- Non-food Packaging

- Western Europe Tinplate Packaging Market

Western Europe Tinplate Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Western Europe Tinplate Packaging Market by Product Type (Cans, Boxers and Containers, Pails), Thickness (Below 0.15 mm, 0.15 mm to 0.30 mm, More than 0.30mm), End-use Industry (Paints, Chemicals), and Country Analysis, 2026 - 2033

Western Europe Tinplate Packaging Market Size and Trends Analysis

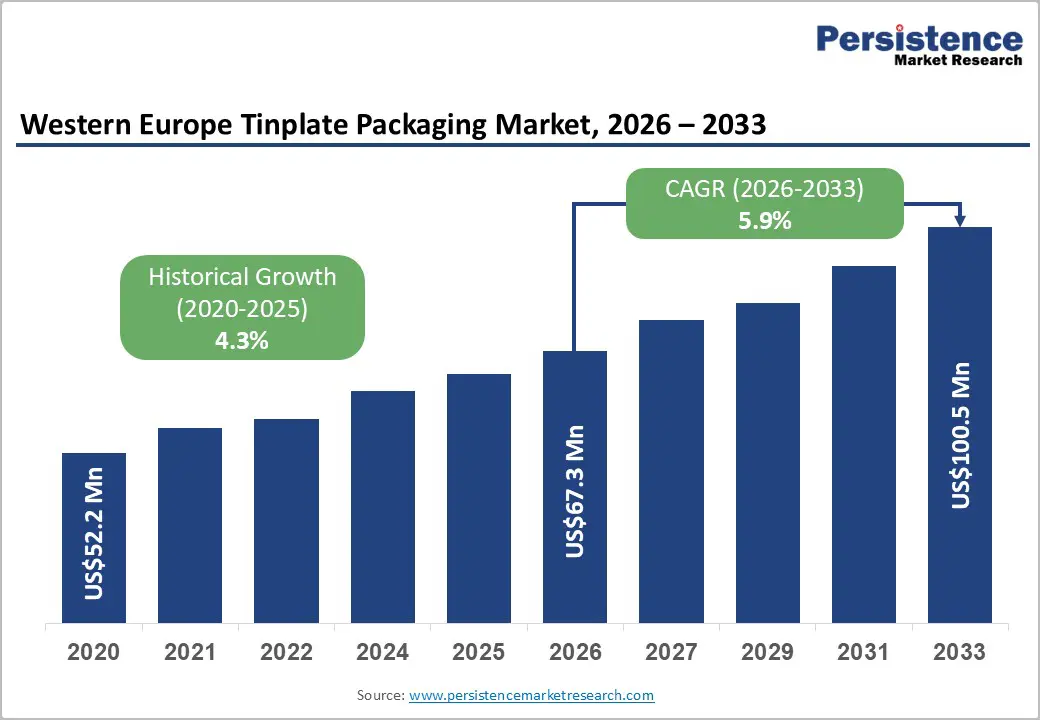

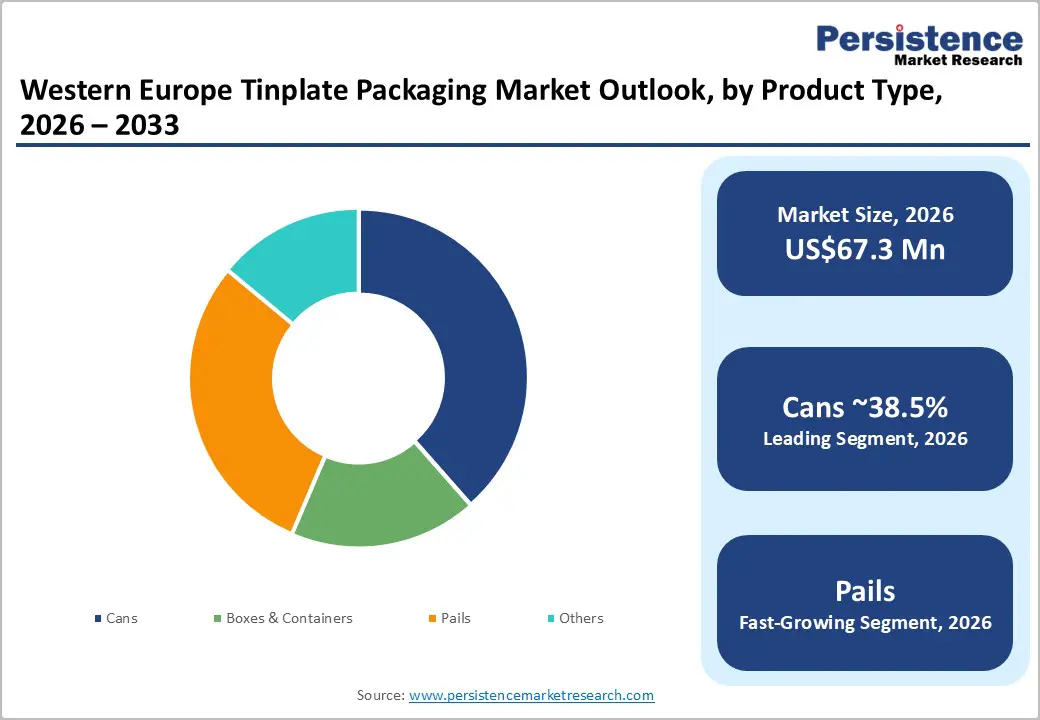

The Western Europe tinplate packaging market size is expected to be valued at US$67.3 million in 2026 and is predicted to reach US$100.5 million by 2033, surging at a CAGR of 5.9% between 2026 and 2033, driven by rising demand for sustainable and fully recyclable packaging solutions that comply with EU circular economy targets.

Growth is further supported by increasing consumption of canned food and beverages, especially in urban markets seeking long shelf life and convenience.

Key Industry Highlights:

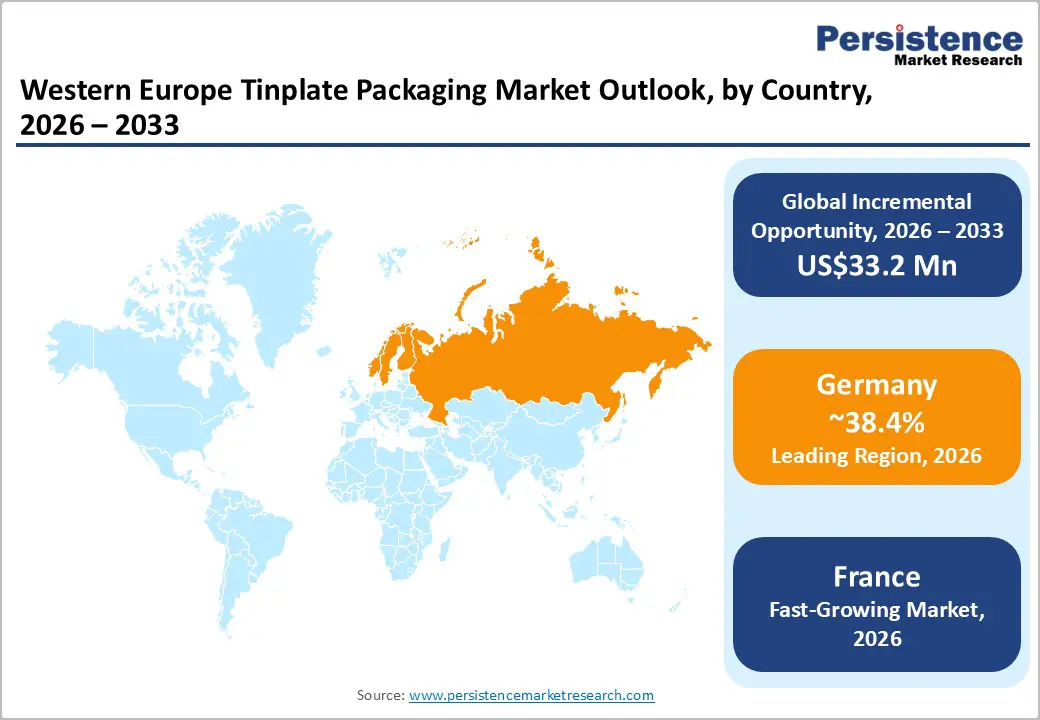

- Leading Country: Germany, with about a 38.4% share in 2026, owing to its well-established manufacturing base and high consumption of packaged industrial goods.

- Fast-growing Country: France, spurred by rising demand for sustainable packaging and increasing government push toward circular economy practices.

- Leading Product Type: Cans, approximately 38.5% share in 2026, as these provide superior barrier protection and long shelf life, making them ideal for food and beverage storage.

- Dominant End-use Industry: Paints, nearly 52.2% in 2026, as metal packaging ensures chemical stability and safe storage of solvent-based formulations under REACH regulations.

- Anti-Dumping Duties: In January 2025, the European Commission imposed provisional anti-dumping duties on tinplate imports from China, with rates of 14.1% for Baoshan Iron & Steel Co. and WISCO-Nippon Steel Tinplate Co., 47.1% for Shougang Jingtang United Iron & Steel Co., and 62.6% for other China-based companies.

DRO Analysis

Driver - Urgent Need to Comply with Circular Economy Principles

Western Europe's waste-sorting systems are built to handle tinplate's key physical property, i.e., magnetism. As tinplate is magnetic, it gets pulled out from mixed municipal waste automatically during sorting without any consumer effort. This gives it a consistent recovery advantage over plastic or glass. The results are notable. According to a January 2026 press release from thyssenkrupp Rasselstein, Germany's recycling rate for tinplate from private end consumption reached a record 94.3% in 2024.

The total tinplate consumption recycling rate hit 92.5%, a level that has held stable at around 90% since 2006. On the policy side, the EU's Packaging and Packaging Waste Directive requires at least 80% of ferrous metal packaging to be recycled by 2030, a target that tinplate in leading markets already exceeds. This regulatory tailwind keeps tinplate strongly positioned in procurement decisions across Western Europe.

Rising Demand for Food Items with Long Shelf Life

Tinplate creates a complete physical barrier against oxygen, light, and moisture. This is not a minor technical detail, but it directly addresses one of Europe's most prominent food system problems. The EU estimates that around 59 million tons of food waste are generated annually across the bloc. Tinplate cans, by keeping food shelf-stable for years without refrigeration, reduce spoilage throughout the supply chain.

It complies with the EU's Farm to Fork Strategy, which targets a 50% reduction in food waste by 2030. Unlike modified atmosphere packaging or flexible pouches, tinplate requires no cold chain, cutting energy costs for storage and transport. For processors of fish, vegetables, and ready meals, this makes tinplate a practical, not just a sustainable, choice.

Restraint - BPA Phase-Out May Push Up Coating Costs

For decades, BPA-based epoxy coatings were the default interior lining for tinplate food cans. They were cost-effective, durable, and chemically stable. That is now changing at a fast pace. Commission Regulation (EU) 2024/3190 came into force on January 20, 2025, banning BPA and its salts in food contact materials, including varnishes and coatings applied to metal cans. Transition periods give manufacturers until July 2026 for most single-use food contact articles, but the clock is running.

Switching to BPA-free polyester or acrylic coatings is costly and not straightforward. These alternatives behave differently with acidic products such as tomatoes, pickles, or fruit preserves, further leading to adhesion failures or taste transfer in some formulations. Small-scale can-makers across Western Europe face the steepest challenge, as they lack the research and development budgets to reformulate swiftly. Trade associations have responded critically, citing insufficient impact assessments, short transition periods, and a lack of exemptions for critical applications. These signals indicate that compliance pressure will likely weigh on margins for the near term.

Opportunity- Lightweighting Tinplate without Losing Structural Strength

The Western Europe tinplate packaging market is creating a new competitive advantage through material efficiency by using less steel per can while keeping performance intact. Germany's thyssenkrupp Rasselstein, the country's only tinplate manufacturer, is at the forefront. Its Rasselstein D&I Solid grade, developed for two-piece drawn and wall-ironed (D&I) food cans, enables up to 10% material savings by increasing axial stability by 20%. It allows for meaningful thickness reductions without compromising can integrity.

At METPACK 2026, the company also introduced a digital tool called the Canculator. It is integrated into its Packaging Steel App and built on finite element analysis as well as machine learning. It enables customers to calculate potential thickness reductions for their specific can dimensions within seconds. For high-volume can manufacturers, even small reductions in material usage can generate substantial cost savings, making this a highly attractive commercial innovation.

Emergence of High-Performance Tinplate for Aerosol Packaging

The aerosol segment is a surging end-use for tinplate in Western Europe, and materials innovation is keeping tinplate competitive against aluminium. At METPACK 2026, thyssenkrupp Rasselstein presented rasselstein CUP, short for Cup Ultimate Performance, a tinplate grade developed specifically for aerosol valve mounting cups.

Rasselstein CUP combines excellent formability with significantly higher strength and low earing, which matters as mounting cups undergo intense mechanical stress during pressure filling. Low earing means less material waste during the stamping process and high production line speeds. Improved tinplate grades that support quick throughput and tight tolerances give Western Europe-based producers a tangible advantage as demand extends.

Category-wise Analysis

Product Type Insights

Cans are predicted to lead with a share of approximately 38.5% in 2026 in Western Europe tinplate packaging market, as these provide high expandability and superior barrier protection, which is important for food and beverage products. Tinplate cans prevent light, oxygen, and contamination, helping extend shelf life without preservatives. This complies with strict EU food safety norms set by the European Food Safety Authority, which pushes brands toward reliable packaging formats such as cans. Also, cans fit well into automated high-speed filling lines, which reduces operational costs for large manufacturers.

Pails are estimated to be the fastest-growing segment in the forecast period, owing to rising demand from industrial and construction sectors, where bulk handling is demanded. Unlike cans, pails can carry larger volumes and are easier to transport and store on job sites. This is especially relevant in Western Europe, where infrastructure renovation projects are increasing under initiatives such as the European Commission’s renovation wave strategy. These projects require bulk paints, coatings, and adhesives, which are typically packed in metal pails.

End-use Industry Insights

The paints segment is anticipated to dominate with a share of nearly 52.2% in 2026, as the industry relies heavily on metal packaging for chemical stability and shelf life. Several solvent-based paints react with air or moisture, so tinplate containers help maintain product quality. This is important in Western Europe, where compliance with REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) regulations is strict. Metal packaging reduces contamination risks and ensures safe storage of volatile compounds.

The chemicals segment is expected to remain in the second position in 2026, owing to stringent rules revolving around hazardous material handling and transport. Regulations under REACH and CLP (Classification, Labelling and Packaging) require superior and leak-proof packaging. Tinplate containers meet these standards better than several other alternatives. This is pushing chemical manufacturers to shift toward metal packaging for solvents, lubricants, and specialty chemicals.

Country Insights

Germany Tinplate Packaging Market Trends

Germany is anticipated to dominate in 2026 with a share of nearly 38.4%, as it is Western Europe’s largest consumer and has the most advanced recycling infrastructure. The country alone consumed 1.3 million tons of tinplate in 2024, far more than any other Western European country. Its recycling efficiency for tinplate packaging reached 91% in 2023, the highest in the continent, which complies perfectly with national circular economy laws. The country also hosts leading tinplate producers and has well-established food and beverage industries that rely heavily on tinplate cans for shelf stability and safety.

Domestic manufacturers are actively investing in sustainable tinplate technologies, making it a hub for innovation.

France Tinplate Packaging Market Trends

In 2026, France will likely showcase the fastest growth and account for approximately 17.9% of the share in the Western Europe tinplate packaging market. Growth is attributed to exponential demand for canned foods and beverages, as well as superior government backing for circular economy initiatives. The France metal packaging market, including tinplate packaging, is experiencing steady growth, driven by increasing consumer demand for safe, durable, and extended shelf-life packaging solutions.

The country’s national packaging waste regulations now require high recycled content, compelling brands to switch to tinplate, which is infinitely recyclable without quality loss. Recent press releases from France’s Ministry of Ecological Transition highlight new incentives for metal packaging reuse in the food sector, validating this shift.

U.K. Tinplate Packaging Market Trends

A share of nearly 11.6% is expected to be recorded by the U.K. in 2026 in Western Europe tinplate packaging market. This growth is due to robust and diversified demand across packaging, automotive, and appliance sectors. Post-Brexit, the country has maintained strict food-safety standards that favor tinplate’s superior barrier properties against moisture and oxygen. Food-grade tinplate packaging and electronic components are broadening applications, though manufacturers face compliance challenges with evolving U.K. and EU regulatory shifts. The steady growth reflects a mature but stable market where tinplate remains the go-to for premium food cans and aerosol containers.

The Netherlands Tinplate Packaging Market Trends

The Netherlands is predicted to account for a share of nearly 8.7% in 2026, as it serves as Western Europe’s main logistics hub and has achieved 88% packaging recycling or reuse in 2024, well above the EU target of 65%. This exceptional performance is augmented by the Dutch Circular Netherlands 2030 strategy, which explicitly promotes metal packaging due to its high recyclability. The country’s strategic port infrastructure further allows easy import of tinplate and export of finished packaged goods, making it attractive for multinational food and beverage companies. Recent Verpact reports confirm that Dutch packaging companies are constantly adopting tinplate to meet circularity goals.

Spain Tinplate Packaging Market Trends

Spain is estimated to hold a share of approximately 6.8% in 2026 in Western Europe tinplate packaging market, owing to rising consumption of canned seafood, fruits, and vegetables, its traditional food export strengths, combined with tourism-backed demand for beverage cans. Spain-based food processors are now switching to tinplate to meet EU packaging waste directives that mandate high recycling rates by 2025. The country’s metal packaging industry is extending capacity to serve both domestic and Mediterranean markets, though growth is moderated by a smaller industrial base compared to Germany or France.

Belgium Tinplate Packaging Market Trends

Belgium is anticipated to be one of the key countries in Western Europe tinplate packaging market, with a share of approximately 5.9% in 2026. The country is faring well as a high-value niche player, using its position as the EU’s headquarters location and superior chemical/pharma sectors that use tinplate for specialty industrial packaging. Belgium’s recycling rate for metal packaging exceeds 85%, in line with EU averages, and its Antwerp port facilitates tinplate trade. The country focuses on premium applications such as cosmetic tins and pharmaceutical containers rather than mass food cans, which supports high margins despite small total volume.

Competitive Landscape

The Western Europe tinplate packaging market is highly fragmented, with competition spread across various multinational metal packaging companies, regional tinplate container manufacturers, and integrated steel producers. Players such as Trivium Packaging, Silgan Metal Packaging, Massilly Group, Colep Packaging, and ArcelorMittal maintain dominant regional footprints through extensive product portfolios and long-term relationships with food, beverage, industrial, and pharmaceutical customers.

Competition is increasingly centered on sustainability, lightweighting, and circular economy initiatives rather than pricing alone. Manufacturers are investing in thin tinplate gauges, novel protective coatings, and high-recyclability packaging formats to comply with Western Europe's strict packaging waste norms. Companies that can demonstrate low carbon footprints and high recycled-content usage are gaining an advantage, especially among food and beverage brands seeking to meet sustainability commitments.

Key Industry Developments:

- In May 2026, Metal Packaging Europe (MPE) declared the completion of a new Life Cycle Assessment (LCA) in 2025. Its LCA showed that tinplate cut emissions by 10% since 2022, while steel cans used 18% less electricity and became 13% lighter.

- In March 2026, Hubergroup Print Solutions introduced its Tinkredible MGA metal decoration ink. It is a mineral oil-free, bisphenol A-free, and PFAS-free low-migration ink series designed for monobloc and three-piece tinplate metal cans used in food and beverage packaging.

- In January 2026, Tata Steel Nederland commissioned a new production line for packaging steel at its IJmuiden facility, using its proprietary Trivalent Chromium Coating Technology (TCCT). It enables more sustainable production of packaging steel and already complies with future chemical-use legislation under EU REACH regulations.

Companies Covered in Western Europe Tinplate Packaging Market

- Silgan Metal Packaging

- Trivium Packaging

- KLANN Packaging GmbH

- ColepPackaging

- LK-PremiumPack GmbH

- Hoffmann Neopac AG

- ArcelorMittal

- LABRY S.A.

- The Massilly Group

- RLM Packaging Ltd.

- Emballator

- Blechwarenfabrik Limburg GmbH

- Roberts Metal Packaging

- Tinpac Ltd.

- Litochap

- Others

Frequently Asked Questions

The Western Europe tinplate packaging market is projected to be valued at US$67.3 million in 2026.

The Western Europe tinplate packaging market is expected to reach US$100.5 million by 2033.

Key market trends include increasing focus on recyclable steel packaging and lightweight tinplate development.

Cans are predicted to be the leading product type with a share of nearly 38.5% in 2026, as these support high-speed automated filling and comply with the high steel recycling rates of Western Europe.

The Western Europe tinplate packaging market is expected to grow at a CAGR of 5.9% from 2026 to 2033.

Silgan Metal Packaging, Trivium Packaging, KLANN Packaging GmbH, and ColepPackaging are a few key market players.