- Executive Summary

- Global Recycled Plastic Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Automotive Industry Overview

- Global Regulatory Environment Overview

- Global Supply Chain Stability Overview

- Global Economic Growth and Industrial Expansion Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Recycled Plastic Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Recycled Plastic Market Outlook: By Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by By Product Type , 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type , 2026-2033

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polypropylene (PP)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Others

- Market Attractiveness Analysis: By Product Type

- Global Recycled Plastic Market Outlook: By Source

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by By Source, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by By Source, 2026-2033

- Bottles

- Films

- Foams

- Fibers

- Containers & Packaging

- Others

- Market Attractiveness Analysis: By Source

- Global Recycled Plastic Market Outlook: By Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by By Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Packaging

- Building & Construction

- Automotive

- Textiles

- Electrical & Electronics

- Furniture

- Industrial Use

- Others

- Market Attractiveness Analysis: By Application

- Global Recycled Plastic Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Recycled Plastic Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type , 2026-2033

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polypropylene (PP)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Others

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by By Source, 2026-2033

- Bottles

- Films

- Foams

- Fibers

- Containers & Packaging

- Others

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Packaging

- Building & Construction

- Automotive

- Textiles

- Electrical & Electronics

- Furniture

- Industrial Use

- Others

- Europe Recycled Plastic Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type , 2026-2033

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polypropylene (PP)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Others

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by By Source, 2026-2033

- Bottles

- Films

- Foams

- Fibers

- Containers & Packaging

- Others

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Packaging

- Building & Construction

- Automotive

- Textiles

- Electrical & Electronics

- Furniture

- Industrial Use

- Others

- East Asia Recycled Plastic Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type , 2026-2033

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polypropylene (PP)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Others

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by By Source, 2026-2033

- Bottles

- Films

- Foams

- Fibers

- Containers & Packaging

- Others

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Packaging

- Building & Construction

- Automotive

- Textiles

- Electrical & Electronics

- Furniture

- Industrial Use

- Others

- South Asia & Oceania Recycled Plastic Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type , 2026-2033

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polypropylene (PP)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by By Source, 2026-2033

- Bottles

- Films

- Foams

- Fibers

- Containers & Packaging

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Packaging

- Building & Construction

- Automotive

- Textiles

- Electrical & Electronics

- Furniture

- Industrial Use

- Others

- Latin America Recycled Plastic Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type , 2026-2033

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polypropylene (PP)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Others

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by By Source, 2026-2033

- Bottles

- Films

- Foams

- Fibers

- Containers & Packaging

- Others

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Packaging

- Building & Construction

- Automotive

- Textiles

- Electrical & Electronics

- Furniture

- Industrial Use

- Others

- Middle East & Africa Recycled Plastic Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type , 2026-2033

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polypropylene (PP)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by By Source, 2026-2033

- Bottles

- Films

- Foams

- Fibers

- Containers & Packaging

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Packaging

- Building & Construction

- Automotive

- Textiles

- Electrical & Electronics

- Furniture

- Industrial Use

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- CLEAN HARBORS, INC.

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Plastipak Holdings, Inc.

- Custom Polymers

- Waste Connections

- Shell International B.V.

- Fresh Pak Corp

- SUEZ worldwide

- KW Plastics.

- Republic Services

- REMONDIS SE & Co. KG

- Covestro AG

- Ultra-Poly Corporation.

- Veolia

- ReVital Polymers.

- WM Intellectual Property Holdings, L.L.C.

- CLEAN HARBORS, INC.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Plastics, Polymers & Resins

- Recycled Plastic Market

Recycled Plastic Market Size, Share, and Growth Forecast 2026 - 2033

Recycled Plastic Market by Product Type (Polyethylene Terephthalate (PET), High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), Polypropylene (PP), Polystyrene (PS), Polyvinyl Chloride (PVC), Others), By Source (Bottles, Films, Foams, Fibers, Containers & Packaging, Others), By Application (Packaging, Building & Construction, Automotive, Textiles, Electrical & Electronics, Furniture, Industrial Use, Others), and Regional for 2026 - 2033

Recycled Plastic Market Size and Trend Analysis

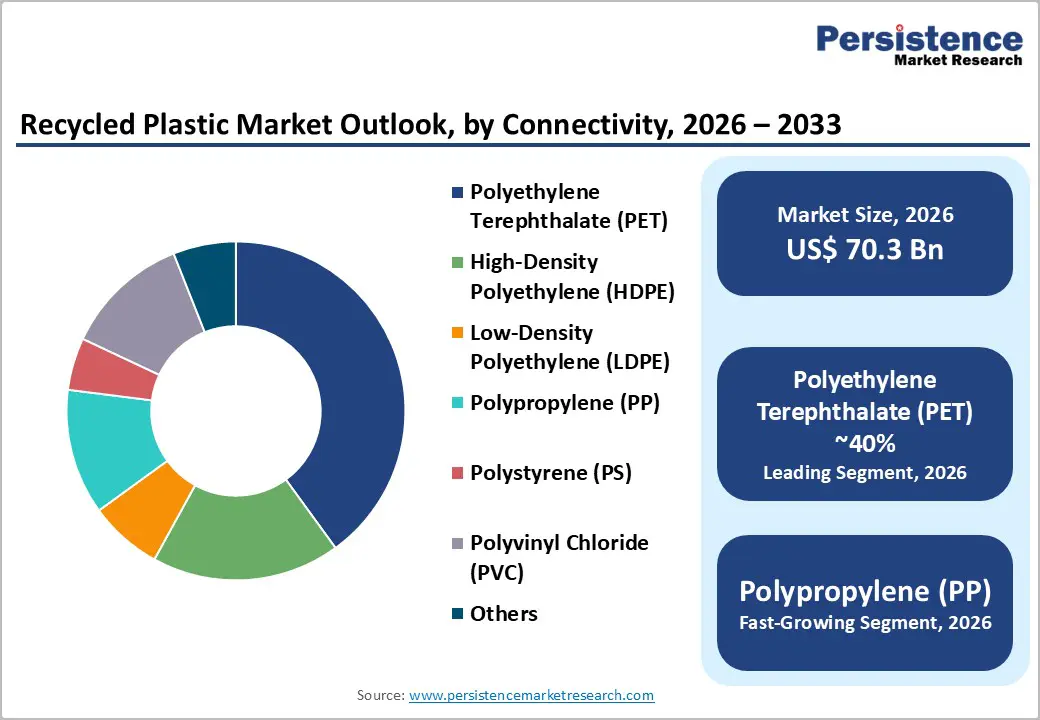

The global recycled plastic market is likely to be valued at US$ 70.3 billion in 2026 and is expected to reach US$ 131.0 billion by 2033, growing at a CAGR of 9.3% during the forecast period from 2026 to 2033. This expansion is being driven by tightening global regulations on plastic waste, rising corporate commitments to circular-economy targets, and growing consumer preference for products made with post-consumer recycled (PCR) content.

Key Industry Highlights:

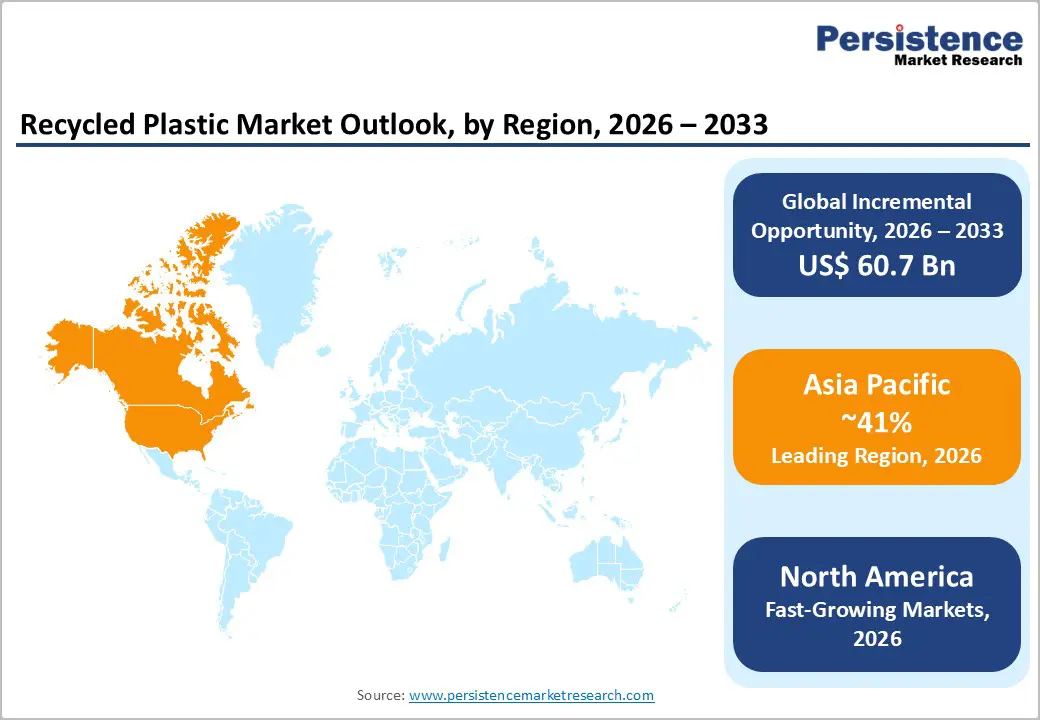

- Regional Leadership: Asia Pacific leads the Recycled Plastic Market by volume and installed recycling capacity, supported by rapid industrialization, large packaging and construction sectors, and strong policy momentum in China, India, and ASEAN countries.

- Fastest-Growing Market: North America is emerging as a fast-growing region, driven by Extended Producer Responsibility (EPR) laws, recycled-content mandates, and rising investments in bottle-to-bottle and chemical recycling infrastructure.

- Dominant Product Type: Polyethylene Terephthalate (PET) is the dominant product-type segment, accounting for roughly 40% of global recycled plastic demand, primarily due to its extensive use in beverage bottles and food-grade packaging.

- Fastest-Growing Product Type: Recycled Polypropylene (rPP) is one of the fastest-growing segments, driven by increasing adoption in automotive interiors, battery enclosures, and consumer-goods containers as manufacturers seek to reduce Scope 3 emissions.

- Key Opportunity: The expansion of chemical and advanced recycling for mixed films and multi-layer laminates represents a major opportunity to convert hard-to-recycle waste into high-quality recycled resins, broadening the feedstock base and creating new revenue pockets.

| Key Insights | Details |

|---|---|

|

Recycled Plastic Market Size (2026E) |

US$ 70.3 Bn |

|

Market Value Forecast (2033F) |

US$ 120.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.5% |

Market Dynamics

Drivers - Regulatory Push for Recycled Content and EPR Schemes

Stringent regulatory frameworks mandating minimum recycled-content requirements for plastic packaging are among the strongest drivers of the recycled-plastic market. In the European Union, the Packaging and Packaging Waste Regulation (PPWR), which entered into force in February 2025 and will apply from August 2025, sets binding recycled-content targets for plastic packaging and reinforces design-for-recycling criteria. By 2030, the regulation mandates 30% recycled content in PET-based contact-sensitive packaging and 10–35% in other plastic packaging categories, creating a structural pull for rPET, rHDPE, and other mechanically recycled streams.

In the United States, states such as California have enacted Assembly Bill 793, which requires beverage containers to contain 25% recycled content by 2025 and 50% by 2030, directly boosting demand for food-grade recycled PET. Similar recycled-content targets are being introduced in India and China, where central authorities have mandated minimum recycled-content requirements for PET bottles and containers, signaling long-term policy support for the recycled-plastic market.

Corporate Sustainability Commitments and Brand-Led PCR Adoption

Major consumer-goods and beverage companies are increasingly committing to high levels of post-consumer recycled (PCR) content in their packaging portfolios, thereby significantly expanding the addressable market for recycled resins. Global beverage giants such as Coca-Cola and PepsiCo have pledged to use 50% rPET in their bottles by 2030, while retailers such as Boots and M&S are integrating recycled HDPE and rPET into bottles, trays, and flexible packaging formats.

These commitments are backed by long-term offtake agreements with recyclers and investments in bottle-to-bottle recycling infrastructure, particularly in the EU and the U.S. In parallel, Extended Producer Responsibility (EPR) systems in several OECD countries are shifting financial responsibility for collection and recycling to producers, thereby incentivizing them to design for recyclability and to increase the use of recycled plastic to meet compliance targets and reduce plastic tax liabilities. This convergence of brand-driven demand and regulatory pressure is creating a durable growth engine for the recycled plastic market.

Restraints - Feedstock Quality, Contamination, and Sorting Inefficiencies

One of the primary constraints on the Recycled Plastic Market is the inconsistency and contamination of post-consumer plastic waste streams, which reduce yield, increase processing costs, and limit the availability of food-grade recycled resins. Data from the European Environment Agency indicate that roughly 25% of collected plastic waste is rejected at sorting facilities due to contamination, incorrect sorting, or mixed polymers, undermining the efficiency of mechanical recycling.

Globally, only about 14% of plastic packaging is collected for recycling, and an estimated 2% is effectively recycled into products of equal or higher value, highlighting the gap between collection and the production of high-quality outputs. This low effective recycling rate constrains the supply of rPET, rHDPE, and other high-value recyclates, forcing brand owners to blend recycled content with virgin material or rely on more expensive chemical recycling solutions, thereby limiting the pace at which the Recycled Plastic Market can scale.

Competition from Low-Cost Virgin Plastics and Price Volatility

Another key restraint is the persistent price advantage of virgin plastic over many recycled resins, particularly during periods of low oil prices, which can erode manufacturers' economic incentive to switch to recycled plastic. In several emerging markets, low-cost virgin polyolefins remain abundant and heavily subsidized, making it difficult for recyclers to compete on price without policy support such as plastic taxes or recycled-content mandates.

Recycled resin prices are subject to volatility driven by fluctuations in collection volumes, sorting capacity, and demand from key end-use sectors such as packaging and automotive. This volatility complicates long-term procurement planning for brand owners and can delay or dilute their circular-economy commitments, thereby acting as a structural brake on the growth of the recycled-plastic market.

Opportunities - Rapid Growth of Recycled Polypropylene (rPP) in Automotive and Consumer Goods

Recycled polypropylene (rPP) is among the fastest-growing segments in the Recycled Plastic Market, driven by rising demand from the automotive and consumer-goods sectors. PP is widely used in automotive interiors, bumpers, battery enclosures, and under-the-hood components, and manufacturers are increasingly substituting virgin PP with rPP to reduce carbon footprint and meet Scope 3 emissions targets.

In Europe and North America, leading automakers such as Volkswagen, BMW, and Ford have announced targets to incorporate 20% recycled plastics in new vehicles by 2030, with rPP playing a central role. In parallel, consumer-goods companies are adopting rPP for rigid containers, household products, and toys, supported by improvements in sorting and washing technologies that enhance the quality and consistency of rPP streams. This combination of regulatory pressure, brand-led demand, and technological progress positions rPP as a high-growth opportunity segment in the recycled plastic market.

Expansion of Chemical and Advanced Recycling for Hard-to-Recycle Streams

The development and commercialization of chemical and advanced recycling technologies present a major opportunity to unlock value from hard-to-recycle plastic waste such as mixed films, multi-layer laminates, and contaminated packaging. Traditional mechanical recycling struggles with these streams, but chemical recycling routes such as pyrolysis, depolymerization, and dissolution can convert mixed or contaminated plastics back into monomers or feedstocks suitable for producing food-grade resins. The companies such as Eastman, Dow, and SUEZ announced or expanded molecular-recycling facilities targeting PET and mixed plastics, signaling growing industry confidence in these technologies. As these facilities scale, they are expected to increase the availability of high-quality recycled resins from previously non-recyclable waste, thereby broadening the feedstock base and creating new revenue pockets for participants.

Category-wise Analysis

By Product Type Insights

Among product-type segments, polyethylene terephthalate (PET) is the leading polymer in the recycled plastic market, accounting for approximately 40% of global recycled plastic volume. This dominance is underpinned by the widespread use of PET in beverage bottles, food containers, and rigid packaging, which are highly visible, easily collected, and widely accepted in curbside recycling programs. In Europe and North America, rPET has become the material of choice for bottle-to-bottle recycling, with several national markets achieving over 30% recycled content in PET bottles. Beverage majors such as Coca-Cola and PepsiCo have committed to using 50% rPET by 2030, thereby underpinning long-term demand and driving investment in food-grade recycling infrastructure. In Asia, particularly in China and India, new regulations mandating minimum recycled-content requirements for PET bottles and containers are expected to further consolidate PET’s leadership position in the recycled-plastic market.

By Source Insights

By source, bottles are the largest feedstock category for recycled plastics, accounting for approximately 52% of post-consumer plastic recovered for recycling in markets such as the United States. PET and HDPE bottles dominate this stream, benefiting from well-established collection systems, deposit-return schemes, and brand-driven bottle-to-bottle recycling initiatives. In the U.S., more than 56% of post-consumer plastic recovered for recycling comes from bottles, underscoring their importance as a high-quality, high-volume feedstock for the recycled plastic market.

In Europe, deposit-return systems in countries such as Germany, Sweden, and Norway achieve collection rates above 90% for PET bottles, enabling high yields of food-grade rPET. As more regions adopt bottle-deposit schemes and mandatory recycled-content targets, the bottles segment is expected to remain the backbone of the market.

By Application Insights

By application, packaging is the dominant end-use segment, capturing an estimated 40% of global recycled plastic demand. Within this context, rPET and rHDPE are the primary resins used for bottles, trays, clamshells, and other rigid containers for food, beverages, pharmaceuticals, and personal-care products. Industry data indicate that packaging accounts for over 50% of the recyclate PET market and a similar share of the recycled HDPE market, reflecting the centrality of packaging in circular-economy strategies. In Europe, recycled-plastic packaging is further supported by PPWR-driven recycled-content targets and design-for-recycling requirements, while in Asia, the rapid growth of e-commerce and fast-moving consumer goods (FMCG) is increasing demand for sustainable packaging solutions. As brands across food, beverage, cosmetics, and pharmaceuticals intensify their PCR commitments, the packaging segment will continue to anchor growth in the global market.

Regional Insights

North America Recycled Plastic Market Trends

North America is a mature and innovation-driven hub for the Recycled Plastic Market, with the United States leading the adoption of Extended Producer Responsibility (EPR)-style laws in several states and strong brand-led demand for post-consumer recycled (PCR) content. States such as California, Oregon, Maine, and Colorado have implemented or are advancing EPR frameworks that require producers to fund or manage recycling of their packaging, while Assembly Bill 793 in California mandates 25% recycled content in beverage containers by 2025 and 50% by 2030. These policies are stimulating investments in bottle-to-bottle recycling, advanced sorting, and chemical recycling infrastructure, particularly for rPET and rHDPE. At the same time, contamination and sorting inefficiencies remain challenges, with studies indicating that 25–30% of collected plastic waste is rejected at sorting facilities, underscoring the need for improved design for recycling and consumer education.

North America also benefits from a robust innovation ecosystem, with companies such as Plastipak Holdings, Inc., Clean Harbors, Inc., and Republic Services expanding food-grade recycling capacity and integrating digital traceability and blockchain-based compliance tools into their operations. The region is a key market for automotive and packaging applications of recycled plastics, with major automakers and FMCG brands sourcing rPET, rHDPE, and rPP to meet Scope 3 emissions targets and circular-economy pledges. As EPR frameworks expand across more states and plastic tax mechanisms gain traction, North America is expected to remain a high-growth region in the Recycled Plastic Market, albeit with ongoing challenges related to feedstock quality and infrastructure investment.

Europe Recycled Plastic Market Trends

Europe is one of the most regulated and policy-advanced regions for the Recycled Plastic Market, with the European Union leading the world in circular-economy legislation. The Packaging and Packaging Waste Regulation (PPWR), which entered into force in February 2025 and will apply from August 2025, sets binding recycled-content targets, design-for-recycling criteria, and reuse obligations for plastic packaging, creating a strong pull for rPET, rHDPE, and other mechanically recycled resins. By 2030, the regulation requires 30% recycled content in PET-based contact-sensitive packaging and 35% in other plastic packaging categories, directly shaping investment decisions by brand owners and recyclers. Countries such as Germany, the United Kingdom, France, and Spain are at the forefront of implementation, supported by existing deposit-return schemes, EPR systems, and high PET bottle collection rates.

In Germany, recycled HDPE demand is particularly strong, with the national market projected to reach around 1.5 billion euros by 2026, driven by packaging, construction, and consumer-goods applications. The UK is also expanding its EPR framework for packaging, which is expected to increase demand for recycled plastics across FMCG, retail, and e-commerce sectors. At the same time, Europe faces challenges related to feedstock contamination and sorting inefficiencies, with the European Environment Agency reporting that 20% of collected plastic waste is rejected at sorting facilities. Despite these hurdles, the combination of harmonized regulation, strong brand commitments, and advanced recycling infrastructure positions Europe as a core region for growth.

Asia Pacific Recycled Plastic Market Trends

Asia-Pacific is the largest region for the Recycled Plastic Market, driven by rapid industrialization, urbanization, and the expansion of the packaging, construction, and textile sectors. In China, the 2018 ban on plastic waste imports triggered a wave of domestic recycling capacity development, particularly for PET and HDPE, while new regulations mandating minimum recycled content in PET bottles and containers are expected to further increase demand. India has also strengthened its Plastic Waste Management Rules, including recycled-content targets and EPR-style obligations for producers and brand owners, creating a structured policy environment for post-consumer recycling. In Japan and South Korea, advanced sorting technologies and extended producer responsibility systems support high recovery rates for PET bottles and rigid packaging, reinforcing the region’s leadership in mechanical recycling.

ASEAN countries such as Vietnam, Thailand, and Indonesia are emerging as important manufacturing and recycling hubs, benefiting from low labor costs, growing domestic consumption, and foreign direct investment (FDI) in the packaging and automotive industries. In India, the plastic recycling market is projected to grow from about 4.1 billion dollars in 2024 to nearly 6.9 billion dollars by 2033, reflecting strong underlying demand for recycled PET, HDPE, and PP. Across the Asia Pacific, the building and construction sector is increasingly adopting recycled HDPE, LDPE, and PP for pipes, decking, and plastic lumber, supported by green-building standards and municipal procurement policies. These dynamics make Asia Pacific a critical growth engine for the Recycled Plastic Market over the 2026–2033 horizon.

Competitive Landscape

The global recycled plastic market is moderately consolidated at the global level, with a mix of large multinational waste-management and recycling companies, specialized resin producers, and regional players. Major integrated players such as Veolia, SUEZ worldwide, REMONDIS SE & Co. KG, Republic Services, Waste Connections, and Clean Harbors, Inc. dominate collection, sorting, and mechanical recycling capacity in North America and Europe, while companies such as Plastipak Holdings, Inc. and Covestro AG focus on high-value food-grade rPET and engineering-grade recycled resins. The market is becoming increasingly competitive as chemical recycling and advanced sorting technologies lower entry barriers and attract new entrants from the chemical, energy, and technology sectors. Leading firms are differentiating themselves through vertical integration, digital traceability platforms, food-grade certification, and long-term offtake agreements with FMCG and automotive brands, while emerging business models emphasize closed-loop partnerships, plastic-credit trading, and circular-economy-as-a-service offerings.

Key Developments:

- In February 2025: Plastipak Holdings, Inc. announced a major expansion of its food-grade rPET production capacity in North America, investing over 300 million dollars to add new bottle-to-bottle recycling lines and increase output by more than 200,000 metric tons per year. The expansion is aligned with long-term supply agreements with leading beverage brands seeking to meet 50% rPET targets by 2030, reinforcing Plastipak’s position as a key supplier in the Recycled Plastic Market.

- In August 2024, SUEZ worldwide and Shell International B.V. formed a joint venture to develop chemical recycling facilities in Europe, targeting mixed and contaminated plastic waste streams that are difficult to process through mechanical recycling. The JV plans to deploy pyrolysis and dissolution technologies to produce high-quality feedstocks for food-grade resins, strengthening the supply of recycled plastic for packaging and automotive applications.

- In March 2024: Veolia inaugurated a state-of-the-art plastic sorting facility in France, capable of processing over 100,000 metric tons of post-consumer plastic waste annually with AI-driven optical sorting and near-infrared (NIR) technology. The facility is designed to increase the yield of high-purity rPET and rHDPE, supporting brand commitments to PCR content and enhancing Europe’s position in the Recycled Plastic Market.

Companies Covered in Recycled Plastic Market

- CLEAN HARBORS, INC.

- Plastipak Holdings, Inc.

- Custom Polymers

- Waste Connections

- Shell International B.V.

- Fresh Pak Corp

- SUEZ worldwide

- KW Plastics

- Republic Services

- REMONDIS SE & Co. KG

- Covestro AG

- Ultra‑Poly Corporation

- Veolia

- ReVital Polymers

- WM Intellectual Property Holdings, L.L.C.

- Indorama Ventures Public Company Limited

- Far Eastern New Century Corporation

- Alpla Group

- Alpek S.A.B. de C.V.

- Berry Global Inc.

Frequently Asked Questions

The Recycled Plastic Market is estimated at US$ 70.3 Billion in 2026 and is projected to reach US$ 131.0 Billion by 2033, expanding at a CAGR of 9.3% between 2026 and 2033, supported by regulatory mandates, corporate sustainability commitments, and rising demand for post‑consumer recycled (PCR) resins.

Key demand drivers include recycled‑content mandates such as the EU Packaging and Packaging Waste Regulation (PPWR) and California Assembly Bill 793, Extended Producer Responsibility (EPR) schemes, and brand‑led PCR commitments by beverage, FMCG, and automotive companies seeking to reduce Scope 3 emissions and meet circular‑economy targets.

The Polyethylene Terephthalate (PET) segment dominates the Recycled Plastic Market, accounting for roughly 55–60% of global recycled plastic demand, driven by its widespread use in beverage bottles, food containers, and rigid packaging, along with strong bottle‑to‑bottle recycling infrastructure in Europe and North America.

Asia Pacific leads the Recycled Plastic Market in terms of volume and installed capacity, supported by rapid industrialization, large packaging and construction sectors, and policy‑driven recycling initiatives in China, India, and ASEAN countries, which are expanding domestic collection and processing infrastructure.

A key opportunity lies in chemical and advanced recycling for mixed films, multi‑layer laminates, and contaminated packaging, which can convert hard‑to‑recycle waste into high‑quality recycled resins and expand the feedstock base for food‑grade and engineering‑grade applications.

Major players include CLEAN HARBORS, INC., Plastipak Holdings, Inc., Waste Connections, Republic Services, SUEZ worldwide, Veolia, REMONDIS SE & Co. KG, Covestro AG, Shell International B.V., KW Plastics, Indorama Ventures Public Company Limited, and Berry Global Inc., among others, spanning collection, sorting, mechanical recycling, and chemical‑recycling activities.