- Executive Summary

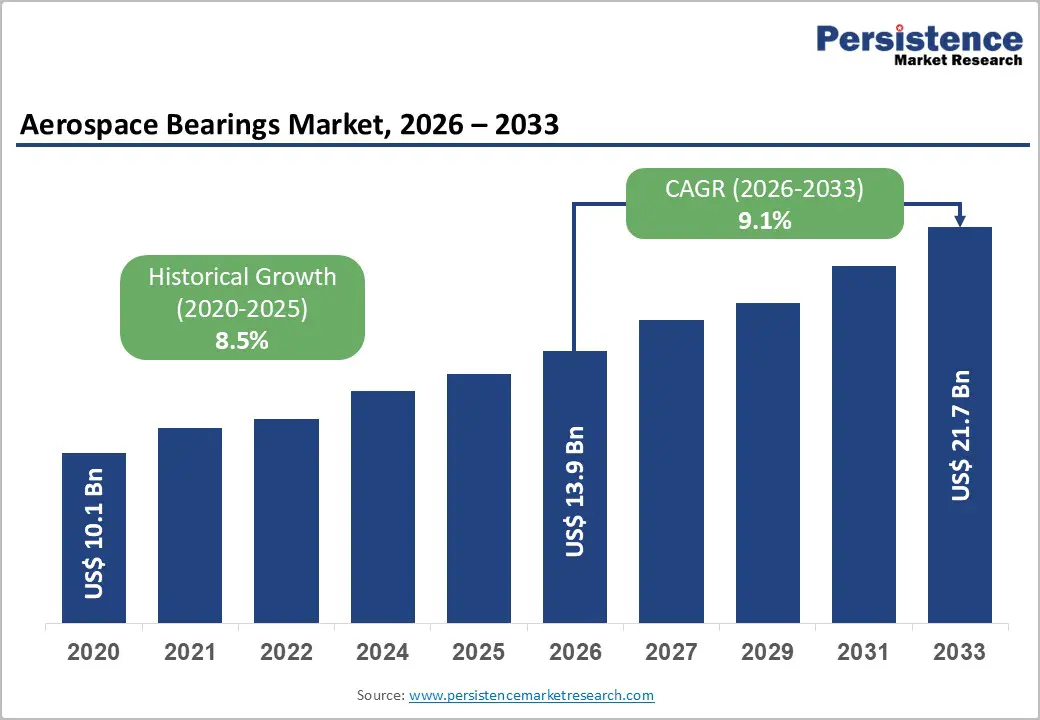

- Global Aerospace Bearings Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply-Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Aerospace Industry Overview

- Global Steel Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Aerospace Bearings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Aerospace Bearings Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Plain Bearings

- Roller Bearings

- Ball Bearings

- Roller Screws

- Ball Screws

- Market Attractiveness Analysis: Product Type

- Global Aerospace Bearings Market Outlook: Platform

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Platform, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Platform, 2026-2033

- Fixed-Wing

- Commercial Aircraft

- Business Jet

- General Aviation Aircraft

- Military Aircraft

- Rotary-Wing

- Civil Helicopters

- Military Helicopters

- Unmanned Aerial Vehicle (UAV)

- Fixed-Wing

- Market Attractiveness Analysis: Platform

- Global Aerospace Bearings Market Outlook: Material

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Material, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Stainless Steel

- Fiber Reinforced Composites

- Engineered Plastics

- Aluminum Alloys

- Metal Backed

- Market Attractiveness Analysis: Material

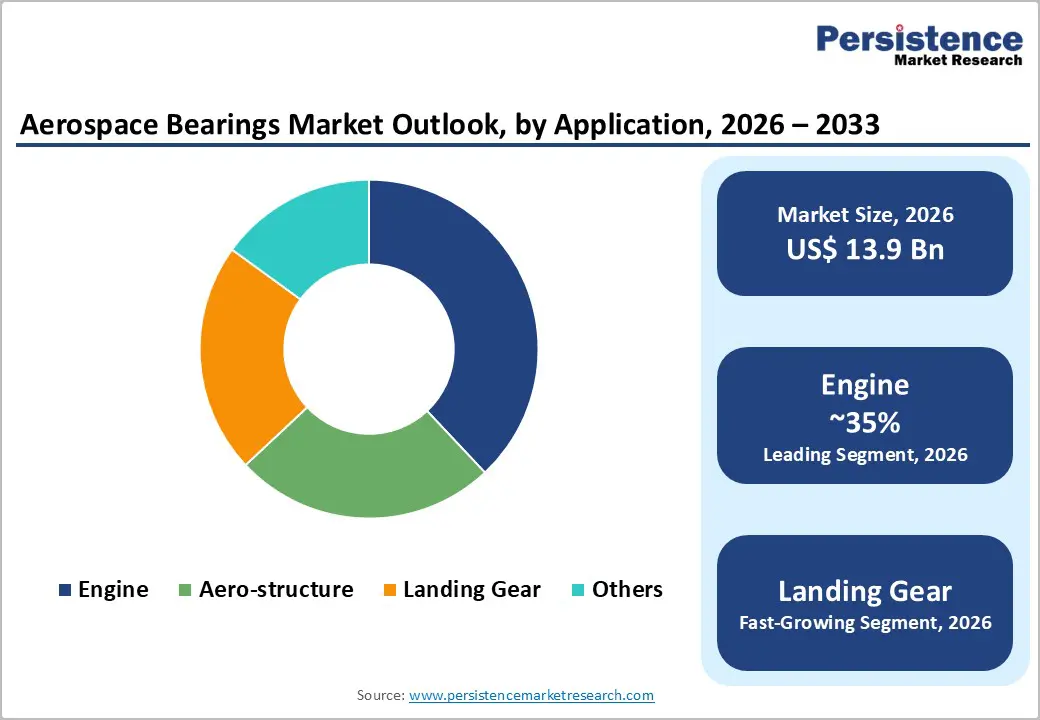

- Global Aerospace Bearings Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Engine

- Aero-structure

- Landing Gear

- Others

- Market Attractiveness Analysis: Application

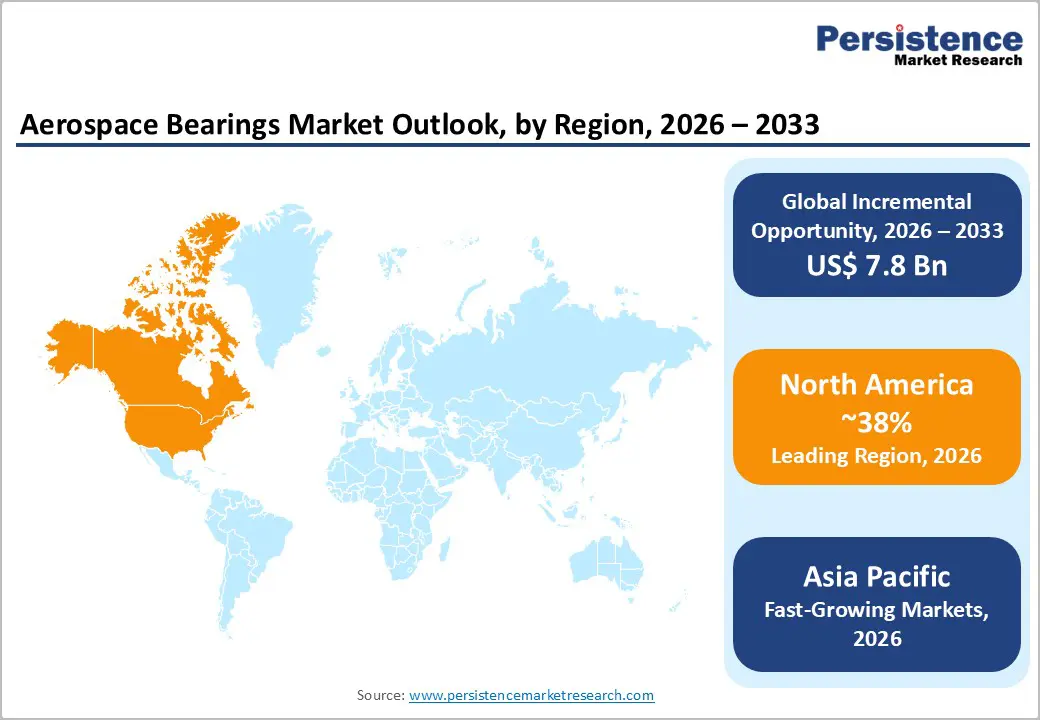

- Global Aerospace Bearings Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Aerospace Bearings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Plain Bearings

- Roller Bearings

- Ball Bearings

- Roller Screws

- Ball Screws

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Platform, 2026-2033

- Fixed-Wing

- Commercial Aircraft

- Business Jet

- General Aviation Aircraft

- Military Aircraft

- Rotary-Wing

- Civil Helicopters

- Military Helicopters

- Unmanned Aerial Vehicle (UAV)

- Fixed-Wing

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Stainless Steel

- Fiber Reinforced Composites

- Engineered Plastics

- Aluminum Alloys

- Metal Backed

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Engine

- Aero-structure

- Landing Gear

- Others

- Europe Aerospace Bearings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Plain Bearings

- Roller Bearings

- Ball Bearings

- Roller Screws

- Ball Screws

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Platform, 2026-2033

- Fixed-Wing

- Commercial Aircraft

- Business Jet

- General Aviation Aircraft

- Military Aircraft

- Rotary-Wing

- Civil Helicopters

- Military Helicopters

- Unmanned Aerial Vehicle (UAV)

- Fixed-Wing

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Stainless Steel

- Fiber Reinforced Composites

- Engineered Plastics

- Aluminum Alloys

- Metal Backed

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Engine

- Aero-structure

- Landing Gear

- Others

- East Asia Aerospace Bearings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Plain Bearings

- Roller Bearings

- Ball Bearings

- Roller Screws

- Ball Screws

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Platform, 2026-2033

- Fixed-Wing

- Commercial Aircraft

- Business Jet

- General Aviation Aircraft

- Military Aircraft

- Rotary-Wing

- Civil Helicopters

- Military Helicopters

- Unmanned Aerial Vehicle (UAV)

- Fixed-Wing

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Stainless Steel

- Fiber Reinforced Composites

- Engineered Plastics

- Aluminum Alloys

- Metal Backed

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Engine

- Aero-structure

- Landing Gear

- Others

- South Asia & Oceania Aerospace Bearings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Plain Bearings

- Roller Bearings

- Ball Bearings

- Roller Screws

- Ball Screws

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Platform, 2026-2033

- Fixed-Wing

- Commercial Aircraft

- Business Jet

- General Aviation Aircraft

- Military Aircraft

- Rotary-Wing

- Civil Helicopters

- Military Helicopters

- Unmanned Aerial Vehicle (UAV)

- Fixed-Wing

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Stainless Steel

- Fiber Reinforced Composites

- Engineered Plastics

- Aluminum Alloys

- Metal Backed

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Engine

- Aero-structure

- Landing Gear

- Others

- Latin America Aerospace Bearings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Plain Bearings

- Roller Bearings

- Ball Bearings

- Roller Screws

- Ball Screws

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Platform, 2026-2033

- Fixed-Wing

- Commercial Aircraft

- Business Jet

- General Aviation Aircraft

- Military Aircraft

- Rotary-Wing

- Civil Helicopters

- Military Helicopters

- Unmanned Aerial Vehicle (UAV)

- Fixed-Wing

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Stainless Steel

- Fiber Reinforced Composites

- Engineered Plastics

- Aluminum Alloys

- Metal Backed

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Engine

- Aero-structure

- Landing Gear

- Others

- Middle East & Africa Aerospace Bearings Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Plain Bearings

- Roller Bearings

- Ball Bearings

- Roller Screws

- Ball Screws

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Platform, 2026-2033

- Fixed-Wing

- Commercial Aircraft

- Business Jet

- General Aviation Aircraft

- Military Aircraft

- Rotary-Wing

- Civil Helicopters

- Military Helicopters

- Unmanned Aerial Vehicle (UAV)

- Fixed-Wing

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Stainless Steel

- Fiber Reinforced Composites

- Engineered Plastics

- Aluminum Alloys

- Metal Backed

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Engine

- Aero-structure

- Landing Gear

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- AST Bearings

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Aurora Bearings

- GGB Bearings Technology

- JTEKT

- Kaman Specialty Bearings

- National Precision Bearings

- New Hampshire Ball Bearings

- August Steinmeyer GmbH & Co. KG

- UMBRAGROUP

- Kugel Aerospace & Defence

- Thomson Industries, Inc.

- Beaver Aerospace & Defense, Inc.

- AST Bearings

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Aerospace & Defense

- Aerospace Bearings Market

Aerospace Bearings Market Size, Share, and Growth Forecast 2026 - 2033

Aerospace Bearings Market by Product Type (Plain Bearings, Roller Bearings, Ball Bearings, Roller Screws and Ball Screws), By Platform (Fixed-Wing, Rotary-Wing and Unmanned Aerial Vehicle (UAV)), by Material (Stainless Steel, Fiber Reinforced Composites, Engineered Plastics, Aluminum Alloys and Metal Backed), By Application (Engine, Aero-structure, Landing Gear and Others) and Regional Analysis 2026 - 2033

Key Industry Highlights:

- Leading Region: North America dominates global market with 38% market share driven by Boeing and Airbus commercial aircraft production, U.S. Department of Defense modernization programs, and established aerospace manufacturing ecosystem supporting sustained bearing procurement demand expansion

- Fastest-Growing Region: Asia Pacific emerging as fastest-growing region expanding at highest CAGR supported by China's COMAC C919 aircraft development with 1,000+ orders, India's expanding aviation sector, and Japan's advanced manufacturing capabilities supporting cost-competitive bearing production and regional supply chain integration

- Dominant Product Segment: Fixed-wing commercial aircraft commanding 52% market share anchored by Boeing 737 MAX recovery and Airbus A320 family production expansion with 17,000+ unit order backlog establishing multi-year manufacturing visibility supporting baseline bearing demand sustainability

- Fastest-Growing Segment: Unmanned aerial vehicle (UAV) segment advancing fastest at 8.68% CAGR driven by military procurement acceleration, commercial delivery service deployment, and specialized electromagnetic interference resistance requirements supporting emerging platform bearing innovation and market opportunity realization

- Opportunity: Advanced thermal management bearing integration and ceramic hybrid technology adoption representing major market opportunity supported by aircraft electrification initiatives, extreme temperature engine development, and fuel efficiency imperatives justifying premium pricing and technology differentiation strategies.

| Key Insights | Details |

|---|---|

| Laser Processing Market Size (2026E) | US$ 13.9 Bn |

| Market Value Forecast (2033F) | US$ 21.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.5% |

Market Dynamics

Drivers - Unprecedented Commercial Aircraft Fleet Expansion and Production Rate Acceleration Supporting Baseline Bearing Demand

Commercial aviation recovery combined with expanded production schedules represents the most significant aerospace bearings market expansion driver, with coordinated Boeing and Airbus production initiatives establishing sustained baseline equipment demand. Airbus commercial aircraft deliveries reached approximately 735 aircraft in 2023, with current guidance targeting 770 aircraft in 2024 and expected expansion toward 800+ deliveries in 2026, establishing unprecedented production volumes requiring synchronized bearing procurement across multiple aircraft programs.

Boeing 737 MAX production recovery following quality remediation and regulatory clearance, combined with resumed deliveries to Chinese carriers representing approximately 47 of Boeing's 53 total China deliveries in 2024, demonstrates synchronized global demand supporting bearing supplier capacity investments. Airbus order backlogs exceeding 17,000 units across A320, A350, and A400M programs establish multi-year production visibility supporting original equipment manufacturer bearing supplier planning and investment justification.

Accelerating Advanced Bearing Technology Integration and Electrification Requirements Supporting High-Performance Component Adoption

Aircraft electrification initiatives and advanced thermal management system integration drive exceptional bearing equipment demand expansion, with flight control actuation system electrification requiring specialized high-precision components. Electrified flight-control actuators utilizing roller screws and hybrid foil-magnetic bearing designs deliver 15-20% energy efficiency improvements compared to traditional positive temperature coefficient (PTC) alternatives, directly supporting vehicle efficiency targets and operator cost reduction objectives.

Aerospace coatings protecting bearing surfaces from corrosion and thermal degradation increasingly integrate with advanced bearing designs supporting extended operational lifespan and reliability assurance across demanding flight environments.

Restraints - Stringent Certification Requirements and Extended Time-to-Market Cycles Creating Production Planning Constraints for Bearing Manufacturers

Aerospace bearing certification complexity represents substantial market expansion constraint with airworthiness authorities including Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA) requiring comprehensive qualification programs extending multi-year certification timelines delaying market entry for innovative bearing designs.

Composite cage technology offering superior high-temperature performance and reduced friction characteristics requires lengthy qualification cycles despite demonstrating competitive advantages, creating disincentives for bearing manufacturers pursuing emerging material adoption. Supplier qualification requirements including Purchasing Performance Assessment Plan (PPAP) audits and AS9100 aerospace quality management compliance necessitate substantial capital investment and operational capability development creating barriers for emerging market entrants.

Rising Raw Material Costs and Supply Chain Vulnerability Creating Cost Pressures and Production Disruptions

Bearing material cost escalation including elevated titanium alloy, specialty steel, and ceramic component pricing creates substantial margin compression affecting profitability across bearing manufacturer portfolios. Semiconductor component shortages affecting electronic control modules and temperature sensor integrations within advanced bearing systems create procurement complexity with delivery lead times extending 16-24 weeks cascading through manufacturing schedules. Geopolitical trade restrictions including United States export controls affecting advanced materials and components create supply chain uncertainty affecting bearing manufacturer ability to source specialized inputs supporting Chinese aerospace manufacturers including COMAC aircraft programs. Supply chain imbalances between North American and European bearing suppliers relative to Asia-Pacific manufacturing hubs create logistics cost elevation and delivery uncertainty affecting competitive positioning.

Opportunity - Unmanned Aerial Vehicle Proliferation and Military Aircraft Modernization Programs Establishing High-Growth Bearing Market Segments

Unmanned aerial vehicle (UAV) market expansion driven by military procurement programs and commercial drone platform development represents exceptional bearing opportunity with specialized electromagnetic interference resistance requirements and extended flight duration design objectives. U.S. Army and NATO defense modernization initiatives including rotorcraft life-extension programs supporting Black Hawk and Apache helicopter service life extension through advanced bearing technology integration create sustained high-value equipment procurement opportunities. Military aviation modernization including Eurofighter Typhoon upgrades, F-35 Lightning II production expansion, and future combat air system (FCAS) development establish bearing demand growth opportunities supporting European aerospace suppliers maintaining technology differentiation positioning. UAV endurance requirements supporting intelligence, surveillance, and reconnaissance (ISR) missions and cargo transport applications demand bearings offering superior fatigue resistance and extended operating interval capabilities exceeding traditional commercial aircraft requirements.

Advanced Thermal Management System Integration and Low-Temperature Operating Condition Requirements Supporting Specialized Bearing Development

Space launch vehicle expansion including commercial satellite deployment and private aerospace company initiatives establish emerging bearing opportunities with cryogenic environment operation requirements and extended mission duration reliability demands. Fiber-reinforced composite bearing adoption expanding at accelerating rates due to superior corrosion resistance, lightweight characteristics, and thermal performance advantages create emerging material technology market segments with premium pricing justification. Hybrid ceramic-steel bearing development combining advanced rolling elements with next-generation steel formulations including high-nitrogen steels and powder metallurgy designs establish high-performance market segments supporting spacecraft system applications and next-generation engine programs.

Category-wise Analysis

Product Type Insights

Ball bearings dominate the aerospace bearing market commanding approximately 43% market share, reflecting proven baseline performance across diverse aircraft applications and established aerospace certification foundations. Ball bearing prevalence reflects cost-effectiveness combined with demonstrated reliability supporting high-speed turbine engine applications, flight control system integration, and landing gear assemblies across commercial and military aircraft platforms. Traditional ball bearing designs accommodating radial and axial load requirements support aircraft engine main shaft support, accessory gearbox applications, and flight control surface actuation with established manufacturing processes enabling economies of scale and competitive pricing. Advanced ball bearing variants incorporating ceramic hybrid designs with rolling elements combining ceramic composition with steel raceway construction deliver superior high-temperature performance enabling 400°C+ operating environments in modern turbofan engines.

Platform Insights

Fixed-wing commercial aircraft command approximately 52% of aerospace bearing market revenue, driven by high-volume production programs including Airbus A320 family and Boeing 737 MAX establishing standardized bearing specifications across multiple aircraft variants. Single-aisle aircraft dominance with Boeing projecting single-aisle jets forming 76% of future deliveries established sustained high-volume bearing demand supporting manufacturing economies of scale and supplier capacity utilization optimization. Commercial aircraft bearing requirements encompassing engine main and auxiliary bearing applications, flight control system integration, and landing gear assemblies create distributed bearing demand across multiple original equipment manufacturer suppliers supporting competitive ecosystem development.

Material Insights

Metallic bearing solutions secured approximately 43% market share in 2024 with steel and titanium compositions continuing to deliver proven performance supporting cost-effectiveness and manufacturing maturity. High-nitrogen steels and powder metallurgy bearing designs enabling optimized grain structure development to deliver superior contact fatigue strength supporting extended service life and reliability assurance across demanding aerospace applications. Aluminum alloy bearing construction offering lightweight benefits while maintaining structural integrity support aerospace efficiency objectives with weight reduction directly translating to fuel consumption reduction. Stainless steel bearing adoption providing superior corrosion resistance and extended operational lifespan supports marine environment aircraft and salt-spray exposure applications including coastal region helicopter operations.

Application Insights

Aircraft engine applications command approximately 35% of aerospace bearing revenues reflecting multiple bearing requirement per aircraft with turbofan engines containing hundreds of precision bearings supporting high-speed rotation and extreme temperature operation. Engine bearing criticality extending across main shaft support, auxiliary gearbox operation, and accessory pad bearing requirements creates volume concentration supporting bearing supplier specialization and dedicated development programs.

Landing gear assemblies representing approximately 28% of bearing demand accommodate extreme load conditions during takeoff, landing, and taxiing operations requiring tapered roller bearing and ball bearing combinations delivering structural integrity assurance and operational reliability. Flight control system integration supporting aero-surface actuation including aileron, elevator, and rudder control requires specialized bearing designs enabling precise movement and dynamic response requirements supporting aircraft handling characteristics optimization.

Regional Insights

North America Aerospace Bearings Market Share and Trends

North America maintains strong market position with approximately 38% global aerospace bearing market share anchored by United States leadership in commercial aircraft manufacturing and military aerospace programs establishing sustained bearing procurement demand. Boeing commercial aircraft production centered in Seattle, Washington and South Carolina facilities combined with distributed supplier network across United States regions supports approximately 40% of global aircraft deliveries driving corresponding bearing consumption across engine, flight control, and landing gear applications.

Regulatory framework established by Federal Aviation Administration (FAA) establishing stringent airworthiness standards and certification requirements supports mature U.S. bearing manufacturing ecosystem with established quality assurance capabilities and AS9100 compliance infrastructure. Major bearing suppliers including New Hampshire Ball Bearings, AST Bearings, Aurora Bearings, and National Precision Bearings maintain U.S.-based manufacturing operations supporting rapid response capabilities and supply chain resilience for original equipment manufacturer customers.

Europe Aerospace Bearings Market Share and Trends

Europe commands approximately 26% global aerospace bearing market share, characterized by stringent environmental regulations and advanced technology adoption, driving sophisticated bearing solution development. Airbus commercial aircraft operations dominating European aerospace sector with final assembly lines in Hamburg, Germany, fuselage production in Toulouse, France, and wing manufacturing across multiple European locations, establishing foundational bearing demand with A320 family production exceeding 750 aircraft annually.

European rotorcraft operations, including Airbus Helicopters production and military helicopter programs supporting the defense modernization drive, specialized demand for rotor transmission systems and flight control actuation. The United Kingdom aerospace sector, led by BAE Systems and regional aircraft manufacturers, contributes to bearing market dynamics with military platform modernization and combat aircraft production, supporting specialized bearing requirements.

Asia Pacific Aerospace Bearings Market Share and Trends

Asia Pacific represents the fastest-growing region with approximately 35% global aerospace bearing market share, driven by China's extraordinary commercial aircraft expansion and emerging market aircraft demand acceleration. China's COMAC C919 aircraft development with orders exceeding 1,000 aircraft and manufacturing ramp-up initiatives create exceptional bearing procurement opportunities supporting regional supplier capacity investments and technology partnership expansion.

India's emerging aviation sector with Hindustan Aeronautics Limited (HAL) developing domestic fighter aircraft and expanding commercial aircraft maintenance operations, creates growth opportunities with air ambulance services and commercial aviation expansion, driving rotary-wing bearing demand acceleration. Japan's aerospace manufacturing ecosystem, including Mitsubishi Heavy Industries supplying approximately 35% of Boeing 787 content, and advanced manufacturing capabilities support specialized bearing production and technological innovation initiatives.

Competitive Landscape

The aerospace bearings market exhibits significant consolidation among global manufacturers including SKF AB (Sweden), The Timken Company, NSK Ltd (Japan), RBC Bearings Incorporated, Schaeffler Group (Germany), GGB Bearing Technology, JTEKT Corporation (Japan), and Kaman Specialty Bearings collectively commanding substantial market share through comprehensive bearing portfolios, established original equipment manufacturer relationships, and continuous research investment.

Market leaders pursue expansion through strategic partnerships with aircraft manufacturers, defense contractors, and aerospace suppliers, integration of advanced materials, including ceramic hybrids and composite designs, and research initiatives advancing thermal management bearing innovation supporting next-generation aerospace platform development. Traditional bearing manufacturers, including SKF and Timken increasingly developing specialized aerospace solutions.

Key Market Developments

- In November 2024, NSK Ltd. Introduces Gas Turbine Generator Bearing Specifically Engineered for Advanced eVTOL Aircraft Propulsion Systems. NSK Ltd. unveiled a specialized bearing design optimized for electric vertical takeoff and landing (eVTOL) aircraft applications, addressing high-speed generator requirements and thermal management challenges supporting emerging advanced air mobility platform development.

- In June 2024, RBC Bearings Announces 20.7% Year-on-Year Increase in Aerospace and Defense Division Revenues Reaching US$ 519.3 Million - RBC Bearings Incorporated reported significant sales acceleration across aerospace and defense sectors reflecting sustained demand from commercial aircraft production expansion and military modernization program participation, demonstrating bearing supplier capacity optimization.

Companies Covered in Aerospace Bearings Market

- AST Bearings

- Aurora Bearings

- GGB Bearings Technology

- JTEKT

- Kaman Specialty Bearings

- National Precision Bearings

- New Hampshire Ball Bearings

- August Steinmeyer GmbH & Co. KG

- UMBRAGROUP

- Kugel Aerospace & Defence

- Thomson Industries, Inc.

- Beaver Aerospace & Defense, Inc.

- Others Key Players

Frequently Asked Questions

The global aerospace bearings market was valued at US$ 13.9 million in 2026 and is projected to reach US$ 21.7 million by 2033, representing a 6.6% CAGR expansion through the forecast period.

Primary growth drivers include unprecedented commercial aircraft fleet expansion with Airbus order backlogs exceeding 17,000 units and Boeing 737 MAX production recovery establishing multi-year production visibility supporting sustained bearing procurement. Military aviation modernization including U.S.

Fixed-wing commercial aircraft dominate with approximately 52% market share driven by high-volume production programs including Airbus A320 family producing 750 aircraft annually and Boeing 737 MAX recovery supporting baseline bearing demand across engine, flight control, and landing gear applications.

North America maintains dominant market position with approximately 38% global market share supported by United States leadership in commercial aircraft manufacturing, military aerospace programs, and established bearing supplier ecosystem. manufacturing capabilities supporting competitive bearing production and regional supply chain integration acceleration.

Market leaders include SKF AB, RBC Bearings, and Schaeffler Group leveraging German engineering expertise in precision bearing manufacturing.