- LED & Lighting (Optoelectronics)

- LED Work Light Market

LED Work Light Market Size, Share, and Growth Forecast 2026 - 2033

LED Work Light Market by Product (Flashlight, Spotlight, Clamplight, Lantern, Others), Operation (Battery Operated, Plug-in) End-use (Residential, Commercial & Institutional, Industrial), Sales Channel (Direct Sales, Retail Outlets, Online), and Regional Analysis, 2026 - 2033

LED Work Light Market Size and Trend Analysis

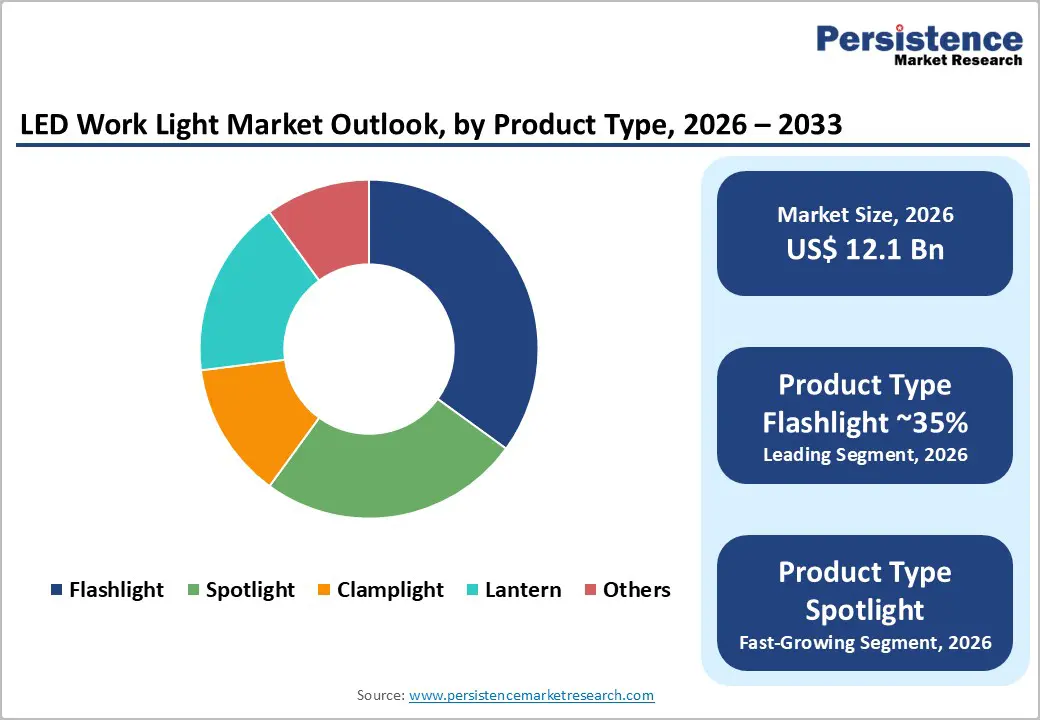

The global LED work light market size is projected to reach US$ 12.1 billion in 2026 and reach US$ 16.0 billion by 2033, registering a CAGR of 4.1% during the forecast period from 2026 to 2033. This growth is driven by the increasing demand for energy-efficient, high-lumen lighting solutions across industrial, construction, and commercial sectors.

Rising emphasis on worker safety and operational efficiency has fueled the adoption of durable, explosion-proof, and cordless work lights. Supportive government regulations, such as the DOE standards in the U.S. and similar EU directives, alongside the expansion of cordless power tool ecosystems by brands like Milwaukee and DeWalt, further propel market growth.

Key Market Highlights:

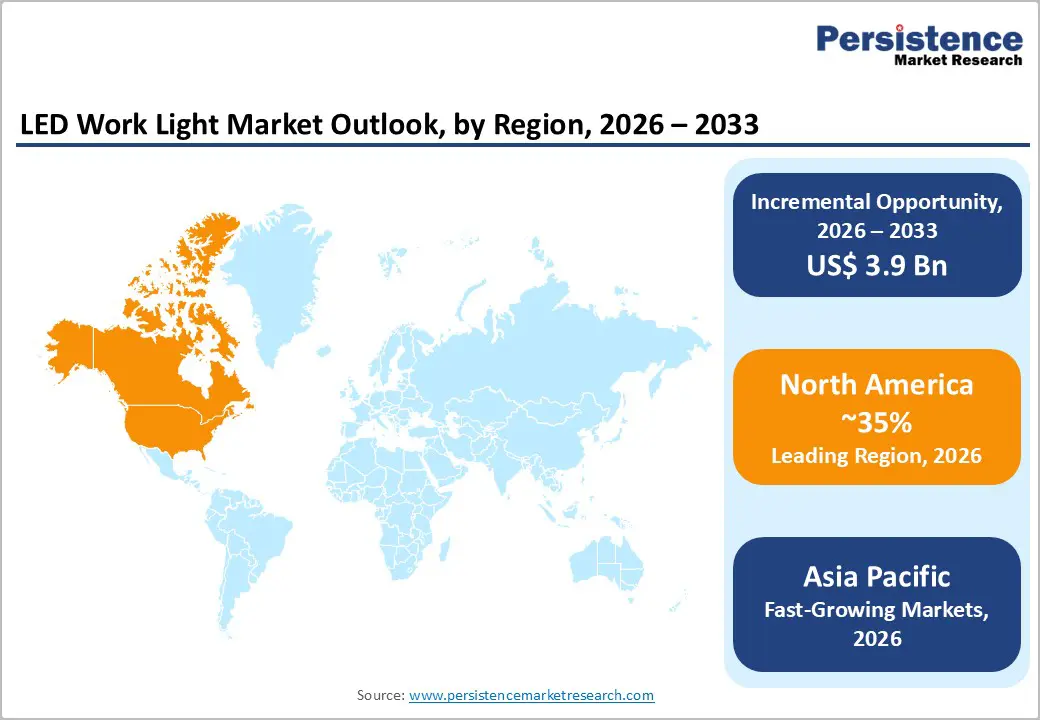

- Leading Region: North America leads the global LED Work Light Market, accounting for approximately 35% of revenue in 2026, driven by strict OSHA regulations and high adoption of cordless tool ecosystems among professional contractors.

- Fastest Growing Region: Asia Pacific is the fastest-growing market, capturing around 28% of revenue by 2026, supported by rapid industrialization, large-scale infrastructure projects, and rising adoption of energy-efficient LED solutions in construction, mining, and automotive sectors.

- Dominant Segment: Battery-operated LED work lights dominate with a 62% market share, favored for portability, interoperability with lithium-ion tool batteries, and long runtimes across industrial and professional applications.

- Fastest Growing Segment: Industrial end-use is expanding rapidly, accounting for 45% of revenue, driven by automation, continuous high-intensity lighting needs, and demand for hazardous location-compliant solutions.

- Key Market Opportunity: Integration of IoT-enabled smart controls, remote monitoring, and asset management features presents a significant opportunity for high-margin, value-added lighting solutions.

| Key Insights | Details |

|---|---|

|

LED Work Light Market Size (2026E) |

US$ 12.1 Billion |

|

Market Value Forecast (2033F) |

US$ 16.0 Billion |

|

Projected Growth CAGR (2026-2033) |

4.1% |

|

Historical Market Growth (2020-2025) |

3.5% |

Market Dynamics

Drivers - Expansion of Cordless Power Tool Ecosystems Driving Adoption of LED Work Lights

The growing integration of LED work lights into universal lithium-ion battery platforms is significantly accelerating market growth. Leading players like Techtronic Industries (Milwaukee) and Stanley Black & Decker have designed proprietary systems (M18, 20V MAX) that are compatible across hundreds of tools, including high-performance work lights. This interoperability reduces the need for multiple power sources, lowers total ownership costs, and encourages tradespeople to purchase "bare tool" lights to complement existing toolkits.

Advancements in battery density and efficiency now enable LED work lights to operate for over 12 hours on a single charge, ensuring continuous illumination at remote construction sites or areas without grid access. The portability, long runtime, and compatibility with power tool ecosystems make these lights indispensable for professional contractors and DIY enthusiasts, driving consistent volume growth globally.

Impact of Stringent Occupational Safety Standards on LED Work Light Demand

Stringent workplace safety regulations enforced by organizations such as OSHA and the International Electrotechnical Commission (IEC) are compelling industries to modernize their lighting infrastructure. Poor illumination is a leading contributor to slip, trip, and fall incidents, while LED work lights provide superior Color Rendering Index (CRI) and uniform lumen output, enhancing visibility and reducing eye strain compared to halogen or fluorescent alternatives.

In hazardous environments like mining, oil, and gas, the rising demand for ATEX and IECEx-certified explosion-proof LED work lights underscores their importance. Operating at lower temperatures, these lights significantly reduce the risk of igniting flammable gases or dust, ensuring worker safety and regulatory compliance. The combination of high performance, durability, and safety certifications is driving adoption across industrial and commercial sectors worldwide.

Restraints - High Initial Procurement Costs Limiting Adoption of Industrial-Grade LED Work Lights

Despite offering long-term energy savings and lower maintenance costs, the upfront investment required for industrial-grade LED work lights remains a key barrier, particularly for small and medium-sized enterprises (SMEs). Advanced units with thermal management systems, impact-resistant polycarbonate lenses, and IP67-rated enclosures command a premium compared to conventional halogen or fluorescent fixtures.

For budget-constrained contractors and residential users, this cost difference often delays the transition to LED technology. Although prices are gradually declining, the premium associated with “smart” and connected LED variants continues to challenge mass adoption in developing regions, where initial capital expenditure is a critical decision driver.

Vulnerability to Global Supply Chain Disruptions Restricts Market Growth

The production of LED work lights is heavily reliant on global electronic component supply, including semiconductors, rare earth elements for LED chips, and lithium-ion batteries. Geopolitical tensions, trade restrictions, or raw material shortages can create price volatility and production delays, impacting profit margins and delivery schedules for manufacturers.

Dependence on key manufacturing hubs in East Asia for components such as driver circuits and heat sinks exposes the market to logistic bottlenecks. Any disruption in these critical supply chains can result in inventory shortages, price spikes, and delayed project timelines, slowing market expansion and limiting manufacturers’ ability to meet growing industrial and commercial demand.

Opportunity - Integration of Smart IoT-Enabled Technologies Unlocking New Revenue Streams

The convergence of LED work lighting with Internet of Things (IoT) technologies presents a significant growth opportunity for market leaders. Smart work lights equipped with Bluetooth or Wi-Fi connectivity enable remote control of intensity, scheduling, and battery monitoring via mobile applications. Innovations such as Milwaukee Tool’s ONE-KEY technology allow asset tracking and tool customization, enhancing operational efficiency and theft prevention on large commercial and institutional job sites.

Adoption of app-enabled diagnostics, remote fleet management, and automated scheduling allows facility managers to efficiently manage hundreds of lighting units, reducing manual oversight and downtime. Manufacturers investing in these connected solutions are well-positioned to secure high-value contracts and differentiate their portfolios in a rapidly digitizing industrial landscape.

Rising Demand for Explosion-Proof LED Work Lights in Hazardous Industrial Environments

Specialized niche markets such as underground mining, chemical processing, and offshore drilling are driving demand for intrinsically safe, explosion-proof LED work lights. These environments require lighting that withstands extreme vibration, corrosive atmospheres, and potential explosive hazards, while ensuring worker safety.

As global energy and infrastructure projects expand into deeper and harsher conditions, the need for Class I, Division 1-compliant, robust LED work lights is escalating. Companies like Larson Electronics and Streamlight Inc., focusing on rugged, failure-proof lighting solutions, are well-positioned to capture substantial market share by serving high-risk industrial sectors that prioritize safety and reliability over cost.

Category-wise Analysis

Industrial End-use Analysis

The Industrial segment is projected to command the largest share of the LED Work Light Market, accounting for approximately 45% of total revenue by 2026. This dominance stems from the extensive application of work lights in manufacturing plants, automotive repair shops, and large-scale infrastructure projects, where continuous, high-intensity illumination is essential across multiple shifts.

The energy efficiency of LED technology reduces operational costs, while Industry 4.0 adoption and smart factory initiatives fuel demand for reliable, maintenance-free lighting. LEDs’ resistance to vibration, impacts, and harsh industrial environments further solidifies their preference among operators, making them the standard solution for heavy machinery, assembly lines, and industrial maintenance operations.

Battery Operated Analysis

The Battery Operated segment is expected to dominate with around 62% market share, reflecting a major industry shift from corded to cordless solutions. Advances in Lithium-Ion battery technology have enabled high-output floodlights and spotlights to deliver long runtimes without grid dependency, ensuring mobility and operational flexibility.

Sectors such as emergency response, utility maintenance, and remote construction particularly benefit from cordless designs, while the ability to swap batteries across tools fosters brand loyalty and recurring purchases. Enhanced portability, combined with extended runtime and compatibility with power tool ecosystems, ensures that battery-operated LED work lights remain the forefront driver of market growth in the portable lighting category.

Flashlight Product Type Analysis

The Flashlight segment accounts for an estimated 35% of total volume, reflecting its ubiquitous presence across residential, commercial, and industrial applications. From pocket-sized inspection lights for HVAC technicians to heavy-duty tactical units for law enforcement, flashlights remain essential tools for professional and recreational use.z

LED technology enables compact, high-lumen designs, replacing bulky incandescent predecessors while offering features such as rechargeable batteries, waterproofing, and tactical-grade construction. Steady demand from sectors including camping, hiking, and on-site professional applications ensures the flashlight segment maintains a consistent revenue stream and strong market penetration.

Retail Outlets Sales Channel Analysis

Retail outlets represent the leading sales channel, contributing approximately 48% of global sales. Big-box retailers like The Home Depot, Lowe’s, and industrial distributors play a critical role in product availability, allowing customers to inspect quality and brightness before purchase.

Immediate availability for urgent job-site needs, combined with strategic in-store displays, brand partnerships, and bundled offers, drives both professional and DIY purchases. The tactile experience, product demonstrations, and impulse-buy potential ensure that retail channels remain the primary route to market, outperforming online distribution for time-sensitive and high-investment LED work light products.

Regional Insights

North America LED Work Light Market Trends

North America is projected to remain the largest regional market, accounting for approximately 35% of global revenue by 2026. Growth is fueled by a robust construction sector, a strong DIY culture, and stringent workplace safety regulations enforced by OSHA, which mandate adequate illumination in construction and industrial environments. Industrial and commercial operators increasingly prefer durable, high-performance LED work lights that can withstand vibration, impacts, and extreme weather conditions.

Major players like Milwaukee Tool and DeWalt drive innovation in connected, modular, and battery-compatible lighting solutions, enhancing interoperability across tool platforms. Additionally, government-funded infrastructure modernization and smart city initiatives sustain demand for portable and stationary LED work lights, ensuring the region remains a high-value market for professional contractors and industrial buyers.

Europe LED Work Light Market Trends

Europe holds a significant share in the global LED work light market, with a projected CAGR of 4.5% between 2026 and 2033. The region’s growth is driven by strict energy efficiency directives, sustainability mandates, and industrial safety regulations, prompting industries to adopt eco-friendly, high-CRI LED lighting. Countries such as Germany, the U.K., and France emphasize premium quality, ergonomic design, and certified performance, favoring established European brands like Ledlenser and Hella.

Industrial, automotive, and manufacturing sectors invest heavily in certified work lights to ensure precision, worker safety, and operational efficiency. The combination of regulatory enforcement and demand for durable, high-performance solutions has created a stable and mature market environment, with gradual adoption of advanced smart lighting technologies further supporting long-term growth.

Asia Pacific LED Work Light Market Trends

Asia Pacific is expected to be the fastest-growing regional market, accounting for approximately 28% of global revenue by 2026. Rapid industrialization, urbanization, and large-scale infrastructure projects in China, India, and ASEAN countries are driving demand for cost-effective, high-output LED work lights. Sectors such as construction, mining, and automotive repair are transitioning from traditional halogen fixtures to energy-efficient LEDs due to durability and operational cost benefits.

China’s role as a global manufacturing hub for LED components ensures competitive pricing and broad product availability, while rising domestic consumption and awareness of energy conservation further accelerate adoption. The combination of expanding industrial activities, infrastructure modernization, and growing urban populations positions the region as a high-growth market for portable and fixed LED work lighting solutions.

Competitive Landscape

The LED Work Light Market is moderately fragmented, with a mix of global power tool manufacturers and specialized lighting companies. Competition is intense, driven by factors such as battery platform compatibility, lumen-per-watt efficiency, durability, and runtime performance. Companies increasingly focus on innovation and product differentiation to capture both professional and industrial segments, while maintaining brand loyalty and extensive distribution networks.

Market strategies are shifting toward ecosystem integration, designing work lights that operate exclusively with proprietary battery systems to secure long-term customer retention. Additionally, mergers, acquisitions, and strategic alliances are employed to access advanced LED, battery, and smart connectivity technologies, enhancing competitive positioning and market share.

Key Market Developments

- In October 2024, Milwaukee Tool (Techtronic Industries) launched the new M18 Service Area Light and Pivoting Area Light, expanding their lighting solutions with USB charging capabilities and high-definition output for versatile job site use.

- In January 2024, Makita Corporation introduced new 40V max XGT Cordless Underhood Work Lights, designed specifically for automotive mechanics requiring powerful, adjustable illumination without the hassle of cords.

- In May 2024, Larson Electronics released a new explosion-proof LED drop light equipped with a paint spray gun cover, targeting safety-critical applications in hazardous industrial painting and coating environments.

Companies Covered in LED Work Light Market

- Milwaukee Tool

- DeWalt

- Bosch Professional

- Makita Corporation

- Snap-on Incorporated

- Ledlenser GmbH

- Streamlight Inc.

- Cooper Lighting

- CAT Licensed Lights

- Hella GmbH & Co. KGaA

- Vision X Lighting

- Larson Electronics LLC

- Baja Designs

- Nilight

- Aurora Lighting

Frequently Asked Questions

The global LED work light market is forecast to reach US$ 16.0 Billion by 2033, growing at a CAGR of 4.1% from 2026.

Key drivers include the widespread adoption of cordless battery platforms, strict industrial safety regulations, and the superior energy efficiency of LED technology over traditional lighting.

The Battery Operated segment dominates with around 62% market share, driven by portability, rechargeable lithium-ion batteries, and compatibility with power tools.

North America leads with approximately 35% of global revenue, supported by a strong contractor base, DIY culture, and strict workplace illumination standards.

Developing smart connected lights with Bluetooth control and explosion-proof fixtures for hazardous industries presents significant growth opportunities.