- Technology

- Workspace as a Service Market

Workspace as a Service Market Size, Share, and Growth Forecast 2026 - 2033

Workspace as a Service Market by Product Type (System Integrated Services, Desktop as a Service (DaaS), Application as a Service (AaaS)), Deployment Type (Public, Private, Hybrid), Enterprise Size (SME, Large Enterprise), End-user (BFSI, Education, Retail, Government, IT & Telecom, Healthcare, Others), and Regional Analysis for 2026 - 2033

Workspace as a Service Market Size and Trend Analysis

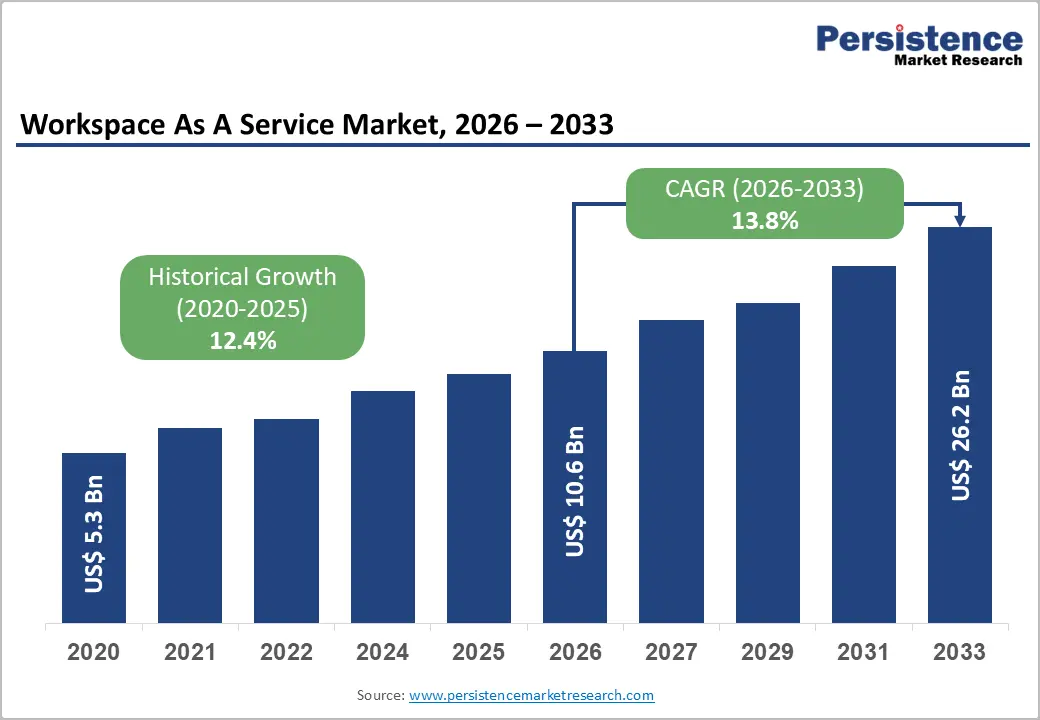

The global workspace as a service (WaaS) market is valued at US$ 10.6 Bn in 2026 and is projected to reach US$ 26.2 Bn by 2033, growing at a CAGR of 13.8% between 2026 and 2033.

This high-velocity growth is propelled by the structural enterprise transition to cloud-first digital workplace architectures, underpinned by the sustained adoption of hybrid and remote work models, rapid integration of Artificial Intelligence (AI) and zero-trust security frameworks into virtual desktop platforms, and the growing preference of organisations for operational expenditure (OpEx) models over capital-intensive on-premises infrastructure.

Key Industry Highlights:

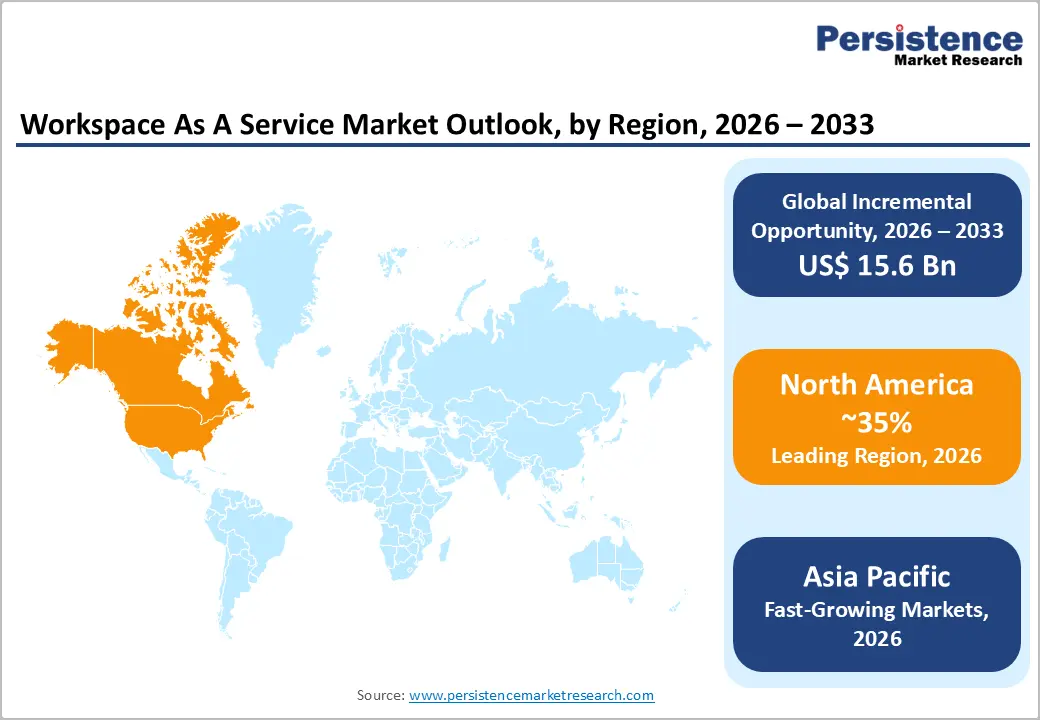

- Leading Region: North America leads the global WaaS market with approximately 35.6% revenue share in 2024, anchored by U.S. enterprise cloud adoption, hyperscaler infrastructure density, and regulatory frameworks driving secure virtual workspace compliance.

- Fastest Growing Region: Asia Pacific is the fastest growing WaaS market, projected at a CAGR of 12.7% through 2030, driven by China's Digital China initiative, India's IT sector, and ASEAN multinational expansion requiring secure distributed workplace infrastructure.

- Dominant Segment: Desktop as a Service (DaaS) leads the product type category with approximately 57% market share in 2024, driven by Microsoft Windows 365, Amazon WorkSpaces, and Citrix DaaS serving enterprise demand for full-OS virtual desktop delivery.

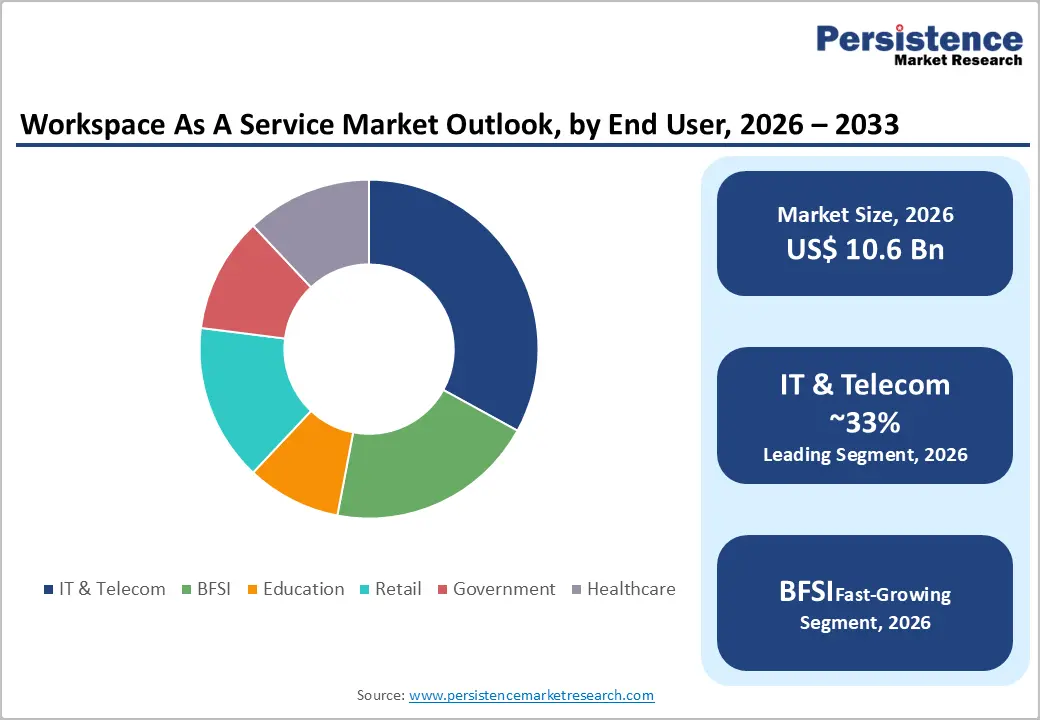

- Fastest Growing Segment: The BFSI end-use vertical is the fastest growing segment, projected at 12.4% CAGR through 2030, fuelled by DORA compliance mandates, PCI DSS requirements, and the hybrid work transformation of financial trading and wealth management operations.

- Key Market Opportunity: SME adoption of pay-as-you-go WaaS represents the highest-volume growth opportunity with SMEs accounting for 53% of new WaaS deployments in 2023 as hyperscaler pricing democratises access to enterprise-grade virtual desktop and application delivery.

| Key Insights | Details |

|---|---|

| Workspace as a Service Market Size (2026E) | US$ 10.6 Bn |

| Market Value Forecast (2033F) | US$ 26.2 Bn |

| Projected Growth CAGR (2026 - 2033) | 13.8% |

| Historical Market Growth (2020 - 2025) | 12.4% |

DRO Analysis

Drivers - Accelerating Hybrid Work Adoption and Enterprise Cloud-First Transformation

The global structural shift to hybrid and remote work models remains the most powerful demand driver for the WaaS market. According to the International Labour Organization (ILO), approximately 74% of businesses globally have adopted hybrid work models, compelling their IT departments to deploy cloud-hosted virtual desktop and application environments that ensure consistent, secure, device-agnostic productivity.

In 2024, over 1.2 billion employees globally accessed hosted desktops or virtual applications a 14% increase compared to 2023. WaaS eliminates the capital burden of hardware refresh cycles; enterprises report 34% reductions in IT operational costs upon WaaS adoption. The U.S. Bureau of Labor Statistics confirms that flexible work arrangements have become a permanent expectation for knowledge workers, ensuring that enterprise demand for scalable, cloud-managed workspaces remains structurally robust through the forecast period and beyond.

AI Integration and Zero-Trust Security Frameworks Elevating WaaS Value Proposition

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into WaaS platforms is fundamentally elevating the technology's value proposition beyond simple desktop virtualisation, driving accelerated adoption across regulated and high-security enterprise verticals. In 2024, approximately 29% of WaaS deployments integrated AI-based monitoring to improve user experience and reduce downtime, while 36% of enterprises prioritised WaaS solutions offering zero-trust security frameworks.

In 2025, Microsoft expanded its WaaS security capabilities with AI-driven threat detection across Azure Virtual Desktop (AVD) and Windows 365, serving over 40 million enterprise users globally. Simultaneously, by Q3 2024, AWS expanded its AppStream platform to support GPU-powered virtual desktops, serving 12 million developers.

Restraints - Data Security and Regulatory Compliance Concerns in Multi-Tenant Cloud Environments

Despite its benefits, WaaS adoption faces resistance from organisations with stringent data residency and sovereignty requirements. GDPR in Europe, HIPAA in the U.S. healthcare sector, and various national data protection laws across Asia impose strict constraints on where enterprise data can reside and be processed.

In 2024, 36% of enterprises cited data security as the primary concern in WaaS adoption decisions. Regulated verticals, including banking, defence, and government frequently require private or sovereign cloud deployments, adding complexity and cost that can limit the addressable market for standard public cloud WaaS offerings.

Legacy IT Infrastructure Integration Complexity and Migration Challenges

A significant number of enterprises, particularly in legacy-intensive sectors such as manufacturing, public administration, and financial services, operate mission-critical applications that were not designed for cloud-hosted virtual delivery. In 2024, 39% of enterprises reported difficulties migrating legacy IT systems to WaaS platforms, making integration complexity the leading technical restraint.

Latency sensitivity, application compatibility issues, and the cost of application rearchitecting create meaningful barriers to wholesale WaaS adoption. Additionally, 65% of WaaS providers reported increased expenses related to secure data storage and bandwidth provisioning, and 29% of organisations cited unpredictable pricing models as a key challenge in budget forecasting for WaaS deployments.

Opportunities - BFSI Sector Demand for Secure, Compliant Virtual Workspace Infrastructure

The Banking, Financial Services, and Insurance (BFSI) sector represents the most commercially compelling near-term growth opportunity in the WaaS market, with the segment projected to expand at the fastest vertical CAGR of 12.4% through 2030 among all end-use sectors. Financial institutions require WaaS platforms that deliver zero-trust endpoint security, multi-factor authentication (MFA), session isolation, and audit trail capabilities mandated by Basel III, PCI DSS, and DORA (Digital Operational Resilience Act) the EU regulation applicable from January 2025.

The growing adoption of hybrid working in financial trading, wealth management, and insurance underwriting is driving banks to deploy secure WaaS solutions for thousands of remote knowledge workers. In November 2024, Citrix (Cloud Software Group) announced the general availability of Citrix DaaS for Amazon WorkSpaces Core, combining Citrix's enterprise-grade DaaS with AWS's managed VDI infrastructure, providing BFSI organisations with a powerful, compliance-ready, hybrid multi-cloud virtual desktop platform.

SME Adoption Driven by Pay-As-You-Go Pricing and Managed Service Models

Small and Medium Enterprises (SMEs) represent a high-growth, high-volume expansion frontier for the WaaS market. Historically constrained by the capital costs of enterprise-grade VDI infrastructure, SMEs are now rapidly adopting WaaS through the pay-as-you-go and managed service delivery models offered by hyperscalers and specialist managed service providers. In 2024, SMEs accounted for 41% of total WaaS adoption globally, and 53% of all new WaaS deployments in 2023 were made by SMEs reflecting the segment's accelerating uptake.

Amazon WorkSpaces and Windows 365 Cloud PC have democratised access to enterprise WaaS, offering per-user monthly billing that aligns IT costs directly to business activity. Tech Mahindra's FLEX Digital Workplace Services a multi-cloud platform supporting 3D graphics and CAD workloads extends WaaS accessibility to SMEs in engineering and design sectors previously excluded by graphics performance constraints.

Category-wise Analysis

Product Type Insights

Within the product type category, Desktop as a Service (DaaS) is the dominant segment, accounting for approximately 57% of total WaaS market revenue in 2024. DaaS's leadership is attributed to enterprise demand for full operating-system virtual desktop images that support legacy line-of-business applications, enable centralised IT patch management, and deliver a consistent Windows desktop experience across geographically dispersed workforces.

The November 2024 general availability of Citrix DaaS for Amazon WorkSpaces Core combining Citrix's enterprise DaaS control plane with AWS's managed VDI infrastructure exemplifies the platform convergence trends reinforcing DaaS dominance. Microsoft's Windows 365 cloud PC, which provides personalised full-Windows virtual desktops streamed from over 60 Azure cloud regions, commands an estimated 25-35% of the DaaS segment alone.

Deployment Type Insights

The Public Cloud deployment model is the leading segment in the deployment type category, accounting for approximately 51% of WaaS revenue in 2024. Public cloud WaaS delivered through hyperscaler platforms including Amazon WorkSpaces, Microsoft Azure Virtual Desktop (AVD), and Google Cloud Workstations benefits from global infrastructure density, rapid elasticity, and competitive pay-as-you-go pricing that lower barrier to adoption for SMEs and large enterprises alike.

Hybrid deployment is the fastest growing model, projected at a premium CAGR through 2033, as enterprises seek to balance the scalability and cost efficiency of public cloud with the data sovereignty and low-latency performance of on-premises or private cloud resources.

Enterprise Size Insights

The Large Enterprise segment leads the WaaS market by enterprise size, accounting for approximately 59% of total market revenue in 2024. Large enterprises defined as organisations with more than 1,000 employees have the most complex, geographically distributed IT environments and the greatest regulatory compliance requirements, making them the natural primary adopters of sophisticated, managed WaaS solutions with enterprise-grade security, SLA commitments, and custom integration capabilities.

In 2023, over 71% of Fortune 500 companies integrated WaaS solutions to support hybrid work structures. However, the SME segment is the fastest growing by enterprise size projected to outpace large enterprise adoption through 2033 driven by cost-accessible DaaS pricing, managed service availability, and the critical role WaaS plays in enabling SMEs to attract and retain talent by offering remote and flexible work capabilities.

End Use Insights

The IT & Telecom sector leads the WaaS market by end use, accounting for approximately 33% of total market revenue in 2024. IT and telecommunications firms have been early and heavy adopters of WaaS as cloud computing, virtualisation, and BYOD policies are intrinsic to their operational culture enabling developers, engineers, and support staff to access enterprise environments securely from any device globally.

BFSI is the fastest growing end-use vertical, driven by the implementation of DORA, PCI DSS, and hybrid trading desk requirements. The Healthcare vertical is also growing rapidly, with 22% of healthcare organisations implementing WaaS services in 2024 to support telehealth, remote diagnostics, and HIPAA-compliant clinical data access underpinning a diversified end-use expansion trajectory through 2033.

Regional Analysis

North America Workspace as a Service Market Trends

North America leads the global WaaS market, accounting for approximately 35.6% of total revenue in 2024, supported by mature cloud infrastructure, high broadband penetration, and early-adopter behaviour across the technology, financial services, and media sectors. The United States is the dominant national market, with the U.S. WaaS segment projected at a CAGR of 11.1% through 2030.

North American regulatory clarity including NIST Cybersecurity Framework guidance on cloud security and the FTC's remote work data protection guidelines, has accelerated enterprise WaaS rollouts by providing clear compliance frameworks for public cloud deployments. In November 2024, Citrix (Cloud Software Group) announced Citrix DaaS for Amazon WorkSpaces Core general availability, providing North American enterprises, particularly in financial services and healthcare, with a combined Citrix + AWS platform offering enterprise DaaS with Microsoft 365 Apps support, encrypted disk security, and flexible compute pricing.

Asia Pacific Workspace as a Service Market Trends

Asia Pacific is the fastest growing regional market for WaaS, accounting for approximately 26% of global revenue in 2024, and is projected to record the highest regional CAGR of 12.7% through 2030. China is the largest national market in the region, supported by the government's Made in China 2025 and Digital China initiatives, which drive enterprise IT modernisation and cloud adoption across the country's manufacturing, financial, and technology sectors.

India is a rapidly growing WaaS market, driven by the country's booming IT services sector, the Government of India's Digital India programme, and the large-scale remote work adoption across the 2+ million employee IT services industry. Tech Mahindra, headquartered in Pune, India offers FLEX Digital Workplace Services, a multi-cloud WaaS platform supporting 3D graphics and CAD workloads, positioning India as a technology innovator in the global WaaS landscape alongside a cost-competitive delivery hub.

Europe Workspace as a Service Market Trends

Europe is a high-value, compliance-driven market for WaaS, accounting for approximately 27% of global WaaS revenue in 2024. The European Union's General Data Protection Regulation (GDPR) and the Digital Operational Resilience Act (DORA) applicable from January 2025 for financial entities, are creating powerful demand for WaaS platforms with certified EU data residency, audit logging, and incident reporting capabilities.

In May 2024, Colt Technology Services expanded its Colt IQ Network platform with enhanced virtual workspace delivery capabilities for enterprise clients across Europe and Asia, reflecting the growing commercial opportunity in European managed WaaS. Microsoft's commitment to EU Data Boundary, ensuring that European customer data for Microsoft 365 and Azure Virtual Desktop is stored and processed within the EU, has been a decisive competitive advantage in winning enterprise WaaS contracts in Germany, France, and the Benelux region.

Market Structure Analysis

The global WaaS market is moderately concentrated, with three hyperscalers Microsoft, Amazon Web Services (AWS), and Google, commanding most of the public cloud WaaS infrastructure revenue through Azure Virtual Desktop, Windows 365, Amazon WorkSpaces, and Google Cloud Workstations. Microsoft alone holds an estimated 25-35% of the DaaS segment through its native enterprise ecosystem integration. Key differentiators include AI-driven workspace intelligence, zero-trust security integration, and hyperscaler global data centre density.

Key Developments:

- In June 2025, Amazon announced USD 10 billion investment in North Carolina datacenters to expand AI infrastructure and create 500 jobs, strengthening its Workspace as a Service region in the southeastern United States.

- In March 2025: ServiceNow finalized the USD 2.85 billion acquisition of Moveworks to infuse agentic AI across employee workflows.

Companies Covered in Workspace as a Service Market

- Amazon Web Services, Inc.

- Broadcom (VMware Inc.)

- Cloud Software Group, Inc. (Citrix)

- Colt Technology Services Group Limited

- Dell Inc.

- Econocom Group SE

- Microsoft

- Tech Mahindra Limited

- Unisys Corporation

- Evolve IP, LLC

Frequently Asked Questions

The global Workspace as a Service (WaaS) Market is estimated at US$ 10.6 Bn in 2026 and is projected to reach US$ 26.2 Bn by 2033, expanding at a CAGR of 13.8% during the forecast period.

The primary demand drivers include the structural global adoption of hybrid and remote work with 74% of businesses globally operating hybrid work models the integration of AI and zero-trust security frameworks into WaaS platforms, and the strong preference for OpEx-based IT models. Over 1.2 billion employees accessed hosted desktops or virtual applications in 2024.

The Desktop as a Service (DaaS) segment leads the WaaS market by product type with approximately 57% revenue share in 2024. DaaS is preferred by enterprises for full operating-system virtual desktop delivery, centralised IT management, and support for legacy line-of-business applications.

North America leads the global WaaS market with approximately 35.6% revenue share in 2024, supported by a mature cloud infrastructure ecosystem, high enterprise broadband penetration, and the world's densest concentration of hyperscaler data centres.

The leading companies in the global WaaS market include Microsoft Corporation , Amazon Web Services, Inc., Cloud Software Group, Inc., Broadcom, Google LLC, and Omnissa, among others.