- Executive Summary

- Global Parking Management System Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Mn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Digital Transformation and ICT Penetration

- Infrastructure Development Outlook

- Semiconductor Industry Outlook

- Government Infrastructure Spending

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis

- Price by Components

- Price Impact Factors

- Global Parking Management System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Parking Management System Market Outlook: Component

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Component, 2020-2025

- Current Market Size (US$ Mn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Access Control

- Security and Surveillance

- Revenue Management

- Parking Reservation & Booking

- Permit Management

- Parking Guidance

- Others

- Services

- System Integration & Installation

- Software Configuration & Customization

- Maintenance & Technical Support

- Training & Consulting

- Managed Services

- Market Attractiveness Analysis: Component

- Global Parking Management System Market Outlook: Deployment

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Deployment, 2020-2025

- Current Market Size (US$ Mn) Forecast, by Deployment, 2026-2033

- On-Premise

- Cloud-Based

- Hybrid

- Market Attractiveness Analysis: Deployment

- Global Parking Management System Market Outlook: Location

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Location, 2020-2025

- Current Market Size (US$ Mn) Forecast, by Location, 2026-2033

- On-Street Parking

- Off-Street Parking

- Market Attractiveness Analysis: Location

- Global Parking Management System Market Outlook: End User

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by End User, 2020-2025

- Current Market Size (US$ Mn) Forecast, by End User, 2026-2033

- Municipal & Government

- Private Parking Operators

- Commercial

- Residential

- Transportation & Transit

- Market Attractiveness Analysis: End User

- Global Parking Management System Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) Analysis by Region, 2020-2025

- Current Market Size (US$ Mn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Parking Management System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- North America Market Size (US$ Mn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Mn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Access Control

- Security and Surveillance

- Revenue Management

- Parking Reservation & Booking

- Permit Management

- Parking Guidance

- Others

- Services

- System Integration & Installation

- Software Configuration & Customization

- Maintenance & Technical Support

- Training & Consulting

- Managed Services

- North America Market Size (US$ Mn) Forecast, by Deployment, 2026-2033

- On-Premise

- Cloud-Based

- Hybrid

- North America Market Size (US$ Mn) Forecast, by Location, 2026-2033

- On-Street Parking

- Off-Street Parking

- North America Market Size (US$ Mn) Forecast, by End User, 2026-2033

- Municipal & Government

- Private Parking Operators

- Commercial

- Residential

- Transportation & Transit

- Europe Parking Management System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Europe Market Size (US$ Mn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Benelux

- Nordics

- Rest of Europe

- Europe Market Size (US$ Mn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Access Control

- Security and Surveillance

- Revenue Management

- Parking Reservation & Booking

- Permit Management

- Parking Guidance

- Others

- Services

- System Integration & Installation

- Software Configuration & Customization

- Maintenance & Technical Support

- Training & Consulting

- Managed Services

- Europe Market Size (US$ Mn) Forecast, by Deployment, 2026-2033

- On-Premise

- Cloud-Based

- Hybrid

- Europe Market Size (US$ Mn) Forecast, by Location, 2026-2033

- On-Street Parking

- Off-Street Parking

- Europe Market Size (US$ Mn) Forecast, by End User, 2026-2033

- Municipal & Government

- Private Parking Operators

- Commercial

- Residential

- Transportation & Transit

- East Asia Parking Management System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- East Asia Market Size (US$ Mn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Mn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Access Control

- Security and Surveillance

- Revenue Management

- Parking Reservation & Booking

- Permit Management

- Parking Guidance

- Others

- Services

- System Integration & Installation

- Software Configuration & Customization

- Maintenance & Technical Support

- Training & Consulting

- Managed Services

- East Asia Market Size (US$ Mn) Forecast, by Deployment, 2026-2033

- On-Premise

- Cloud-Based

- Hybrid

- East Asia Market Size (US$ Mn) Forecast, by Location, 2026-2033

- On-Street Parking

- Off-Street Parking

- East Asia Market Size (US$ Mn) Forecast, by End User, 2026-2033

- Municipal & Government

- Private Parking Operators

- Commercial

- Residential

- Transportation & Transit

- South Asia & Oceania Parking Management System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- South Asia & Oceania Market Size (US$ Mn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Mn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Access Control

- Security and Surveillance

- Revenue Management

- Parking Reservation & Booking

- Permit Management

- Parking Guidance

- Others

- Services

- System Integration & Installation

- Software Configuration & Customization

- Maintenance & Technical Support

- Training & Consulting

- Managed Services

- South Asia & Oceania Market Size (US$ Mn) Forecast, by Deployment, 2026-2033

- On-Premise

- Cloud-Based

- Hybrid

- South Asia & Oceania Market Size (US$ Mn) Forecast, by Location, 2026-2033

- On-Street Parking

- Off-Street Parking

- South Asia & Oceania Market Size (US$ Mn) Forecast, by End User, 2026-2033

- Municipal & Government

- Private Parking Operators

- Commercial

- Residential

- Transportation & Transit

- Latin America Parking Management System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Latin America Market Size (US$ Mn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Mn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Access Control

- Security and Surveillance

- Revenue Management

- Parking Reservation & Booking

- Permit Management

- Parking Guidance

- Others

- Services

- System Integration & Installation

- Software Configuration & Customization

- Maintenance & Technical Support

- Training & Consulting

- Managed Services

- Latin America Market Size (US$ Mn) Forecast, by Deployment, 2026-2033

- On-Premise

- Cloud-Based

- Hybrid

- Latin America Market Size (US$ Mn) Forecast, by Location, 2026-2033

- On-Street Parking

- Off-Street Parking

- Latin America Market Size (US$ Mn) Forecast, by End User, 2026-2033

- Municipal & Government

- Private Parking Operators

- Commercial

- Residential

- Transportation & Transit

- Middle East & Africa Parking Management System Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Middle East & Africa Market Size (US$ Mn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Mn) Forecast, by Component, 2026-2033

- Hardware

- Software

- Access Control

- Security and Surveillance

- Revenue Management

- Parking Reservation & Booking

- Permit Management

- Parking Guidance

- Others

- Services

- System Integration & Installation

- Software Configuration & Customization

- Maintenance & Technical Support

- Training & Consulting

- Managed Services

- Middle East & Africa Market Size (US$ Mn) Forecast, by Deployment, 2026-2033

- On-Premise

- Cloud-Based

- Hybrid

- Middle East & Africa Market Size (US$ Mn) Forecast, by Location, 2026-2033

- On-Street Parking

- Off-Street Parking

- Middle East & Africa Market Size (US$ Mn) Forecast, by End User, 2026-2033

- Municipal & Government

- Private Parking Operators

- Commercial

- Residential

- Transportation & Transit

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- IBM Corporation

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Siemens AG

- Bosch Group

- Amano Corporation

- SKIDATA GmbH

- SWARCO AG

- Kapsch TrafficCom

- T2 Systems, Inc.

- Atos SE

- SAP SE

- FlashParking Inc.

- ParkMobile LLC

- Others

- IBM Corporation

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Communication Infrastructure & Services

- Parking Management System Market

Parking Management System Market Size, Share, and Growth Forecast, 2026 - 2033

Parking Management System Market by Component (Hardware, Software, Services), Deployment (On-Premises, Cloud-Based, Hybrid), Location (On-Street Parking, Off-Street Parking), End-user, and Regional Analysis for 2026 - 2033

Parking Management System Market Size and Trends

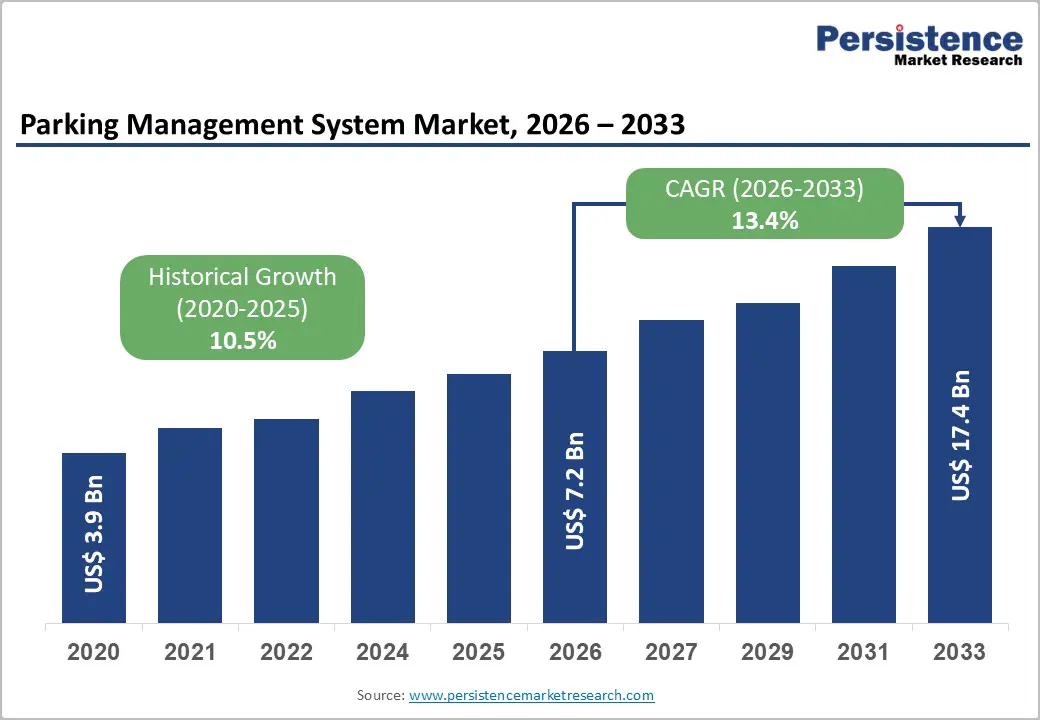

The global parking management system market size is projected to rise from US$7.2 billion in 2026 to US$17.4 billion by 2033. It is anticipated to witness a CAGR of 13.4% during the forecast period from 2026 to 2033, driven by escalating urbanization, technological innovation in IoT and AI, and heightened regulatory focus on sustainable urban mobility.

The market's trajectory reflects the critical role parking management systems play in addressing urban congestion, optimizing space utilization, and supporting smart city infrastructure development worldwide. The exponential rise in vehicle ownership across emerging markets, integration of advanced technologies enabling real-time parking data analytics, and government mandates promoting electric vehicle infrastructure integration within parking ecosystems.

Key Industry Highlights:

- Leading Component: Hardware dominates with over 48% market share in 2026, valued above US$ 3.5 Bn, driven by essential physical infrastructure like sensors, barriers, cameras, and automated payment kiosks. Software is the fastest-growing segment at 17.2% CAGR, powered by AI, IoT, and predictive analytics for real-time monitoring, automated payments, and mobile reservations.

- Leading Deployment: On-premises hold over 46% market share in 2026, valued at above US$ 3.3 Bn, preferred for data control, regulatory compliance, and integration with legacy systems. Cloud-based deployments are the fastest-growing at 18.1% CAGR, enabling remote management, IoT integration, and scalable, user-friendly parking solutions.

- Leading Location: Off-street parking commands over 60% market share in 2026, valued above US$ 4.3 Bn, due to organized, secure parking demand in urban commercial spaces. On-street parking is fastest-growing at a positive CAGR, driven by urbanization, limited space, and smart mobility initiatives.

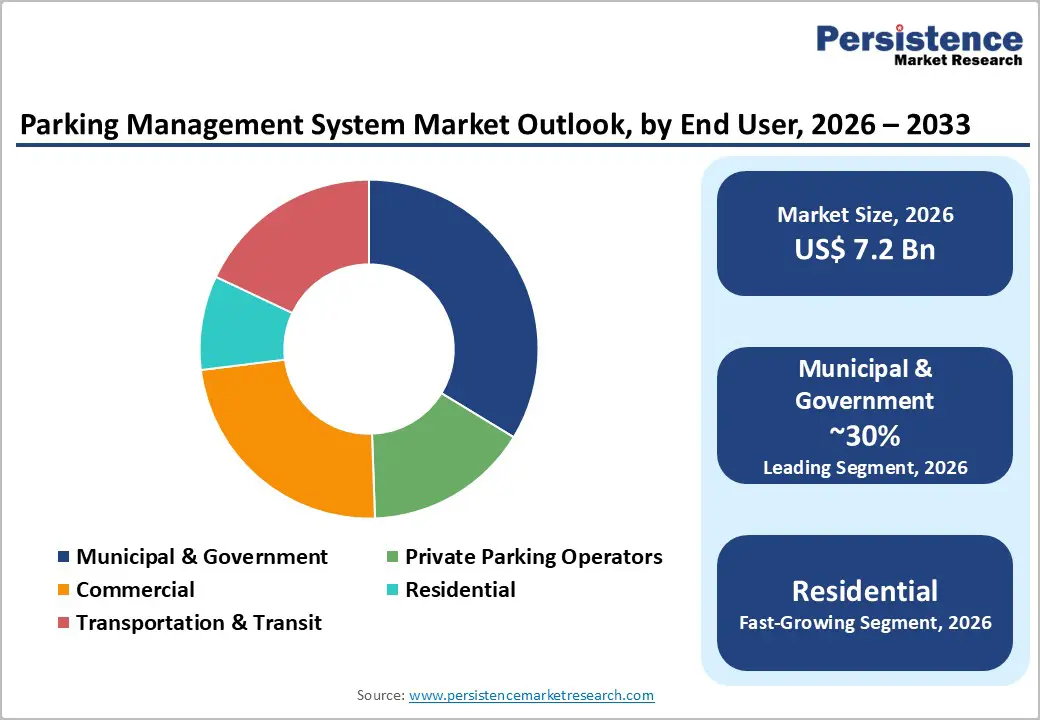

- Leading End-user: Municipal & government maintain dominance with over 30% market share in 2026, valued above US$ 2.2 Bn, supported by traffic management, smart city initiatives, and regulatory mandates. Residential parking is growing rapidly, driven by rising vehicle ownership and demand for secure, efficient solutions in urban housing complexes.

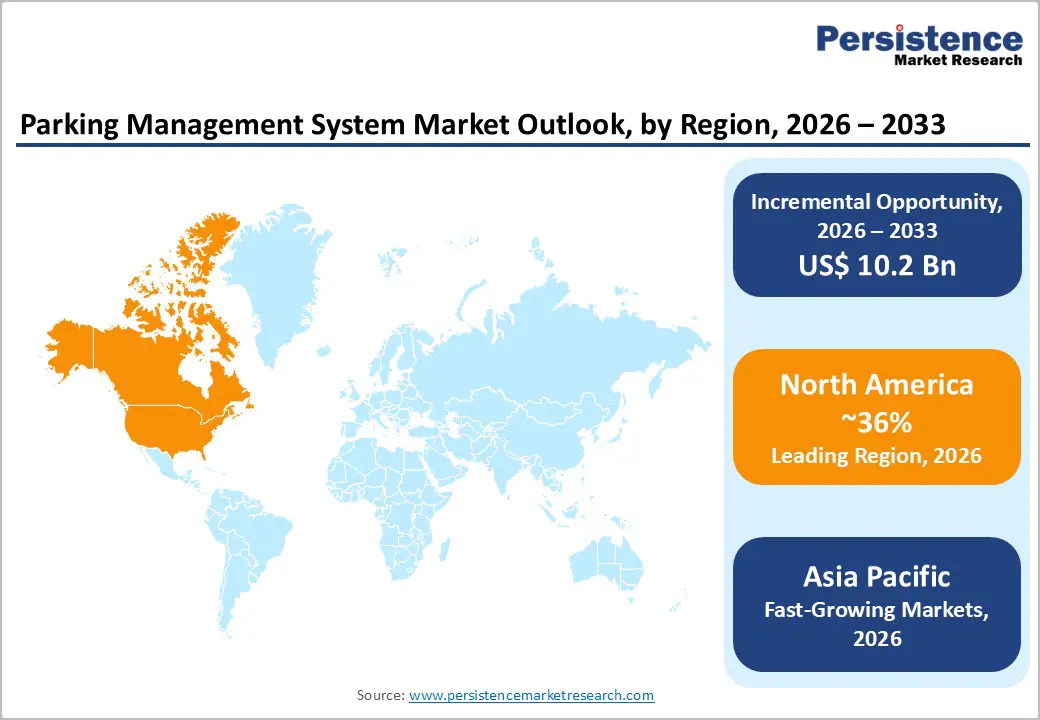

- Leading Region: North America leads with over 36% share in 2026, valued above US$ 2.6 Bn, led by the U.S. at ~US$ 1.9 Bn, supported by smart city programs and regulatory backing. Asia Pacific is the fastest-growing region at 17.8% CAGR, led by China and emerging Indian markets. Europe holds over 28% share by 2033, valued above US$ 2.0 Bn, driven by sustainable mobility policies and ITS adoption.

| Key Insights | Details |

|---|---|

|

Parking Management System Market Size (2026E) |

US$7.2 Bn |

|

Market Value Forecast (2033F) |

US$17.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

13.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

10.5% |

Market Dynamics

Driver - Urban Congestion and Traffic Management Imperatives

Urban traffic congestion imposes a significant economic burden, with parking searches contributing up to 30% of city traffic. Growing vehicle ownership, including the projected rise of U.S. electric vehicles from 3 million in 2022 to 12–24 million by 2030 noted by EIA, exacerbates this challenge. Traditional parking approaches are increasingly inadequate, while intelligent parking systems reduce search times by ~40% and traffic congestion by ~30% in well-implemented areas. These improvements translate into fuel savings, lower emissions, and smoother traffic flow, justifying municipal investments in such technologies.

Technological Advancement in IoT, AI, and Real-Time Analytics

The integration of IoT, AI, and cloud computing has revolutionized parking management, enabling real-time occupancy detection, predictive demand forecasting, and dynamic pricing. AI-powered license plate recognition and automated payment systems streamline access control and enforcement, reducing operational costs by approximately 18% through optimized space utilization and lower personnel requirements. These technological advancements, coupled with mobile apps and sensor networks, are accelerating the adoption of smart parking solutions among municipalities and private operators, enhancing efficiency and overall market growth.

Restraint - High Initial Capital Expenditure and Infrastructure Integration Complexity

High initial capital expenditure and implementation complexity pose significant barriers. Deploying comprehensive systems requires substantial investments in hardware (sensors, LPR cameras, signage), software licensing, system integration, and staff training, with per-facility costs ranging from US$ 50,000 to 500,000+ and mid-sized municipal projects often exceeding US$ 5–15 million. Integration with legacy infrastructure and payment systems adds technical and logistical challenges, particularly in densely populated urban areas. Extended payback periods (5–7 years) and uncertain ROI further limit adoption among smaller operators and municipalities.

Data Privacy, Cybersecurity, and Regulatory Uncertainty

Cloud-based parking management systems generate large volumes of personal location data, creating stringent compliance obligations under GDPR, CCPA, and emerging data protection regulations. This exposes organizations to significant liability from potential data breaches, necessitating high investment in cybersecurity and compliance infrastructure. Regulatory uncertainty around data retention, consent mechanisms, and cross-border data transfers adds operational complexity and cost unpredictability. As a result, some operators prefer on-premises solutions despite the efficiency of cloud deployments, slowing adoption and increasing total cost of ownership.

Opportunity - Integration with Autonomous Vehicle Ecosystems and Mobility-as-a-Service Platforms

Autonomous vehicle (AV) adoption is set to reshape parking management economics, driving demand for systems that enable vehicle-to-infrastructure communication for optimized drop-offs, pickups, and remote parking. This integration creates new software and services revenue streams, expected to contribute significantly to the market. Mobility-as-a-Service (MaaS) platforms further expand opportunities by linking parking with multi-modal transport and real-time transit data. Companies offering integrated parking within MaaS ecosystems achieve premium positioning and higher customer retention through enhanced service efficiency.

Data Monetization and Smart City Ecosystem Positioning

Parking management systems generate valuable data assets occupancy patterns, traffic flow characteristics, driver behavior, and urban mobility trends that municipalities and urban planners leverage for evidence-based infrastructure planning. Data monetization strategies, including anonymized analytics sales to transportation planning authorities, real estate developers, and retail operators, create secondary revenue streams beyond core parking operations. This opportunity positions parking management as foundational smart city infrastructure, creating organizational partnerships and integration opportunities with broader urban intelligence platforms.

Category-wise Analysis

Component Insights

Hardware dominates the global market, capturing more than 48% market share in 2026 with a value exceeding US$ 3.5 Bn as physical infrastructure is essential for smooth operations. Devices like parking sensors, ticketing machines, barriers, cameras, and automated payment kiosks form the backbone of any system, ensuring accurate vehicle detection, security, and real-time monitoring. The growing demand for smart and automated parking solutions, especially in urban areas with high vehicle density, drives hardware adoption. Frequent upgrades and integration with software platforms further reinforce hardware’s dominant role in meeting operational and user needs.

Software demonstrates the highest growth rate at 17.2% CAGR due to cities and enterprises increasingly requiring smarter, data-driven parking solutions. Advanced software enables real-time monitoring, automated payment, mobile reservations, and predictive analytics, meeting the rising demand for convenience and efficiency. Integration with IoT, AI, and smart city initiatives further drives adoption, as stakeholders seek scalable, flexible, and customizable solutions to enhance user experience and operational control. Access control software specifically commands 22% of the software segment by 2026, reflecting enterprise demand for integrated security and access management capabilities.

Deployment Insights

On-premises hold over 46% market share in 2026 with a value exceeding US$ 3.3 Bn due to organizations prioritizing direct control over their data and system security. Many require highly customized systems that integrate with existing infrastructure, which on-premises deployments facilitate. Critical operations like real-time parking guidance, access control, and revenue management benefit from low-latency, reliable on-site systems. These needs make on-premises solutions the preferred choice for ensuring operational efficiency and compliance with local regulations.

Cloud-based deployments are expected to grow at the highest rate, with a CAGR of 18.1% as they address the need for real-time data access and remote management across multiple parking locations. They reduce infrastructure costs and simplify system updates, enabling municipalities and operators to scale operations quickly. Cloud solutions support advanced analytics, IoT integration, and mobile-based payment options, fulfilling the growing demand for seamless, user-friendly parking experiences.

Location Insights

Off-street parking commands the largest market share at over 60% in 2026 with a value exceeding US$ 4.3 Bn, due to the growing need for organized, secure, and efficient parking in urban areas where space is limited. Businesses, malls, airports, and commercial complexes prioritize off-street solutions to reduce congestion, ensure safety, and improve vehicle flow. These facilities benefit from advanced management systems, such as automated ticketing, guidance, and reservation features, which enhance user convenience and operational efficiency.

On-street parking is expected to grow at a CAGR of 18.7%, due to increasing urbanization and the rising number of vehicles in city centers, which intensifies parking scarcity. Cities are adopting smart parking solutions to reduce congestion, optimize limited space, and improve traffic flow. Real-time guidance, digital payments, and monitoring systems meet the growing need for convenience and efficiency for both drivers and municipalities. Regulatory pressures and the push for sustainable urban mobility further drive investments in on-street parking management.

End-user Insights

Municipal & government maintain a dominant market position with over 30% market share in 2026 and value exceeding US$ 2.2 Bn as they are primarily responsible for urban planning, traffic regulation, and public infrastructure management. The growing need to reduce traffic congestion, optimize parking space utilization, and implement smart city initiatives drives their adoption of advanced parking solutions. Government mandates for digitalization and cashless parking systems further boost investments in automated and IoT-enabled parking management.

Residential is expected to grow at significant rates, driven by increasing demand for organized and secure parking in urban housing complexes and gated communities. With rising vehicle ownership and limited parking space in residential areas, residents need smart solutions for efficient space utilization. Automated systems, real-time monitoring, and reservation features are becoming essential to reduce congestion and enhance convenience. The growing adoption of IoT-based and app-integrated solutions supports faster deployment in residential settings, driving market growth.

Regional Insights

North America Parking Management System Market Trends

North America maintains market leadership with over 36% share in 2026, reaching US$ 2.6 Bn value, with the U.S. market alone crossing US$ 1.9 Bn by 2026. The region demonstrates mature market characteristics with established technology adoption patterns, regulatory frameworks supporting smart city investments, and well-developed vendor ecosystems. The regulatory environment is particularly supportive, with federal funding mechanisms including the USDOT Smart City Challenge and infrastructure investment programs providing implementation capital. North American organizations prioritize cloud-based and SaaS-model solutions, with this deployment category representing over 42% of regional spending by 2026.

Asia Pacific Parking Management System Market Trends

Asia-Pacific emerges as the highest-growth region with 17.8% projected CAGR through 2033, driven by exceptional urbanization momentum in China, Japan, India, and Southeast Asia, combined with government initiatives prioritizing smart city infrastructure development. China represents the largest regional market value, driven by government smart city initiatives, explosive vehicle ownership growth, and concentrated urban development. Beijing, Shanghai, Shenzhen, and Chongqing have implemented advanced parking management systems, generating measurable traffic congestion reduction and municipal revenue enhancement. India represents an emerging major opportunity with the Smart City Mission targeting 100 cities for modernization. Indian cities including Bangalore, Mumbai, Delhi, and Hyderabad are initiating parking management system implementations, though market development remains early-stage relative to China.

Europe Parking Management System Market Trends

Europe is expected to hold more than 28% share by 2033 with value exceeding US$ 2.0 Bn, driven by strong regulatory support for sustainable urban mobility, stringent data protection requirements, and fragmented national implementation standards. European Union directives, including the Intelligent Transport Systems (ITS) Directive and Smart Cities and Communities Initiative, establish mandatory implementation requirements, creating structural demand for parking management systems. Germany leads European adoption with 8-9 major cities implementing comprehensive systems; the UK market features regulatory support through Department for Transport initiatives; France emphasizes parking as a mobility management tool; Spain prioritizes smart city development in major urban centers.

Competitive Landscape

The parking management system market is largely fragmented, with numerous global and regional players competing across hardware, software, and service segments. Companies are focusing on differentiation through the integration of advanced technologies, including IoT, AI-based analytics, and smart payment solutions, to stand out. Forming strategic partnerships and collaborating with municipalities and private parking operators helps expand market reach. Companies focus on customized solutions, competitive pricing, and after-sales support to enhance customer retention and gain a competitive edge.

Key Industry Developments

- In December 2025, Space Genius unveiled its redesigned User Interface Demo for its parking management software, offering a faster, more intuitive reservation experience for customers. The update features streamlined navigation, enhanced facility visuals, custom color management, travel time indicators, and a new cruise reservation widget, helping operators boost brand engagement and customer satisfaction.

- In March 2025, HUB Parking Technology launched its Digital Portfolio, an enterprise-level suite of applications built on the JMS Management System to modernize parking management. The platform enables ticketless, sustainable, and seamlessly integrated parking solutions across urban, commercial, residential, airport, and event environments, addressing evolving smart parking demands.

- In February 2025, ParkHub acquired ElimiWait, a specialized platform for valet parking operations. The acquisition strengthens ParkHub’s market position by integrating advanced valet management capabilities into its comprehensive parking solutions portfolio.

Companies Covered in Parking Management System Market

- IBM Corporation

- Siemens AG

- Bosch Group

- Amano Corporation

- SKIDATA GmbH

- SWARCO AG

- Kapsch TrafficCom

- T2 Systems, Inc.

- Atos SE

- SAP SE

- FlashParking Inc.

- ParkMobile LLC

- Others

Frequently Asked Questions

The global parking management system market is projected to be valued at US$7.2 Bn in 2026.

The need to reduce urban congestion and optimize limited parking space through real-time monitoring, automation, and data-driven decision-making is a key driver of the market.

The parking management system market is expected to witness a CAGR of 13.4% from 2026 to 2033.

Growing adoption of smart city initiatives, AI-enabled analytics, and cloud-based parking platforms is creating strong growth opportunities.

IBM Corporation, Siemens AG, Bosch Group, Amano Corporation, SKIDATA GmbH, SWARCO AG are among the leading key players.