- Sensors & Controls

- Precision Farming Market

Precision Farming Market Size, Share, and Growth Forecast, 2025- 2032

Precision Farming Market by Component (Precision Farming Hardware, Farm Management Software (FMS), Services), Application (Soil Monitoring, Yield Monitoring, Crop Scouting, Field Mapping, Farm Management Systems, Weather Tracking & Forecasting, Others), and Regional Analysis for 2025 - 2032

Precision Farming Market Share and Trends Analysis

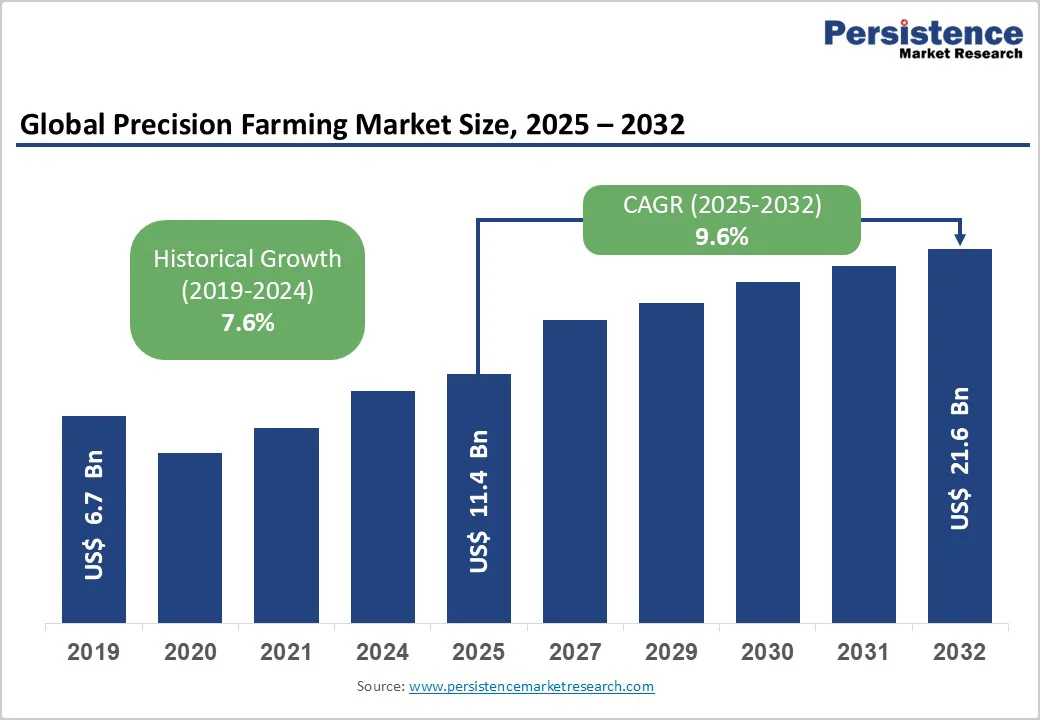

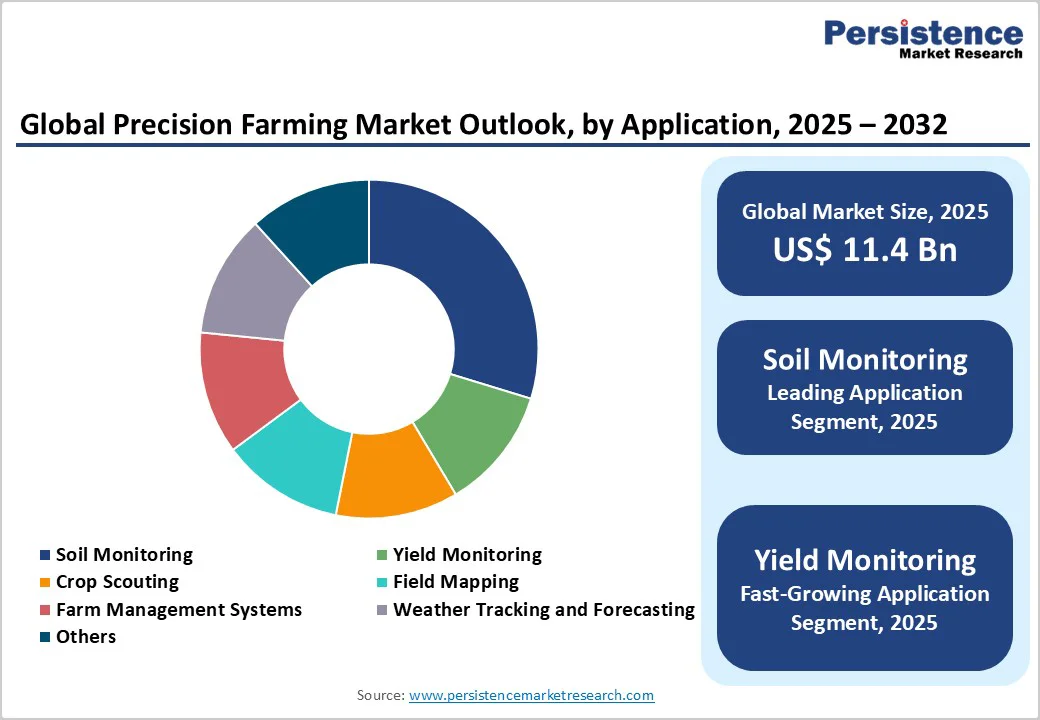

The global precision farming market size is likely to be valued at US$11.4 billion in 2025, and is projected to reach US$21.6 billion by 2032, growing at a CAGR of 9.6% during the forecast period 2025 - 2032.

This robust expansion reflects the accelerating integration of advanced technologies, including GPS/GNSS systems, IoT sensors, artificial intelligence (AI), and drone-based monitoring, into mainstream agricultural operations.

The market's growth trajectory is underpinned by an exponential rise in global food demand driven by population growth surpassing 8 billion, the urgent need to optimize resources amid climate volatility, and increasing regulatory pressure for sustainable farming practices.

Technology adoption is transitioning from early-stage pilot programs in developed markets to widespread implementation across diverse farm sizes and geographies, with precision farming hardware commanding the largest revenue share, while farm management software demonstrates the fastest growth.

Key Industry Highlights

- Rising Food Demand Drives Precision Farming Adoption: Global food production must increase by 70% by 2050 to meet population growth, pushing farmers toward precision farming technologies that boost yields and reduce input waste.

- Surge in Autonomous and Robotic Equipment: Autonomous tractors and harvesters are reshaping agriculture, with leading OEMs like John Deere and AGCO achieving 20-35% productivity gains and labor savings up to 50%.

- Hardware Segment Leads Market Revenue: Precision farming hardware is expected to capture over 42% of market revenue in 2025, supported by declining sensor costs and robust equipment durability.

- Farm Management Software Emerges as the Fastest-growing Segment: Farm management software is projected to grow the fastest between 2025 and 2032, fueled by AI analytics and subscription-based digital platforms.

- Soil and Yield Monitoring Enhance Sustainability: Soil monitoring accounts for over 22% of applications, enabling considerable water savings, while yield monitoring achieves 98% accuracy and up to 92% predictive yield forecasting.

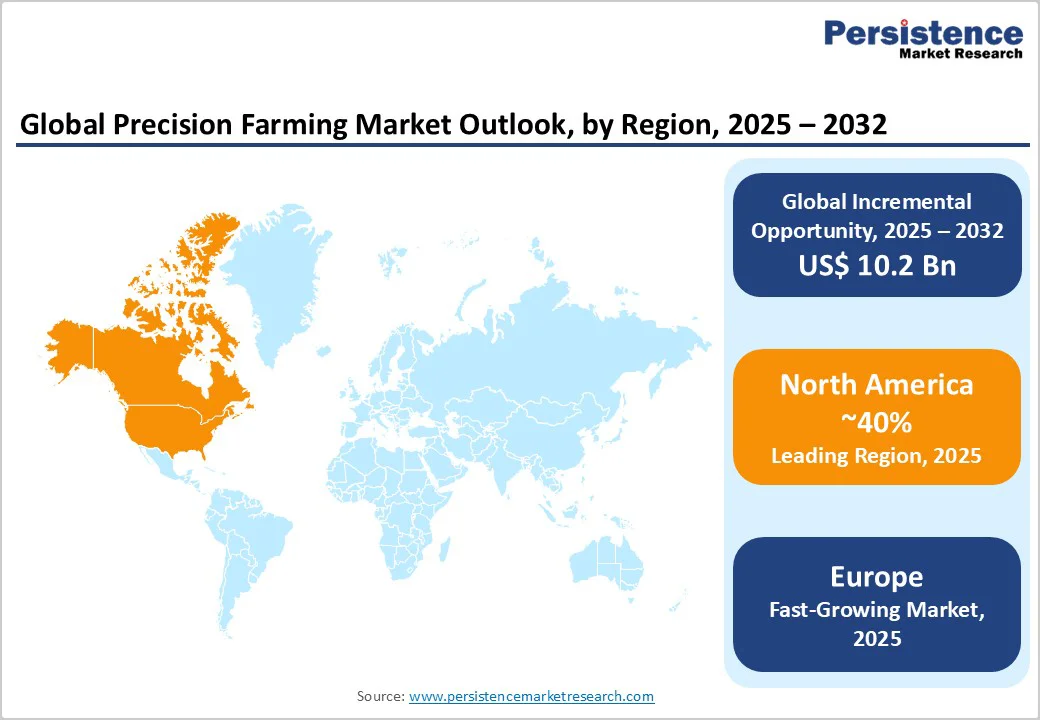

- North America Maintains Global Leadership: With around 42% revenue share, North America remains dominant due to mature agricultural infrastructure and high precision farming penetration in large U.S. farms.

- Europe Emerges as the Fastest-growing Regional Market: The European market is advancing rapidly through sustainability mandates, digital innovation, and EUR 6.2 billion in German CAP investments.

- Consolidated Market with Strategic Partnerships: John Deere, AGCO, CNH Industrial, Trimble, and Topcon are the top players, controlling over 50% of the market, reinforced by partnerships such as AGCO-Trimble’s PTx Trimble JV and Deere’s acquisition of Smart Apply.

| Key Insights | Details |

|---|---|

| Precision Farming Market Size (2025E) | US$11.4 Bn |

| Market Value Forecast (2032F) | US$21.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 9.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Global Food Demand and Agricultural Productivity Pressures

The global population is projected to grow significantly over the coming decades, creating unprecedented pressure on food production systems. Population growth will add billions of people, with the fastest expansion occurring in developing nations, particularly in sub-Saharan Africa and parts of Asia.

Urbanization will accelerate simultaneously, with most of the world's population living in cities by 2050. This combination of population growth and urban migration will intensify demand for food supplies and create challenges for agricultural systems. To meet this growing demand, the farm sector must substantially increase food production in the coming years.

Precision farming technologies offer a practical solution to these productivity challenges by optimizing how farmers use resources and make decisions based on data. Field studies demonstrate that precision farming systems can reduce input waste while increasing productivity and profitability. Farms adopting these technologies report lower fuel consumption, reduced fertilizer use, and fewer pesticide applications than with traditional farming methods.

These efficiency gains benefit both food security and farm economics, making precision agriculture an attractive investment for producers seeking to maintain or improve profitability while meeting rising demand. Supporting this are government mechanisms that are providing financial assistance and establishing favorable policy frameworks, promoting these technologies and making them more accessible to farmers.

Rural Connectivity Gaps and Digital Infrastructure Limitations

Reliable internet connectivity remains inconsistent across rural agricultural regions, creating a significant barrier to the adoption of precision farming. A large percentage of farms located in remote areas lack stable mobile networks, broadband access, or consistent satellite internet coverage.

This connectivity limitation is particularly acute in developing economies across Africa, South Asia, and Latin America, where many farms cannot access advanced precision agriculture technologies due to infrastructure constraints. Even in areas with connectivity, bandwidth limitations and high latency can prevent real-time monitoring and equipment coordination.

Alternative solutions, such as satellite-based systems and low-power wide-area networks, partially address connectivity challenges but require additional investments and technical expertise that many farmers cannot readily access.

Autonomous Equipment and Robotics Integration

The next phase of precision farming advancement centers on fully autonomous equipment that operates with minimal human intervention. Autonomous agricultural equipment addresses acute labor shortages in farming while simultaneously improving operational efficiency and productivity. Leading manufacturers have developed autonomous tractors, harvesters, and specialty equipment that can operate independently within defined field conditions.

These autonomous systems deliver significant labor savings and productivity improvements compared to traditional farming methods. The autonomous agricultural equipment market is experiencing rapid growth, with expansion expected to accelerate through 2030.

Precision farming infrastructure, including GPS guidance systems, field-mapping technology, and connectivity solutions, provides the essential foundation that autonomous equipment needs to operate effectively in field operations.

Category-wise Analysis

Component Insights

Precision farming hardware remains the dominant component in agricultural technology investments in 2025, reflecting its essential role in modern farming operations. This segment includes automation systems, precision guidance equipment, and sensing devices that collect critical farm data.

Advanced displays and steering systems help farmers operate equipment with high accuracy, while sensors monitor soil conditions, crop health, and environmental factors in real time. Hardware solutions deliver proven benefits, including increased productivity, reduced input costs, and improved operational efficiency.

Sensor costs have decreased significantly in recent years, and manufacturers now offer extended warranties on wireless sensors, making these investments more affordable and reliable for farmers of all sizes.

Farm management software (FMS) has emerged as the fastest-growing segment for the 2025 - 2032 period, as farmers increasingly recognize the value of data analysis and cloud-based tools. Modern software platforms enable farmers to collect, analyze, and act on farm data from multiple sources through a single interface.

These platforms generate subscription-based revenues by providing continuous agronomic insights and recommendations tailored to individual farm conditions. Leading companies offer cloud-based systems that synchronize data across devices and integrate artificial intelligence for predictive analytics. As FMS technologies become increasingly sophisticated and user-friendly, adoption rates are accelerating across diverse farm sizes and regions.

Application Insights

Soil monitoring represents a critical application of precision agriculture, providing the foundation for sustainable and efficient farming practices. Ground-based sensors measure essential soil parameters including moisture content, temperature, nutrient concentrations, and salinity at various soil depths. These sensors deliver regular data updates that help farmers make informed decisions about fertilization, irrigation, and tillage practices.

Soil monitoring insights enable farmers to reduce fertilizer overapplication, optimize water use, and prevent soil degradation. Integration with farm management software allows farmers to create customized application maps that improve efficiency and support environmental stewardship. Regulatory frameworks in major agricultural regions are supporting the adoption of soil monitoring by requiring consistent assessment of soil health.

Yield monitoring is likely to be the fastest-growing precision agriculture application through 2032, as it provides immediate, measurable benefits to farm operations. Modern yield monitors equipped with advanced sensors accurately map crop productivity, enabling farmers to identify underperforming areas and optimize management decisions.

These systems provide real-world validation of farming practices and enable farmers to benchmark their performance against historical data and peer operations. Advanced yield monitoring systems achieve high accuracy and seamlessly transfer data to cloud platforms where farmers can analyze multi-season trends.

Integration of yield data with satellite imagery and artificial intelligence enhances the ability to forecast yields before harvest, which supports better logistics planning and marketing decisions. By closing the feedback loop between field performance and decision-making, yield monitoring helps farmers continuously improve their operations and maximize profitability.

Regional Insights

North America Precision Farming Market Trends

North America maintains its position as the global leader in precision farming adoption and investment, reflecting decades of technological advancement and strong infrastructure development. The U.S. accounts for the majority of regional market value, demonstrating its status as the world's most technologically advanced agricultural economy.

Precision farming technologies are widely adopted on large commercial farms, enabling farmers to reduce input costs and improve operational efficiency. Key growth drivers include access to extensive dealer networks that provide local support, farmer familiarity with precision technologies developed over many years, and government programs that assist with equipment costs.

Additional revenue opportunities through carbon-credit monetization programs further incentivize technology adoption among producers seeking new income sources.

Government support mechanisms continue to strengthen precision farming adoption across North America. The U.S. Department of Agriculture (USDA) provides cost-sharing assistance programs that help farmers purchase precision equipment and reduce initial capital requirements.

On large farms, private 5G networks enable real-time coordination of equipment and support the deployment of emerging autonomous systems. Canada represents a mature market where grain producers across the Prairie Provinces have successfully adopted precision technologies at scale, benefiting from economies of scale across large agricultural operations.

Europe Precision Farming Market Trends

Europe has rapidly become the fastest-growing regional market for precision farming, driven by ambitious sustainability goals and supportive government policies. Germany leads European advancement with substantial investments in digital agriculture infrastructure and widespread broadband coverage that reaches agricultural areas.

Leading German equipment manufacturers integrate precision systems directly into machinery at the factory level, enabling rapid adoption. France supports adoption through collaborative research partnerships between government and private companies, along with farmer training programs and financial grants for the purchase of sensors and software.

The U.K. maintains innovation momentum through subsidy programs and specialized agricultural technology centers. Spain and Italy are deploying satellite-based irrigation management systems to help farmers manage water resources during drought conditions.

Eastern European countries are accelerating precision farming adoption using EU funding for equipment modernization, though fiber connectivity limitations remain a challenge in some areas. Regulatory frameworks established by the EU, including sustainability mandates and soil health requirements, are driving farmers to adopt precision technologies to meet compliance obligations.

The regional market benefits from access to European satellite systems that provide positioning and earth observation data for agricultural applications. These converging factors of regulatory support, government investment, technology innovation, and access to advanced satellite systems are positioning Europe for sustained rapid growth in precision farming adoption.

Competitive Landscape

The global precision farming market landscape includes several large established companies alongside numerous smaller regional and specialized players. The largest companies collectively hold a significant share of the worldwide market, though the degree of market concentration varies considerably by product category.

Guidance and steering systems show higher concentration among leading manufacturers, while software and analytics solutions feature greater competition and lower barriers to entry. This fragmentation reflects the diverse nature of precision farming technology, where established equipment manufacturers compete alongside specialized technology providers and emerging digital agriculture companies.

Equipment manufacturers are pursuing vertical integration by offering complete systems from machinery through software and dealer support, allowing farmers to work within a single brand ecosystem with seamless integration. Specialized technology providers are focusing on retrofit solutions and partnerships with multiple equipment manufacturers, serving farmers with mixed-brand fleets who need compatible technology across different machines.

Software and data analytics companies are emphasizing agronomic insights and decision support tools that work across different equipment brands, appealing to farmers seeking data-driven farming practices independent of equipment choices. This diversity of competitive approaches provides farmers with multiple options for adopting precision farming technologies that align with their specific operations, preferences, and existing equipment investments.

Key Industry Developments

- In November 2025, AGCO Corporation showcased its full portfolio of agricultural brands and precision farming technologies at AGRITECHNICA 2025, featuring new tractor series, autonomous systems, and mixed-fleet farm management solutions. The company highlighted innovations including Fendt autonomous technologies with AI-powered weed control, the Valtra Coach Talking Tractor with AI assistance, and battery-electric equipment options designed to reduce emissions. Key product launches included PTx's new FarmENGAGE mixed-fleet management platform, advanced precision planting systems, and sustainable technologies such as electric tractors and carbon calculators.

- In July 2025, EOS Data Analytics unveiled an updated AI-driven satellite analytics platform designed to help farmers in Southeastern Europe optimize crop monitoring and boost yields sustainably. The platform uses advanced satellite technology and artificial intelligence to detect crop health issues such as water stress, fungal infections, and nutrient deficiencies, enabling farmers to make targeted management adjustments. The European precision agriculture market is experiencing rapid growth as farmers adopt satellite and AI analytics tools, supported by government digitalization initiatives through the Common Agricultural Policy.

- In February 2025, Topcon Corporation entered into a strategic partnership with Bonsai Robotics to accelerate agricultural automation, particularly for permanent crops. The collaboration integrates Bonsai Robotics’ vision-based autonomous driving technology with Topcon Agriculture’s expertise in sensors, connectivity, and smart implements. By combining Bonsai’s navigation systems with Topcon’s autosteering, telematics, and integration capabilities, the partnership aims to deliver advanced automation solutions that reduce labor intensity, improve data-driven decision-making, and enhance precision harvesting across complex agricultural environments.

Companies Covered in Precision Farming Market

- Acron Group

- Abaco S.p.A.

- Ag Leader Technology

- AgEagle Aerial Systems Inc

- AGCO Corporation

- Bayer AG (Climate LLC.)

- CNH Industrial N.V.

- Cropx Inc.

- Deere & Company

- Hexagon AB

- Kubota Corporation

- TeeJet Technologies

- Topcon Corporation

- Trimble Inc.

- Other Market Players

Frequently Asked Questions

The global precision farming market is estimated to reach US$ 11.4 billion in 2025.

The key market driver is the growing need to enhance farm productivity and resource efficiency through data-driven agricultural practices.

The market is poised to witness a CAGR of 9.6% from 2025 to 2032.

The accelerating integration of GPS/GNSS systems, IoT sensors, AI, and drone-based monitoring into mainstream agricultural operations to address the urgent need for resource optimization amid climate volatility, and the transition of technology adoption from early-stage pilot programs in developed markets to widespread implementation across diverse farm sizes and geographies are key market opportunities.

Abaco S.p.A., Ag Leader Technology, AgEagle Aerial Systems Inc., AGCO Corporation, and Bayer AG (Climate LLC) are some of the key players in the market.