- Specialty & Fine Chemicals

- Propylene Oxide Market

Propylene Oxide Market Size, Share, and Growth Forecast 2026 - 2033

Propylene Oxide Market by Production Process (Chlorohydrin Process, Styrene Monomer Process, TBA Co-Product Process, Hydrogen Peroxide Process, Cumene-Based Process), Application (Polyether Polyols, Propylene Glycols, Glycol Ethers, Others), End-user (Automotive, Building & Construction, Chemical & Pharmaceutical, Textile & Furnishing, Packaging, Electronics, Others), and Regional Analysis, 2026 - 2033

Propylene Oxide Market Size and Trend Analysis

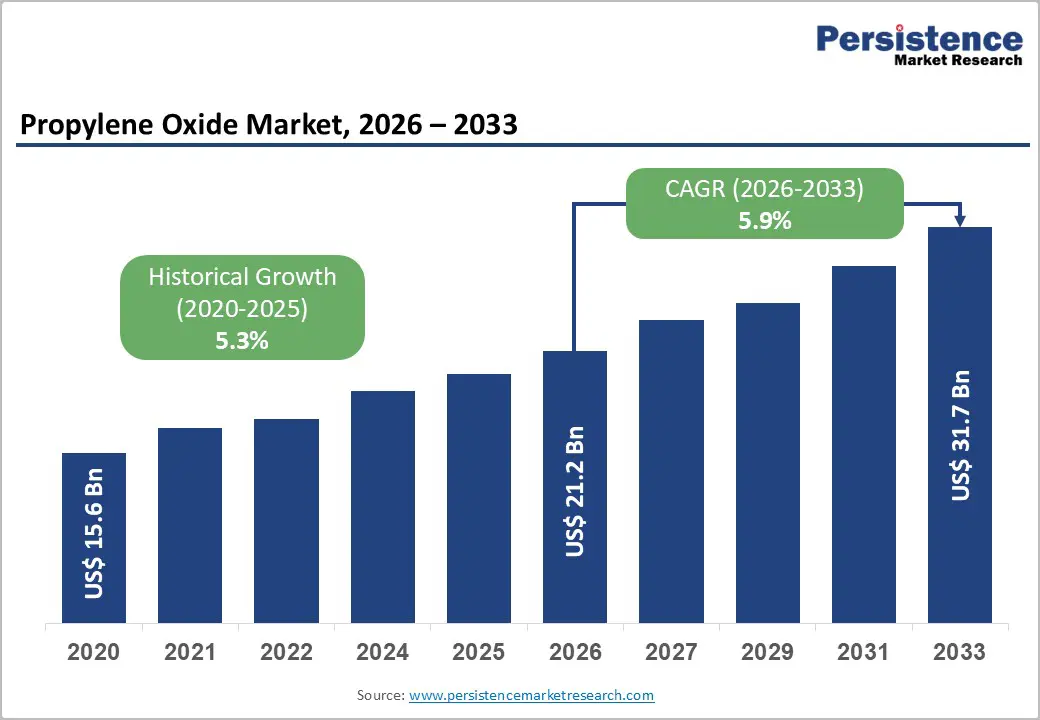

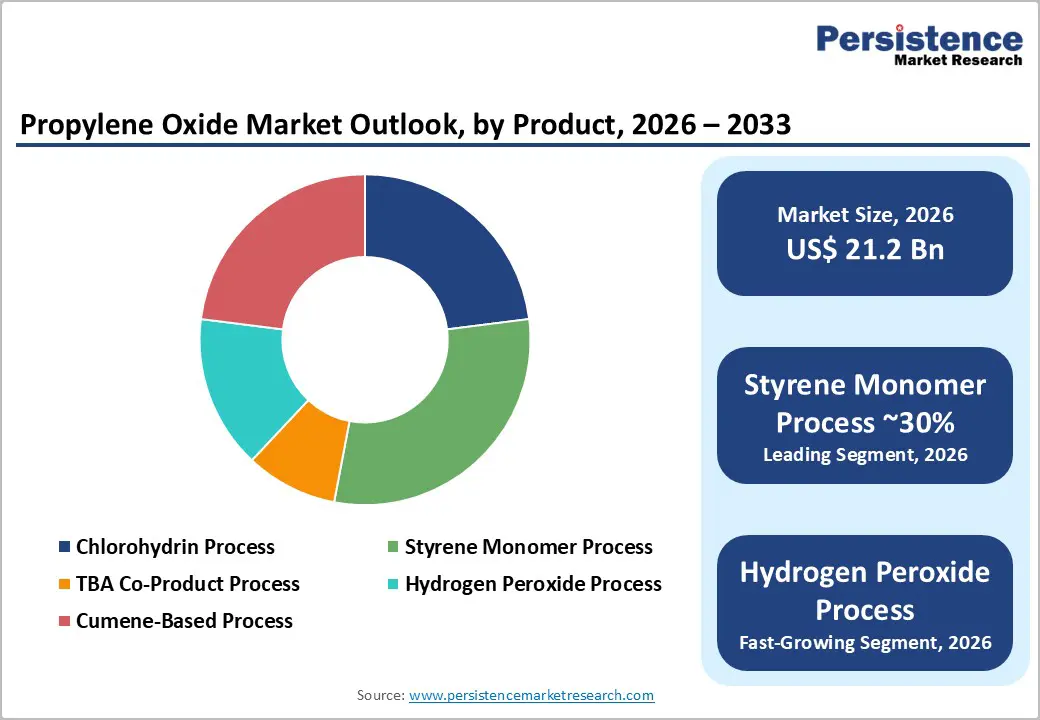

The global propylene oxide market size is expected to be valued at US$ 21.2 billion in 2026 and projected to reach US$ 31.7 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

This sustained growth is primarily driven by the expanding global polyurethane industry's insatiable demand for propylene oxide-derived polyether polyols, used in automotive seating, building insulation, and furniture foam, combined with the rapid adoption of cleaner hydrogen peroxide-to-propylene oxide (HPPO) production technology.

The market grew from US$ 15.6 billion in 2020 at a historical CAGR of 5.3%, underpinned by accelerating automotive production and construction activity in the Asia Pacific, growing propylene glycol demand from the pharmaceutical and food industries, and significant capacity expansion investments in the Middle East and China by major petrochemical producers.

Key Industry Highlights

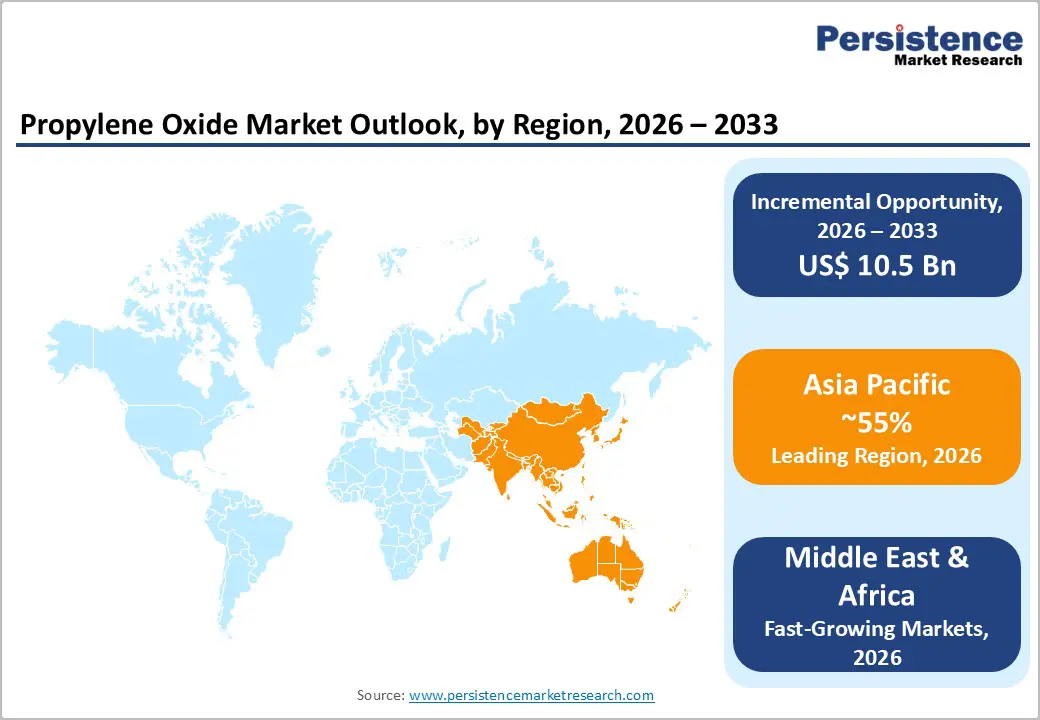

- Leading Region: Asia Pacific commands 55% global propylene oxide market share in 2026, anchored by China's 45% world demand share per CPCIF data, Japan's advanced polyurethane technology sector, and India's rapidly expanding construction and automotive polyurethane consumption markets.

- Fastest Growing Region: MEA is the fastest growing PO region through 2026 - 2033, driven by SABIC and Saudi Aramco Vision 2030 PO capacity investments leveraging low-cost refinery propylene, growing regional polyurethane construction demand, and automotive assembly expansion across GCC markets.

- Leading Production Process: The SM/PO process holds 30% production market share in 2026, sustained by LyondellBasell, Repsol, and Shell's large-scale integrated facilities where styrene co-product economics cross-subsidize PO production costs across the U.S., Europe, and Asia Pacific.

- Fastest Growing Segment: HPPO is the fastest growing production process at 8% CAGR (2026 - 2033), driven by EU Green Deal environmental mandates, REACH restrictions on chlorinated byproducts, and BASF/Dow's commercially proven 300,000 ton/year Antwerp facility demonstrating the technology's industrial scalability.

- Key Opportunity: IEA-mandated building insulation upgrades under EU EPBD and U.S. IECC codes, combined with EV polyurethane weight reduction demand for battery thermal management and seating, represent the highest-growth structural opportunity for PO-derived polyether polyol consumption through 2033.

DRO Analysis

Drivers - Expanding Polyurethane Industry Driving Insatiable Polyether Polyol Demand

The polyurethane industry is the single most important demand driver for propylene oxide, as polyether polyols, produced by reacting PO with initiators under alkaline catalysis, account for the majority of global PO consumption. The American Chemistry Council (ACC) and ISOPA (European Diisocyanate & Polyol Producers Association) document consistent growth in global polyurethane foam production for automotive, construction, and appliance applications.

The automotive sector's accelerating electric vehicle (EV) production is generating additional polyurethane demand for lightweight seating systems, battery thermal management foam, and sound insulation, each requiring significant polyether polyol input. Building insulation demand, driven by stringent energy efficiency codes including the EU's Energy Performance of Buildings Directive (EPBD), is further sustaining polyurethane rigid foam growth that directly consumes PO-derived polyols at scale globally.

Asia Pacific Industrial Expansion and Growing Chemical Intermediate Consumption

The relentless expansion of industrial production and chemical manufacturing across China, India, and Southeast Asia is creating growing, diversified demand for propylene oxide as a key chemical intermediate across multiple downstream value chains. China's position as the world's largest propylene oxide consumer, accounting for approximately 45% of global demand per Chinese Petroleum and Chemical Industry Federation (CPCIF) data, reflects the scale of its integrated PO-to-polyol-to-polyurethane manufacturing ecosystem.

India's rapidly expanding construction sector, driven by PMAY housing programs and Smart Cities Mission infrastructure, generates growing demand for polyurethane insulation and sealants requiring PO-derived intermediates. Regional PO capacity expansion by major producers including LyondellBasell, BASF SE, and domestic Chinese producers reflects producers' confidence in Asia Pacific's long-term demand trajectory through 2033.

Restraints - Environmental Regulation and Chlorinated Byproduct Concerns with Chlorohydrin Process

The chlorohydrin process, historically the second-largest PO production method, generates substantial quantities of chlorinated wastewater and calcium chloride byproducts that face increasingly stringent environmental regulatory pressure under the EU's Industrial Emissions Directive (IED)) and equivalent regulations globally.

Treatment and disposal of these chlorinated waste streams add significant operating cost burdens and, in some jurisdictions, regulatory liability. This is compelling operators to retire chlorohydrin capacity and transition to cleaner processes, creating near-term supply disruption risk and capital reallocation costs that constrain overall market expansion rates.

Propylene Feedstock Price Volatility and Petrochemical Supply Chain Exposure

Propylene oxide production is fundamentally dependent on propylene, a petroleum refinery and steam cracker byproduct, as its primary feedstock. Crude oil and natural gas price volatility directly impacts propylene availability and cost, creating significant PO production cost variability.

The IEA documents propylene price fluctuations of 30-50% in extreme market conditions, compressing PO producer margins when feedstock costs spike without corresponding downstream price pass-through. This feedstock exposure limits margin predictability and can deter capacity investment during periods of elevated petrochemical price uncertainty.

Opportunities - Hydrogen Peroxide Process (HPPO): Fastest Growing Technology Driving Green PO Production

The Hydrogen Peroxide to Propylene Oxide (HPPO) process represents the fastest growing production technology for propylene oxide at an estimated CAGR of 8% through 2026 - 2033, driven by its significantly lower environmental footprint compared to conventional chlorohydrin and co-product processes. HPPO produces PO with water as the primary byproduct rather than co-products requiring market placement or chlorinated waste streams.

BASF SE and Dow Inc. jointly developed the HPPO process commercially implemented at their Antwerp facility, producing 300,000 tons of PO annually. Evonik's hydrogen peroxide catalyst technology and LyondellBasell's HPPO partnerships are expanding the technology's global adoption. The EU's Green Deal and REACH regulations constraining chlorinated chemical pathways are creating regulatory incentives favoring HPPO as the process of choice for new PO capacity investments in Europe.

Middle East & Africa Green PO Capacity: Fastest Growing Regional Opportunity

The Middle East & Africa region represents the fastest growing regional opportunity for propylene oxide, driven by Gulf Cooperation Council (GCC) petrochemical integration strategies that are incorporating PO production as a value-added downstream extension of existing propylene supply chains. Saudi Arabia's SABIC and Saudi Aramco have active downstream chemical investment programs under Vision 2030 that target significant PO and polyol capacity expansion to capture growing regional and Asian export market demand.

The availability of low-cost propylene feedstock from GCC refineries provides a structural cost advantage that makes MEA PO capacity economically competitive on a global basis. Growing regional polyurethane foam demand from the GCC's active construction sector and automotive assembly industry is additionally sustaining domestic PO consumption growth, with the region projected to record the highest CAGR among all regions through 2033.

Category-wise Analysis

Production Process Insights

The styrene monomer process (SM/PO) is the leading production process segment, accounting for approximately 30% market share in 2026. In the styrene monomer co-production route, propylene is oxidized with ethylbenzene hydroperoxide to produce propylene oxide and styrene monomer simultaneously, making the economics of this process dependent on both PO and styrene market conditions.

The process is commercially operated at a large industrial scale by producers including LyondellBasell, Repsol, and Royal Dutch Shell across major production hubs in the United States, Europe, and Asia. The SM/PO route's advantage lies in the high co-product value of styrene, a major plastics monomer, which cross-subsidizes PO production economics, enabling competitive pricing. Its large installed capacity base across mature markets sustains its market share leadership despite growing competition from cleaner HPPO technology.

Application Insights

Polyether polyols is the dominant application segment, accounting for approximately 68% of total propylene oxide consumption in 2026. Polyether polyols are the primary building blocks for polyurethane foams, elastomers, coatings, and sealants, collectively representing one of the world's most important synthetic polymer families.

The ISOPA documents that global polyurethane production exceeds 25 million tons annually, with flexible foam for furniture and automotive seating, rigid foam for construction insulation, and reaction injection molding (RIM) applications collectively consuming the majority of global polyether polyol output. The automotive industry's growing adoption of lightweight polyurethane components for electric vehicles, reducing vehicle weight and extending battery range, sustains structural demand growth for polyether polyols derived from PO.

End-user Insights

The building & construction sector is the dominant end-user segment, accounting for approximately 32% of propylene oxide consumption in 2026. Building insulation, particularly polyurethane rigid foam used in roofing panels, wall insulation boards, and cavity insulation systems, is the single largest application for PO-derived polyether polyols globally. The IEA identifies building envelope insulation as one of the most cost-effective carbon reduction measures available, with polyurethane delivering superior thermal performance per unit thickness compared to alternative insulation materials.

Mandatory building energy codes including the EU EPBD, U.S. International Energy Conservation Code (IECC), and national building regulations across Asia Pacific are driving specification of high-performance insulation that disproportionately favors PO-based polyurethane systems, sustaining the construction sector's dominant end-use position.

Regional Insights

Asia Pacific leads the global propylene oxide market with approximately 55% market share in 2026, while Middle East & Africa (MEA) is the fastest growing region, projected to record the highest CAGR through 2026 - 2033, driven by GCC petrochemical integration, low-cost feedstock advantages, and active polyurethane demand growth from construction and automotive sectors.

North America Propylene Oxide Market Trends and Insights

North America is a mature, highly integrated propylene oxide market with well-established SM/PO and HPPO production facilities operating on scale. The region is characterized by active capacity optimization and technology upgrading investments, particularly toward HPPO, driven by environmental compliance requirements. Growing demand from automotive lightweight materials and building insulation upgrade programs sustains regional consumption growth, with LyondellBasell and Dow Inc. operating the region's largest PO facilities.

U.S. Propylene Oxide Market Size

The United States accounts for approximately 76% of North American propylene oxide market revenue in 2026. The U.S. is home to some of the world's largest PO production facilities, with LyondellBasell's Texas and New Jersey operations and Dow's Texas sites representing major capacity centers. Strong automotive polyurethane demand and residential construction insulation applications sustain U.S. market growth, projected at approximately 5.4% CAGR through 2033.

Europe Propylene Oxide Market Trends and Insights

Europe's propylene oxide market is undergoing an environmental technology transition, with the EU Industrial Emissions Directive driving retirement of chlorohydrin capacity and investment in HPPO and SM/PO processes at European production sites. The EU Green Deal's building renovation wave, targeting 35 million building retrofits, and automotive lightweighting programs are sustaining polyurethane demand. BASF SE, LyondellBasell, and Repsol operate major European PO facilities serving integrated downstream polyol production.

Germany Propylene Oxide Market Size

Germany holds approximately 24% of European propylene oxide market revenue in 2026. BASF SE's Ludwigshafen Verbund site, the world's largest integrated chemical complex, operates Europe's most advanced PO-to-polyol production system. Germany's strong automotive manufacturing cluster (BMW, Volkswagen, Mercedes-Benz) drives high-value polyurethane demand for seating, instrument panels, and insulation applications requiring PO-derived polyols.

U.K. Propylene Oxide Market Size

The United Kingdom represents approximately 11% of European propylene oxide market revenue in 2026. The UK's Future Homes Standard and Building Regulations Part L energy efficiency mandates are driving polyurethane insulation demand in residential construction. Huntsman Corporation's UK polyurethane operations and active construction renovation programs sustain PO derivative consumption. UK market CAGR is projected at approximately 5.5% through 2033.

France Propylene Oxide Market Size

France contributes approximately 10% of European propylene oxide market revenue in 2026. France's RE2020 building energy standard and active residential renovation programs under national energy efficiency schemes sustain polyurethane insulation demand. France's chemical industry cluster in Normandy and the Rhone Valley processes significant PO volumes for downstream polyol and glycol ether applications serving automotive, construction, and specialty chemical end markets.

Asia Pacific Propylene Oxide Market Trends and Insights

Asia Pacific dominates global propylene oxide production and consumption, with China accounting for approximately 45% of world PO demand per CPCIF data. China's integrated petrochemical-to-polyurethane industrial clusters, concentrated in Guangdong, Shandong, and Jiangsu provinces, represent the world's largest single-geography PO consumption market. Japan's advanced polyurethane technology sector and India's rapidly expanding construction and automotive markets are secondary but fast-growing regional demand drivers.

India Propylene Oxide Market Size

India represents approximately 8% of Asia Pacific propylene oxide market revenue in 2026. India's expanding automotive production, supported by the PLI scheme for the automobile sector, and rapid construction activity under PMAY and Smart Cities Mission, are driving polyurethane demand and associated PO consumption growth. India is projected to grow at approximately 8.2% CAGR through 2033, among the fastest in the region.

Japan Propylene Oxide Market Size

Japan contributes approximately 9% of Asia Pacific propylene oxide market revenue in 2026. Mitsui Chemicals, Sumitomo Chemical, and Tokuyama Corporation are key domestic producers. Japan's advanced automotive and electronics industries generate high-value polyurethane and specialty glycol ether demand. Japan's Top Runner Program is building energy standards to sustain polyurethane insulation consumption. Japan is projected at approximately 5.0% CAGR through 2033.

Southeast Asia Propylene Oxide Market Size

Southeast Asia collectively accounts for approximately 11% of the Asia Pacific propylene oxide market revenue in 2026. Thailand, Indonesia, and Vietnam are experiencing rapid construction and manufacturing sector growth generating polyurethane demand. The ASEAN Plan of Action for Energy Cooperation and national building energy codes across the region are progressively driving insulation upgrading demand. Several major chemical producers are investing in regional PO and polyol production capacity to serve growing ASEAN domestic market demand.

Competitive Landscape

The global propylene oxide market exhibits a moderately consolidated competitive structure, with a small number of vertically integrated petrochemical majors controlling most of the global capacity. LyondellBasell Industries, BASF SE, Dow Inc., and Huntsman Corporation collectively represent a significant share of global PO production through ownership of multiple large-scale SM/PO and HPPO facilities.

Key competitive differentiators include feedstock integration, process technology ownership (HPPO vs. SM/PO), geographic positioning near downstream polyol demand centers, and forward integration into polyether polyols. Emerging strategic trends include HPPO capacity investments, joint venture structures for new-build facilities, and Middle East expansion to leverage low-cost propylene feedstock advantages.

Key Developments

- In March 2025, BASF SE announced the expansion of its hydrogen peroxide to propylene oxide (HPPO) production capacity at its Antwerp, Belgium facility, reinforcing its commitment to greener PO production technology and targeting growing European demand for sustainable chemical intermediates.

- In October 2024, LyondellBasell Industries completed the commissioning of new propylene oxide capacity in the United States as part of its PO/TBA plant expansion in Texas, adding significant new output to serve North American polyurethane foam and chemical intermediate markets.

- In April 2023, Huntsman Corporation announced strategic investments in its European polyols and propylene oxide production operations to optimize energy efficiency and reduce carbon intensity in line with EU Industrial Emissions Directive requirements and corporate net-zero commitments.

Propylene Oxide Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 15.6 Billion |

| Current Market Value (2026) | US$ 21.2 Billion |

| Projected Market Value (2033) | US$ 31.7 Billion |

| CAGR (2026 - 2033) | 5.9% |

| Leading Region | Asia Pacific, 55% market share (2026) |

| Dominant Category - Production Process | Styrene Monomer Process, 30% share (2026) |

| Top-Ranking Category - Application | Polyether Polyols, 68% share (2026) |

| Incremental Opportunity (2026 - 2033) | US$ 10.5 Billion |

Companies Covered in Propylene Oxide Market

- BASF SE

- Mitsui Chemicals

- Dow Inc.

- Huntsman Corporation

- Lyondellbasell Industries Holdings

- Royal Dutch Shell

- Huntsman International

- SABIC

- Repsol

- Tokuyama Corporation

- Sumitomo Chemical Co.,

- SKC

- LG Chem

- Celanese Corporation

- INEOS Group

Frequently Asked Questions

The global propylene oxide market is projected to be valued at US$ 21.2 billion in 2026, growing from US$ 15.6 billion in 2020. The market is forecast to reach US$ 31.7 billion by 2033 at a CAGR of 5.9%, representing an absolute dollar opportunity of US$ 10.5 billion.

Primary drivers include the global polyurethane industry consuming over 25 million tons annually per ISOPA data, with PO-derived polyether polyols as the fundamental raw material. EU EPBD building renovation wave targeting 35 million building retrofits by 2030 drives rigid polyurethane insulation demand.

Asia Pacific leads with approximately 55% market share in 2026, with China representing 45% of global PO demand per CPCIF data through its massive integrated petrochemical-to-polyurethane industrial clusters. Japan's advanced polyurethane sector, India's expanding construction and automotive markets, and Southeast Asia's growing manufacturing base collectively reinforce Asia Pacific's dominant position.

The HPPO (Hydrogen Peroxide to Propylene Oxide) process at 8% CAGR is the highest-growth technology segment, driven by EU IED compliance mandates, retiring chlorohydrin capacity, and BASF/Dow's commercially proven 300,000 ton/year Antwerp HPPO facility demonstrating industrial scalability.

Key companies include LyondellBasell Industries, BASF SE, Dow Inc., Huntsman Corporation, SABIC, Repsol, Royal Dutch Shell, Mitsui Chemicals, Sumitomo Chemical, SKC, LG Chem, Covestro AG, INEOS Group, Celanese Corporation, and Tokuyama Corporation.