- Marine

- Outboard Engines Market

Outboard Engines Market Size, Share, and Growth Forecast 2026 - 2033

Outboard Engines Market by Power (Less than 30 HP, 30 HP – 100 HP, 100 HP – 150 HP, 150 HP – 400 HP, above 400 HP), by Application (Recreational, Commercial, Military / Defense), Engine Type (Two-Stroke Engines, Four-Stroke Engines, Electric), and Regional Analysis, 2026-2033

Outboard Engines Market Size and Trend Analysis

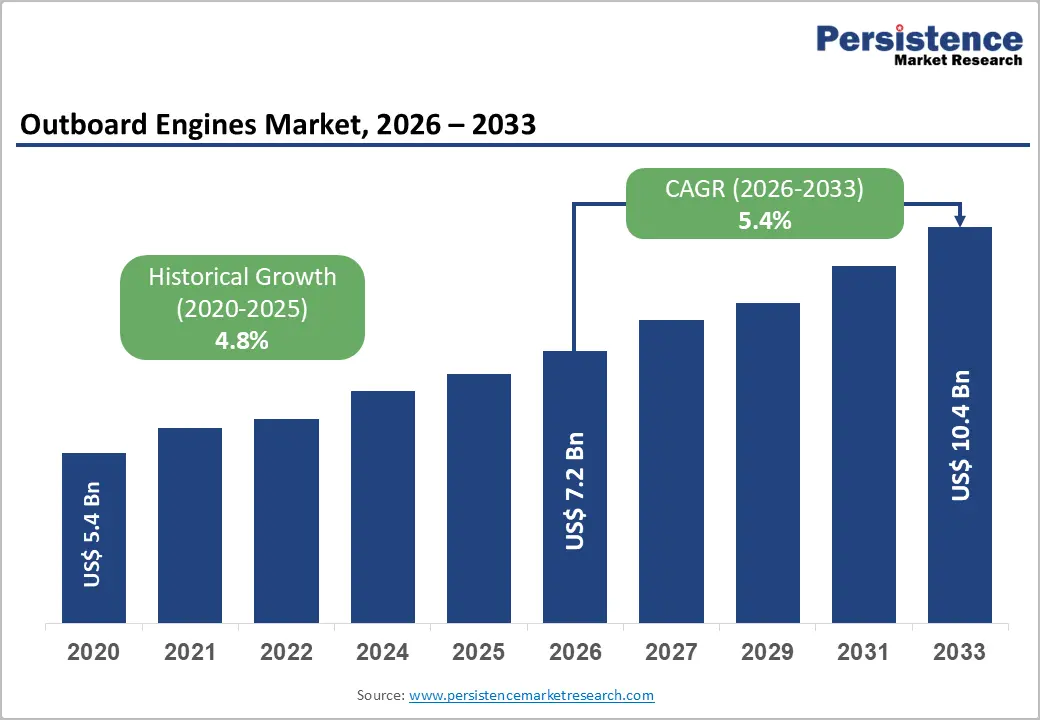

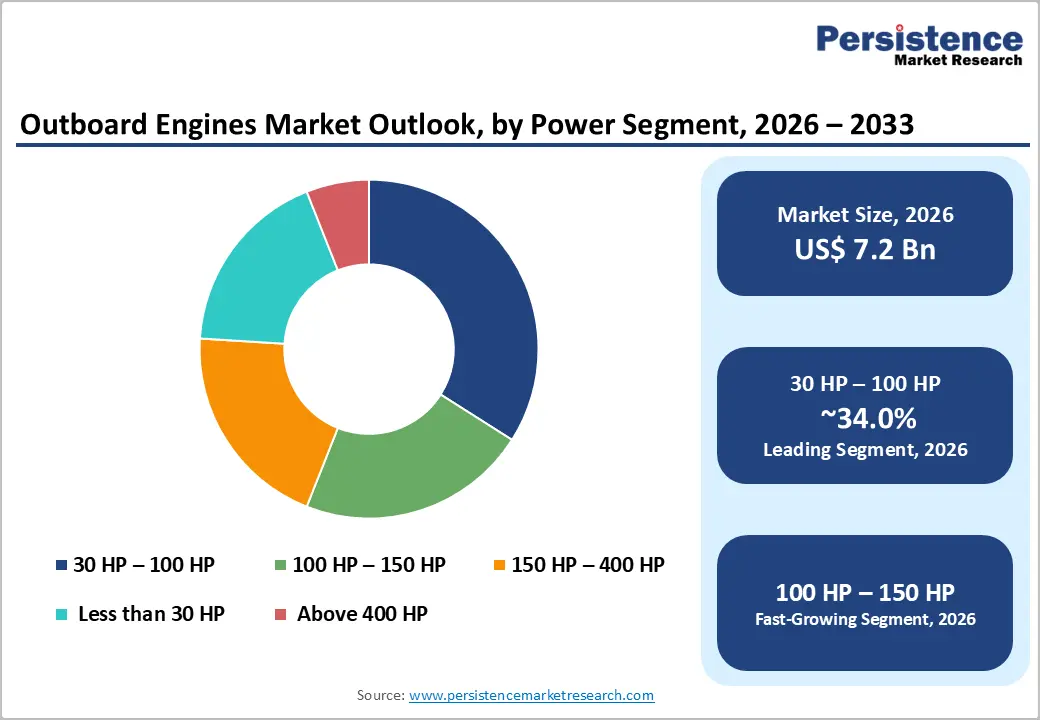

The global outboard engines market size is expected to be valued at US$ 7.2 billion in 2026 and projected to reach US$ 10.4 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033. The market trajectory is shaped by a shift toward four-stroke and electric propulsion, replacing aging two-stroke fleets across recreational, commercial, and defense waterways. Stricter emission norms enforced by the U.S. Environmental Protection Agency (EPA) and the European Union’s Stage V Non-Road Mobile Machinery Regulation are pushing manufacturers to upgrade portfolios.

Recreational boating registrations recorded by the National Marine Manufacturers Association (NMMA) continue to climb in coastal economies, while patrol-vessel fleet renewals by coast guards across the Asia Pacific and the Middle East sustain commercial demand.

Key Industry Highlights:

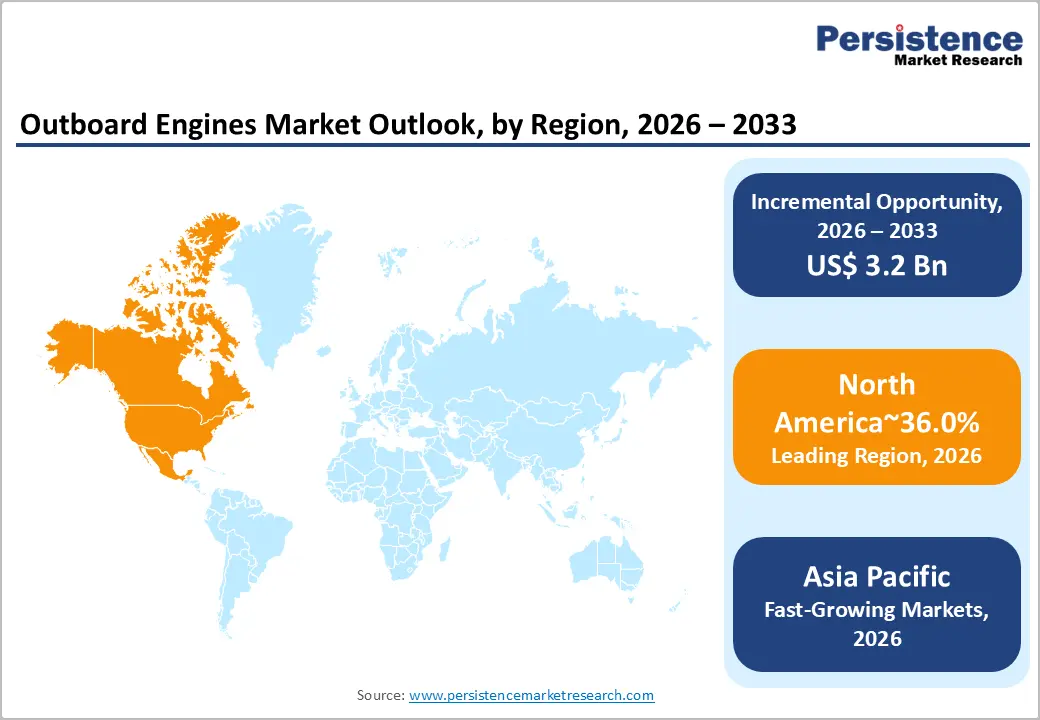

- Leading Region: North America leads with approximately 36% market share in 2025, anchored by the U.S. recreational boating economy and U.S. Coast Guard fleet renewal programs that sustain high-HP outboard demand.

- Fast-Growing Market: Asia Pacific records the fastest forecast CAGR of about 6.2% through 2033, supported by China’s fishing fleet modernization, India’s PMMSY subsidies, and rising recreational boating across Southeast Asia.

- Dominant Application: The recreational application segment dominates with around 62% share in 2025, driven by NMMA-tracked U.S. boat ownership, European leisure boating, and growing Asia Pacific marina infrastructure.

- Fastest Growing Power Segment: The 100 HP – 150 HP power band records the fastest forecast CAGR of about 6% through 2033, fueled by mid-size offshore center-console adoption and commercial workboat upsizing.

- Key Opportunity: Electric outboard adoption led by Torqeedo, Mercury Avator, and Pure Watercraft opens a multi-billion-dollar replacement opportunity as inland emission zones expand across Europe and North America through 2033.

DRO Analysis

Drivers - Recreational Boating Resurgence and First-Time Buyer Penetration

Recreational boating remains the cornerstone of outboard engine demand, with the NMMA reporting that U.S. recreational boating contributed approximately US$230 billion in annual economic output and supported nearly 812,000 jobs. New powerboat retail sales in the United States crossed 230,000 units in 2024, with first-time buyers comprising about 34% of the new boat purchaser base, according to NMMA consumer surveys.

Coastal lifestyle migration, post-pandemic interest in outdoor leisure, and accessible financing through marine lenders such as the National Marine Lenders Association members have widened the buyer pool. This influx directly translates to outboard repower cycles every 8–12 years, sustaining aftermarket replacement volumes.

Defence and Coast Guard Fleet Modernisation

Naval and coast guard fleet renewals are reinforcing the commercial backbone of the market. The U.S. Coast Guard operates over 1,600 small boats, many powered by twin or quad outboard configurations, and its FY 2025 budget allocated approximately US$13.95 billion, with portions earmarked for Response Boat–Small (RB-S II) and Special Purpose Craft replacements. Similarly, the Indian Coast Guard inducted multiple Interceptor Boats and Fast Patrol Vessels under the Make in India initiative, while NATO member states accelerated maritime patrol capability acquisitions following heightened Black Sea and Baltic activity. High-output 400+ HP outboards from Mercury Marine and Yamaha Motor Co., Ltd. dominate these specifications, lifting average selling prices.

Restraints - Stringent Emission Regulations and Compliance Costs

Regulatory tightening, while a long-term enabler, imposes near-term cost burdens. The EPA Marine SI Engine Rule and EU Recreational Craft Directive (2013/53/EU) mandate progressively lower NOx, hydrocarbon, and particulate thresholds, requiring fuel injection upgrades, catalytic systems, and onboard diagnostics.

The California Air Resources Board (CARB) further restricts two-stroke carbureted engines below specific HP ratings. Smaller manufacturers and regional players face certification costs that can exceed US$1.5 million per engine family, limiting product breadth and pushing some legacy two-stroke models out of OECD markets entirely.

Volatility in Raw Material and Aluminium Pricing

Outboard engines rely heavily on aluminum alloys, stainless steel, and copper for housings, propellers, and wiring. London Metal Exchange (LME) aluminum prices oscillated between US$ 2,150 and US$ 2,650 per tonne through 2024–2025, while copper crossed US$ 9,800 per tonne in 2024.

Compounded by Red Sea shipping detours via the Cape of Good Hope, freight costs added 15–20% to delivered component prices. Manufacturers such as BRP Inc. and Suzuki Motor Corporation absorbed margin pressure rather than fully pass through, constraining profitability and delaying capacity investments in some product lines.

Opportunities - Electric Outboard Adoption and Inland Waterway Decarbonization

The shift toward electric propulsion represents the most disruptive opportunity. The International Maritime Organisation (IMO) revised greenhouse gas strategy targets net-zero shipping emissions by or around 2050, and although IMO rules primarily target large vessels, regional bodies like the European Inland Navigation authorities and the U.S. National Park Service are imposing electric-only zones on lakes such as Lake Tahoe and parts of the German Bodensee.

Companies including Torqeedo GmbH (a DEUTZ AG subsidiary), Pure Watercraft, and Mercury Marine’s Avator series are scaling production, with Torqeedo reporting deliveries surpassing 20,000 units annually. Battery cost declines tracked by BloombergNEF, falling to roughly US$ 115 per kWh in 2024, are narrowing the total cost of ownership gap versus combustion equivalents.

High-Horsepower Premium Segment for Offshore and Centre-Console Boats

Offshore centre-console boats increasingly carry triple, quadruple, and even quintuple outboard rigs above 400 HP, with Mercury Racing 600 and Yamaha XTO 450 anchoring this premium tier. The NMMA noted that boats over 36 feet in length grew at the fastest pace in U.S. retail registrations through 2024.

Sport-fishing tournaments organised by the International Game Fish Association (IGFA) and offshore fishing demand from the Gulf of Mexico and the Australian Great Barrier Reef corridors are catalysing demand for these high-margin units. With average selling prices exceeding US$ 70,000 per unit, this segment offers manufacturers disproportionate revenue contribution and brand-positioning leverage.

Category-wise Analysis

Power Insights

The 30 HP – 100 HP category leads the global outboard engines market with an estimated 34% share in 2025. This power band aligns with the most popular boat lengths between 16 and 22 feet, which dominate recreational fleets across the United States, Scandinavia, and Australia. According to the NMMA, aluminum fishing boats and pontoon boats typically rigged in this HP range together represented over 45% of new powerboat units sold in the U.S. in 2024.

The segment also serves commercial fishing skiffs in Southeast Asia and patrol craft for inland waterway authorities. The dominance of four-stroke fuel-injected variants from Yamaha Motor Co., Ltd., Honda Marine, and Suzuki Motor Corporation in this band, combined with strong dealer networks and replacement-cycle demand, anchors leadership.

Application Insights

The Recreational segment dominates the market with approximately 62% share in 2025, supported by the deep cultural penetration of leisure boating in mature economies. The NMMA reports that U.S. boat ownership stands at over 100 million participants and 11.6 million registered boats, while European Boating Industry data records about 6 million recreational boats across the European Union. Pontoons, bowriders, fishing boats, and personal watercraft tenders almost exclusively rely on outboard propulsion.

Discretionary spending recovery, marina expansion in the Mediterranean and Florida coastlines, and the rise of boat clubs and fractional-ownership models such as Freedom Boat Club (now part of Brunswick Corporation) reinforce the segment’s dominance, ensuring sustained replacement and upgrade demand from individual consumers.

Engine Type Insights

The Four-Stroke Engines segment commands roughly 64% market share in 2025, driven by superior fuel economy, lower emissions, and quieter operation compared to two-stroke alternatives. Phase-out mandates under the U.S. EPA and CARB rules effectively eliminated carbureted two-stroke sales in North America, while the EU Stage V regulations achieved similar results across Europe.

Major OEMs, including Yamaha Motor Co., Ltd., Mercury Marine, Honda Marine, and Suzuki Motor Corporation, have transitioned their entire portfolios to four-stroke architecture above 15 HP. Direct fuel injection, variable valve timing, and digital throttle-and-shift controls once premium features, are now standard across mid-range four-stroke offerings, reinforcing segment leadership and supporting the broader electric vehicle and marine propulsion transition narrative.

Regional Insights

North America Outboard Engines Market Trends and Insights

North America holds a share of 36% in 2025, anchored by the United States and supported by Canada’s strong recreational fishing culture across the Great Lakes and British Columbia coastline. NMMA retail data, expanding marina capacity, and fleet renewals at the U.S. Coast Guard and Department of Homeland Security waterborne units underpin demand. Hurricane-driven repower cycles in the Gulf states further accelerate aftermarket activity.

U.S. Outboard Engines Market Size

The United States outboard engines market value stood at US$ 2,105.3 Million in 2025, driven by record new powerboat registrations exceeding 230,000 units reported by the NMMA, sustained center-console boat demand in Florida, Texas, and the Carolinas, and large fleet contracts under the U.S. Coast Guard’s Response Boat program. Repower cycles from saltwater corrosion in Gulf marinas and tournament fishing in the Atlantic seaboard add structural depth.

Europe Outboard Engines Market Trends and Insights

Europe holds a share of 25.0% in 2025, supported by dense coastal recreational boating in the Mediterranean, Baltic, and North Sea corridors. The European Boating Industry records approximately 6 million recreational craft, while EU Stage V regulations are accelerating replacement of older two-stroke fleets. Defense procurement by NATO members is also reinforcing high-HP demand.

Germany Outboard Engines Market Size

Germany outboard engines market value stood at US$ 326.0 Million in 2025, driven by the country’s strong inland waterway network across the Rhine, Elbe, and Bodensee, and rising electric outboard adoption led by Torqeedo GmbH, headquartered near Munich. Stringent emission zones on Bavarian and Brandenburg lakes have catalyzed early electric uptake among rental fleets and private owners.

U.K. Outboard Engines Market Size

The United Kingdom outboard engines market accounts for roughly 15% of European demand, with strong activity around Solent, Cornwall, and Scottish Highlands boating hubs. The Royal Yachting Association (RYA) reports over 3.5 million participants in boating activities annually, while Royal National Lifeboat Institution (RNLI) rescue-craft renewals and rising small commercial workboat demand support steady aftermarket consumption.

France Outboard Engines Market Size

France outboard engines market value stood at US$ 221.0 Million in 2025, driven by the country’s Mediterranean and Atlantic coastlines, with strong demand from Côte d’Azur charter operators and Brittany fishing communities. The Fédération Française des Industries Nautiques (FIN) reports France as Europe’s largest pleasure-boat builder, sustaining outboard rigging demand for sub-30-foot powerboats and tenders.

Asia Pacific Outboard Engines Market Trends and Insights

Asia Pacific holds a share of 27.0% in 2025, with the region representing the fastest-growing geography at a forecast CAGR of approximately 6.2% between 2026 and 2033. Coastal economies across China, Indonesia, Vietnam, and the Philippines rely on outboard-powered fishing vessels for livelihood, while recreational boating is rising in Japan, Australia, and emerging in India. Chinese domestic manufacturers and Japanese OEMs jointly dominate regional supply.

China Outboard Engines Market Size

China outboard engines market value stood at US$ 495.7 Million in 2025, driven by the world’s largest fishing fleet the Ministry of Agriculture and Rural Affairs of China records over 560,000 motorized fishing vessels and rapid expansion of inland recreational boating around Qiandao Lake and Qingdao. Domestic players such as Hidea Power Machinery and Parsun Power Machine have scaled exports while government subsidies for fishing vessel modernization add structural demand.

India Outboard Engines Market Size

India outboard engines market value stood at US$ 257.0 Million in 2025, driven by traditional fishing fleets along Kerala, Gujarat, and Tamil Nadu coastlines, where the Department of Fisheries records over 200,000 motorized boats. Government schemes such as Pradhan Mantri Matsya Sampada Yojana (PMMSY), with an outlay of INR 20,050 Crore, subsidize mechanization, while Indian Coast Guard patrol craft expansion under Make in India boosts higher-HP segment demand.

Japan Outboard Engines Market Size

Japan accounts for approximately 16% of Asia Pacific outboard engine demand, supported by domestic manufacturing leadership of Yamaha Motor Co., Ltd., Honda Marine, Suzuki Motor Corporation, and Tohatsu Corporation. The Japan Marine Industry Association (JMIA) reports steady recreational boating around Tokyo Bay, Seto Inland Sea, and Okinawa, while coastal fishing co-operatives renew aging fleets under Fisheries Agency modernization grants.

Competitive Landscape

The global outboard engines market is moderately consolidated, with the top five manufacturers Yamaha Motor Co., Ltd., Mercury Marine (Brunswick Corporation), Honda Marine, Suzuki Motor Corporation, and BRP Inc. collectively commanding an estimated 70–75% of global revenue.

Strategies center on portfolio electrification, with Mercury Avator and Torqeedo Deep Blue spearheading the transition; modular platform architectures enabling shared components across HP bands; and digital integration through SmartCraft and Helm Master EX systems. Dealer-network depth, marine warranty reach, and joint development with boat builders such as Boston Whaler and Sea Ray remain decisive differentiators.

Key Developments:

- In March 2025, Honda Motor Co., Ltd. showcased its latest developments in the outboard engines market by unveiling a new “Sporty White” color option for its large-size outboard motor lineup (BF350, BF250, BF225, and BF200) at the HISWA In-Water Boat Show 2025 in the Netherlands. The update targets the premium high-horsepower segment, enhancing product differentiation and appeal in the recreational boating market.

- In April 2025, Suzuki Motor Corporation announced the development of a new anodising technology for outboard engine components, aimed at enhancing durability and environmental performance. The technology, first implemented in the DF140B outboard engine, significantly improves corrosion resistance of critical parts such as cooling ducts, cylinder block, cylinder head, and crankcase key components exposed to seawater environments.

Global Outboard Engines Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 5.4 Billion |

|

Current Market Value (2026) |

US$ 7.2 Billion |

|

Projected Market Value (2033) |

US$ 10.4 Billion |

|

CAGR (2026-2033) |

5.4% |

|

Leading Region |

North America, 36% |

|

Dominant Power Category |

30 HP – 100 HP, Holds 34% Share in (2025) |

|

Top-ranking Application |

Recreational, Holds 64% share in (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 3.2 Billion |

Companies Covered in Outboard Engines Market

- Yamaha Motor Co., Ltd.

- Brunswick Corporation

- Suzuki Motor Corporation

- Honda Motor Co., Ltd.

- BRP Inc.

- Tohatsu Corporation

- Parsun Power Machine Co., Ltd.

- Hidea Power Machinery Co., Ltd.

- Cox Powertrain Ltd.

- Elco Motor Yachts

Frequently Asked Questions

The global outboard engines market is expected to be valued at US$ 7.2 Billion in 2026 and is projected to reach US$ 10.4 Billion by 2033, growing at a CAGR of 5.4% during the forecast period.

Recreational boating resurgence with NMMA reporting U.S. economic output of US$ 230 Billion and over 230,000 new powerboat unit sales in 2024 combined with coast guard fleet modernization, is the primary demand driver.

North America leads with approximately 36% market share in 2025, anchored by the United States market valued at US$ 2,105.3 Million, supported by strong recreational boating culture and U.S. Coast Guard procurement.

Electric outboard adoption driven by IMO decarbonization goals, expanding emission zones on European and North American lakes, and falling battery costs (~US$ 115/kWh per BloombergNEF) represents the most significant long-term growth opportunity.

Leading players include Yamaha Motor Co., Ltd., Mercury Marine (Brunswick Corporation), Honda Marine, Suzuki Motor Corporation, BRP Inc., Tohatsu Corporation, Torqeedo GmbH, Pure Watercraft, and Hidea Power Machinery, collectively accounting for the majority of global revenue.