- Off-Road Equipment & Machinery

- Farm Equipment Rental Market

Farm Equipment Rental Market Size, Share, and Growth Forecast 2026 - 2033

Farm Equipment Rental Market by Equipment (Tractors, Harvesters, Balers, Sprayers, Others), Power Output (Less than 40 HP, 41 HP to 100 HP, more than 100 HP), Drive Type (Two-wheel Drive, Four-wheel Drive), and Regional Analysis for 2026 - 2033

Farm Equipment Rental Market Size and Trend Analysis

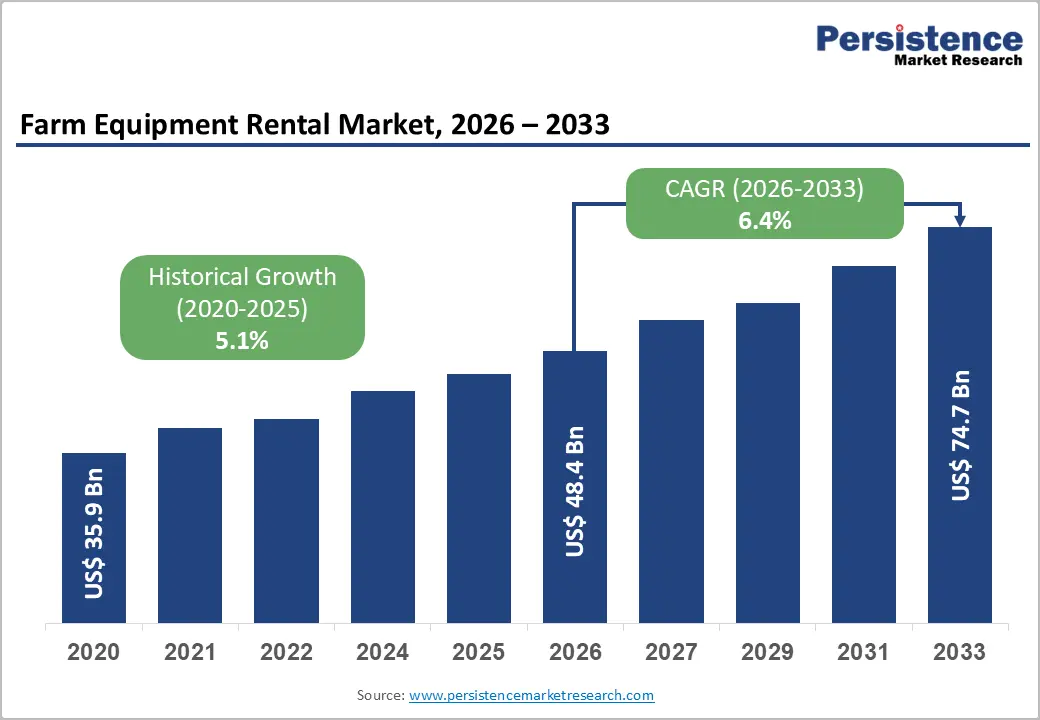

The global Farm Equipment Rental market is valued at US$ 48.4 billion in 2026 and is projected to reach US$ 74.7 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

The sustained growth trajectory of the farm equipment rental market is underpinned by the rise in ownership costs of modern agricultural machinery, accelerating mechanization across emerging economies, and growing awareness of cost-effective rental models. As tractor prices in the U.S. surged by nearly 50% between 2020 and 2023, according to industry data, smallholder and mid-scale farmers increasingly prefer renting over purchasing.

Key Industry Highlights:

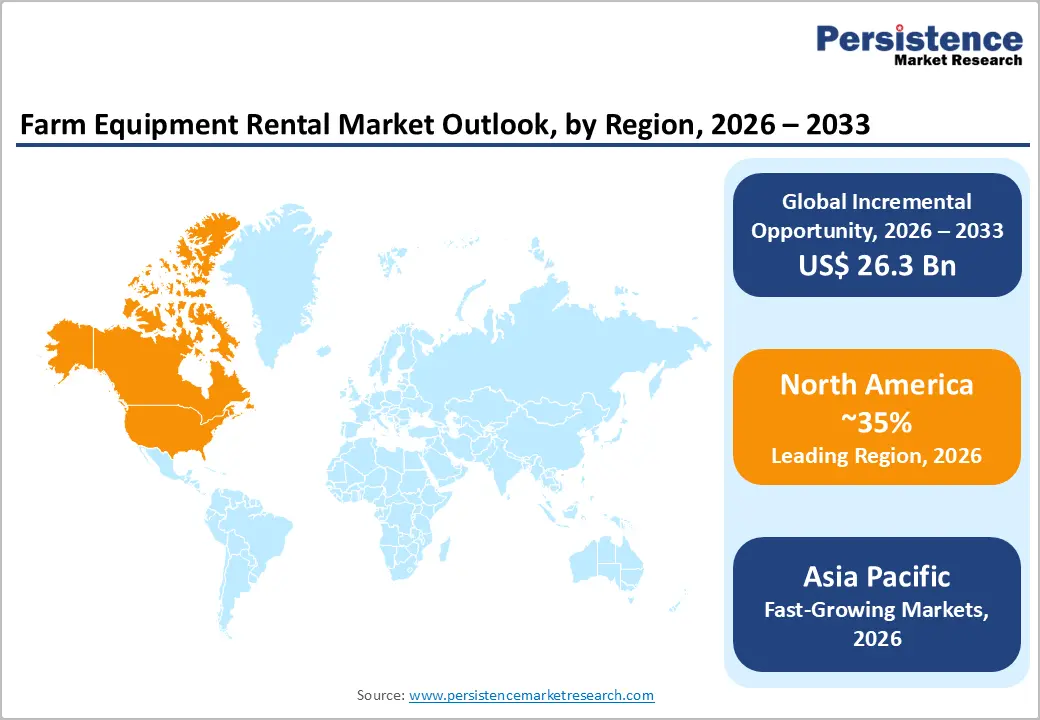

- Leading Region: North America leads the farm equipment rental market, driven by the U.S. agricultural sector's high technology adoption, rising equipment prices, and labor shortages compelling farmers toward flexible rental solutions.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, propelled by India and China's large smallholder populations, government-backed Custom Hiring Centre (CHC) programs, and rising mechanization rates across ASEAN agricultural economies.

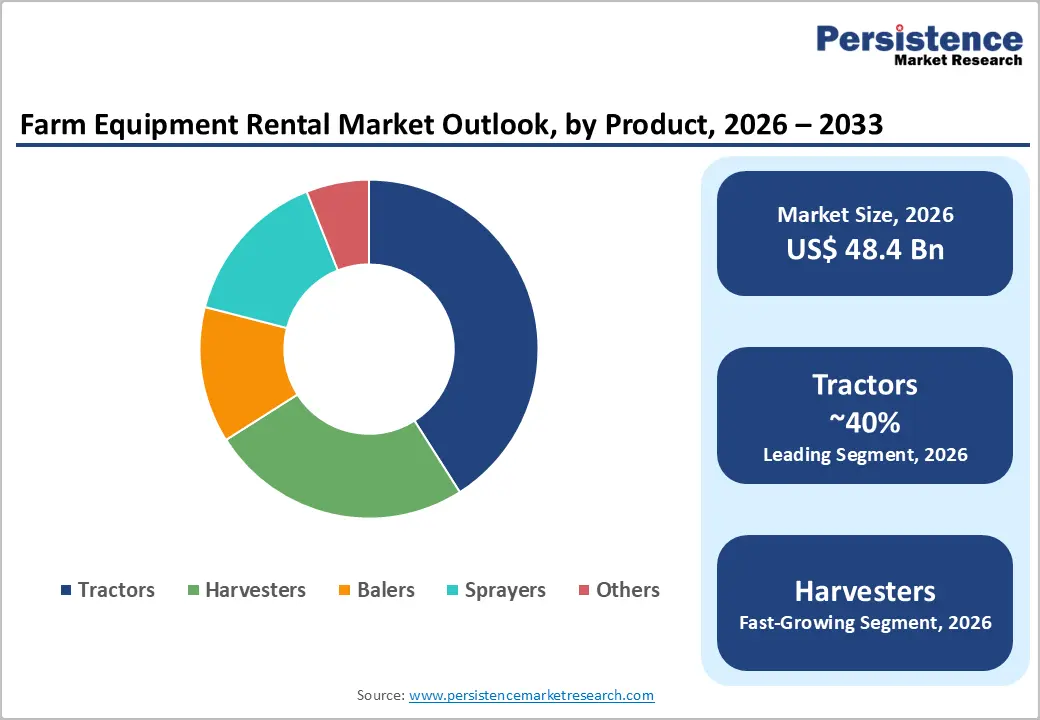

- Dominant Equipment Segment: Tractors dominate the equipment category with approximately 39% share, underpinned by their versatility across all major farming operations and wide applicability across diverse farm sizes and crop types globally.

- Fastest Growing Segment: The Harvesters segment is the fastest-growing equipment category, driven by escalating seasonal labor shortages, rising demand for mechanized crop collection, and integration of AI-powered sorting and harvesting technologies into next-generation rental fleets.

- Key Opportunity: App-based digital rental platforms integrated with GPS, IoT, and AI-enabled equipment present high-margin growth opportunities, particularly in South Asia and Southeast Asia where government subsidies and rising farmer incomes are expanding accessible market scale.

| Key Insights | Details |

|---|---|

|

Farm Equipment Rental Market Size (2026E) |

US$ 48.4 Bn |

|

Market Value Forecast (2033F) |

US$ 74.7 Bn |

|

Projected Growth CAGR (2026–2033) |

6.4% |

|

Historical Market Growth (2020–2025) |

5.1% |

DRO Analysis

Drivers - Rising Cost of Farm Equipment Ownership Accelerating Rental Adoption

One of the most compelling catalysts driving the global farm equipment rental market is the steep and ongoing rise in equipment ownership costs. Modern agricultural machinery integrating GPS, telematics, AI-based precision agriculture, and autonomous navigation systems has seen significant price escalation in recent years. In the United States, tractor list prices rose nearly 50% between 2020 and 2023, driven by precision component integration and supply chain disruptions.

According to the Association of Equipment Manufacturers (AEM), sales of tractors under 100 HP declined by over 14% in the first 10 months of 2024, reflecting that price-sensitive farmers are deferring outright purchases. For small and marginal farmers who constitute over 84% of landholdings in countries like India rental services offer the only viable pathway to mechanization, creating substantial and recurring demand across both developed and emerging markets.

Government Initiatives and Agricultural Mechanization Policies Fuelling Market Growth

Supportive government policies and agricultural mechanization schemes are playing a pivotal role in expanding the farm equipment rental market globally. In India, the Ministry of Agriculture and Farmers Welfare's Sub-Mission on Agricultural Mechanization (SMAM) has distributed over 19.5 lakh machines and established more than 52,000 Custom Hiring Centres (CHCs) as of 2024, subsidizing up to 40–50% of equipment costs for small and marginal farmers.

In the European Union, the Common Agricultural Policy (CAP) provides financial incentives for modernizing farm equipment, while mandating compliance with environmental standards that favour renting newer, lower-emission machinery over operating older purchased units. In Bihar, India, the state government's mobile app-based farm equipment rental platform and the Mukhyamantri Harit Krishi Sanyantra Yojana offer 50% subsidy on machinery rental.

Restraints - Seasonal Demand Volatility and Equipment Unavailability During Peak Periods

One of the most significant constraints impeding the farm equipment rental market is the highly seasonal nature of agricultural operations, which creates acute demand spikes followed by prolonged periods of low utilization. Tractors, harvesters, and sprayers are most intensively required during planting and harvesting windows, placing severe strain on rental fleet capacity. Equipment rental companies frequently struggle to meet concentrated peak demand, resulting in booking backlogs and farmer dissatisfaction.

This imbalance discourages rental adoption, particularly among farmers who require guaranteed equipment access during time-critical operations. Furthermore, extreme weather variability is amplifying unpredictability: industry data indicate that the number of extreme weather events in Europe increased by nearly half between 2021–2022 and 2023–2024, complicating planting and harvesting schedules and exacerbating equipment demand surges.

Infrastructure Deficits and Low Awareness in Rural and Less Developed Regions

Despite growing global adoption, the farm equipment rental market faces notable headwinds in less developed and rural regions due to inadequate physical infrastructure and limited farmer awareness. Poor road connectivity increases logistics costs for transporting heavy machinery to remote farms, while insufficient maintenance infrastructure and shortage of skilled technicians lead to prolonged equipment downtime.

In India, as of 2024, the overall farm mechanization rate stands at only 47% significantly below China at 60% and Brazil at 75%, with the mechanization of harvesting and threshing lagging at merely 34%. Many farmers remain unaware of rental agreements and the tangible cost and productivity benefits of renting, resulting in persistent reliance on traditional ownership models. Overcoming these awareness and infrastructure gaps requires sustained investment and targeted outreach by both governments and private sector participants.

Opportunities - Integration of Precision Agriculture Technology and Autonomous Equipment in Rental Fleets

The convergence of precision agriculture and the rental model presents a high-growth opportunity for market participants. Farmers increasingly seek access to advanced machinery, including GPS-guided tractors, AI-powered harvesters, autonomous sprayers, and drone-based crop monitoring systems but are deterred by the prohibitive upfront costs of ownership. Rental companies that integrate these technologies into their fleets can offer differentiated value propositions, enabling farmers to benefit from precision agriculture without capital commitment.

In September 2024, Kubota North America Corporation acquired Bloomfield Robotics, a startup specializing in AI-based crop health imaging, to enhance predictive maintenance and optimize precision equipment usage. Similarly, Deere & Company's See & Spray technology is expensive to own but rentable at a fraction of the cost, illustrating the untapped revenue potential for technology-enabled rental offerings.

Expansion into Emerging Markets via Digital Rental Platforms and App-Based Services

Digital platforms and mobile-first rental models represent a high-potential growth avenue, particularly in South Asia and Southeast Asia, where smartphone penetration is rising rapidly alongside agricultural mechanization demand. In India, government-supported platforms and private agri-tech ventures have demonstrated the scalability of app-based equipment rental. Trringo, integrated with the Direct Benefit Transfer (DBT) portal, has accelerated subsidy reimbursement cycles and significantly expanded farmer access.

With over 52,000 CHCs already operational and neighbouring countries like Bangladesh and Nepal planning pilot rollouts, the regional opportunity is substantial. In Bihar, a mobile app-based farm equipment rental service was launched specifically for small farmers in July 2022. Companies investing in digital booking systems, IoT-enabled fleet management, and localized last-mile logistics infrastructure are uniquely positioned to build scalable, asset-light rental platforms that capture first-mover advantages in these underpenetrated high-growth markets.

Category-wise Analysis

Equipment Insights

Tractors lead the global farm equipment rental market by equipment type, accounting for approximately 39% of total market revenue in 2025. This dominant position is attributed to the unmatched versatility of tractors across virtually every stage of the agricultural cycle, including tillage, planting, fertilizer application, irrigation, and haulage. Tractors serve as the primary power source for a broad range of attachments and implements, making them indispensable regardless of farm size or crop type.

The wide availability of tractor models across power ranges, from sub-40 HP compact units suited to smallholder farms to 830 HP high-capacity machines for large grain estates, ensures broad market applicability. In February 2024, Deere & Company introduced its new 9RX Series four-track tractors with models reaching up to 830 horsepower, underscoring continued investment in high-performance rental-grade machinery.

Power Output Insights

In the power output segmentation, the 41 HP to 100 HP category holds the leading share of the farm equipment rental market at approximately 47%. This mid-range power bracket is particularly suited to the operational requirements of small and medium-scale farms that constitute most global agricultural holdings. Equipment in this power range, covering most standard tractors and multi-function harvesters, delivers an optimal balance of fuel efficiency, operational versatility, and affordability of rental rates, making it the most widely demanded category across both developed and emerging markets.

In India, government emission norms under TREM Stage IV have driven consumer preference toward 45–50 HP tractor models offering 4WD at a lower cost. In Europe, mid-range equipment meets CAP compliance requirements while addressing diverse crop management needs across the Germany, France, and Spain markets.

Drive Type Insights

The Four-wheel Drive (4WD) segment dominates the drive type category, accounting for approximately 54% of the farm equipment rental market share. Four-wheel drive equipment offers superior traction, load-bearing capacity, and performance across diverse terrain conditions, critical factors for farming operations spanning uneven, waterlogged, or challenging terrain.

The growing adoption of 4WD tractors is particularly pronounced in Europe, where large farm holdings and chronic labour shortages demand high-performance, heavy-duty machinery with over 80% market share in the segment as of 2024, driven by Deere & Company (9R, 6R, 7R series), CNH Industrial (Case IH Magnum, New Holland T9), and AGCO Corporation (Massey Ferguson 8700, Fendt 1000 Vario).

Additionally, the regulatory push toward precision agriculture and autonomous operations disproportionately favors 4WD platforms, given their structural capability to support heavier sensor packages, autonomous navigation systems, and variable-rate application technology.

Regional Analysis

North America Farm Equipment Rental Market Trends

North America represents a technologically advanced and innovation-driven segment of the global farm equipment rental market. The United States leads regional demand, propelled by consistently rising equipment prices with individual tractor models appreciating by nearly 50% between 2020 and 2023 alongside a persistent farm labor shortage that is accelerating mechanization. Over 40% of U.S. farmers report ongoing challenges in sourcing adequate agricultural labor, driving demand for autonomous and precision-capable rental equipment.

In Canada, high interest rates and escalating equipment costs are compelling farmers to transition from ownership to rental models, supported further by drought pressures. The Government of Canada's National Agroclimatic Risk Report highlights that over 90% of farmland in Alberta was affected by drought conditions in recent seasons, reinforcing the economic rationale for flexible, rental-based access to equipment over capital-intensive ownership.

Asia Pacific Farm Equipment Rental Market Trends

Asia Pacific is the fastest growing in the global farm equipment rental market, accounting for approximately 45% of global revenue share projected by 2033. The region's growth is driven primarily by India, China, and Southeast Asia, where large smallholder farm populations, rising rural-to-urban labor migration, and active government mechanization schemes create structural demand for rental services. In India, 86% of farmers hold marginal land (under 2 hectares), making individual ownership of advanced machinery economically unviable.

In China, the government allocated USD 3.5 billion for agricultural machinery subsidies in 2024, driving rapid mechanization adoption. The National Bureau of Statistics of China data confirms that agricultural wages in urban-adjacent farming zones have risen substantially, reinforcing the economic rationale for rental over labor.

Europe Farm Equipment Rental Trends

Europe's farm equipment rental market is shaped by the dual forces of regulatory compliance requirements and the structural evolution of agricultural policy. The European Union's Common Agricultural Policy (CAP) provides substantial financial incentives for adopting efficient and environmentally compliant farming equipment, creating a natural alignment with rental service models that offer access to newer, low-emission machinery. Germany, France, and Spain are key contributors to European rental demand, with large-scale farming operations increasingly preferring 4WD high-horsepower equipment for grain production and viticulture.

Europe also faces heightened climate-related operational risk: extreme weather events on the continent increased by nearly half between 2021–2022 and 2023–2024, with over 16,000 events recorded in 2023–2024 versus approximately 11,000 in the prior period. This climate volatility is reinforcing the preference for rental models, as farmers seek to avoid large capital commitments in a more uncertain operating environment.

Competitive Landscape

The global farm equipment rental market exhibits a moderately fragmented competitive structure, with a handful of large multinational original equipment manufacturers (OEMs) such as Deere & Company, CNH Industrial, and AGCO Corporation coexisting with specialized regional and local rental operators. Leading OEMs leverage their brand equity, extensive dealer networks, and in-house financing capabilities to extend into rental services, while independent operators compete on flexibility, localized service, and pricing. Key competitive differentiators include fleet technology sophistication, digital booking platforms, maintenance capabilities, and geographic reach.

Key Developments:

- In September 2025, SNS Insider reported that CNH is set to launch an enhanced tractor lineup in 2026. The revamped specialty tractors, including the New Holland T4F, T4V, and T4F S Series, will feature larger fuel tanks, improved ergonomics, and upgraded hydraulic systems. Additionally, Case IH's Early Riser planters will see enhancements in planting accuracy.

- In June 2025, CNH Industrial announced its plans to unveil a revamped agricultural equipment lineup for the 2026 model year. This lineup will showcase redesigned tractors, spanning from 20 to over 700 horsepower, under both the New Holland and Case IH brands.

Companies Covered in Farm Equipment Rental Market

- Deere & Company

- CNH Industrial

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra

- Flaman Group

- Pacific AG Rentals LLC

- Messick's

- CLAAS KGaA mbH

- The Papé Group, Inc.

- Other key players

Frequently Asked Questions

The global Farm Equipment Rental market is valued at US$ 48.4 Bn in 2026 and is projected to reach US$ 74.7 Bn by 2033, growing at a CAGR of 6.4% during the forecast period 2026–2033.

The market is primarily driven by the escalating cost of farm equipment ownership with tractor prices rising nearly 50% in the U.S. between 2020 and 2023 and government-backed mechanization programs.

The Tractors segment leads the global Farm Equipment Rental market, commanding approximately 39% of total market share. Their dominance stems from unmatched operational versatility across all major farming functions including tilling, planting, harvesting support, and haulage and applicability across diverse farm sizes and geographies from sub-40 HP compact models to 830 HP industrial-scale units.

North America currently leads the farm equipment rental market, driven by the technologically advanced U.S. agricultural sector, high equipment ownership costs, and persistent labor shortages. Asia Pacific is the fastest-growing region, with a projected revenue share of approximately 45% by 2037, driven by India's 52,000+ CHC network and China's USD 3.5 billion agricultural machinery subsidy program in 2024.

The global Farm Equipment Rental market is led by Deere & Company, CNH Industrial, AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra, which together command over 60% of global agricultural equipment revenue.