- Industrial Machinery

- Industrial Dryers Market

Industrial Dryers Market Size, Share, and Growth Forecast, 2025 - 2032

Industrial Dryers Market By Technology (Spray Dryers, Freeze Dryers), End-user (Food & Beverage, Pharmaceuticals & Fine Chemicals), Mode of Operation, and Regional Analysis for 2025 - 2032

Industrial Dryers Market Size and Trends Analysis

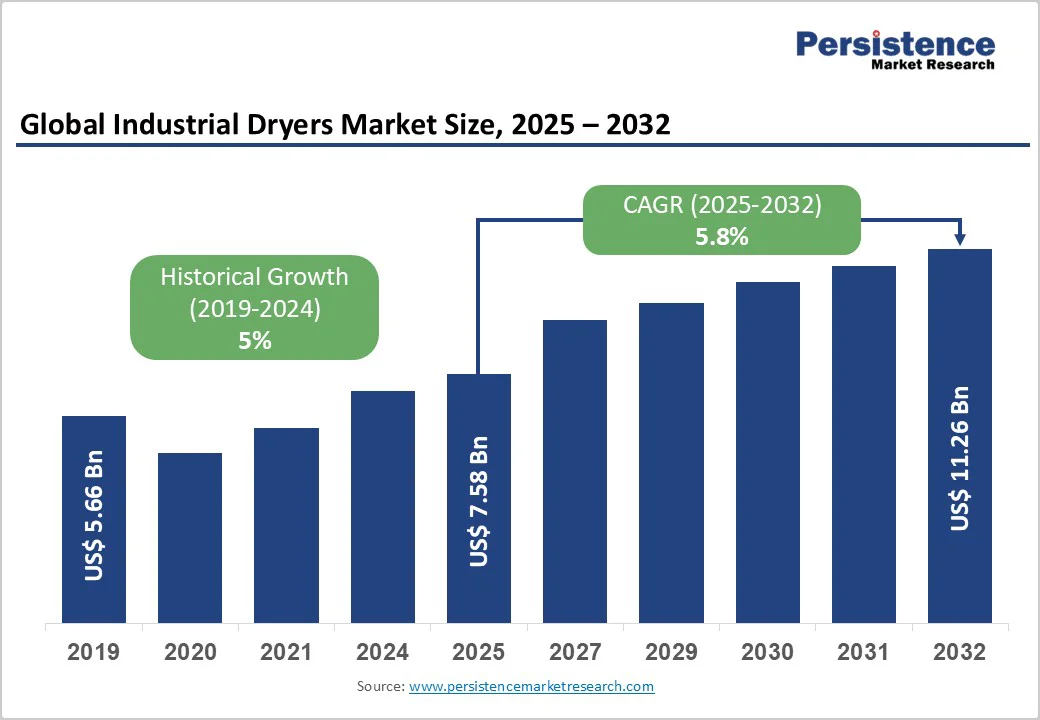

The global industrial dryers market size is likely to be valued at US$7.58 Billion in 2025 and is projected to reach US$11.26 Billion by 2032, growing at a CAGR of 5.8% between 2025 and 2032, driven by the rapid expansion of the food processing and pharmaceutical industries, rising demand for energy-efficient equipment due to stricter environmental regulations, and increasing adoption of automation and digital controls in manufacturing.

The market outlook remains positive, supported by steady growth in mature economies and accelerated capacity expansion in Asia Pacific and emerging markets.

Key Industry Highlights

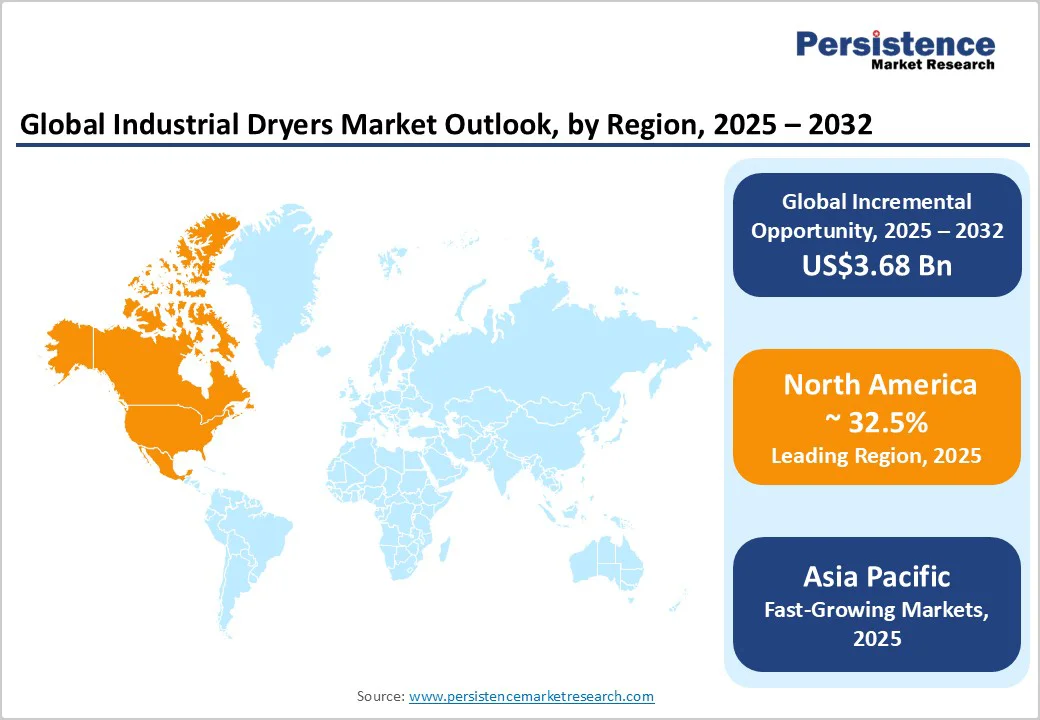

- Leading Region: North America accounts for 32.5% of the global revenue in 2025, driven by strong demand from the pharmaceutical, food, and specialty chemical industries, supported by the FDA and EPA efficiency regulations.

- Fastest-Growing Region: Asia Pacific, projected to grow at a CAGR of 8.5% between 2025 and 2032, led by China, India, and Japan due to large-scale industrial expansion and rising packaged food demand.

- Investment Plans: Significant investments are directed toward energy-efficient and digitalized dryers, with leading OEMs expanding service centers and local assembly hubs in Asia Pacific to capture the rising demand.

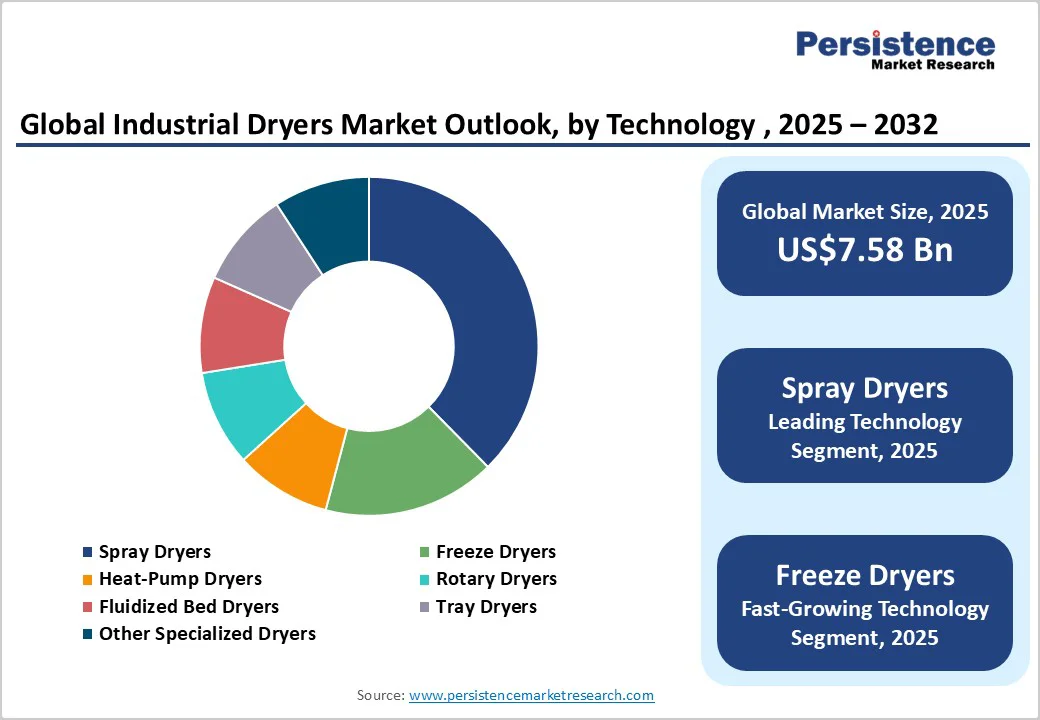

- Dominant Technology: Spray dryers hold 41% share of the global market in 2025, making them the backbone of food and pharma drying operations.

- Leading End-user: The food & beverage segment represents 33% of global market share in 2025, supported by strong demand for powdered milk, baby food, instant coffee, and packaged ingredients.

| Key Insights | Details |

|---|---|

| Industrial Dryers Market Size (2025E) | US$7.58 Bn |

| Market Value Forecast (2032F) | US$11.26 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand from the Food and Pharmaceutical Industries and Regulatory Compliance

Food and beverage processing accounts for more than one-third of total demand, making it the largest consumer of industrial dryers. Powdered dairy products, coffee, instant mixes, and nutraceuticals rely heavily on spray and belt dryers. Pharmaceutical companies are also investing in advanced drying technologies for active ingredients and excipients, particularly under stringent quality and hygiene standards.

These industries are expected to remain long-term growth pillars, ensuring a steady pipeline of new installations and replacements.

Industrial dryers are among the most energy-intensive pieces of equipment in a plant. Governments across North America, Europe, and Asia are tightening energy consumption and emissions rules. As a result, companies are prioritizing dryers that reduce energy use per kilogram of output through heat recovery systems, insulation upgrades, or hybrid heating sources.

Regulatory incentives and the push toward net-zero targets are turning efficiency into a procurement requirement.

Manufacturers are rapidly adopting Industry 4.0 practices. Industrial dryers now incorporate advanced sensors, real-time monitoring, and predictive maintenance systems. These upgrades reduce wastage, improve product uniformity, and extend machine life.

Automation has also reduced the need for manual oversight, cutting labor costs. The trend is especially strong in pharmaceuticals, where quality consistency is critical, and in food processing, where downtime directly impacts throughput.

High Capital Investments, Long Payback Periods, and Supply Chain Disruptions

Advanced dryers, such as spray, vacuum, or freeze dryers, come with high upfront costs. For many mid-sized processors, the investment burden is significant, particularly in regions with tight credit access. While efficiency improvements reduce operating costs, the initial outlay and uncertain demand outlook in some sectors extend payback timelines. This deters some companies from immediate adoption.

Dryers require specialized components such as heat exchangers, seals, and control systems. Global supply chain bottlenecks and rising raw material costs have increased equipment lead times and procurement risks. For capital projects that depend on strict commissioning schedules, delays in delivery can raise total costs and cause production setbacks.

Opportunities in the Retrofit and Energy Upgrade Market and Expansion in Emerging Markets

A large base of existing dryers offers an opportunity for retrofits and upgrades. Adding heat recovery systems, control packages, or better insulation allows customers to improve performance without full equipment replacement. Retrofits often have shorter payback periods and are particularly attractive in regions with high energy prices. This segment is expected to generate substantial aftermarket revenue.

Asia Pacific, Latin America, and parts of Africa are witnessing the rapid expansion of food processing, chemical manufacturing, and pharmaceutical facilities. New greenfield projects and industrial modernization programs are creating opportunities for original equipment manufacturers (OEMs). Localized manufacturing and distribution networks can help global players tap into this growth while reducing costs.

Freeze-drying and vacuum drying are expanding in niche but high-value applications such as biologics, specialty chemicals, and nutraceuticals. These processes require precise temperature control to preserve sensitive compounds. Although smaller in size compared to mainstream food and chemical segments, these specialized markets are growing at faster rates and offer higher margins.

Category-wise Analysis

Technology Insights

Spray dryers account for the largest share of 41% in the industrial dryers market, supported by their versatility in transforming liquid and slurry-based inputs into uniform, free-flowing powders. They are widely deployed in food processing for milk powder, instant coffee, and flavors, as well as in pharmaceutical formulations where precise particle size distribution is critical.

Their ability to deliver consistent output at high volumes makes them indispensable in industries operating on strict quality and safety standards. With established infrastructure across developed markets, spray dryers remain the most cost-effective solution for bulk drying applications.

Freeze-dryers are emerging as a vital technology for biologics, vaccines, nutraceuticals, and high-value chemicals, where preserving molecular integrity is paramount. Growth is further driven by the expansion of personalized medicine and the rising demand for probiotic supplements.

Heat-pump dryers, meanwhile, are gaining traction in textiles, food, and specialty chemicals because of their ability to lower energy consumption by up to 40% compared with conventional dryers. Both technologies, while currently smaller in installed base, are projected to expand at double the industry CAGR between 2025 and 2032, supported by sustainability initiatives and demand for high-value products.

End-user Insights

The food and beverage sector accounts for nearly 33% of total industrial dryer demand, reflecting its role in processing staples such as powdered milk, baby food, coffee, tea, and snack ingredients. The expansion of convenience food consumption, combined with growing exports of packaged products, continues to sustain this leadership.

In emerging markets, rising disposable incomes are increasing reliance on packaged food, which in turn drives investments in large-scale drying plants. With consumer focus on shelf stability and flavor retention, food producers prefer dryers that maintain nutritional integrity while ensuring operational efficiency.

Pharmaceuticals and fine chemicals are forecast to grow at the fastest pace, propelled by rising biologics production and heat-sensitive APIs (active pharmaceutical ingredients). Freeze-drying has become essential in vaccine manufacturing, supported by national health initiatives and global funding for pandemic preparedness.

Regulatory agencies such as the U.S. FDA and EMA enforce strict validation and monitoring standards, pushing pharmaceutical manufacturers to adopt high-specification dryers with automation and integrated monitoring systems. The fine chemicals segment benefits from precision drying needs in pigments, catalysts, and specialty intermediates, ensuring this category outpaces food in terms of CAGR over 2025 - 2032.

Mode of Operation Insights

Continuous dryers remain the backbone of food, chemical, and fertilizer plants, enabling uninterrupted high-volume production. Their design minimizes labor requirements and ensures steady throughput, aligning with large-scale manufacturing environments. In markets, including North America and Europe, where operational efficiency and labor costs are critical, continuous dryers represent the most cost-effective drying solution.

Their integration into automated lines further boosts their appeal, allowing producers to maintain consistent output quality and reduce downtime. This segment’s dominance reflects industries’ reliance on high-capacity solutions to meet global demand.

Pre-engineered, modular skid-based dryers are increasingly popular in emerging economies and mid-scale plants seeking cost-effective, quick-deployment solutions. These systems minimize installation time and project risk, making them attractive to firms expanding in fast-growing sectors such as nutraceuticals, specialty chemicals, and dairy powders.

Their portability and scalability allow manufacturers to add capacity incrementally, avoiding large upfront capital investments. With rising demand in Asia Pacific and Latin America, modular dryers are projected to expand at the highest CAGR among operation modes, supported by flexible financing models and interest from SMEs entering global supply chains.

Regional Insights

North America Industrial Dryers Market Trends - Regulatory Demand and OEM Strength Drive U.S. and Canada Growth

North America accounts for 32.5% of the global industrial dryers market, led by the United States, which accounts for more than half of regional sales. Growth is primarily driven by the expansion of pharmaceutical manufacturing, food processing, and specialty chemicals, all of which require high-specification dryers.

Regulatory oversight from the FDA and EPA mandates energy-efficient, validated equipment, creating steady demand for advanced systems. The market benefits from a mature ecosystem of OEMs and service providers, with companies such as GEA Group, Carrier Vibrating Equipment, and FLSmidth actively competing.

Competitive dynamics are defined by high after-sales service penetration and a growing market for leasing and financing models, enabling mid-sized firms to access premium technologies. Investment trends include acquisitions of niche technology startups in freeze-drying and partnerships focused on integrating IoT-based monitoring systems. With R&D spending in biologics and food innovation expanding, the U.S. continues to lead regional growth, while Canada is emerging as a hub for dairy-based drying operations, particularly in whey and milk powders.

Europe Industrial Dryers Market Trends - Sustainability Push and Modernization Sustain EU Market Momentum

Europe is a technologically mature market, anchored by countries such as Germany, France, and the U.K., which account for the bulk of installations. Demand stems largely from dairy processing, specialty chemicals, and pharmaceuticals, supported by strong regulatory frameworks.

The EU Green Deal and stricter energy-efficiency targets are accelerating the replacement of conventional dryers with more sustainable models, including heat-pump dryers and retrofitted continuous systems. Germany leads with robust exports of engineering solutions, while France maintains a strong food-processing base.

Competition is shaped by global OEMs such as GEA, ANDRITZ, and Bühler, which dominate the regional landscape with advanced, patented technologies. Public and private funding mechanisms encourage companies to modernize their equipment in line with carbon-reduction goals, with programs emphasizing retrofitting and digital integration.

Spain and Eastern European countries are experiencing rising installations due to dairy exports and chemical production capacity. Europe maintains steady growth, though its expansion rate is slower compared with Asia Pacific, reflecting a focus on upgrading rather than new installations.

Asia Pacific Industrial Dryers Market Trends - Industrial Expansion and Policy Support Fuel APAC Growth

Asia Pacific is the fastest-growing regional market, projected to outpace all others between 2025 and 2032. China, India, and Japan lead demand, supported by rapid industrial expansion in food, pharmaceuticals, and chemicals.

Government initiatives such as “Made in China 2025” and India’s PLI schemes for pharmaceuticals encourage local production and capital investments in advanced processing technologies. Rising disposable incomes are driving packaged food consumption, while vaccine and biologics production is boosting the adoption of freeze-drying systems.

The region benefits from cost-competitive labor and rising domestic demand, leading to high volumes of new installations rather than retrofits. Japan maintains strict quality and safety standards, ensuring strong uptake of premium dryers, while India and Southeast Asia prioritize capacity expansion at competitive price points.

Global OEMs are increasingly setting up local assembly, service, and R&D centers to reduce lead times and tap into this demand. The combination of strong local consumption, export opportunities, and industrial policy support makes Asia Pacific the primary growth driver for the global industrial dryers market.

Competitive Landscape

The global industrial dryers market is moderately concentrated, dominated by multinational firms such as GEA Group, ANDRITZ, Bühler, and SPX FLOW, which lead premium sectors such as pharmaceuticals, dairy, and specialty chemicals through strong R&D and global service networks. Mid-sized and regional players compete in cost-sensitive rotary and fluidized bed dryer segments, emphasizing price and delivery speed.

The top 8-10 firms control about half of global revenue, with the rest fragmented. Competition centers on energy efficiency, digital integration, and lifecycle services, while key strategies include expanding in Asia Pacific and developing performance-based, energy-efficient service models.

Key Industry Developments

- In January 2024, ANDRITZ acquired a European freeze-drying specialist to expand its portfolio in pharmaceuticals, biologics, and premium food drying applications. This acquisition strengthens its high-value segment positioning and responds to rising demand for freeze-dried biologics and nutraceuticals.

- In September 2023, GEA entered into a regional partnership with a leading process equipment supplier in Asia Pacific to scale spray-drying and continuous dryer delivery capabilities. The collaboration focuses on China, India, and Southeast Asia, where demand is growing for high-throughput food and chemical processing equipment.

- In April 2024, Bühler and GEA introduced energy-efficient continuous dryers equipped with advanced heat recovery and digital monitoring platforms. These products target European and North American markets, aligning with new EU Green Deal energy mandates and U.S. EPA efficiency regulations.

Companies Covered in Industrial Dryers Market

- GEA Group

- ANDRITZ AG

- Bühler Group

- SPX FLOW Inc.

- Hosokawa Micron Corporation

- Tetra Pak (Processing Division)

- Bucher Industries

- Coperion (ThyssenKrupp)

- ALQUA Inc.

- Carrier Vibrating Equipment

- Yamato Scale

- Godfrey & Wing

- Wuxi Modern Spray Drying Equipment Co., Ltd.

- FLSmidth

- SiccaDania

- Delta Industrial Services

- Niro Atomizer

- Pulcra Chemicals

- Marubishi Engineering

- Lödige Industries

Frequently Asked Questions

The industrial dryers market size is US$7.58 Billion in 2025.

The industrial dryers market is projected to reach US$11.26 Billion by 2032.

The key trends are the rising adoption of energy-efficient, digitally enabled dryers and the growth of freeze-drying for pharmaceuticals and biologics.

By technology, spray dryers are the leading segment, holding 41% of the global market in 2025. By end-use industry, food & beverage leads with 33% share.

The industrial dryers market is expected to grow at a CAGR of 5.8% between 2025 and 2032.

The key players in the industrial dryers market include GEA Group, ANDRITZ AG, Bühler Group, SPX FLOW Inc., and Hosokawa Micron Corporation.