- Executive Summary

- Global Smart Watch Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Consumer Spending Power

- Technology Adoption Growth

- Smartphone Penetration Expansion

- Healthcare Cost Pressure

- Internet Connectivity Expansion

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Smart Watch Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Smart Watch Market Outlook: Watch Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Watch Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Watch Type, 2026-2033

- Standalone Smart Watches

- Extension Smart Watches

- Hybrid Smart Watches

- Market Attractiveness Analysis: Watch Type

- Global Smart Watch Market Outlook: Price Range

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Price Range, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Price Range, 2026-2033

- Medium Priced

- Low Priced

- High Priced

- Market Attractiveness Analysis: Price Range

- Global Smart Watch Market Outlook: Operating System

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Operating System, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Operating System, 2026-2033

- Watch OS (iOS)

- Android

- Linux

- Pebble OS

- RTOS

- Tizen

- Market Attractiveness Analysis: Operating System

- Global Smart Watch Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Smart Watch Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Watch Type, 2026-2033

- Standalone Smart Watches

- Extension Smart Watches

- Hybrid Smart Watches

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Price Range, 2026-2033

- Medium Priced

- Low Priced

- High Priced

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Operating System, 2026-2033

- Watch OS (iOS)

- Android

- Linux

- Pebble OS

- RTOS

- Tizen

- Europe Smart Watch Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Watch Type, 2026-2033

- Standalone Smart Watches

- Extension Smart Watches

- Hybrid Smart Watches

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Price Range, 2026-2033

- Medium Priced

- Low Priced

- High Priced

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Operating System, 2026-2033

- Watch OS (iOS)

- Android

- Linux

- Pebble OS

- RTOS

- Tizen

- East Asia Smart Watch Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Watch Type, 2026-2033

- Standalone Smart Watches

- Extension Smart Watches

- Hybrid Smart Watches

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Price Range, 2026-2033

- Medium Priced

- Low Priced

- High Priced

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Operating System, 2026-2033

- Watch OS (iOS)

- Android

- Linux

- Pebble OS

- RTOS

- Tizen

- South Asia & Oceania Smart Watch Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Watch Type, 2026-2033

- Standalone Smart Watches

- Extension Smart Watches

- Hybrid Smart Watches

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Price Range, 2026-2033

- Medium Priced

- Low Priced

- High Priced

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Operating System, 2026-2033

- Watch OS (iOS)

- Android

- Linux

- Pebble OS

- RTOS

- Tizen

- Latin America Smart Watch Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Watch Type, 2026-2033

- Standalone Smart Watches

- Extension Smart Watches

- Hybrid Smart Watches

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Price Range, 2026-2033

- Medium Priced

- Low Priced

- High Priced

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Operating System, 2026-2033

- Watch OS (iOS)

- Android

- Linux

- Pebble OS

- RTOS

- Tizen

- Middle East & Africa Smart Watch Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Watch Type, 2026-2033

- Standalone Smart Watches

- Extension Smart Watches

- Hybrid Smart Watches

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Price Range, 2026-2033

- Medium Priced

- Low Priced

- High Priced

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Operating System, 2026-2033

- Watch OS (iOS)

- Android

- Linux

- Pebble OS

- RTOS

- Tizen

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Apple

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Fitbit Inc.

- Samsung Electronics Co., Ltd

- Sony Corporation

- Garmin Ltd.

- Fossil Group, Inc.

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Nokia Corporation (Withings)

- LG Electronics Inc.

- Apple

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Clothing, Footwear, & Accessories

- Smartwatch Market

Smartwatch Market Size, Share, and Growth Forecast, 2026 - 2033

Smartwatch Market by Watch Type (Standalone Smartwatches, Extension Smartwatches, and Hybrid Smartwatches), By Operating System (Watch OS (iOS), Android, Linux, Pebble OS, RTOS, and Tizen), By Price Range (Medium Priced, Low Priced, and High Priced) and Regional Analysis for 2026 - 2033

Smartwatch Market Size and Trends Analysis

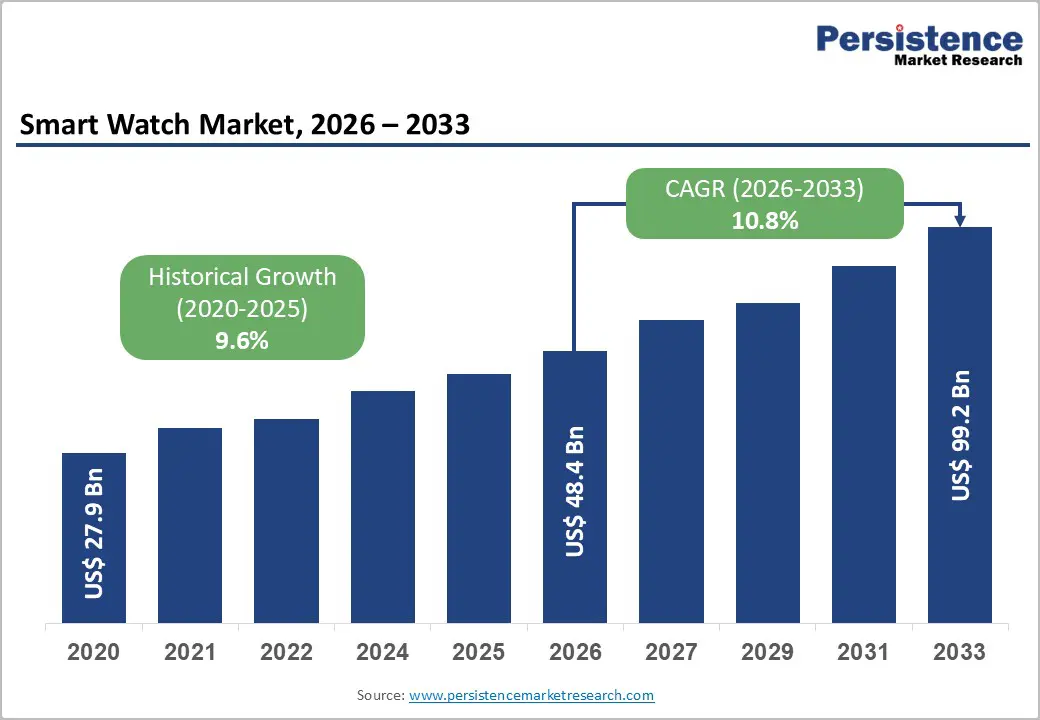

The global smartwatch market size was valued at US$ 48.4 billion in 2026 and is projected to reach US$ 99.2 billion by 2033, growing at a CAGR of 10.8% between 2026 and 2033. The market nearly doubled from 2020 to 2026 supported by rapid consumer adoption of wrist-worn wearables for health tracking, notifications, and connectivity.

Smartwatches accounted for around 46% of the broader wearable tech sector in 2024, underlining their central role within the category. Growth is reinforced by rising global health awareness, persistent physical inactivity risks, and the evolution of smartwatches toward regulated medical-grade functions.

Key Industry-Highlights:

- Preventive Health Demand: Rising preventive healthcare awareness drives smartwatch adoption. WHO reports 31% global adult inactivity in 2022 (1.8 billion people), with over 65% of smartwatch buyers citing health monitoring as their primary purchase motivation.

- Global smartwatch shipments recorded 4% year-on-year growth in 2025, indicating a gradual recovery in the wearable devices market driven by improving consumer demand and expanding adoption of health-tracking smart devices.

- Medical Feature Validation: Regulatory approvals strengthen the credibility of smartwatches. Apple and Samsung received U.S. FDA clearance for ECG monitoring, enabling atrial fibrillation detection and expanding smartwatch use in regulated digital health and remote patient-monitoring ecosystems.

- Market Saturation Pressure: Mature markets show slowing growth. Global smartwatch shipments declined nearly 7% in 2024, while Apple shipments fell 19% year-on-year and market share dropped from 25% to 22%.

- Regulatory Compliance Burden: Medical-grade features require strict compliance with frameworks such as the EU MDR and FDA regulations, increasing development costs, extending time-to-market, and strengthening the competitive advantage of well-capitalized global manufacturers.

- Remote Health Opportunity: WHO estimates nearly 500 million people could develop chronic diseases by 2030, creating demand for remote patient-monitoring programs using smartwatches to track cardiac rhythm, activity, and sleep in real time.

- AI Ecosystem Monetization: Smartwatch platforms are shifting toward AI-driven services and subscriptions. With average selling prices around US$259 in 2023, vendors increasingly monetize through apps, cloud analytics, and personalized digital-health insights.

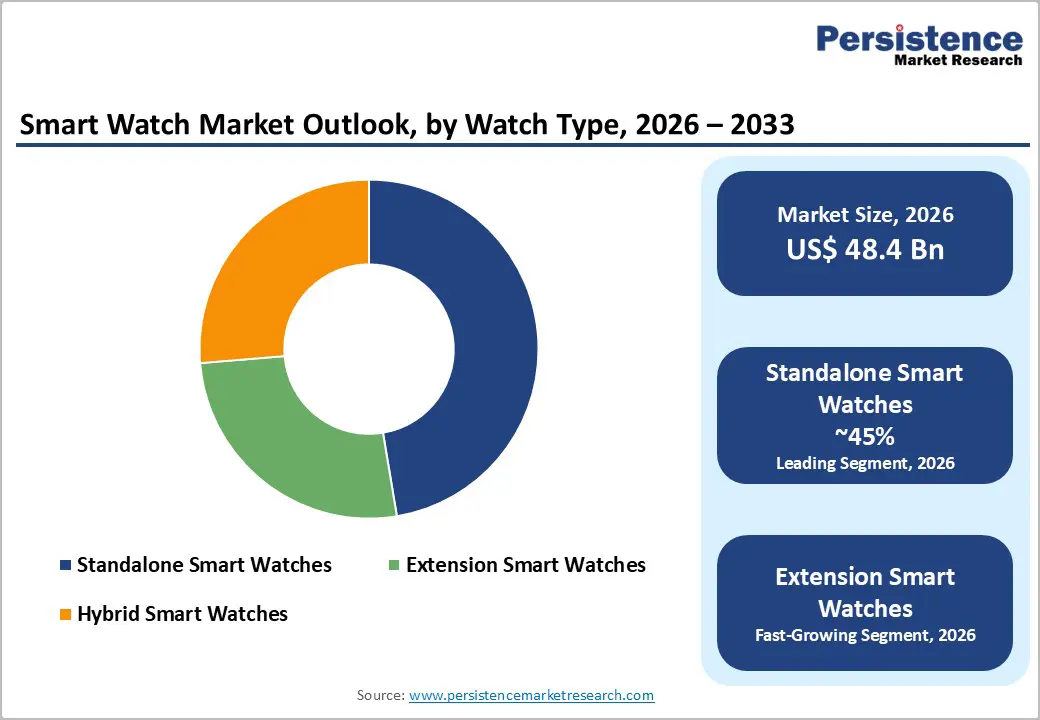

- Standalone Watch Leadership: Standalone smartwatches lead the product segment, capturing over 45% revenue share in 2026 due to LTE connectivity, independent functionality, and premium pricing across major brands like Apple and Samsung.

- Android Platform Growth: WatchOS held over 30.1% revenue share in 2026, but Android-based systems, including Wear OS, are expanding fastest, projected to grow at about 11.5% CAGR between 2026 and 2033.

- Mid-Price Segment Dominance: Smartwatches priced between US$120-180 accounted for over 40.2% of global revenue in 2026, offering balanced affordability and features such as AMOLED displays, GPS tracking, and advanced health monitoring.

- Asia Pacific Expansion: Asia Pacific drives global smartwatch shipments, accounting for nearly 39-40% in 2025 and projected to grow at a 19-20% CAGR through 2030, supported by strong Chinese and Indian consumer demand.

| Key Insights | Details |

|---|---|

| Smartwatch Market Size (2026E) | US$ 48.4 Bn |

| Market Value Forecast (2033F) | US$ 99.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.6% |

Market Dynamics

Drivers - Rising health risks and preventive wellness focus

The smartwatch market is strongly underpinned by the global shift toward proactive health management and digital wellness. The World Health Organization estimates that 31% of adults worldwide, around 1.8 billion people, were physically inactive in 2022, with inactivity projected to reach 35% by 2030 if trends continue. Physical inactivity is associated with higher risks of cardiovascular disease, diabetes and certain cancers, creating strong policy and consumer incentives for tools that nudge behavior change. Smartwatches provide continuous monitoring of steps, heart rate, sleep and other vital metrics, with over 65% of users citing health and fitness tracking as the primary purchase reason in 2023. This positions smartwatches as a scalable, relatively low-cost mechanism for improving population health, supporting sustained device adoption across age and income groups.

Preventive health pressures institutionalize smartwatch health monitoring

Regulators have progressively cleared smartwatch-based diagnostic and monitoring functions, effectively elevating selected models to the status of regulated medical devices. Apple’s smartwatch ECG function received FDA de novo clearance as a Class II medical device, enabling detection of atrial fibrillation and secure sharing of rhythm traces with clinicians. Similarly, Samsung’s ECG monitoring app for Galaxy Watch obtained U.S. FDA clearance, while comparable capabilities are rolling out across other markets, subject to country-specific approvals.

In Europe, the EU Medical Device Regulation (MDR 2017/745) applies when wearables claim diagnostic or therapeutic intent, requiring clinical evidence, risk management and CE marking, but also providing a clear pathway for reimbursement-eligible medical wearables. These regulatory developments validate smartwatches as legitimate tools within digital health pathways, encouraging payers, providers, and employers to integrate them into remote patient monitoring, chronic-disease management, and corporate wellness programmes, thereby expanding addressable revenue pools beyond consumer electronics.

Restraint - Short upgrade cycles, market saturation, and demand cyclicality

Leading markets such as North America and Western Europe are reaching high smartwatch penetration, triggering slower replacement-driven growth and exposure to macro cycles. Global smartwatch shipments declined by around 7% in 2024, with Apple - still the leading vendor - seeing shipments fall 19% year-on-year and share slipping from 25% to 22%. Shipments of wearable devices overall have fluctuated, with IDC reporting low single-digit growth and quarters of decline as post-pandemic demand normalised and channel inventories remained elevated. These dynamics constrain volume growth and intensify price competition in mid and entry tiers, compressing margins and raising the threshold for R&D ROI.

Regulatory compliance, data privacy, and clinical risk exposure

Once health-monitoring features make medical claims, smartwatches must comply with demanding regulatory frameworks such as the EU MDR, U.S. FDA medical-device regulations and national data-protection laws. Manufacturers must perform risk analysis, clinical evaluation, extensive technical documentation, and implement certified quality systems, materially increasing time-to-market and compliance costs. Furthermore, misclassification risk, false positives or negatives in ECG or arrhythmia detection, and data-security breaches can trigger litigation, recalls, or reputational damage. Smaller OEMs and new entrants may struggle to absorb these fixed costs, limiting innovation in regulated features and reinforcing the advantage of large, well-capitalized incumbents.

Opportunities - Expansion of remote patient monitoring and reimbursed digital health

WHO projects that without stronger physical-activity policies, nearly 500 million people could develop cardiovascular disease, obesity, diabetes or other NCDs between 2020 and 2030, at an estimated public-health cost of US$ 27 billion annually.

Health systems and payers are therefore scaling remote patient monitoring (RPM) programmes that use connected wearables to track cardiac rhythm, activity and sleep in real time. In North America and parts of Europe, RPM programmes and FDA-cleared smartwatch functions are already linked to reimbursement codes, enabling device-plus-service models spanning hardware, cloud analytics and clinician dashboards. Given the current smartwatch market size projections, even modest penetration into reimbursed chronic-disease cohorts represents a multi-billion-dollar incremental revenue pool, particularly for vendors able to partner with hospitals, insurers, and telehealth platforms.

Software, AI, and ecosystem monetization beyond hardware margins

Smartwatch hardware ASPs averaged around US$ 259 in 2023, with expectations of gradual increases as vendors introduce premium models with advanced health, battery, and durability features. At the same time, platforms such as watchOS and Wear OS are deepening integration with app stores, cloud services, and AI-driven personalisation, making software experiences - rather than pure hardware specs - the primary differentiators.

On-device AI chips and algorithms, showcased by players such as Zepp Health and leading APAC vendors, enable continuous, low-power analytics of heart rhythm, stress, and sleep stages, unlocking subscription revenue for coaching and insights. This shift creates opportunities to expand average revenue per user via paid apps, premium health features, and cross-device bundles with smartphones, headphones, and connected fitness equipment, reinforcing ecosystem lock-in.

Category-wise Analysis

Product Type Insights

The global smartwatch market shows distinct performance trends across watch types, with standalone smartwatches dominating revenue share while extension smartwatches record the fastest growth. In 2026, standalone smartwatches accounted for more than 45% of total market revenue, reflecting strong consumer demand for devices equipped with integrated cellular connectivity. These smartwatches operate independently of smartphones and support functions such as voice calls, messaging, music streaming, and emergency communication directly from the wrist. Their popularity is particularly strong among users engaged in outdoor sports, safety monitoring, and parental tracking applications. Major technology brands, including Apple, Samsung, and several Chinese OEMs have introduced LTE- and eSIM-enabled models, which typically command higher average selling prices (ASPs), further strengthening their revenue dominance.

Extension smartwatches are projected to be the fastest-growing segment, with a CAGR of 11.3% between 2026 and 2033. These devices rely on smartphone connectivity but provide essential features such as notifications, fitness tracking, and application support at relatively affordable prices. Their cost-effectiveness makes them especially attractive in emerging markets and among first-time smartwatch buyers. In contrast, hybrid smartwatches combining traditional analog designs with digital health tracking remain a niche segment.

Operating System Insights

In the global smartwatch market, WatchOS (iOS) continues to lead in revenue share, accounting for more than 30.1% of total market revenue in 2026. This dominance is largely driven by Apple’s strong brand presence, premium pricing strategy, and seamless integration within the broader iOS ecosystem. Apple smartwatches benefit from high user loyalty, an extensive app ecosystem, and advanced health-monitoring features, such as FDA-cleared ECG capabilities, fall detection, and health-tracking tools, which reinforce their leadership in the premium smartwatch segment. Market research firms including Counterpoint consistently rank Apple as the largest smartwatch vendor globally in terms of revenue and profitability, even as shipment growth moderates in some regions. However, Android-based operating systems, including Google’s Wear OS and several proprietary platforms, are emerging as the fastest-growing segment, projected to expand at a CAGR of around 11.5% between 2026 and 2033.

Manufacturers such as Samsung, Xiaomi, Oppo, and OnePlus are accelerating adoption by launching feature-rich smartwatches in the mid-price segment. In regions such as the Asia Pacific, Android-powered platforms already dominate shipments due to competitive pricing and strong compatibility with Android smartphones, creating broader opportunities for developers and digital services.

Price Range Insights

In the global smartwatch market, the mid-priced segment accounts for the largest share of revenue, accounting for over 40.2% of global revenue in 2026. This segment generally falls within the US$120-180 price range, aligning with the broader trend in wearable device average selling price (ASP). Mid-range smartwatches provide an optimal balance between advanced features and affordability, making them highly attractive to mainstream consumers. Devices in this category typically include AMOLED displays, multi-day battery life, GPS tracking, and health monitoring features such as SpO2 sensors, offering strong functionality without premium pricing. As a result, they are widely adopted across both developed and emerging markets and are increasingly used in corporate wellness initiatives.

While premium smartwatches priced above US$400 offer high margins through advanced materials and specialized features, their sales volumes remain relatively limited. In contrast, low-priced smartwatches below US$100 are experiencing the fastest growth, projected to expand at a CAGR of approximately 11.6% from 2026 to 2033. This growth is largely driven by intense competition among Asian manufacturers and declining component costs, enabling wider consumer access to wearable technology.

Regional Insights and Trends

North America Smartwatch Market Trends

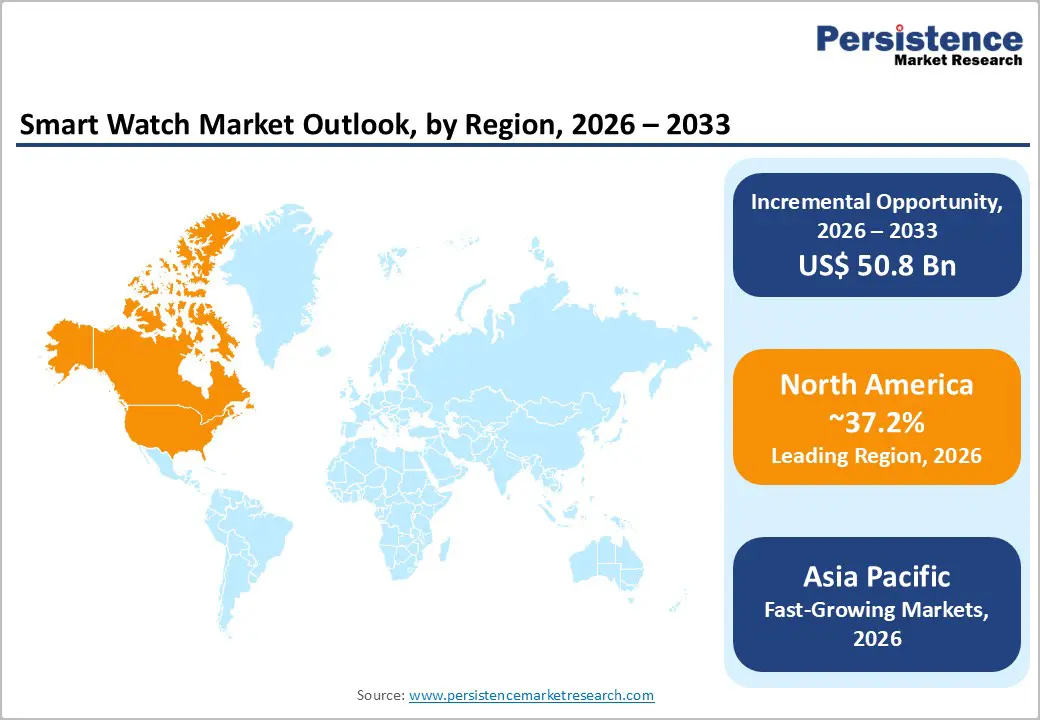

North America remains the largest regional market for smartwatches, accounting for nearly 45% of global revenue in 2022, and is expected to maintain its leadership position through 2030. The regional market generated approximately US$17 billion in revenue in 2022 and is projected to grow at a compound annual growth rate (CAGR) of around 8-9%, potentially surpassing US$32 billion by 2030. The United States represents the dominant share of regional demand, supported by high disposable income levels, widespread smartphone penetration, and strong adoption of connected fitness and digital health technologies.

Several structural factors continue to drive market expansion in the region. The widespread rollout of LTE and 5G networks enhances device connectivity, while employer-sponsored wellness programs and insurance initiatives that reward activity tracking encourage smartwatch adoption. North America also benefits from a strong technology and innovation ecosystem, led by companies such as Apple, Google (Fitbit), and Garmin, alongside numerous semiconductor and software developers advancing biosensing accuracy, artificial intelligence analytics, and battery performance.

Regulatory frameworks are well established, with the U.S. FDA approving multiple smartwatch ECG and arrhythmia-detection features, providing regulatory clarity while ensuring compliance and safety standards for health-focused wearable devices.

Asia Pacific Smartwatch Market Trends

Asia Pacific is emerging as the fastest-growing region in the global smartwatch market, driven by strong shipment volumes, competitive pricing, and rapid technology adoption. The region accounted for nearly 40% of global smartwatch shipments in 2025 and is projected to reach CAGR of around 20% through 2030. China remains the dominant market within the region, contributing roughly 39% of the regional share, supported by strong shipment growth of nearly 20-30% annually. This expansion is fueled by major domestic brands such as Huawei, Xiaomi, and OPPO, along with rising demand for children’s smartwatches.

India is another rapidly expanding market, expected to record CAGR exceeding 20%, driven by cost-competitive brands like Noise and boAt. Government initiatives such as production-linked incentives are also encouraging local manufacturing and reducing production costs. Meanwhile, ASEAN countries, Japan, and South Korea contribute additional demand, particularly for fitness, sports, and elder-care wearable applications. Strong electronics manufacturing ecosystems in China, Vietnam, and India enable efficient production and aggressive pricing strategies. As a result, Asia Pacific continues to strengthen its role as both a global smartwatch manufacturing hub and a major driver of wearable technology adoption.

Competitive Landscape

The global smartwatch market is moderately consolidated at the top, with Apple, Samsung, Huawei, Garmin, Google (Fitbit) and Xiaomi together accounting for a majority of shipments and an even higher share of revenues. Below these leaders, a fragmented long tail of brands - including Fossil, Amazfit (Zepp Health), Suunto, Withings, Mobvoi and numerous regional OEMs - compete on design, niche health features, price points and regional focus.

Market concentration is highest in North America, where a handful of U.S. and Korean brands dominate, while Asia Pacific exhibits more fragmented competition due to strong domestic challengers.

Key Industry Developments

- March 2026 - Qualcomm Introduces Snapdragon Wear Elite for AI-Powered Wearables: Qualcomm Technologies launched the Snapdragon Wear Elite platform, the first NPU-powered wearable chipset designed for personal AI devices, enabling on-device AI processing and supporting ecosystems such as WearOS, Android, and Linux.

- February 2026 - AsteroidOS 2.0 Revives Linux-Based Smartwatch Ecosystem: The developer community released AsteroidOS 2.0, an open-source Linux operating system for smartwatches that enhances customization, extends device lifecycles, and promotes a vendor-independent wearable technology ecosystem.

- November 2025 - Garmin Expands Manufacturing Footprint in Southeast Asia: Garmin announced plans to establish its first Southeast Asia manufacturing facility in Thailand to produce smartwatches and electronic wearables, strengthening regional supply chains and supporting growing global demand for wearable technology.

- In November 2025, Titan Launches Evoke 2.0 Smartwatch Line: Titan introduced its Evoke 2.0 premium smartwatch series, integrating advanced health-monitoring features with modern design, blending the brand’s analogue watchmaking heritage with smart technology to enhance personalized lifestyle functionality.

- In January 2024, Fire-Boltt expanded its wearable portfolio with the launch of the Android-based Dream Wristphone, featuring a compact and streamlined design that enhances functionality and redefines the wearable technology experience.

- In July 2023, Samsung Electronics Co., Ltd. launched the Galaxy Watch6 and Galaxy Watch6 Classic, offering advanced health monitoring capabilities, refined design features, and an improved mobile experience, marking a notable advancement in the smartwatch market.

Companies Covered in Smartwatch Market

- Fitbit Inc.

- Samsung Electronics Co., Ltd

- Sony Corporation

- Garmin Ltd.

- Fossil Group, Inc.

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Nokia Corporation (Withings)

- LG Electronics Inc.

- Other Market Players

Frequently Asked Questions

The Smartwatch market is estimated to be valued at US$ 48.4 Bn in 2026.

The key demand driver for the smartwatch market is the growing consumer focus on health and fitness monitoring. Increasing awareness of preventive healthcare has encouraged consumers to adopt wearable devices that track vital health metrics such as heart rate, blood oxygen levels (SpO₂), sleep patterns, physical activity, and stress levels.

In 2026, the North America region will dominate the market with an exceeding 37.2% revenue share in the global Smartwatch market.

Standalone Smartwatches dominate the product landscape, commanding over 45% of total market revenue in 2026, driven by their independent connectivity features such as built-in LTE, GPS, and Wi-Fi, enabling users to make calls, send messages, stream music, and access apps without relying on smartphones.

Key players operating in the Smartwatch market include Apple Inc., Fitbit Inc., Samsung Electronics Co., Ltd., Sony Corporation, Garmin Ltd., Fossil Group, Inc., Huawei Technologies Co., Ltd., and Xiaomi Corporation, which compete through innovation in health monitoring, connectivity features, design, and ecosystem integration.