- Specialty & Fine Chemicals

- AI in Chemicals Market

AI in Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

AI in Chemicals Market by Technology (Machine Learning (ML), Deep Learning, Natural Language Processing (NLP), Computer Vision, Predictive Analytics, Generative AI), Application (Drug & Chemical Discovery, Process Optimization, Predictive Maintenance, Supply Chain Optimization, Quality Control & Inspection, Production Planning & Scheduling, Safety and Risk Management, Energy Management), Deployment Model (Cloud-based, On-premise, Hybrid), End-user, Regional Analysis, 2026 - 2033

AI in Chemicals Market Size and Trend Analysis

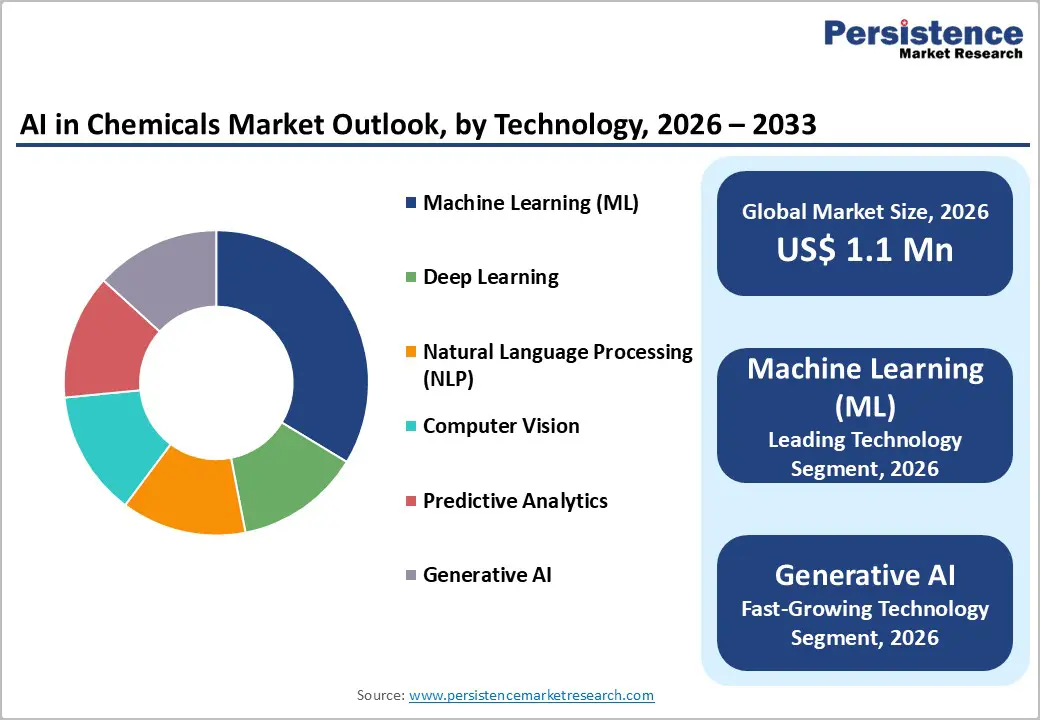

The global ai in chemicals market size is expected to be valued at US$ 1.1 Billion in 2026 and projected to reach US$ 6.4 Billion by 2033, growing at an exceptional CAGR of 28.7% between 2026 and 2033.

Accelerating digital transformation across the global chemicals industry, the exponential advancement of generative AI and machine learning platforms, and mounting pressure to reduce R&D timelines, operational costs, and carbon emissions are the principal forces driving this extraordinary market trajectory.

The global chemicals industry, representing over US$ 5 trillion in annual output according to the American Chemistry Council (ACC), is increasingly deploying AI across molecular discovery, process optimization, predictive maintenance, and supply chain management to unlock productivity gains estimated at US$ 500 billion annually by McKinsey & Company. Strategic investments by hyperscale technology providers including Microsoft, Google, and NVIDIA in AI infrastructure, combined with growing in-house AI capability building by major chemical companies such as BASF and Honeywell, are compounding adoption velocity across all subsectors of the global chemicals value chain.

Key Industry Highlights

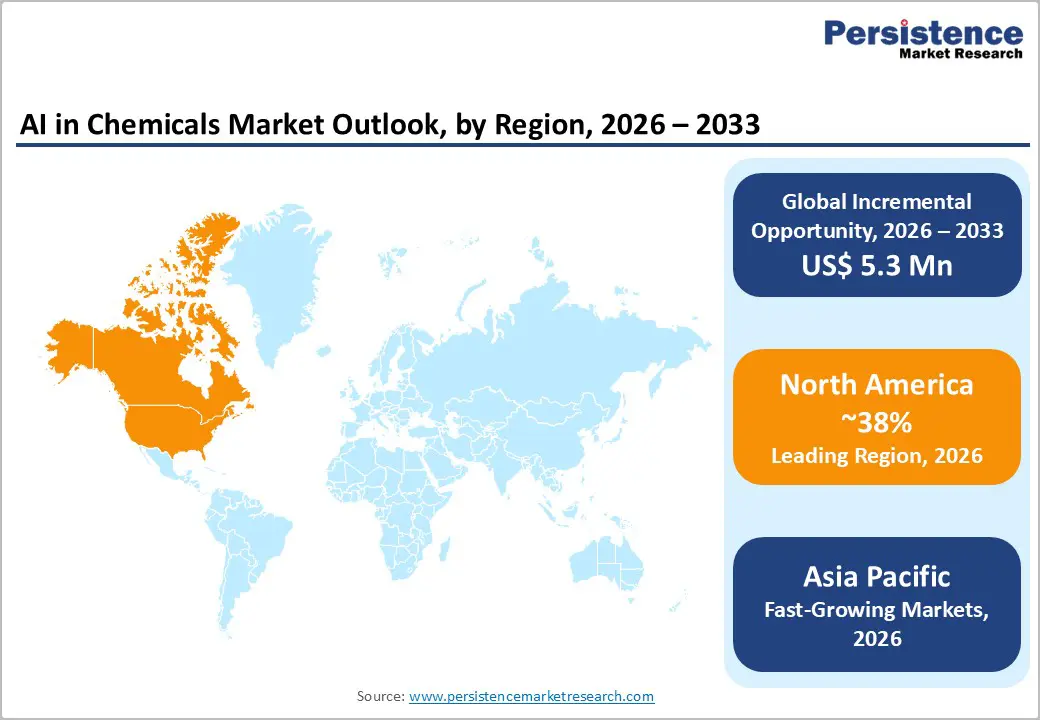

- Leading Region: North America commands approximately 38% of global AI in Chemicals market revenue in 2025, anchored by the world's most advanced AI ecosystem, U.S. National AI Initiative funding, and co-development partnerships between Silicon Valley hyperscalers and major chemical companies.

- Fastest Growing Region: Asia Pacific is projected to grow at a CAGR of 32% during 2026 - 2033, driven by China's New Generation AI Development Plan, Japan's materials AI programs, and India's rapidly digitizing mid-size chemical sector adopting cloud AI platforms.

- Dominant Segment: Machine Learning commands approximately 34% market share in 2025, deployed across process optimization, predictive maintenance, and quality control applications by leaders including BASF (with over 500 active ML models) and Honeywell.

- Fastest Growing Segment: Generative AI is the fastest growing technology segment, with platforms including NVIDIA BioNeMo, Insilico Medicine's Chemistry42, and Microsoft's Azure Chemistry Copilot enabling autonomous molecular discovery with 10-100x throughput gains over conventional R&D approaches.

- Key Market Opportunity: Unplanned chemical plant downtime costing approximately US$ 20 billion annually per ACC data, combined with IEA-reported 8-20% energy savings from AI process optimization, creates a compelling, high-certainty ROI opportunity for AI deployment across global petrochemical and specialty chemical operations.

| Key Insights | Details |

|---|---|

| AI in Chemicals Market Size (2026E) | US$ 1.1 Billion |

| Market Value Forecast (2033F) | US$ 6.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 28.7% |

| Historical Market Growth (2020 - 2025) | 23.4% |

Market Dynamics

Drivers - AI-Accelerated Molecular Discovery Reducing Chemical R&D Timelines and Costs

Traditional chemical and materials discovery processes are lengthy and capital-intensive, with average timelines from molecular conception to commercial scale spanning 10-15 years and costing hundreds of millions of dollars. AI, particularly machine learning-based molecular property prediction, generative chemistry models, and physics-informed neural networks, is fundamentally compressing these timelines. Google DeepMind's AlphaFold has already demonstrated the transformative power of AI in predicting protein structures, accelerating drug and biochemical discovery programs globally. The U.S. Department of Energy (DOE) has funded over US$ 400 million in AI for materials discovery programs since 2021, including the Materials Genome Initiative, recognizing AI's capacity to identify novel functional materials orders of magnitude faster than conventional combinatorial chemistry. Chemical companies deploying AI-driven discovery platforms report cycle time reductions of 40-70% for lead candidate identification, representing transformative competitive advantages.

Operational Excellence Imperative: AI-Driven Process Optimization and Energy Efficiency

The chemicals industry is one of the world's most energy-intensive manufacturing sectors, consuming approximately 10% of global industrial energy according to the International Energy Agency (IEA). Process optimization AI, using real-time sensor data, digital twins, and reinforcement learning algorithms, is enabling chemical plants to achieve energy consumption reductions of 8-20% and yield improvements of 3-10% without capital expenditure. Honeywell's Experion Process Knowledge System integrates AI optimization across refinery and petrochemical operations, reporting energy savings exceeding 5% per deployment. Siemens' Industrial AI platform similarly delivers real-time process control optimization across specialty chemical manufacturing. As chemical companies face intensifying regulatory pressure to reduce Scope 1 and 2 emissions under EU ETS and U.S. EPA climate frameworks, AI-enabled process efficiency has shifted from competitive advantage to regulatory necessity.

Restraints - Data Quality, Availability, and Integration Barriers in Legacy Chemical Plants

The majority of global chemical manufacturing assets were built decades before the digital era, operating on heterogeneous distributed control systems (DCS) and programmable logic controllers (PLC) that generate siloed, inconsistent, and poorly labeled process data. Over 60% of industrial companies cited poor data quality and legacy system integration as the primary barriers to successful AI deployment. Without reliable, high-quality process data, machine learning models cannot achieve the prediction accuracy required for production-critical applications, significantly limiting AI adoption scope in brownfield chemical plants that represent the majority of global production capacity.

AI Talent Scarcity and Domain Expertise Gap in the Chemicals Sector

Successful AI deployment in chemicals requires rare professionals combining deep chemical engineering domain expertise with advanced machine learning and data science capabilities, a talent intersection that remains critically scarce globally. The World Economic Forum (WEF) projects a global shortfall of over 85 million technology workers by 2030, with chemistry-AI interdisciplinary specialists among the scarcest. Chemical companies competing against technology firms, pharmaceuticals, and financial services for AI talent face significant wage premiums and high attrition rates, creating a sustained barrier to building self-sufficient in-house AI capability at scale.

Opportunities - Generative AI for Autonomous Materials and Formulation Discovery

The emergence of large-scale generative AI models trained on chemical knowledge, including IBM's MoLFormer, Microsoft's Azure Chemistry Copilot, and Insilico Medicine's Chemistry42 platform, represents the most transformative opportunity in the AI in chemicals market. Generative AI models can autonomously propose novel molecular structures with targeted functional properties, simulate reaction pathways, predict synthesis routes, and optimize formulation compositions, compressing the discovery-to-formulation cycle from years to weeks. Insilico Medicine became the first company to advance an AI-designed drug candidate into Phase II clinical trials in 2023, demonstrating validated proof of concept for generative AI in discovery workflows. Specialty chemical and agrochemical companies deploying generative AI platforms can unlock discovery pipelines with 10-100x greater throughput versus conventional R&D approaches, creating substantial competitive differentiation and patent pipeline advantages through the forecast period.

AI-Powered Predictive Maintenance and Digital Twin Integration in Petrochemicals

Unplanned downtime in petrochemical and specialty chemical plants costs the global chemicals industry an estimated US$ 20 billion annually according to the American Chemistry Council (ACC). AI-powered predictive maintenance, combining IoT sensor data, vibration analysis, and machine learning failure prediction models, reduces unplanned shutdowns by up to 70% and extends equipment service life by 20-25% according to Siemens AG white papers. Integration with AI-driven digital twin platforms enables real-time simulation of plant operations, enabling scenario testing and optimization without physical experimentation. AWS's partnership with SLB to deploy AI-powered digital oilfield solutions and Schneider Electric's EcoStruxure platform delivering AI-enabled plant optimization for chemicals clients exemplify the rapid commercial scaling of this opportunity, which carries both high ROI certainty and measurable sustainability benefits.

Category-wise Analysis

Technology Insights

Machine Learning (ML) is the leading technology segment in the global AI in Chemicals market, commanding approximately 34% of total market share in 2025. ML's dominance reflects its versatility and proven deployment maturity across the broadest range of chemicals industry applications, from process optimization and predictive maintenance to quality control and supply chain forecasting. ML algorithms, including gradient boosting, random forests, and neural network regressors, are extensively deployed on production process data in both real-time control and offline analytical modes. BASF's internal AI Center has trained over 500 ML models across its global production network for applications including catalyst performance prediction and yield optimization. Generative AI is the fastest growing technology segment, expanding at an above-market CAGR driven by the transformative potential of large chemical language models and molecular generative frameworks for autonomous discovery.

Application Insights

Process Optimization is the leading application segment in the global AI in Chemicals market, accounting for approximately 26% of total revenue share in 2025. Chemical manufacturing processes involve thousands of interdependent variables, temperature, pressure, flow rates, catalyst concentrations, and reaction kinetics, whose simultaneous optimization is beyond the capacity of conventional rule-based control systems. AI-driven process optimization platforms using reinforcement learning and model predictive control (MPC) are demonstrated to achieve 5-15% improvements in yield and throughput while simultaneously reducing energy and raw material consumption. Honeywell's Forge platform and Siemens' Opcenter AI are industry-recognized solutions in this segment. Drug & Chemical Discovery is the fastest growing application segment, propelled by the commercial scaling of generative AI and deep learning molecular simulation platforms, transforming pharmaceutical and specialty chemical R&D workflows.

Deployment Model Insights

Cloud-based deployment is the leading model in the global AI in Chemicals market, representing approximately 55% of total market share in 2025. Cloud platforms offer chemical companies immediate access to enterprise-grade GPU computing infrastructure, pre-trained AI foundation models, and scalable data storage without the capital expenditure of on-premise deployment. Hyperscale cloud providers, including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud have developed specialized chemical and life sciences AI services, including AWS HealthLake Chemistry and Azure OpenAI for Science, that lower the deployment barrier for chemical companies. The Hybrid model is the fastest-growing deployment approach, as chemical companies seek to balance cloud AI scalability benefits with on-premise data security requirements for sensitive proprietary process and formulation data.

End-user Insights

Specialty chemicals manufacturers represent the leading end-user segment in the global AI in Chemicals market, accounting for approximately 30% of total revenue share in 2025. Specialty chemical producers, encompassing performance materials, electronic chemicals, adhesives, coatings, and functional additives, face the most complex AI value proposition, with high-margin products justifying significant technology investment in AI-driven formulation discovery, quality assurance, and customer application development. Companies such as BASF, Evonik, and Clariant are among the most advanced in deploying AI across their specialty portfolios. The Pharmaceutical & Fine Chemical Manufacturers segment is the fastest growing end-user, driven by AI-accelerated drug discovery, regulatory compliance automation, and process analytical technology (PAT) adoption mandated by the FDA's Pharmaceutical Quality Initiative.

Regional Insights

North America AI in Chemicals Market Trends and Insights

North America is the leading regional market for AI in chemicals, commanding approximately 38% of global revenue share in 2025, driven by the world's most advanced AI technology ecosystem, large domestic chemical industry, and progressive regulatory frameworks supporting AI-enabled drug and materials innovation. The U.S. Executive Order on AI (October 2023) and the National AI Initiative Act are accelerating federal investment in AI research infrastructure, including chemistry and materials AI programs at Argonne National Laboratory and Oak Ridge National Laboratory. The proximity of major chemical companies to Silicon Valley and cloud AI hyperscalers in the U.S. facilitates rapid technology co-development partnerships.

The U.S. FDA's progressive stance on AI/ML in pharmaceutical manufacturing, articulated in its 2023 Action Plan for AI/ML-Based Software as a Medical Device, is enabling AI-accelerated pharmaceutical chemistry workflows at companies including Dow Inc., Eastman Chemical, and Celanese. Canada's Pan-Canadian AI Strategy, with CAD 443 million in Phase 2 funding, is building AI research clusters in Toronto and Montreal that are increasingly collaborating with North American chemical companies on materials and process AI applications.

Europe AI in Chemicals Market Trends and Insights

Europe is the second largest regional market for AI in chemicals, characterized by its world-leading specialty chemicals industry and the EU AI Act, the world's first comprehensive AI regulatory framework, which entered into force in August 2024. The EU AI Act's risk-based approach to AI governance is shaping deployment priorities across European chemical companies, creating demand for compliant, explainable AI solutions. Germany's chemical sector, the world's fourth largest, generating over € 200 billion annually per the German Chemical Industry Association (VCI), is the most intensive AI adopter in the region, with BASF, Evonik, and Covestro all operating dedicated AI centers of excellence.

The United Kingdom's AI Sector Deal and dedicated Life Sciences Vision funding are positioning UK chemical and pharmaceutical companies as AI-innovation leaders. France's national AI strategy, with € 1.5 billion allocated to AI research, is supporting specialty chemistry AI projects at TotalEnergies and Air Liquide. Spain's growing fine chemicals and agrichemical sector is increasingly adopting cloud AI platforms for formulation optimization and regulatory documentation automation, benefiting from EU Horizon Europe research funding.

Asia Pacific AI in Chemicals Market Trends and Insights

Asia Pacific is the fastest growing regional market for AI in chemicals, projected to register a CAGR of 32% during 2026-2033, driven by China's aggressive AI industrial policy, Japan's advanced materials manufacturing ecosystem, and India's rapidly digitizing chemical industry. China's New Generation AI Development Plan targets AI industry revenues of US$ 150 billion by 2030, with petrochemicals and specialty materials among prioritized sectors. Sinopec and PetroChina have launched dedicated AI-driven process optimization programs across their refining and petrochemical operations, with reported energy savings exceeding 8% per optimized unit.

Japan's chemicals AI ecosystem is anchored by deep OEM-supplier technology relationships and strong government support through METI's industrial AI programs. Sumitomo Chemical and Mitsubishi Chemical are deploying AI for polymer design and process optimization, while Asahi Kasei has integrated ML-based quality prediction across its specialty materials production. India's Digital India initiative and growing SaaS-based AI adoption among midsize chemical companies, leveraging platforms from Polymerize and SAP, are enabling cost-effective AI deployment even for companies without large in-house data science teams.

Competitive Landscape

The global AI in chemicals market is characterized by a highly fragmented and multi-layered competitive structure, involving technology providers, industrial software developers, and chemical companies deploying proprietary AI platforms. Market competition spans multiple layers including computing infrastructure, cloud-based AI platforms, industrial automation systems, and specialized analytics tools tailored for chemical research and manufacturing operations.

Key competitive strategies revolve around integrating artificial intelligence with existing industrial systems to enable advanced process optimization, predictive maintenance, and intelligent supply chain management. Companies are increasingly investing in domain-specific AI models capable of accelerating molecular discovery, materials design, and formulation development. Strategic collaborations between technology firms and chemical manufacturers are also becoming common, enabling co-development of industry-specific AI solutions. Additionally, AI-as-a-service platforms are gaining traction, allowing chemical companies to deploy scalable analytics tools without heavy infrastructure investments. Vendors are further strengthening their market position by offering integrated ecosystems that combine data platforms, simulation capabilities, and predictive analytics to enhance operational efficiency and innovation across chemical value chains.

Key Developments

- January 2026: Merck entered a strategic memorandum of understanding with ChemLex to integrate AI-enabled automated chemistry platforms into research workflows, targeting faster chemical discovery through automated synthesis, reaction optimization, and high-throughput experimentation across life science and electronics R&D programs.

- October 2025: ACD/Labs and Covestro launched an AI-powered solvent selection tool integrated into the Percepta platform, enabling chemists to use predictive modeling for faster, data-driven solvent recommendations that improve experimental efficiency and support more sustainable chemical research workflows.

- September 2025: Mstack launched Chemstack AI, a closed-loop AI-driven R&D platform designed to accelerate molecular synthesis and commercialization timelines from about 18 months to days, while helping the company achieve 10× revenue growth amid global chemical supply chain disruptions.

Companies Covered in AI in Chemicals Market

- Accenture

- BASF SE

- Google LLC (Alphabet Inc.)

- Honeywell International Inc.

- IBM Corporation

- Insilico Medicine

- Microsoft Corporation

- NVIDIA Corporation

- Siemens AG

- SLB (Schlumberger)

- Schneider Electric SE

- Amazon Web Services (AWS)

- SAP SE

- Xylem Inc.

- Polymerize

- Aspen Technology, Inc.

- Dassault Systèmes (BIOVIA)

- Schrödinger, Inc.

Frequently Asked Questions

The global AI in Chemicals market is expected to reach US$ 1.1 Billion in 2026 and is projected to grow to US$ 6.4 Billion by 2033 at a CAGR of 28.7% during 2026 - 2033.

The market is driven by the need for productivity improvements, faster chemical discovery, energy-efficient process optimization, and increasing digital transformation across chemical manufacturing.

North America leads the global AI in Chemicals market, supported by a strong AI technology ecosystem and widespread adoption of AI solutions in chemical research and manufacturing.

The key opportunity lies in generative AI for autonomous chemical and materials discovery, enabling significantly faster R&D and innovation in the chemicals sector.

Key companies include NVIDIA Corporation, Microsoft, Google LLC, IBM Corporation, Honeywell International Inc., Siemens AG, AWS, BASF SE, Insilico Medicine, SAP SE, Schneider Electric, and Polymerize.cturers.