- Off-Road Equipment & Machinery

- Agricultural Equipment Market

Agricultural Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Agricultural Equipment Market by Product Type (Power Weeder, Rotavators, Threshers & Dehuskers, Power Tillers, Tractors, Plough, Baler, Seed Drill, Others), by Application (Harvesting & Threshing, Weed Cultivation, Plant Protection, Post-harvest & Agro-processing, Land Development & Seed Bed Preparation, Others), by Regional Analysis, 2026 - 2033

Agricultural Equipment Market Size and Trend Analysis

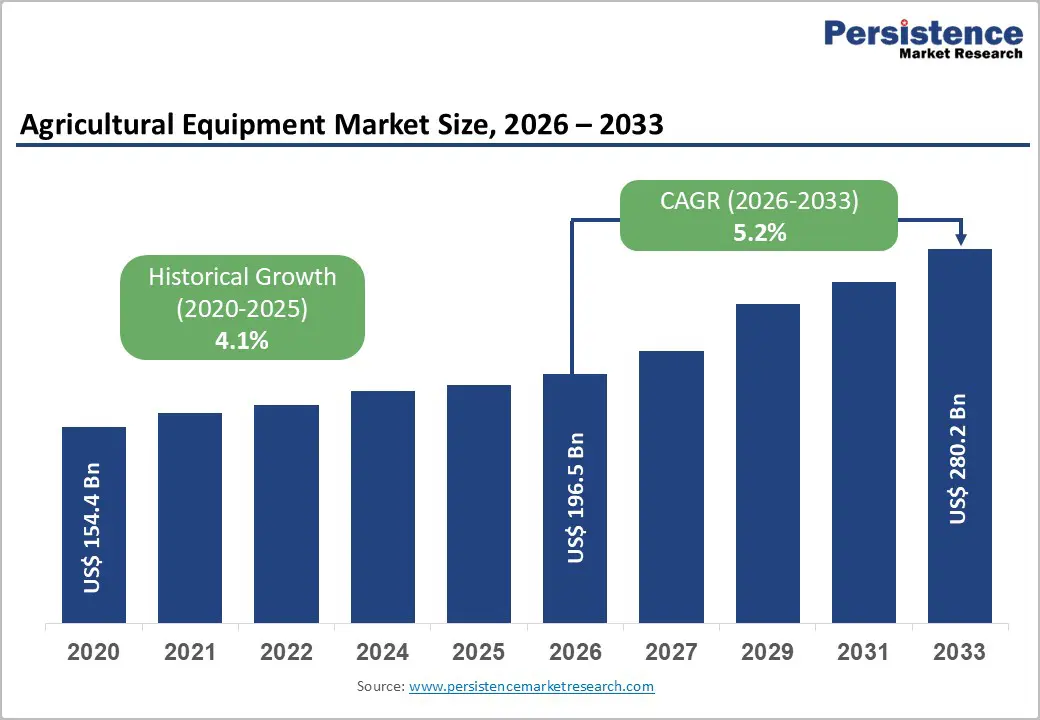

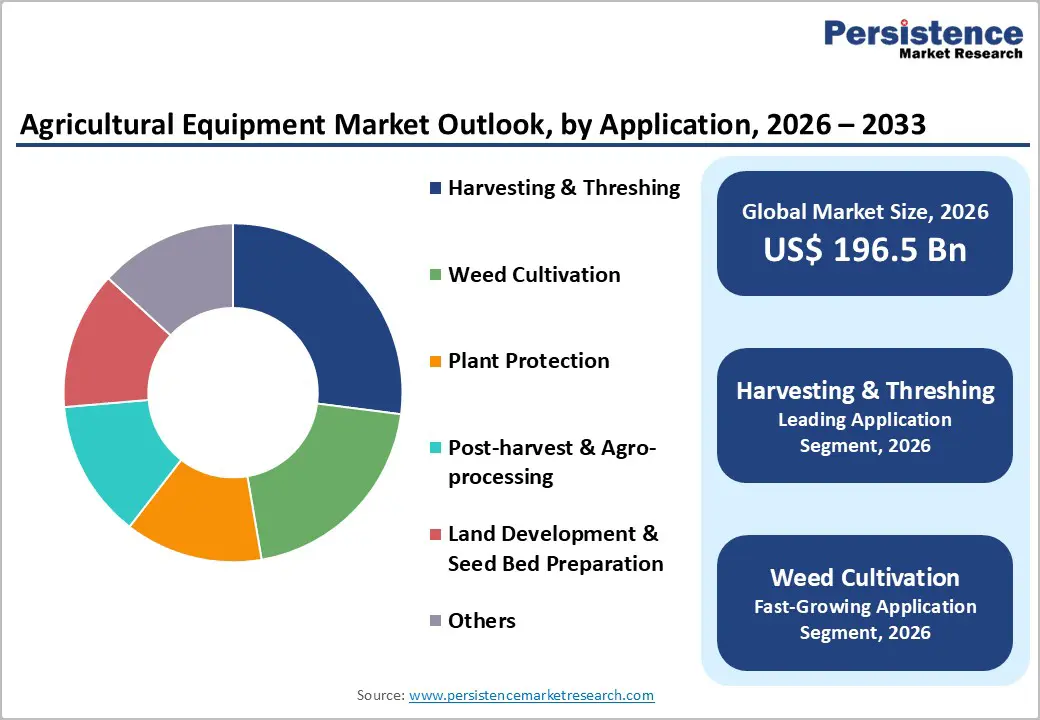

The global agricultural equipment market size is expected to be valued at US$ 196.5 billion in 2026 and projected to reach US$ 280.2 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

The growth is driven by rising demand for farm mechanization, fueled by labor shortages and the need to increase food production to meet global demand. Government initiatives, such as India’s Pradhan Mantri Kisan Samman Nidhi scheme and China’s agricultural modernization policies, are supporting equipment adoption. Additionally, technological advancements in precision agriculture are enhancing operational efficiency, cutting labor requirements by up to 50% per acre, while improving productivity and sustainability across farms worldwide.

Key Market Highlights:

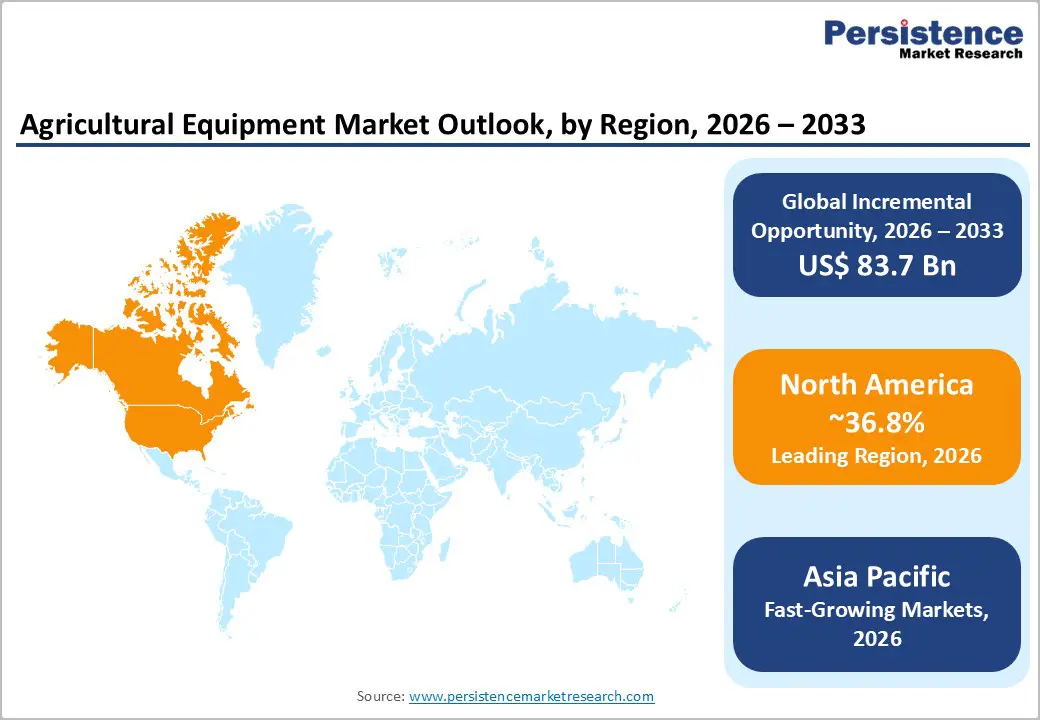

- Leading Region: North America leads the Agricultural Equipment market with 36.8% share (2025), supported by advanced mechanization and precision farming adoption.

- Fastest-Growing Region: Asia Pacific holds 34.5% share (2025) and remains the fastest-growing region, driven by subsidies, labor shifts, and rapid farm modernization.

- Leading Product Category: Tractors dominate the Product Type segment with ~36% share (2025) due to their versatility in plowing, hauling, and seeding operations.

- Leading Application Category: Harvesting & Threshing leads applications with ~46% share (2025), addressing labor shortages and improving yield efficiency.

- Key Growth Opportunity: Precision agriculture technologies, including AI-enabled and autonomous equipment, are creating strong expansion opportunities across emerging mechanized farming markets.

| Key Insights | Details |

|---|---|

| Agricultural Equipment Size (2026E) | US$ 196.5 Billion |

| Market Value Forecast (2033F) | US$ 280.2 Billion |

| Projected Growth CAGR(2026-2033) | 5.2% |

| Historical Market Growth (2020-2025) | 4.1% |

Market Dynamics

Drivers

Rising Farm Mechanization Due to Labor Shortages and Efficiency Needs

Global farm mechanization is accelerating as rural labor forces shrink and wages rise, pushing farmers to adopt modern machinery for higher efficiency. In India, rural labor migration has spurred tractor sales beyond 390,000 units in 2023, according to government data. Farmers increasingly rely on equipment to maintain productivity and meet growing food demand, driving consistent growth in the Agricultural Equipment market.

Advanced technologies, such as GPS-guided tractors and AI-driven farming solutions in China, allow optimized planting, irrigation, and harvesting processes. This shift reduces manual labor dependency, enhances yields, and supports sustainable agricultural practices. As more regions face labor shortages, mechanization adoption is expected to accelerate further, positively influencing market growth and encouraging investment in precision farming tools.

Government Incentives and Subsidies Supporting Modern Equipment Adoption

Governments worldwide are promoting agricultural equipment adoption through subsidies and supportive policies. In 2023, the European Commission allocated EUR 1 billion via Horizon Europe for sustainable agricultural R&D, covering up to 70% of equipment costs. In Asia-Pacific, initiatives like Japan’s Smart Agriculture Project and India’s machinery subsidies encourage the use of tractors, harvesters, and precision tools, lowering adoption barriers.

These policies not only make advanced machinery more accessible but also align with environmental and efficiency goals, including emissions reduction and resource conservation. By supporting mechanization and modern farming techniques, governments are boosting market demand and helping farmers improve productivity, ensuring long-term growth in the global agricultural equipment market.

Restraints

High Initial Investment Costs Limiting Adoption by Smallholder Farmers

High costs of modern agricultural equipment remain a major barrier, particularly for smallholder farmers in developing regions. Advanced machinery requires significant upfront capital, while maintenance and operational expenses add to lifecycle costs. In Eastern Europe, even with financing options, small farms often struggle to afford tractors and harvesters, limiting market penetration and adoption rates.

Supply chain disruptions further increase equipment prices. For instance, the 2023 global semiconductor shortage delayed John Deere production by six months, raising procurement costs and delivery timelines. Such uncertainties discourage investment, especially among smaller farms, slowing overall market growth despite rising mechanization demand and technological advancements.

Fragmented Land Holdings Restricting Efficient Mechanization

Fragmented farmland, common in Asia and parts of Europe, constrains the adoption of large-scale agricultural equipment. Small plots make it difficult to efficiently use tractors, harvesters, and other machinery, reducing operational efficiency. The FAO highlights that land fragmentation significantly slows mechanization, particularly in densely populated agricultural regions where plot sizes remain below optimal thresholds.

In addition, commodity price fluctuations and market uncertainties make small farmers hesitant to invest in expensive equipment. Limited scalability and lower returns on investment further reduce demand for advanced machinery, constraining market expansion and challenging equipment manufacturers to develop solutions suitable for fragmented or small-scale farms.

Opportunity

Advancements in Precision Agriculture Technologies Driving Market Demand

Precision agriculture offers significant growth opportunities, leveraging GPS, IoT, and autonomous systems to optimize resource use and farm productivity. John Deere’s 2024 autonomous tractor integrates AI for real-time analysis, helping address labor shortages and improve operational efficiency. These technologies enable smarter irrigation, planting, and harvesting, reducing costs while enhancing yields, especially in technologically advanced markets like North America and Europe.

Government support in Asia-Pacific, through subsidies and incentives, encourages the adoption of precision farming equipment. High-tech solutions such as AI-driven tractors, drones, and sensor-based monitoring are creating new demand segments. Manufacturers investing in these technologies can tap into high-value markets and cater to farms seeking automation and efficiency improvements, strengthening their market presence globally.

Emerging Mechanization Opportunities in Developing and Fragmented Markets

Mechanization in emerging markets presents strong revenue potential, particularly for smaller, more affordable equipment like power tillers and compact tractors. In Asia, models under 30 HP dominate due to small and fragmented farmland. Initiatives in India and China, including subsidies and government programs, support equipment adoption, making mechanization feasible for smallholder farmers.

Compact and easy-to-use machinery aligns with local farm conditions, addressing labor shortages and increasing productivity. Manufacturers targeting these regions can leverage cost-effective, durable designs to capture market share. By focusing on localized solutions for fragmented lands, companies can unlock significant growth potential in fast-expanding, underserved agricultural markets across Asia and other developing regions.

Category-wise Analysis

Product Type Insights

Tractors dominate the Product Type segment, holding approximately 36% share in 2025. Their versatility across plowing, hauling, and seeding makes them indispensable, with USDA data indicating use on 85% of U.S. farms. In the Asia-Pacific region, tractors remain central to mechanization efforts, particularly 30.1–70 HP models in India and China. Their widespread adoption reflects reliability, efficiency, and adaptability to diverse farming conditions.

Among emerging product types, autonomous and electric tractors are gaining traction. Compact and specialized machinery, such as power tillers and mini-tractors, is increasingly favored in smallholder farms with fragmented land. These tools enhance operational efficiency, reduce manual labor dependence, and enable precision farming, making them key areas of investment for manufacturers targeting evolving market demands and technologically advanced agriculture solutions.

Application Insights

Harvesting and threshing lead the application segment with about 46% share in 2025. Rising labor shortages drive demand for efficient threshers, which minimize crop losses and increase yield consistency. Mechanical threshers account for a good share, reflecting their scalability across different farm sizes and adaptability to staple crops like wheat. The segment’s dominance is supported by mechanization programs in both developed and developing regions.

Faster-growing applications include precision planting, crop protection, and automated irrigation. These areas are increasingly prioritized as farmers adopt smart farming technologies to improve input efficiency, monitor crop health, and optimize resource usage. Mechanized planting systems, drone-based spraying, and sensor-driven irrigation solutions are rapidly expanding, offering new revenue streams and transforming traditional agricultural practices globally.

Regional Insights

North America Agricultural Equipment Market Trends

North America holds a 36.8% share of the global agricultural equipment market, leading in mechanization and advanced technology adoption. Tractors dominate the region, significantly reducing manual labor and boosting productivity across large-scale farms. Precision farming tools, autonomous machinery, and smart irrigation systems are widely implemented, enhancing operational efficiency and resource management. Regulatory frameworks, including emissions and environmental standards, are driving innovation in electric and low-emission equipment. Manufacturers are focusing on sustainable machinery solutions to meet strict compliance requirements while increasing yield and efficiency. The combination of advanced technology adoption and regulatory support ensures North America remains a key high-value market globally.

Europe Agricultural Equipment Market Trends

Europe’s agricultural equipment market is witnessing steady growth, with a CAGR of 5.7% driven by technological adoption and sustainability initiatives. Harmonized regulations across the region promote efficiency, energy conservation, and low-emission machinery. The market is increasingly focused on precision farming, automation, and electric tractors to optimize productivity while reducing environmental impact.

Subsidies, grants, and supportive policies encourage mechanization and modern equipment adoption, especially for large-scale and commercial farms. Manufacturers are innovating in automated harvesters, smart planting systems, and sensor-based monitoring tools to meet evolving farming requirements, positioning Europe as a dynamic market with growing opportunities.

Asia Pacific Agricultural Equipment Market Trends

Asia Pacific holds a 34.5% share of the global agricultural equipment market, reflecting rapid mechanization across small and medium-sized farms. Government incentives, subsidies, and modernization programs are accelerating adoption of tractors, harvesters, and precision tools to meet rising food demand.

Emerging economies in the region prioritize compact, high-efficiency machinery suitable for fragmented farmland. The focus on increasing yields, labor efficiency, and sustainable farming practices is driving demand for modern agricultural equipment, making the Asia Pacific a high-growth region with substantial opportunities for global manufacturers.

Competitive Landscape

The global agricultural equipment market is moderately consolidated, with leading players holding significant market shares through technological innovation and extensive distribution networks. Companies focus on strengthening their presence in high-growth regions, leveraging strategic expansions, collaborations, and localized solutions to capture diverse customer segments.

Research and development investments emphasize precision agriculture, sustainability, and efficiency enhancements. Emerging products integrate autonomous features and electric drives, reflecting the industry’s shift toward smart and eco-friendly solutions. Revenue growth is supported by the adoption of advanced machinery that improves productivity, reduces labor dependency, and meets evolving regulatory and environmental standards across global markets.

Key Developments:

- In November 2025, John Deere unveiled an electric tractor prototype at Agritechnica, highlighting advancements in sustainable farming. This development supports the shift toward low-emission machinery and reinforces innovation in eco-friendly agricultural mechanization solutions worldwide.

- In December 2024, Kubota expanded its compact tiller product lines across Asia, focusing on the needs of small and fragmented farms. This move strengthens its regional presence and supports mechanization growth among smallholder farmers.

- In January 2025, CNH Industrial launched AI-enhanced harvesters designed to improve efficiency and reduce crop losses. The introduction reflects rising adoption of smart farming technologies and supports higher productivity through advanced automation in harvesting operations.

Companies Covered in Agricultural Equipment Market

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- CLAAS Group

- Caterpillar Inc.

- Mahindra & Mahindra Limited

- Yanmar Holdings Co., Ltd.

- SDF Group

- JCB Ltd.

- Lindsay Corporation

- Trimble Inc.

- Raven Industries

- Topcon Positioning Systems

- Kverneland Group

Frequently Asked Questions

The global Agricultural Equipment market is expected to reach US$ 196.5 Billion in 2026.

Rising farm mechanization driven by labor shortages and government support is accelerating demand for modern equipment.

North America leads with 36.8% share in 2025, supported by advanced mechanization and precision farming adoption.

Precision agriculture technologies, including autonomous systems, are creating strong growth potential across emerging markets.

Leading players include Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and CLAAS Group.