- Food Ingredients & Additives

- Industrial Sugar Market

Industrial Sugar Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Industrial Sugar Market by Product Type (White/Refined Sugar, Brown Sugar, Liquid Sugar / Sugar Syrups), Source (Sugarcane, Sugar Beet), by Form (Solid, Liquid), End-user (Food & Beverage, Pharmaceuticals, Personal Care & Cosmetics, Foodservice, Animal Feed & Pet Food, Others), and Regional Analysis from 2025 to 2032

Industrial Sugar Market Share and Trends Analysis

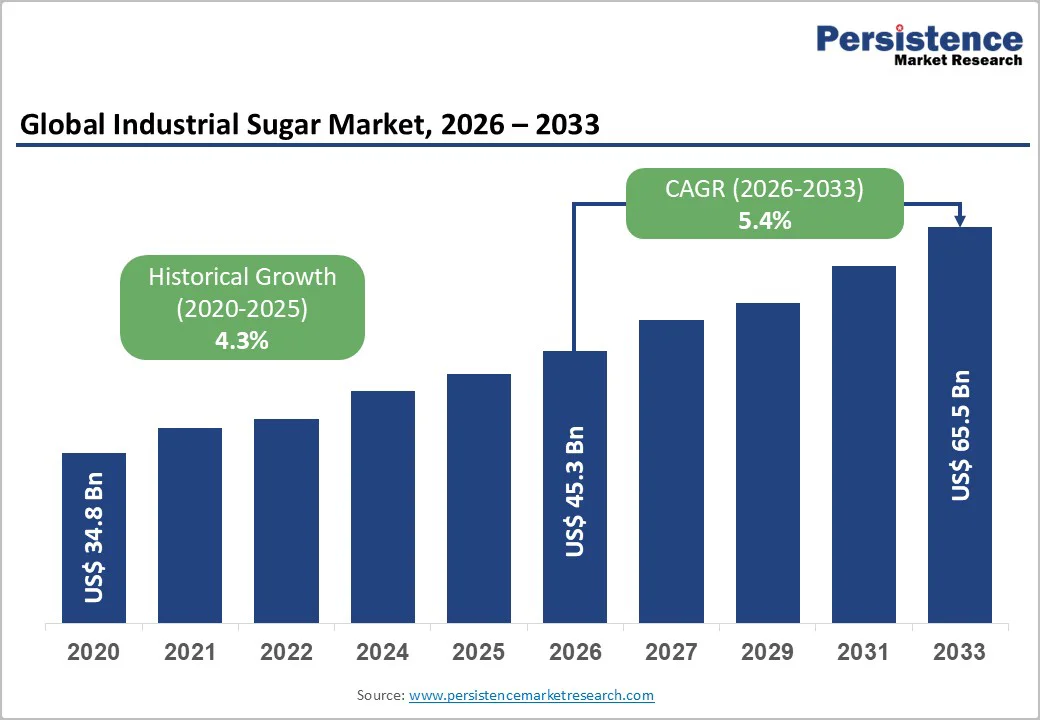

The global industrial sugar market is projected to be valued at US$45.3 billion in 2026 and reach US$65.5 billion by 2033.

The market is projected to record a CAGR of 5.4% from 2026 to 2033. Industrial sugar remains the backbone of confectionery, bakery, and beverage production, with rising global demand driven by indulgent treats, functional beverages, and export-oriented baked goods.

The market is witnessing dynamic shifts as liquid sugar formats gain traction, alternative sweeteners emerge, and regional production hubs invest in advanced refining technologies.

Key Industry Highlights

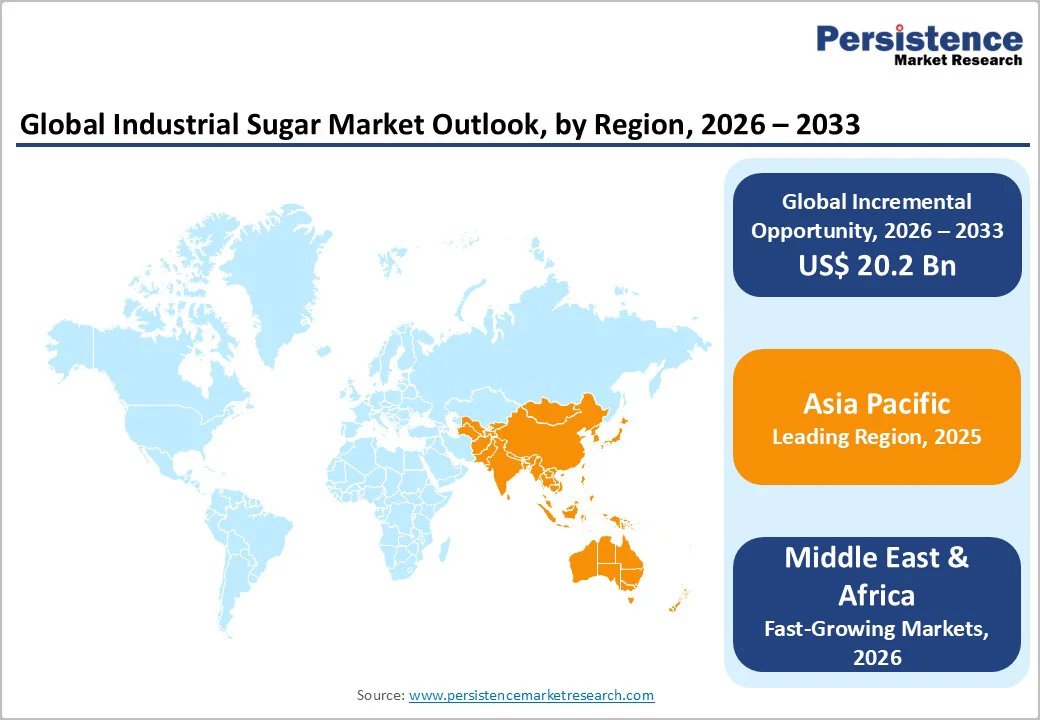

- Leading Region: Asia Pacific, holding 41% market share, driven by expanding confectionery, bakery, and beverage manufacturing, along with the modernization of processing facilities.

- Fastest-Growing Region: Middle East & Africa, fueled by increasing demand for liquid sugar, premium chocolates, and functional bakery products, coupled with investments in refining technologies and supply chain efficiency.

- Fastest-Growing Segment: Liquid Sugar / Sugar Syrups, favored for instant solubility, precise blending, and compatibility with automated production lines.

- Market Drivers: Growth in confectionery and chocolate production accelerates the use of industrial-grade sugar, supporting consistent quality and shelf-stable products.

- Opportunities: Growth in bakery ingredient exports creates long-term B2B partnerships, customized sugar blends, and cross-border logistics solutions.

- Key Developments: In November 2025, India approved exports of 1.5 billion tonnes of sugar for 2025. The UK extended its sugar tax to include bottled milkshakes, pre-packaged lattes, and more fizzy drinks.

| Key Insights | Details |

|---|---|

| Industrial Sugar Market Size (2026E) | US$45.3 Bn |

| Market Value Forecast (2033F) | US$65.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Growth of Confectionery and Chocolate Production Accelerates Industrial-Grade Sugar Usage

A sweet surge in global confectionery and chocolate production is propelling demand for industrial-grade sugar at an accelerated pace. As manufacturers scale up candy, chocolate, and bakery lines, the need for consistent, high-purity sugar with predictable crystallization and solubility properties becomes critical.

Industrial sugar ensures uniform texture, sweetness, and shelf stability across diverse products, supporting innovations such as filled chocolates, premium bars, and sugar-based confections. Rising consumer preference for indulgent treats and seasonal specialties further strengthens adoption in large-scale production facilities.

Confectionery brands are also exploring specialty sugars, such as fine granulated or invert forms, to optimize taste and processing efficiency. This dynamic growth in the sweet goods sector is fueling robust upstream industrial sugar demand worldwide.

Restraints - Rapid Adoption of Alternative Sweeteners, Stevia, and Sugar Alcohols

The rising popularity of alternative sweeteners, including stevia, monk fruit extracts, and sugar alcohols, is reshaping the industrial sugar landscape and acting as a notable restraint. Food and beverage manufacturers are increasingly formulating low-calorie, reduced-sugar, and “better-for-you” products to meet health-conscious consumer demand, reducing reliance on traditional refined sugar.

These substitutes offer functional benefits such as glycemic control and clean-label positioning, making them attractive in confectionery, beverages, and bakery applications. As a result, industrial sugar producers face pressure on volumes and pricing.

The shift toward natural and plant-based sweeteners is especially pronounced in emerging markets and premium product segments, forcing large-scale sugar processors to explore diversification or value-added specialty sugar solutions to sustain competitiveness.

Opportunity - Growth in Bakery Ingredient Exports Creates Opportunities for Large-Scale Sugar Processors

A surge in bakery ingredient exports is opening high-value opportunities for large-scale industrial sugar processors worldwide. As international demand for premixes, sweet doughs, and specialty baked goods rises, manufacturers require reliable, bulk-quality sugar that ensures consistency, sweetness balance, and processing efficiency.

This trend enables sugar producers to establish long-term supply contracts with exporters, co-develop customized sugar blends, and expand into high-volume, cross-border logistics solutions. Startups can capitalize on niche segments by offering traceable, single-origin, or specialty sugar variants tailored for export-oriented bakeries and confectioners.

With global trade in bakery ingredients accelerating, processors that integrate quality assurance, scalable production, and export compliance gain a strategic advantage, strengthening revenue streams and market positioning in the international industrial sugar landscape.

Category-wise Analysis

By Product Type Insights

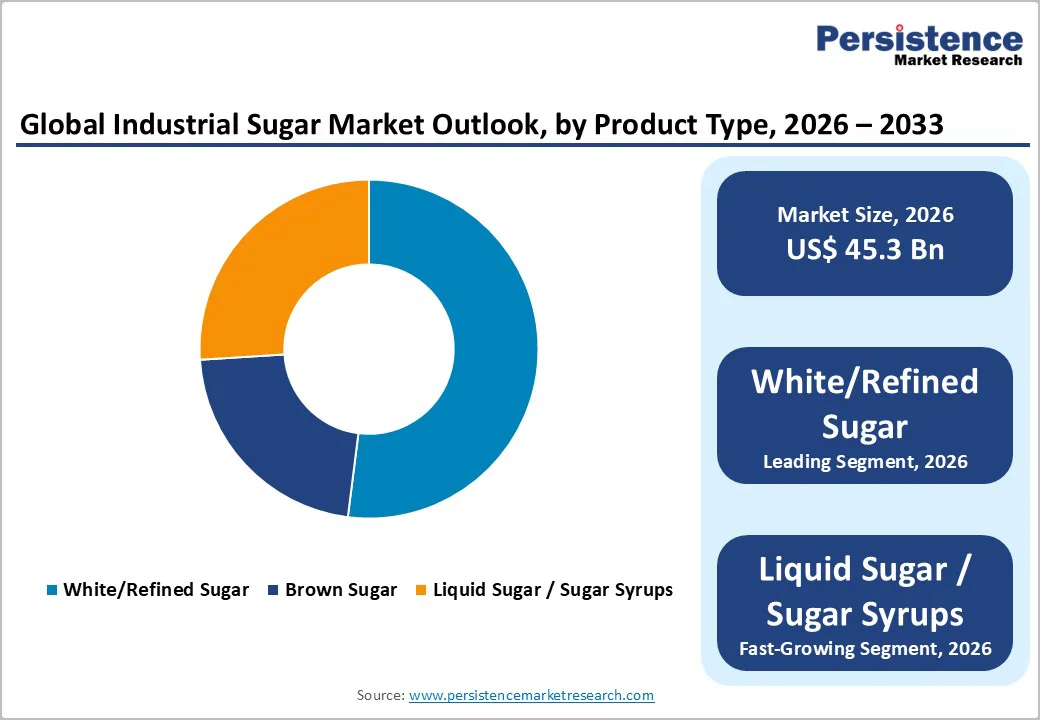

White/Refined sugar holds approx. 52% market share as of 2025, reflecting its dominant role in the global industrial sugar market due to widespread applicability, predictable sweetness, and high solubility across confectionery, bakery, and beverage processing. Its consistent quality and ease of handling make it the preferred choice for large-scale manufacturers seeking uniform product performance and scalable production.

Brown sugar is ideal for applications that require richer flavor profiles, caramel notes, and moisture retention, supporting artisanal baked goods and specialty confections. Liquid sugar and sugar syrups offer rapid dissolving and precise blending, making them ideal for beverages, sauces, and processed foods where consistency and process efficiency are critical.

Across product segments, refined sugar remains the backbone of industrial formulations worldwide.

Liquid Sugar / Sugar Syrups Insights

Liquid sugar/sugar syrups are projected to achieve a CAGR of 6.7% during the forecast period, driven by increasing demand for ready-to-use sweeteners in beverages, sauces, and processed foods. Its ability to dissolve instantly and blend uniformly makes it highly attractive for large-scale manufacturers seeking efficiency, consistency, and reduced production time.

Functional applications, including flavored drinks, dairy-based beverages, and liquid bakery fillings, are further expanding their adoption. The rise of automated production lines and cold-processing techniques has increased reliance on liquid formats to minimize handling complexity and dosing errors.

While white and brown sugars dominate traditional uses, liquid sugar’s convenience, precise control, and compatibility with continuous processes position it as a high-growth segment for industrial applications.

Region-wise Insights

Asia Pacific Industrial Sugar Market Trends

Asia Pacific is the dominant market, accounting for 41% of total market share, driven by rapid growth in processed foods, confectionery, and beverage manufacturing across the region. In China, industrial sugar demand is fueled by expanding ready-to-drink beverages, bakery products, and functional sweets, with manufacturers seeking consistent quality and bulk supply.

India is witnessing strong uptake in sugar syrups and liquid sweeteners for modern bakeries and large-scale confectionery operations. Japan emphasizes high-purity sugar for premium chocolate, desserts, and beverages, with processors adopting advanced refining and automated dosing systems.

Indonesia shows rising interest in liquid sugar for soft drinks and traditional sweet products, supporting industrial efficiency. Across the region, investment in modern processing technologies and export-oriented production is shaping market growth and product diversification.

Middle East & Africa Industrial Sugar Market Trends

Middle East & Africa Industrial Sugar Market is expected to grow at a CAGR of 8.8%, supported by rising demand from confectionery, bakery, and beverage sectors across key countries. In Saudi Arabia, large-scale food manufacturers are increasingly integrating liquid sugar and syrups to streamline the production of soft drinks and packaged sweets.

The UAE is witnessing growth in premium chocolate and dessert segments, driving consistent demand for high-purity refined sugar. South Africa emphasizes modern bakery operations and functional beverage formulations, boosting industrial sugar usage.

Regional trends also include investments in efficient refining technologies, bulk storage solutions, and supply chain modernization to support both domestic consumption and export markets. Increasing urbanization and evolving consumer taste preferences continue to reinforce industrial sugar adoption across the MEA region.

Competitive Landscape

The global industrial sugar market exhibits a moderately consolidated structure, with leading producers leveraging scale, technological advancement, and supply chain control to maintain competitiveness.

Key players are investing in advanced refining and crystallization technologies to improve yield, consistency, and energy efficiency. R&D efforts focus on developing specialty sugar grades, liquid sugar solutions, and clean-label formulations that meet evolving consumer and B2B requirements.

Companies are expanding partnerships with bakeries, confectioners, and beverage manufacturers to secure long-term contracts and enhance market penetration. Regulatory compliance, government subsidies for sugarcane and beet cultivation, and initiatives to increase crop yields shape operational strategies.

Sustainability programs, digital traceability, and energy-efficient processing units further differentiate industry leaders and strengthen their position in global supply chains.

Key Industry Developments:

- In November 2025, India authorized the export of 1.5 billion tonnes of sugar for the 2025 - marketing year, marking a strategic supply decision ahead of the new season. The approval follows industry calls for a higher minimum support price as producers navigate cost pressures and shifting market dynamics.

- In November 2025, the UK announced an extension of its sugar tax to include bottled milkshakes, pre-packaged lattes, and a broader range of fizzy drinks. The move reflects a renewed government push to address rising childhood sugar consumption and escalating public-health concerns.

Companies Covered in Industrial Sugar Market

- Südzucker AG

- Nordzucker AG

- Tereos Group

- British Sugar plc

- Cosan S.A.

- Wilmar International Limited

- Mitr Phol Group

- Illovo Sugar Africa

- Thai Roong Ruang Sugar Group

- American Sugar Refining, Inc.

- Others

Frequently Asked Questions

The global industrial sugar market is projected to be valued at US$ 45.3 Bn in 2026.

Rising production of confectionery and chocolate is boosting demand for industrial-grade sugar, driving growth in the global industrial sugar market.

The global industrial sugar market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Expanding bakery ingredient exports present significant growth opportunities for large-scale sugar processors.

Major players in the global Industrial Sugar market include Südzucker AG, Nordzucker AG, Tereos Group, British Sugar plc, Cosan S.A., Wilmar International Limited, American Sugar Refining, Inc., and others.