated with a handful of multinational diagnostics companies controlling the high-value immunoassay and autoantibody testing segments. The market is led by companies such as Thermo Fisher Scientific, Siemens Healthineers, Danaher Corporation, Bio-Rad Laboratories, Abbott Laboratories, and Revvity through its EUROIMMUN business. Together, key players account for a significant share of global testing revenues, especially in laboratory-based allergy and autoimmune diagnostics.

In autoimmune diagnostics, competition has shifted toward disease-specific autoantibody panels and AI-assisted interpretation tools. Companies such as EUROIMMUN, Inova Diagnostics (Werfen), DiaSorin, and Bio-Rad are investing heavily in advanced ANA, ENA, and multiplex autoimmune assays that can improve diagnostic accuracy for complex diseases such as rheumatoid arthritis, systemic lupus erythematosus, and Sjögren’s syndrome.

Key Industry Developments:

- In November 2025, Exagen Inc. reported Q3 2025 results and announced the commercial launch of seronegative RA markers for anti-PAD4 as the latest addition to its AVISE CTD panel. The company also presented six abstracts at the American College of Rheumatology Conference, including a plenary presentation on the development of a lupus nephritis diagnostic platform.

- In August 2025, AliveDx announced that its MosaiQ instrument had been registered with the U.S. FDA as a Class II 510(k) exempt medical device, authorizing its use in U.S. clinical laboratories. The MosaiQ platform is a continuous random-access immunoassay system designed for multiplex testing of autoimmune diseases, allergies, and related conditions.

- In July 2025, InBio and Beckman Coulter Life Sciences announced a collaboration to improve food allergy research by integrating InBio's purified food protein standards and allergen components with Beckman Coulter's Next-Generation BAT platform. The combined solution is intended to allow multi-allergen testing from a single blood draw with improved reproducibility across high-sensitivity assays.

Companies Covered in Allergy and Autoimmune Disease Diagnostics Market

- Thermo Fisher Scientific, Inc.

- HYCOR Biomedical

- EUROIMMUN Medizinische Labordiagnostika AG (PerkinElmer, Inc.)

- Omega Diagnostics Group PLC

- Lincoln Diagnostics, Inc.

- AESKU.GROUP GmbH

- Minaris Medical America, Inc.

- HOB Biotech Group Corp., Ltd.

- DASIT Group SPA

- R-Biopharm AG

- bioMérieux

- Siemens Healthcare GmbH

- Hoffmann-La Roche Ltd.

- Abbott

- Beckman Coulter, Inc.

- Danaher Corporation

- Quest Diagnostics

- Inova Diagnostics Pte Ltd.

- Others

Frequently Asked Questions

The global allergy and autoimmune disease diagnostics market is projected to be valued at US$13.7 billion in 2026.

The market is expected to reach US$21.4 billion by 2033.

Key market trends include the shift toward precision diagnostics and rising adoption of blood-based testing.

Reagents and consumables are expected to be the leading product and service with a share of nearly 64.3% in 2026, as labs are shifting toward high-throughput automated systems.

The allergy and autoimmune disease diagnostics market is expected to grow at a CAGR of 6.6% from 2026 to 2033.

Thermo Fisher Scientific, Inc., HYCOR Biomedical, and EUROIMMUN Medizinische Labordiagnostika AG (PerkinElmer, Inc.) are a few key market players.