- Automotive

- Airport Shuttle Bus Market

Airport Shuttle Bus Market Size, Share, and Growth Forecast 2026 - 2033

Airport Shuttle Bus Market by Propulsion Type (ICE, Electric), Seating Capacity (Below 25, 26-40, Above 40), Service Type (Terminal-City Shuttle, Inter-Terminal/Parking Shuttle, Hotel/Staff Shuttle), and Regional Analysis for 2026 - 2033

Airport Shuttle Bus Market Size and Trend Analysis

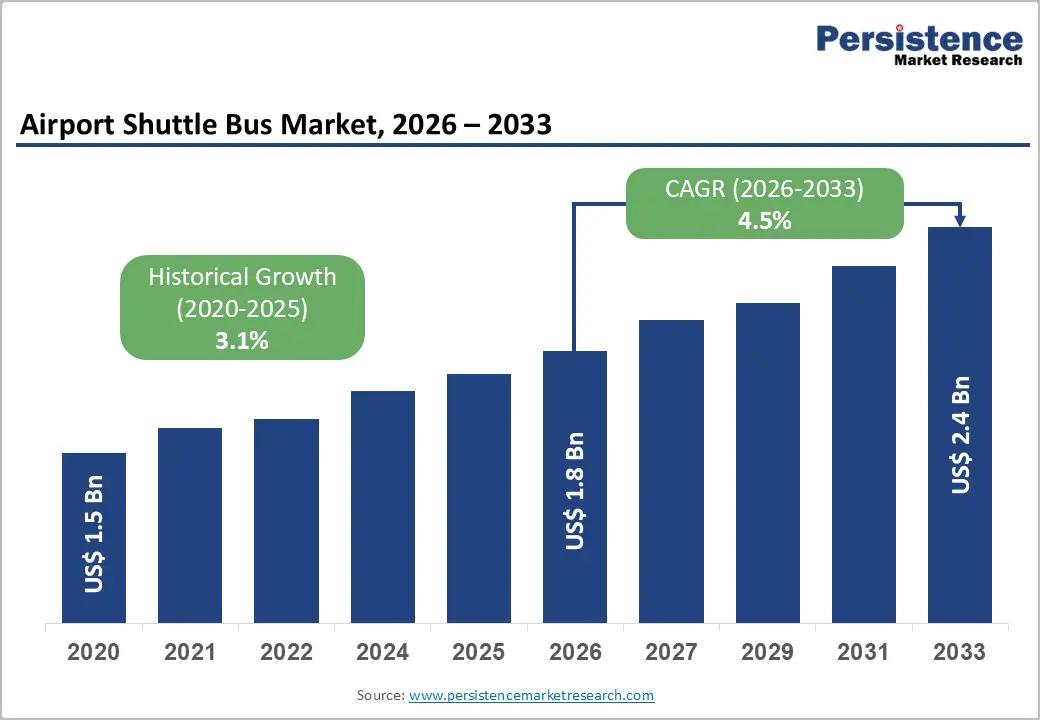

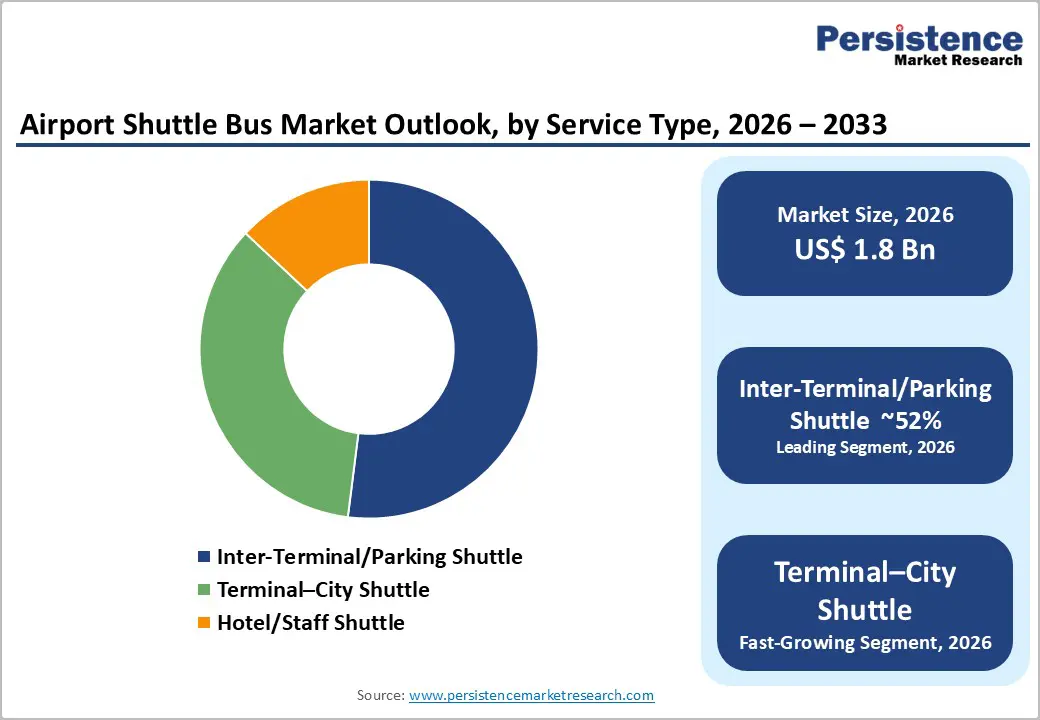

The global airport shuttle bus market size is likely to be valued at US$ 1.8 billion in 2026 and is projected to reach US$ 2.4 Bn by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

The market's sustained growth is fundamentally driven by the robust recovery and continued expansion of global air passenger traffic, which directly necessitates larger and more efficient ground transportation fleets at airport terminals. According to the International Air Transport Association (IATA), global air passenger numbers rebounded to approximately 4.7 billion passengers in 2024, surpassing pre-pandemic peaks, and are projected to reach 7.8 billion by 2043. This long-term growth trajectory is compelling airport operators worldwide to invest in larger, more sustainable shuttle bus fleets.

Key Industry Highlights:

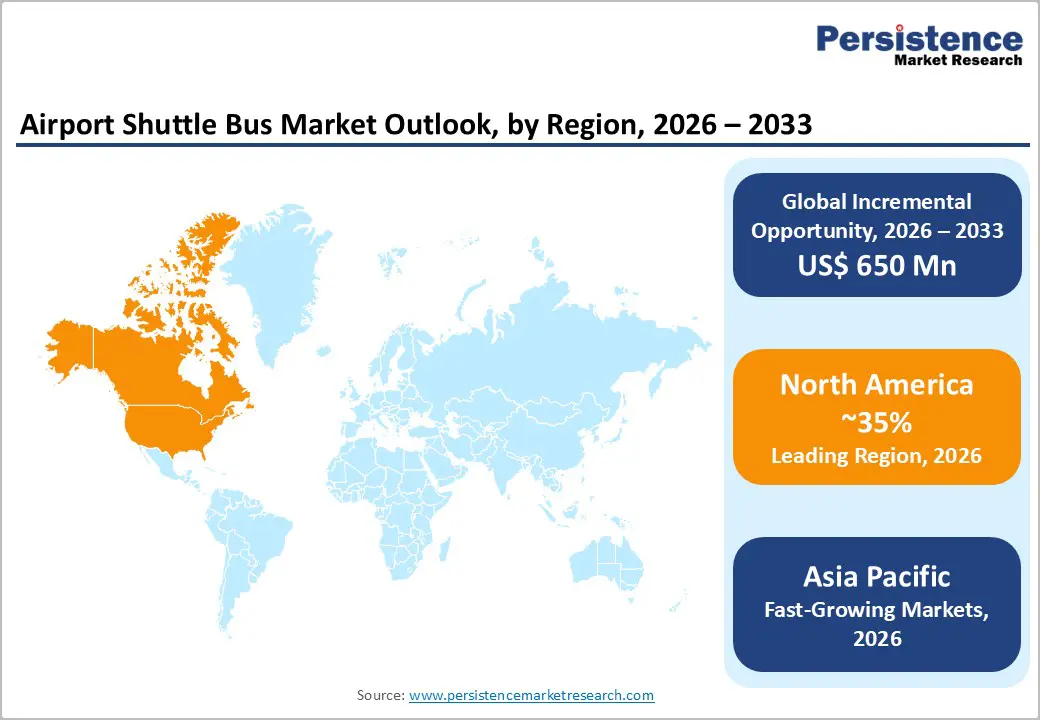

- Leading Region: North America leads the global Airport Shuttle Bus market in revenue, supported by the FAA's US$ 14.5 Bn airport infrastructure investment (May 2025), electric bus adoption at major hubs including Denver International Airport and JFK, and IRA clean vehicle tax credits.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by India's US$ 25 Bn airport infrastructure plan targeting 50 new airports by 2030, Yutong's major Asian airport contracts (October 2024), and China's large-scale electric apron bus fleet deployments.

- Dominant Segment: The Above 40 Seats capacity segment dominates with approximately 58% of market revenue, anchored by the COBUS 3000's 110-passenger capacity (per IATA AHM 950) and its status as the world's most widely deployed purpose-built airport apron bus across 100+ countries.

- Fastest Growing Segment: Electric propulsion is the fastest-growing segment, with COBUS Industries reporting a notable 2024 electric order surge, Dinobus' 210 kWh LFP bus (150 km range) launched in March 2024, and SVPI Ahmedabad's 24/7 electric inter-terminal service from December 2024.

- Key Market Opportunity: Hydrogen fuel cell airport buses led by COBUS Hydra (Toyota Fuel Cell Stack, 400 km range, sub-9-minute refuel) and identified by Dubai International Airport as a priority zero-emission technology represent the market's highest-value premium product opportunity through 2033.

| Key Insights | Details |

|---|---|

| Airport Shuttle Bus Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.4 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.5% |

| Historical Market Growth (2020 - 2025) | 3.1% |

Market Dynamics

Drivers - Surging Global Air Passenger Traffic Expanding Airport Ground Transportation Demand

The most foundational demand driver for the Airport Shuttle Bus market is the continuous, long-term expansion of global air passenger volumes which directly increases the number of passengers requiring inter-terminal, apron, and city-link shuttle transfers at airports worldwide. IATA confirmed that global air passengers recovered to approximately 4.7 billion in 2024, exceeding pre-pandemic record levels, and projects growth to 7.8 billion passengers by 2043. In line with this, domestic air passenger traffic witnessed a 6.12% year-on-year increase in 2024, reaching 161.3 million passengers across reporting markets. As airport boarding bridge availability fails to keep pace with expanded operations particularly at high-traffic international hubs and newly constructed satellite terminals operators are increasingly relying on shuttle buses to manage apron-side passenger movements efficiently.

Airport Decarbonization Mandates Driving Fleet Electrification and Premium Vehicle Investment

The global aviation industry's commitment to reaching net-zero carbon emissions by 2050as adopted by the International Civil Aviation Organization (ICAO) and Airports Council International (ACI)is compelling airport operators to proactively electrify their ground transportation fleets, generating sustained demand for premium electric and hydrogen-powered Airport Shuttle Bus. This transition directly elevates the average unit sale value of shuttle buses, supporting total market revenue growth that outpaces unit volume growth alone. COBUS Industries delivered its 5,000th apron bus in September 2025 to British Airways and reported a significant surge in orders for electric buses in 2024, particularly in Europe and North America. Dinobus launched its 14-meter Pure Electric Airport Bus in March 2024, capable of traveling up to 150 km on a single charge with its 210 kWh LFP battery pack.

Restraints - High Capital Expenditure of Electric Bus Procurement and Charging Infrastructure

A material barrier slowing the pace of electric airport shuttle bus adoption is the substantially higher upfront procurement cost of electric buses compared to conventional ICE (Internal Combustion Engine) alternatives, compounded by the significant capital investment required to install and maintain airport-side charging infrastructure. Electric Airport Shuttle Bus carry purchase prices approximately 40-60% higher than comparable diesel variants, placing significant pressure on the capital budgets of airport operators particularly at regional and secondary airports with tighter fiscal constraints. Airports must additionally retrofit or newly construct high-capacity charging depots, with typical infrastructure costs of US$ 50,000-US$ 150,000 per charging point, creating total electrification project costs running into millions of dollars for medium-sized bus fleets.

Competition from Automated People Movers and Alternative Ground Transport Solutions

Airport Shuttle Bus faces increasing indirect competition from Automated People Movers (APMs), fixed-route inter-terminal rail systems, and expanded airport boarding bridge infrastructure all of which reduce passenger dependency on shuttle buses at major hub airports. ACI World reports that over 70 international airports globally have installed or are planning APM systems, reducing the addressable market for traditional inter-terminal shuttle bus services at large airports. The rise of ride-sharing services and private mobility solutions for city-link airport transfers additionally constrains growth in the terminal-city shuttle service type segment, particularly in markets with well-developed urban mobility ecosystems such as Singapore, London, and San Francisco.

Opportunities - Hydrogen Fuel Cell Airport Buses as a Zero-Emission Range-Extension Solution

The development and commercial deployment of the hydrogen fuel cell Airport Shuttle Bus represent one of the most technically compelling and commercially differentiated growth opportunities in the airport shuttle bus market for the 2026-2033 forecast period. Unlike battery-electric buses which face range limitations and extended recharging downtime in high-duty-cycle airport operations hydrogen fuel cell systems offer refuelling times of under nine minutes and range of up to 400 km, making them inherently well-suited to the operational tempo of large international airports. COBUS Industries has developed the COBUS Hydrathe world's first hydrogen-powered airport bus in partnership with Toyota, utilizing Toyota Fuel Cell Stack technology.

Airport Infrastructure Expansion in Emerging Markets Creating New Fleet Procurement Cycles

The large-scale airport construction and expansion programs underway across Asia Pacific, the Middle East, and South Asia represent a structurally significant demand opportunity for airport shuttle bus manufacturers seeking to capture new fleet procurement cycles in high-growth markets. India's government announced plans to invest approximately US$ 25 Bn in airport infrastructure in early 2025, targeting the development of 50 new greenfield airports and the expansion of over 100 existing airports by 2030 under the Ministry of Civil Aviation's UDAN scheme. Dubai welcomed 14.96 million overnight visitors from January to October 2024an 8% increase year-on-year, cementing Dubai International Airport's position as one of the world's busiest hubs and sustaining fleet expansion demand.

Category-wise Analysis

Propulsion Type Insights

The ICE (Internal Combustion Engine) propulsion segment currently retains the dominant position in the global Airport Shuttle Bus market, accounting for approximately 72% of total market revenue. Diesel-powered buses have historically dominated airport fleets due to their lower acquisition cost, established refuelling infrastructure, and operational reliability across extreme temperature ranges conditions present in airports from the Middle East to Northern Scandinavia. Industry data confirms that the diesel fuel segment held over 85% of airport shuttle bus fleet share as recently as 2023, underscoring the depth of ICE entrenchment. However, the electric segment is the fastest-growing propulsion type by a significant margin, with TAM-Europe reporting that its electric eVivAir series was the most popular product in 2024 across Europe and North America, and COBUS Industries' CEO confirming a particularly notable surge in orders for electric-powered buses through 2024.

Seating Capacity Insights

The Above 40 seats seating capacity segment commands the dominant market position, accounting for approximately 58% of the total airport shuttle bus market revenue. Large-capacity buses are the preferred operational choice at high-volume international airports, where maximizing passenger throughput per bus movement is critical to managing apron congestion and reducing total fleet operating cost per passenger transported. The COBUS 3000 flagship model the world's most widely deployed airport apron bus accommodates up to 110 passengers per trip (per IATA AHM 950 standards), approximately double the capacity of a standard city bus, enabling airports to move large boarding groups to remote stand positions efficiently. COBUS Industries delivered its 5,000th apron bus in September 2025, the vast majority of which are high-capacity models serving major international airports.

Service Type Analysis

The Inter-Terminal/Parking Shuttle service type segment leads the Airport Shuttle Bus market, representing approximately 52% of total market revenue. This dominance reflects the operational architecture of large international airports, which increasingly feature multiple widely separated terminal buildings, satellite piers, and expansive remote parking infrastructure that necessitate continuous, high-frequency shuttle services operating on dedicated routes. International airports account for approximately 68.9% of the total airport bus market demand, according to industry analysis, with high passenger volumes and complex multi-terminal layouts generating the greatest shuttle bus utilization rates globally. The Sardar Vallabhbhai Patel International Airport in Ahmedabad launched dedicated free electric shuttle buses connecting Terminals 1 and 2 in December 2024, operating 24/7 every 30 minutes, with Wi-Fi, climate control, and CCTV exemplifying the premium inter-terminal shuttle service standard increasingly expected at major hubs globally.

Regional Insights

North America Airport Shuttle Bus Market Trends

North America is the leading revenue market for Airport Shuttle Bus in absolute terms, with the United States representing the dominant national market driven by its concentration of major international hub airports including Hartsfield-Jackson Atlanta International Airport, Dallas/Fort Worth International Airport, Denver International Airport (DIA), and John F. Kennedy International Airport.

From a regulatory standpoint, the U.S. EPA's Volkswagen Environmental Mitigation Trust and the Inflation Reduction Act's (IRA) clean commercial vehicle tax credits are providing direct financial incentives for airport operators to procure zero-emission shuttle buses. In April 2024, the Little Rock Municipal Airport Commission approved the purchase of two 14-passenger electric shuttle buses from Endera for long-term parking-to-terminal transfers, reflecting the pervasive adoption of electric shuttle technology even at secondary U.S. airports.

Europe Airport Shuttle Bus Market Trends

Europe represents the most technologically advanced and sustainability-driven regional market for Airport Shuttle Bus, with Germany, the United Kingdom, France, Spain, and Turkey serving as the region's primary demand centres. European airports operate under some of the world's most stringent emission standards, with the European Green Deal and EU Fit for 55 packages mandating measurable decarbonization of airport ground operations, directly accelerating the transition away from diesel shuttle buses toward electric and alternative-fuel platforms.

The United Kingdom has been an early adopter of electric airport bus trials, with Bristol Airport, Glasgow Airport, and London Stansted Airport all having conducted COBUS electric bus pilot programs between 2021 and 2022, paving the way for full commercial fleet transitions. Regulatory harmonization across EU member states under the Clean Vehicles Directive requires that a minimum percentage of public authority vehicle procurement meet zero-emission standards, directly influencing airport operator bus purchasing decisions.

Asia Pacific Airport Shuttle Bus Market Trends

Asia Pacific is the fastest-growing regional market for Airport Shuttle Bus and simultaneously the largest by volume, driven by China's massive and expanding airport network, India's ambitious greenfield airport development program, and Japan, South Korea, Singapore, and ASEAN nations investing heavily in airport capacity expansion to accommodate long-term air travel growth. Zhengzhou Yutong Group (Yutong) secured significant new airport bus orders from major Asian airports in October 2024, reflecting the company's dominant position across the region's bus procurement ecosystems.

India's government announced plans to invest approximately US$ 25 Bn in airport infrastructure in 2025, targeting 50 new greenfield airports under the UDAN regional connectivity scheme. Sardar Vallabhbhai Patel International Airport in Ahmedabad launched a free 24/7 electric inter-terminal shuttle service in December 2024 as a precursor to full fleet electrification reflecting India's policy momentum toward clean airport ground operations.

Competitive Landscape

The global airport shuttle bus market is moderately concentrated, with COBUS Industries, Zhengzhou Yutong Group, TAM-Europe, BYD Company Limited, and New Flyer Industries collectively accounting for approximately 50-55% of total market revenue. COBUS Industries' milestone delivery of its 5,000th apron bus in September 2025 confirms its global market leadership in purpose-built airport buses. Key competitive differentiators include purpose-built airport chassis design, IATA AHM 950-compliant high-density passenger configuration, electric and hydrogen propulsion capability, and established global after-sales service networks. Emerging business model trends include fleet-as-a-service leasing models, e. START diesel-to-electric conversion programs (COBUS), and digital fleet management software integrated with airport operations management systems.

Key Developments:

- In January 2026, BYD announced support for airport fleet electrification programs globally, emphasizing zero-emission shuttle solutions and partnerships with major airports.

- In December 2025, BYD ADL Enviro200EV electric buses introduced at Glasgow Airport car park shuttle service, replacing diesel models.

- In October 2025, Teesside International Airport announced a world-first driverless shuttle bus trial, testing eight-seat autonomous vehicles between terminals as part of a broader airport mobility innovation initiative.

Companies Covered in Airport Shuttle Bus Market

- COBUS Industries

- Zhengzhou Yutong Group Co., Ltd. (Yutong)

- TAM-Europe

- New Flyer Industries

- Motor Coach Industries (MCI)

- ENC (ElDorado National)

- Glaval Bus (Forest River)

- ABC Companies

- Xinfa Airport Equipment Ltd.

- Sanatan Bus Body Builders Pvt. Ltd.

Frequently Asked Questions

The global Airport Shuttle Bus market is valued at US$ 1.8 Bn in 2026 and is projected to reach US$ 2.4 Bn by 2033, growing at a CAGR of 4.5%.

The primary demand drivers include global air passenger traffic recovery to approximately 4.7 billion passengers in 2024 (IATA), with further growth projected to 7.8 billion by 2043, and airport decarbonization commitments by ICAO and ACI targeting net-zero by 2050 and driving electric bus fleet investments.

The Above 40 Seats segment dominates with approximately 58% of total market revenue. Large-capacity buses such as the COBUS 3000which accommodates up to 110 passengers per IATA AHM 950 standards, approximately double the capacity of a standard city bus are the operational standard at major international airports, minimizing per-passenger transport cost and reducing apron congestion during large aircraft boarding cycles.

North America leads global revenue, underpinned by the world's largest concentration of major hub airports, the FAA's US$ 14.5 Bn infrastructure investment, and IRA-driven electric bus procurement incentives. Asia Pacific is the fastest-growing region, powered by China's expanding airport network, India's US$ 25 Bn airport infrastructure plan targeting 50 new airports by 2030, and Yutong's dominant market position across the region.

The key market participants include COBUS Industries the global market leader with 5,000+ apron buses delivered across 100+ countries alongside Zhengzhou Yutong Group, TAM-Europe, BYD Company Limited, New Flyer Industries, Motor Coach Industries / MCI, ENC ElDorado National, Xinfa Airport Equipment Ltd., Dinobus, and Sanatan Bus Body Builders Pvt. Ltd., among others.