- Specialty & Fine Chemicals

- U.S. Smart Greenhouse Market

U.S. Smart Greenhouse Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Smart Greenhouse Market by Product Type (Hydroponics, Non-Hydroponics), Offerings (Hardware, Software & Services), Component (Sensors & Monitoring Systems, HVAC & Climate Control Systems, LED Grow Lighting Systems, Irrigation & Fertigation Systems, Misc.), End User (Commercial Growers, Research & Educational Institutes, Retail Gardens, Misc.), and Regional Analysis for 2026 - 2033

U.S. Smart Greenhouse Market Size and Trends Analysis

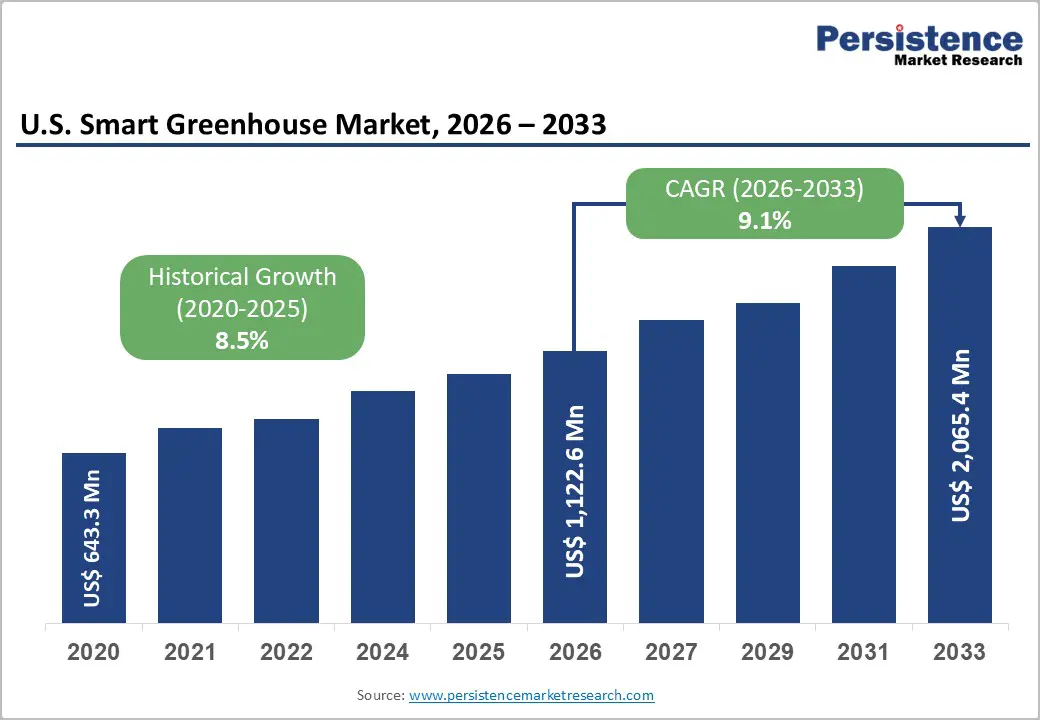

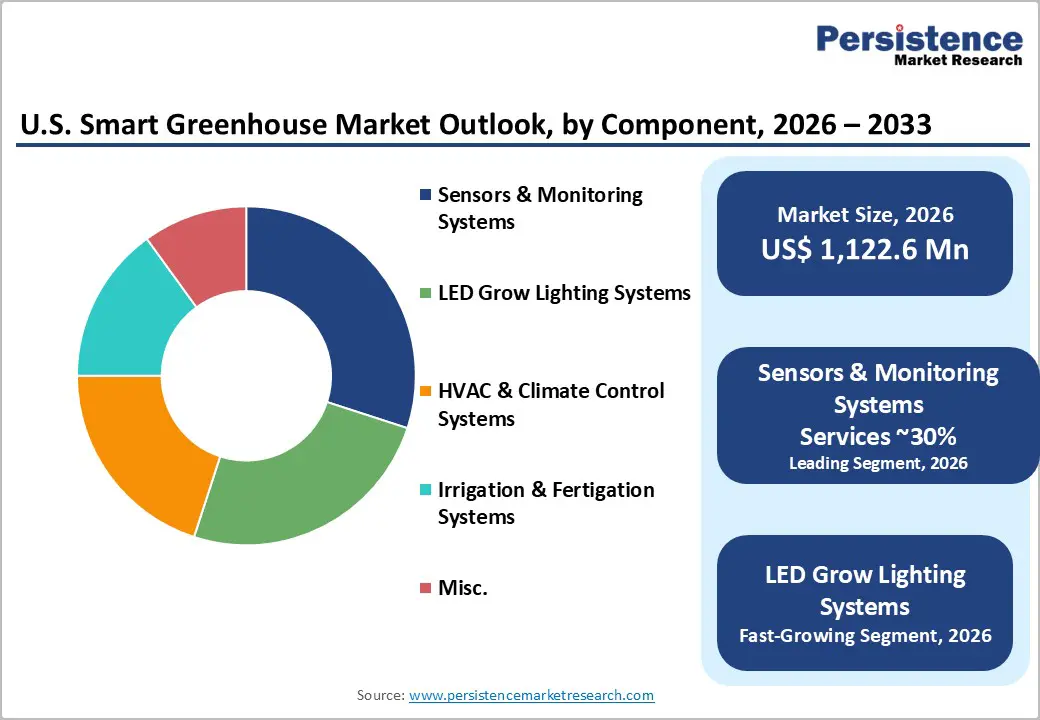

The U.S. smart greenhouse market size was valued at US$ 1,122.6 million in 2026 and is projected to reach US$ 2,065.4 million by 2033, growing at a CAGR of 9.1% between 2026 and 2033. The market recorded a historical CAGR of 8.5% from 2020, when it was valued at US$ 684.3 Mn, reflecting consistent structural momentum in controlled environment agriculture (CEA).

Primary demand drivers include federal policy investment through the USDA's Partnerships for Climate-Smart Commodities initiative, widespread IoT and sensor deployment across agricultural operations, and a measurable shift toward localised, resource-efficient food production systems. Smart greenhouse facilities demonstrate quantifiable efficiency advantages, including the capacity to yield up to 30 times more produce per acre while consuming 90% less water and utilizing 97% less land, reinforcing long-term investment rationale across commercial, research, and institutional end-user segments.

Key Industry Highlights:

- Hydroponics-Based Smart Greenhouses Lead Market Share: Hydroponics systems dominate the U.S. Smart Greenhouse Market with 65% share, driven by high adoption of controlled environment agriculture, vertical farming expansion, and precision yield optimisation.

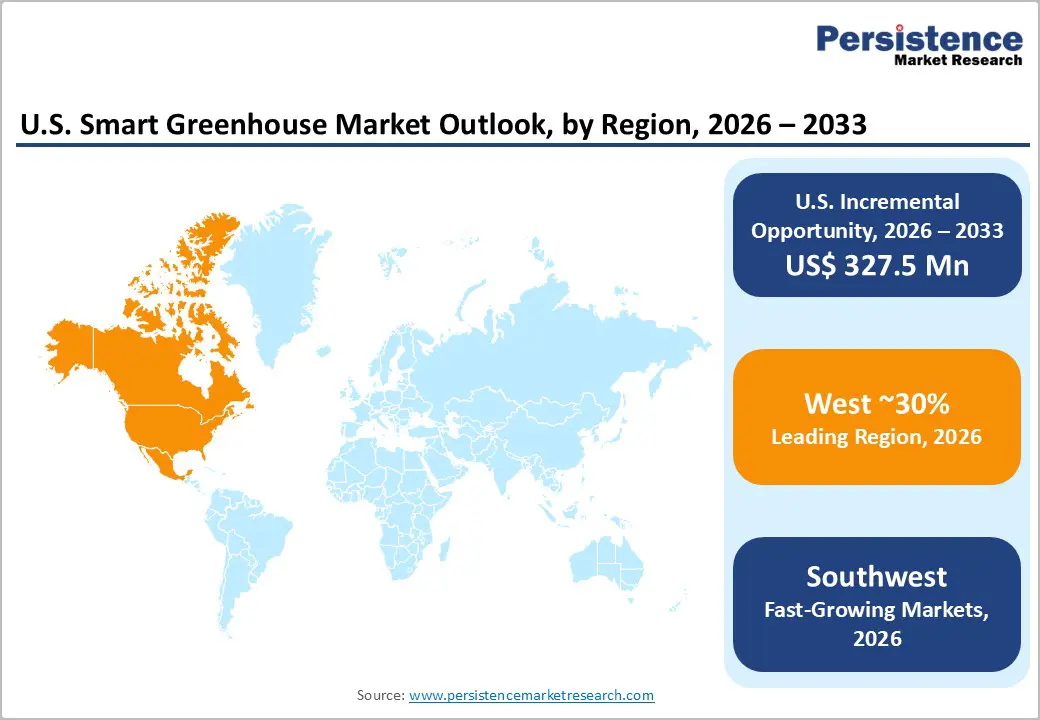

- West Region Dominates Geographic Demand: The West leads with 30% market share, supported by California’s Central Valley speciality crop dominance and strong agri-tech integration across high-value horticulture production systems.

- Sensors & Monitoring Systems Core Technology Backbone: Sensors and monitoring systems hold 30% share, driven by IoT convergence, enabling real-time climate tracking, predictive analytics, and automated greenhouse control systems.

- Commercial Growers Anchor End-user Demand: Commercial growers account for 72% market share, reflecting large-scale deployment of smart greenhouse infrastructure for high-efficiency, high-yield, and year-round production cycles.

- Federal Climate-Smart Investment Accelerates Adoption: The USDA’s $3 billion Climate-Smart Commodities initiative is accelerating adoption of sensor-based, data-driven greenhouse systems across more than 60,000 farms nationwide.

- AI & IoT Integration Driving Structural Transformation: Rapid integration of AI, IoT, and cloud-based monitoring systems is transforming greenhouses into self-optimising production environments with predictive crop management capabilities.

| Key Insights | Details |

|---|---|

| U.S. Smart Greenhouse Market Size (2026E) | US$ 1,122.6 Mn |

| Market Value Forecast (2033F) | US$ 2,065.4 Mn |

| Projected Growth (CAGR 2026 to 2033) | 9.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.5% |

DRO Analysis

Drivers - Federal Investment in Climate-Smart Agriculture Infrastructure

Federal agricultural policy has become a direct structural catalyst for the U.S. Smart Greenhouse Market. In January 2025, the U.S. Department of Agriculture (USDA) advanced its Partnerships for Climate-Smart Commodities initiative, committing over $3 billion across approximately 140 pilot projects to promote climate-resilient agricultural practices.

The program explicitly supports controlled environment agriculture by promoting technologies that enhance greenhouse gas monitoring, optimise resource utilisation, and improve yield predictability capabilities central to smart greenhouse operations. By engaging in over 60,000 farms and fostering collaboration with nearly 100 universities, this initiative accelerates the deployment of sensor-based, data-driven greenhouse systems at scale. The sustained federal commitment establishes stable institutional demand for smart greenhouse technology providers and reinforces CEA as a federally validated platform for sustainable food production in the United States.

IoT and Sensor Technology Convergence in Precision Crop Management

The proliferation of IoT-enabled sensor networks has become a foundational demand driver for the U.S. Smart Greenhouse Market. Agriculture has emerged as one of the most active sectors for IoT adoption, with sensors measuring temperature, humidity, CO2 concentration, light intensity, soil moisture, water pH, and electrical usage now integrated through energy-efficient wireless protocols including LoRa and LTE-M. These connected systems enable remote control of irrigation, ventilation, and lighting via cloud-based platforms accessible through mobile and desktop devices.

In February 2024, Sensaphone launched its Sentinel™ remote monitoring system, enabling continuous multi-parameter greenhouse environment tracking, real-time alerts, and predictive equipment maintenance via cloud infrastructure. Innovations such as battery-free sensors and AI-powered analytics have further strengthened the value proposition, transforming greenhouse facilities into self-optimising production environments with substantially reduced manual labour requirements.

Demographic Transition and Structural Demand for Technology-Assisted Farming

Demographic shifts within U.S. agriculture are generating structural demand for automated, knowledge-embedded farming platforms that support the U.S. Smart Greenhouse Market. With approximately 1.9 million farms, of which nearly 95% are family-operated, and a single U.S. farm now feeding approximately 169 people annually, scalable productivity is a defining operational requirement. Nearly 30% of farmers are new entrants with under 10 years of experience, and the average farmer age stands at 47 years, signalling a generational transition that favours technology-assisted operations.

Geographic concentration of crop production in California's Central Valley and the Midwest Corn Belt creates supply chain vulnerabilities for fresh produce distribution to urban centres. Smart greenhouse platforms, including containerised urban farms and hybrid vertical systems, address these structural inefficiencies by enabling proximate production with consistent, data-verified yield outcomes.

Restraint - Fixed Voice Services Revenue Structural Decline

The full deployment of integrated smart greenhouse systems demands significant upfront capital investment across sensors, HVAC infrastructure, LED lighting, automated irrigation, and software integration. For smaller and mid-scale operators, this poses a substantial barrier, particularly given that U.S. farmers typically receive only approximately 15 cents of every consumer dollar, with the remainder captured by processing and distribution intermediaries. Long payback horizons for technology-intensive greenhouse infrastructure constrain adoption beyond large commercial operators, slowing market penetration across the broader agricultural base and limiting the addressable customer pool for technology vendors in the near term.

Skilled Labour Shortages and Technology Integration Challenges

Effective operation of smart greenhouse systems requires proficiency in data analytics, IoT platform management, and automation system oversight competencies not uniformly distributed across the U.S. agricultural workforce. With nearly 30% of active farmers classified as new entrants, the transition to sensor-driven, fully automated greenhouse environments face operational resistance and knowledge gaps. Integration complexity between legacy greenhouse infrastructure and modern IoT platforms further extends deployment timelines and increases the total cost of adoption. These factors collectively constrain the pace at which potential customers can operate smart greenhouse investments, adding technical risk to project economics.

Opportunities - AI-Driven Crop Intelligence and Predictive Farming Platforms

AI-driven crop management represents a high-impact opportunity within the U.S. Smart Greenhouse Market, specifically by converting farming expertise into scalable, algorithm-embedded operational systems. Organisations like Yanmar have demonstrated this model, deploying edge computing and cloud-based data storage to optimise growing conditions through predefined algorithms and predictive crop maturity estimation, enabling precise harvesting schedules and proactive supply chain coordination. This approach transforms agriculture from an intuition-dependent practice into a structured, data-verifiable process accessible to both experienced and new farming entrants.

For the U.S. market specifically, this opportunity is reinforced by the demographic reality that nearly 30% of farmers are new entrants seeking accessible, high-performance operational frameworks. AI-powered image analysis, real-time environmental optimisation, and automated irrigation and climate adjustment reduce manual labour requirements while improving yield consistency across crop cycles. As USDA-supported university partnerships accelerate applied research in AI greenhouse systems engaging nearly 100 academic institutions, commercial-scale deployment pathways for AI-integrated smart greenhouse platforms are strengthening in both depth and geographic distribution across the United States.

Renewable Energy Integration and Closed-Loop Sustainability Systems

The alignment of smart greenhouse technology with renewable energy and resource-recirculating infrastructure presents a commercially actionable opportunity for the U.S. Smart Greenhouse Market, particularly as federal climate policy directs capital toward sustainable agriculture. Projects such as the Omega Centre for Sustainable Living demonstrate operationally validated models of smart greenhouse systems embedded within closed-loop sustainability infrastructure, recycling water and energy inputs while maintaining high crop productivity with minimal external resource dependency.

From a resource efficiency standpoint, smart greenhouse facilities using hydroponic systems, LED lighting, and real-time monitoring can achieve up to 30 times more produce per acre while consuming nearly 90% less water and 97% less land compared to conventional farming. In the context of ongoing water scarcity pressures across major U.S. agricultural regions, particularly California's Central Valley and federal mandates for climate-smart production practices, energy-optimised greenhouse systems represent a convergence point between operational cost reduction and institutional investment. This positions sustainable smart greenhouse deployments as high-priority assets for institutional capital, corporate food-sector investors, and ESG-aligned procurement programs across the United States.

Category-wise Analysis

Product Type Insights

Hydroponics holds approximately 65% of the U.S. Smart Greenhouse Market in 2026, underpinned by its precision nutrient delivery, compatibility with multi-layer vertical configurations, and integration with AI-based crop management platforms. Hydroponic systems eliminate soil variability and enable year-round crop cycles, making them the preferred method for commercial-scale CEA operators prioritising yield consistency and resource efficiency. Quantifiable operational advantages, including potential for up to 30 times more produce per acre and 90% lower water consumption, make hydroponic smart greenhouse systems the dominant choice for commercial growers targeting high-throughput urban and peri-urban production environments across the United States.

Non-hydroponic cultivation approaches, including soil-based, aeroponic, and aquaponic systems, are gaining accelerated adoption as operators seek cultivation flexibility and lower initial system complexity within the U.S. Smart Greenhouse Market. Aquaponic integrated systems that combine fish and plant production align with closed-loop sustainability frameworks supported by federal climate-smart agriculture funding. The Omega Centre for Sustainable Living demonstrates the operational scalability of non-hydroponic closed-loop production, while Local Bounti's hybrid Stack & Flow architecture incorporates non-hydroponic techniques within a commercially scalable structure. As new farming entrants seek accessible, lower-capital-intensity entry points into CEA, non-hydroponic configurations present a strategic growth pathway for technology providers targeting the broader U.S. market.

End-user Insights

Commercial growers represent approximately 72% of the U.S. Smart Greenhouse Market in 2026, reflecting the scale of capital commitment that large produce operators have directed toward precision agriculture infrastructure. Commercial operations evaluate smart greenhouse investments against measurable ROI metrics, yield per square foot, water and energy consumption, and labour efficiency, all of which smart greenhouse platforms directly optimise. Companies like Gotham Greens and Local Bounti illustrate how commercial CEA deployments are scaling from pilot operations to multi-state production networks. The USDA's climate-smart agriculture initiative, which engages over 60,000 farms, further strengthens procurement incentives for commercial operators adopting automated monitoring, precision fertigation, and climate management systems at production scale.

Research and educational institutions are demonstrating the fastest adoption trajectory among end-user categories, propelled by federal funding mechanisms and the USDA's formal engagement of nearly 100 universities under its climate-smart agriculture initiative. These institutions serve as primary testbeds for next-generation greenhouse technologies piloting AI-driven crop optimisation, advanced sensor networks, and energy-integrated cultivation architectures before commercial deployment. Yanmar's model of converting tacit crop knowledge into structured algorithms through academic collaboration exemplifies the research-to-commercial pathway. As new farmer entrants increasingly use academic greenhouse facilities for hands-on training in automated CEA environments, research institutions are simultaneously serving as both innovation hubs and talent development pipelines within the U.S. Smart Greenhouse Market.

Competitive Landscape

The U.S. Smart Greenhouse Market is characterised by a moderately consolidated-to-oligopolistic competitive structure, with a limited number of global and regional players dominating advanced automation, climate control, and precision agriculture solutions. Leading companies such as Nexus Corporation, Argus Control Systems, Rough Brothers Inc., Netafim Ltd., Heliospectra AB, and Lumigrow Inc. hold strong positions through integrated hardware–software offerings. These firms benefit from high entry barriers driven by capital-intensive R&D, IoT integration, and AI-enabled greenhouse technologies.

Specialised players focusing on lighting systems, sensors, and irrigation solutions create a layered competitive environment. While large players shape system-level deployments, niche innovators continue to introduce disruption through sensor-driven and AI-based farming technologies.

Key Developments:

- In January 2025, the U.S. Department of Agriculture (USDA) advanced its Partnerships for Climate-Smart Commodities initiative, committing over $3 billion across 140 pilot projects focused on sustainable agriculture and climate resilience. The program strongly supports the adoption of controlled environment agriculture (CEA), including smart greenhouse systems, by promoting precision monitoring and data-driven farming practices. This large-scale federal initiative is accelerating the integration of sensor-based monitoring, resource optimisation, and yield prediction technologies across U.S. agriculture.

- On February 29, 2024, Sensaphone introduced its Sentinel™ remote monitoring system, designed for continuous tracking of critical greenhouse conditions such as temperature, humidity, CO2 levels, soil moisture, and electrical usage. The system provides real-time alerts via phone, text, or email when environmental parameters move outside optimal ranges, enabling immediate corrective action. This enhances operational reliability in controlled environment agriculture (CEA).

Companies Covered in U.S. Smart Greenhouse Market

- Nexus Corporation

- Argus Control Systems Limited

- Certhon

- Rough Brothers, Inc. (Prospiant)

- GreenTech Agro LLC

- Sensaphone

- Heliospectra AB

- LumiGrow, Inc.

- Signify

- Growlink

- Netafim

Frequently Asked Questions

The U.S. Smart Greenhouse Market is projected to be valued at US$ 1,122.6 Mn in 2026.

The Hydroponics segment is expected to account for approximately 30% of the U.S. Smart Greenhouse Market by Product Type in 2026.

The U.S. smart greenhouse market is expected to witness a CAGR of 9.1% from 2026 to 2033.

The U.S. Smart Greenhouse Market growth is driven by strong federal support through the USDA’s $3 billion Climate-Smart Commodities initiative, rapid adoption of IoT-enabled sensor networks and AI-based remote monitoring systems (e.g., Sensaphone Sentinel™), and a structural shift toward technology-driven farming due to demographic transition, farm consolidation, and the need for higher productivity per acre amid geographically concentrated crop production in regions like California and the Midwest.

The key market opportunities in the U.S. Smart Greenhouse Market include the expansion of AI-driven crop intelligence and predictive farming platforms that enable data-based automation, yield forecasting, and labor-efficient greenhouse management, along with the growing scope for renewable energy-integrated and closed-loop sustainable greenhouse systems that significantly improve water efficiency, reduce land usage, and align with federal climate-smart agriculture initiatives and ESG-driven investment priorities.

Key players in the Smart Greenhouse Market include Nexus Corporation, Argus Control Systems, Rough Brothers Inc., Netafim Ltd., Heliospectra AB, and Lumigrow Inc.