- Renewable Energy

- ASEAN Energy Transition Market

ASEAN Energy Transition Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

ASEAN Energy Transition Market By Solution Type (Renewable Energy, Energy Efficiency, Electrification, Hydrogen, Others), Technology (Energy Storage Systems, Smart Grids, Electric Vehicles (EVs), Carbon Capture & Storage (CCS), Others), End-user (Residential, Commercial, Utility Scale, Power & Utility, Transportation, Industrial, Others), and Country Analysis for 2026 - 2033

ASEAN Energy Transition Market Trends & Analysis

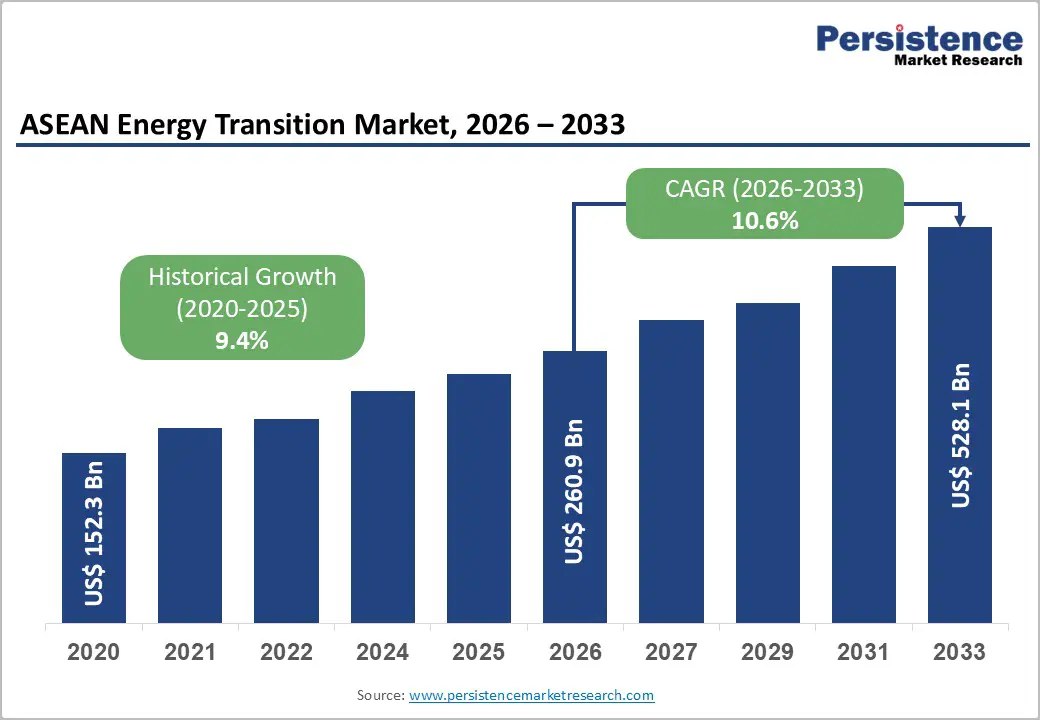

The ASEAN energy transition market size is projected at US$ 260.9 billion in 2026 and is projected to reach US$ 528.1 billion by 2033, growing at a CAGR of 10.6% between 2026 and 2033. This growth is fueled by increased deployment of renewable energy, electrification of transportation, industrial decarbonization, hydrogen investments, smart grid modernization, and global commitments to carbon neutrality and energy security.

Rise in power demand, accelerating net?zero pledges, and falling renewable technology costs are reshaping ASEAN’s power and fuel mix, with clean energy already requiring at least US$ 200 Bn in regional investment by 2030. Strong growth in solar, wind and EVs is being tempered by grid bottlenecks, fossil?fuel subsidies and fragmented regulations, yet policy roadmaps and sustainable finance initiatives are steadily improving bankability and unlocking private capital for large?scale transition projects.

Key Industry Highlights:

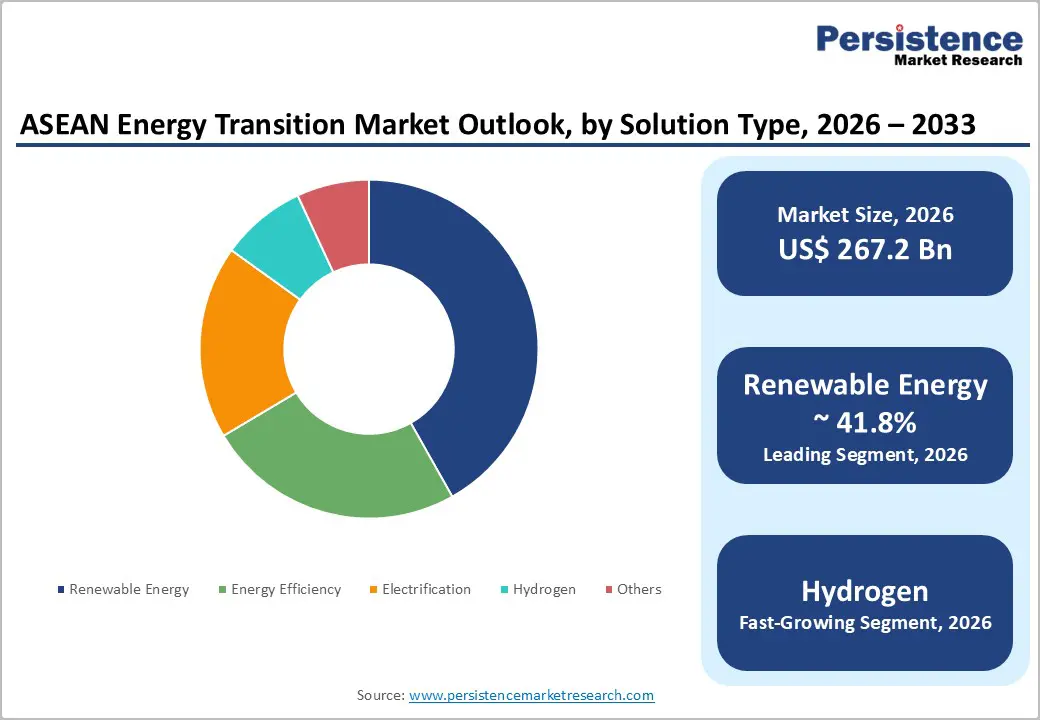

- Leading Solutions: Renewable energy leads solution types with 41.8% share in 2026, benefiting from strong solar and wind growth; Utility Scale assets dominate end?user demand with 24.9% share.

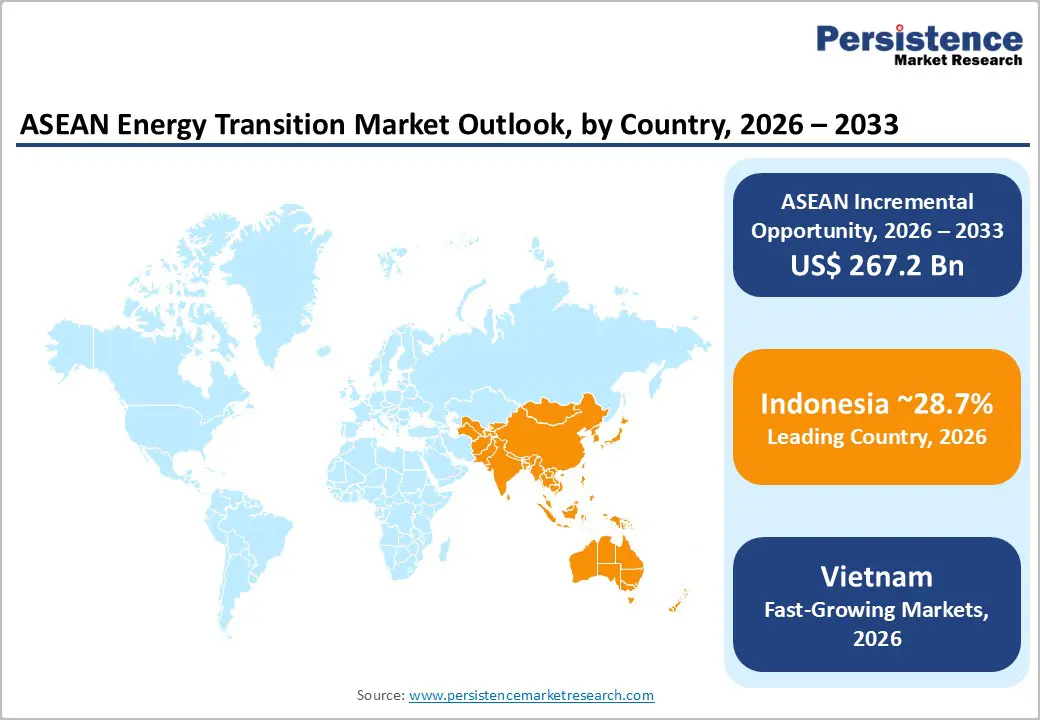

- Regional Dynamics: Indonesia leads with about 28.7% share, while Vietnam is poised for the fast-growth at roughly 13.1% CAGR. The Philippines holds 8% share but likely to achieve around 12.2% CAGR aided by rising renewables and manufacturing activity.

- Strategic Developments: Strategic moves, including multi?billion?peso capex plans by ACEN, large solar projects by Vena Energy, and PLN’s substantial renewable?capacity roadmap, are reshaping project pipelines and competitive positioning across ASEAN.

- Risk-Opportunity Balance: Persistent fossil?fuel subsidies, grid bottlenecks, and bankability constraints remain key risks, but expanding green?finance ecosystems (around US$ 3 Trn opportunity to 2030) and clear net?zero pathways underpin long?term, scalable growth.

Market Dynamics Analysis

Drivers - Accelerating Power Demand and Investment Gaps

Rapid urbanisation and industrialisation are pushing ASEAN’s electricity demand sharply higher, with Southeast Asia needing at least US$ 200 Bn in energy?sector investment by 2030, over three?quarters earmarked for clean energy to meet regional goals. Annual energy investment in 2016-2020 averaged US$ 70 Bn, of which less than US$ 30 Bn went to clean energy, underscoring a sizeable financing gap for renewables, storage and grids.

Academic analysis finds ASEAN must invest around US$ 27 billion per year in renewables alone to achieve its 23% renewables share target in primary energy supply by 2025, yet historically has attracted no more than US$ 8 billion annually into renewables, amplifying the urgency for private capital mobilisation. This gap directly supports multi?year growth in energy?transition solutions across generation, efficiency and electrification.

Net?zero Commitments and Regional Policy Roadmaps

Most major ASEAN economies have announced net?zero or carbon?neutrality targets, covering more than 80% of regional energy supply, and are raising renewable?power roles in national development plans, creating durable policy pull for transition technologies. Indonesia’s Long?Term Strategy for Low Carbon and Climate Resilience (LTS?LCCR) seeks deep power?sector decarbonisation towards net?zero around 2060, while Vietnam’s National Climate Change Strategy embeds a 2050 net?zero goal and caps total 2050 emissions at 185 MtCO?e.

The International Energy Agency (IEA) and partners estimate ASEAN must raise solar? and wind?power’s share of generation to about 23% by 2030 to align with a 2050 net?zero pathway, requiring roughly 164 GW of additional solar and 65 GW of wind capacity on top of existing installations. These quantified pathways directly underpin robust demand for renewable generation, grids, storage, EVs, hydrogen and CCS solutions over the forecast.

Restraints - Fossil?fuel Subsidies and Policy Inconsistency

Several ASEAN governments, including Indonesia, Malaysia, Thailand and Vietnam, allocate substantial public funds to fossil?fuel subsidies, artificially lowering coal, oil and gas prices relative to renewables and slowing switching in power and end?use sectors. A joint IEA-Imperial assessment highlights that renewable?power development remains among the slowest globally, with inconsistent policy signals, underdeveloped project pipelines and entrenched fossil?investment patterns weighing on clean?energy deployment. This policy misalignment raises demand risk and constrains revenue visibility for investors.

Grid Constraints and Project Bankability Challenges

Rapid solar and wind additions, especially in Vietnam and parts of the Philippines, have outpaced transmission expansion, leading to curtailment and pauses in new project approvals until grid upgrades catch up. In Vietnam, around 95% of solar capacity is concentrated in southern provinces with limited demand and grid capacity, while northern demand is surging, creating structural congestion that undermines plant load factors and cash flows. Similar constraints, coupled with complex permitting and off?taker credit concerns, limit the number of bankable projects reaching financial close across ASEAN.

Opportunities - Large?scale Renewables and Grid Modernisation

ASEAN recorded an average 43% annual growth in solar and wind generation between 2015 and 2022, yet combined solar and wind still account for a modest share of total power output, implying significant headroom for expansion. IEA scenarios indicate that achieving a 23% solar? and wind?generation share by 2030 will require more than 200 GW of new variable renewable capacity in Southeast Asia, implying tens of billions of dollars of annual capex into utility?scale solar, onshore/offshore wind and hybrid projects.

Transmission and distribution investments, including smart grids, high?voltage interconnections and digital grid?management systems, are equally critical, with regional analysis stressing that grid interconnectivity is “critical to ASEAN’s energy transition.” Vendors offering integrated solutions, combining generation, storage, grid?stability technologies and advanced forecasting, can capture a substantial portion of the US$ 267.21 Bn incremental ASEAN energy?transition opportunity between 2026 and 2033, based on the market’s expected value increase over the period (US$ 528.07 Bn minus US$ 260.86 Bn).

Electrification, EV Ecosystems and Energy?efficiency Solutions

Electrification of transport and industry is emerging as a major decarbonisation lever, with Vietnam’s net?zero pathway attributing 78% of emissions abatement through mid?century to clean power, carbon capture and energy efficiency, and the remainder to electrification, bioenergy and hydrogen. The Philippines and Indonesia are both promoting EV adoption and local assembly while tightening efficiency standards in buildings and industry, creating cross?sectoral demand for charging infrastructure, smart?metering, demand?response platforms and high?efficiency equipment.

As ASEAN economies scale EV and heat?pump deployment and expand mass transit, the addressable market for associated infrastructure and services grows quickly, particularly in dense urban clusters. Players able to combine Energy efficiency, electrification and energy storage systems into value?based offerings for commercial and industrial customers will be positioned to capture a meaningful share of the projected multi?hundred?billion?dollar market expansion through 2033, reinforced by corporate decarbonisation commitments and green?finance frameworks.

Category wise Analysis

Solution Type Insights

Renewable energy is the leading solution type, accounting for 41.8% of ASEAN energy?transition revenues in 2026, supported by strong growth in solar, wind, hydropower and geothermal capacity, as well as supportive policy targets and power?sector investment commitments. Compared with Energy efficiency, electrification, hydrogen, and others, renewables benefit from clearer regulatory frameworks and mature financing structures, suggesting continued dominance; however, efficiency and electrification may gain share as grids modernise and end?use decarbonisation accelerates.

Hydrogen is the fastest?growing solution segment, expected to expand at about 20.8% CAGR between 2026 and 2033 as pilot projects in industrial clusters, refineries, and transport corridors scale up and as regional strategies integrate hydrogen and ammonia into long?term power?sector planning.

Technology Analysis

Within technology, electric vehicles (EVs) represent the leading segment with around 29.2% share of technology?driven energy?transition revenues in 2026, reflecting strong EV sales momentum, charging?infrastructure build?out, and broader electrification of transport in key ASEAN economies. EVs currently outpace Energy storage systems, smart grids, and CCS in monetisation due to direct consumer uptake and fleet?transition programs, though grid and storage investments are expected to follow as variable renewables increase their penetration.

Carbon Capture & Storage (CCS) is projected to be the fastest?growing technology segment, with an estimated 14.7% CAGR over 2026 - 2033, driven by industrial?decarbonisation roadmaps in Indonesia and Vietnam, national energy master plans that explicitly include CCS targets, and emerging carbon?management business models partnering utilities, industrial emitters, and technology providers.

End?user Insights

On the demand side, utility-scale projects, including large solar parks, wind farms, and grid?connected storage, hold the leading position with a 24.9% share of ASEAN energy?transition revenues in 2026, reflecting the central role of utility?scale assets in national capacity?expansion plans. These projects benefit from sovereign or utility off?take agreements and multilateral financing, giving them scale advantages over residential, commercial, power & utility, transportation, industrial, and others segments, although distributed generation and behind?the?meter solutions are steadily emerging.

Transportation is the fast?growing end?user segment, projected to expand at roughly 15% CAGR between 2026 and 2033, fueled by EV adoption, public?transport electrification, and fuel?efficiency standards that reward clean mobility solutions across two?wheelers, passenger vehicles, buses, and logistics fleets.

Country Insights

Indonesia Energy Transition Market Trends

Indonesia holds roughly 28.7% of ASEAN energy?transition spending, about US$ 75 Bn, driven by its large population, rising electricity demand, and ambitious, though challenging, net?zero and renewable?energy targets, underpinned by national low?carbon and power?sector roadmaps.

Java?Bali Energy Transition Market Trends

The Java?Bali system accounts for approximately 70% of Indonesia’s national electricity demand, concentrating much of the country’s renewable?energy and grid?modernisation investment, including new solar, wind, hydropower, and geothermal projects led by state utility PLN and private IPPs. This dense load centre will remain the largest sub?market for transition solutions, particularly for utility?scale renewables, smart grids, and EV infrastructure.

Beyond Java?Bali, regions such as Sumatra, Sulawesi, and Kalimantan are attracting growing investment in renewables, microgrids, and interconnections, supported by resource endowments and industrial?cluster development in mining and processing. These areas offer opportunities for hybrid systems, off?grid solutions, and green?industrial projects aligned with Indonesia’s industrial decarbonisation roadmap.

Vietnam Energy Transition Market Trends

Vietnam’s energy market is likely to achieve at a significant pace, with an estimated 13.1% CAGR and about 17.5% share of ASEAN energy?transition spending, roughly US$ 45 Bn, driven by rapid solar and wind deployment, strong manufacturing growth and a 2050 net?zero commitment.

Southern Vietnam Energy Transition Market Trends

Southern Vietnam hosts the majority of the country’s installed solar capacity, up to 42% of installed capacity in some southern provinces, and a large share of wind projects, making it the core regional hub for utility?scale renewables, storage and grid?reinforcement investments. Despite challenges, this region remains central to Vietnam’s clean?power expansion and export?oriented industrial clusters.

Northern and central regions are seeing rising demand and industrial relocation, yet currently face limited renewable capacity and grid constraints, creating strong opportunities for new generation, transmission upgrades and cross?regional power flows. As Vietnam implements it’s Just Energy Transition Partnership and updates its power development plans, these regions will increasingly attract investment into diversified renewables, grid infrastructure and flexibility solutions.

Philippines Energy Transition Market Insights

The Philippines currently holds around 8% share of ASEAN energy?transition spending, with a relatively modest base but a strong 12.2% growth rate, supported by rising power demand, high renewable resource potential and private?sector?led project pipelines.

Luzon Energy Transition Market Trends

The Luzon grid accounts for about 71.5% of national electricity consumption, making it the dominant demand centre and primary destination for new solar, wind, and storage investments led by utilities and independent power producers. Renewable energy already accounts for around 29% of total installed capacity nationally, with Luzon hosting major hydropower, geothermal, and solar assets, alongside emerging battery?storage projects.

Visayas and Mindanao, while smaller in demand, are increasingly important for distributed renewables and grid?stability projects, with growing industrial loads and electrification needs. These regions present opportunities for hybrid systems, microgrids and community?level energy access solutions, especially where extending large?scale grid infrastructure is costly or delayed.

Competitive Landscape

The ASEAN energy?transition market is moderately concentrated around large utilities and regional renewable?energy platforms, alongside numerous local developers and technology providers across solar, wind, storage and EV infrastructure. Market leaders differentiate through scale, cross?border portfolios, access to green finance, and proven execution in complex policy environments, while new business models such as corporate PPAs and distributed energy services are gaining traction.

Dominant strategic themes include innovation in renewables plus storage hybrids, cost leadership via scale and localisation, and market expansion into high?growth ASEAN countries through partnerships, M&A and platform investments, with players aligning portfolios to national net?zero targets and tightening ESG expectations.

Strategic Developments:

- In April 2024, ACEN announced around PHP 72 Bn in capital expenditures for 2024 to expand renewable?energy projects in the Philippines and abroad, supporting its plan to reach 20 GW of renewable capacity by 2030 and 100% renewables by 2025.

- In February 2026, ACEN Corporation completed the consolidation of its India renewables platform to 100% ownership, strengthening control over a 1.06 GW portfolio and a nearly 7 GW development pipeline, supporting faster renewable expansion across Asia-Pacific markets.

- In November 2024, Indonesia’s PLN detailed plans to add 28 GW of solar and wind, 31 GW of hydropower and geothermal, and 21 GW of gas capacity by 2040, aligning its portfolio with a 75% renewables and 25% gas mix, and creating substantial equipment and services demand.

- January 2025 - Vietnam net?zero investment opportunity: In January 2025, BloombergNEF estimated that achieving Vietnam’s 2050 net?zero target requires over US$ 2.4 Trn in cumulative investment, with clean power, energy efficiency, and CCS accounting for most emissions abatement, underlining long?term opportunities across the ASEAN energy?transition value chain.

Companies Covered in ASEAN Energy Transition Market

- ACEN Corporation

- Vena Energy

- B.Grimm Power PCL

- Gulf Energy Development PCL

- BCPG PCL

- PLN (Perusahaan Listrik Negara)

- Electricity of Vietnam (EVN)

- Meralco

- AboitizPower

- Sembcorp Industries

- First Gen Corporation

- Other Players

Frequently Asked Questions

The ASEAN energy transition market size is projected to reach about US$ 260.9 Bn in 2026, expanding to approximately US$ 528.1 Bn by 2033 as clean‑energy and decarbonisation investments accelerate.

Key drivers include rapidly rising electricity demand, national net‑zero and renewables targets, falling costs for solar, wind, storage and EV technologies, and a sizeable investment gap requiring at least US$ 200 Bn in energy‑sector investment by 2030.

Between 2026 and 2033, the ASEAN Energy Transition Market is expected to grow at a CAGR of about 10.6%, reflecting robust expansion across renewable generation, grid infrastructure, electrification, hydrogen, CCS and efficiency solutions.

Major opportunities span utility‑scale solar and wind plus grid modernisation, EV ecosystems and energy‑efficiency retrofits, and emerging hydrogen and CCS platforms for industrial decarbonisation, collectively representing an incremental opportunity of roughly US$ 267.2 Bn during 2026 - 2033.

Key players include ACEN Corporation, Vena Energy, B.Grimm Power, Gulf Energy Development, BCPG, PLN, EVN, Meralco, AboitizPower, Sembcorp Industries and First Gen, alongside global technology providers in renewables, storage, EVs, hydrogen and CCS.