- Executive Summary

- Global Titanium Alloy Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Defense Industry Overview

- Global Automotive Industry Overview

- Global EV Sales by Region

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Titanium Alloy Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Titanium Alloy Market Outlook: Microstructure

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Microstructure, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Microstructure, 2026-2033

- Alpha & Near-Alpha Alloys

- Alpha-Beta Alloys

- Beta Alloys

- Other

- Market Attractiveness Analysis: Microstructure

- Global Titanium Alloy Market Outlook: End-use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by End-use Industry, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Aerospace & Defense

- Medical

- Automotive and Shipbuilding

- Industrial & Chemical Processing

- Power Generation

- Other

- Market Attractiveness Analysis: End-use Industry

- Global Titanium Alloy Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Titanium Alloy Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Microstructure, 2026-2033

- Alpha & Near-Alpha Alloys

- Alpha-Beta Alloys

- Beta Alloys

- Other

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Aerospace & Defense

- Medical

- Automotive and Shipbuilding

- Industrial & Chemical Processing

- Power Generation

- Other

- Europe Titanium Alloy Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Microstructure, 2026-2033

- Alpha & Near-Alpha Alloys

- Alpha-Beta Alloys

- Beta Alloys

- Other

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Aerospace & Defense

- Medical

- Automotive and Shipbuilding

- Industrial & Chemical Processing

- Power Generation

- Other

- East Asia Titanium Alloy Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Microstructure, 2026-2033

- Alpha & Near-Alpha Alloys

- Alpha-Beta Alloys

- Beta Alloys

- Other

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Aerospace & Defense

- Medical

- Automotive and Shipbuilding

- Industrial & Chemical Processing

- Power Generation

- Other

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by , 2026-2033

- South Asia & Oceania Titanium Alloy Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Microstructure, 2026-2033

- Alpha & Near-Alpha Alloys

- Alpha-Beta Alloys

- Beta Alloys

- Other

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Aerospace & Defense

- Medical

- Automotive and Shipbuilding

- Industrial & Chemical Processing

- Power Generation

- Other

- Latin America Titanium Alloy Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Microstructure, 2026-2033

- Alpha & Near-Alpha Alloys

- Alpha-Beta Alloys

- Beta Alloys

- Other

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Aerospace & Defense

- Medical

- Automotive and Shipbuilding

- Industrial & Chemical Processing

- Power Generation

- Other

- Middle East & Africa Titanium Alloy Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Microstructure, 2026-2033

- Alpha & Near-Alpha Alloys

- Alpha-Beta Alloys

- Beta Alloys

- Other

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Aerospace & Defense

- Medical

- Automotive and Shipbuilding

- Industrial & Chemical Processing

- Power Generation

- Other

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- VSMPO-AVISMA Corporation

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- ATI Inc.

- TIMET

- Precision Castparts Corp.

- Howmet Aerospace Inc.

- Toho Titanium Co., Ltd.

- OSAKA Titanium Technologies Co., Ltd.

- Kobe Steel, Ltd.

- Western Superconducting Technologies Co, Ltd. (WST)

- Baoji Titanium Co. Ltd.

- Hermith GmbH

- VSMPO-AVISMA Corporation

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Metals & Minerals

- Titanium Alloy Market

Titanium Alloy Market Size, Share, and Growth Forecast 2026 - 2033

Titanium Alloy Market by Microstructure (Alpha & Near-Alpha Alloys, Alpha-Beta Alloys, Beta Alloys, Other), Industry (Aerospace & Defense, Medical, Automotive and Shipbuilding, Industrial & Chemical Processing, Power Generation, Other), and Regional Analysis for 2026 - 2033

Titanium Alloy Market Size and Trend Analysis

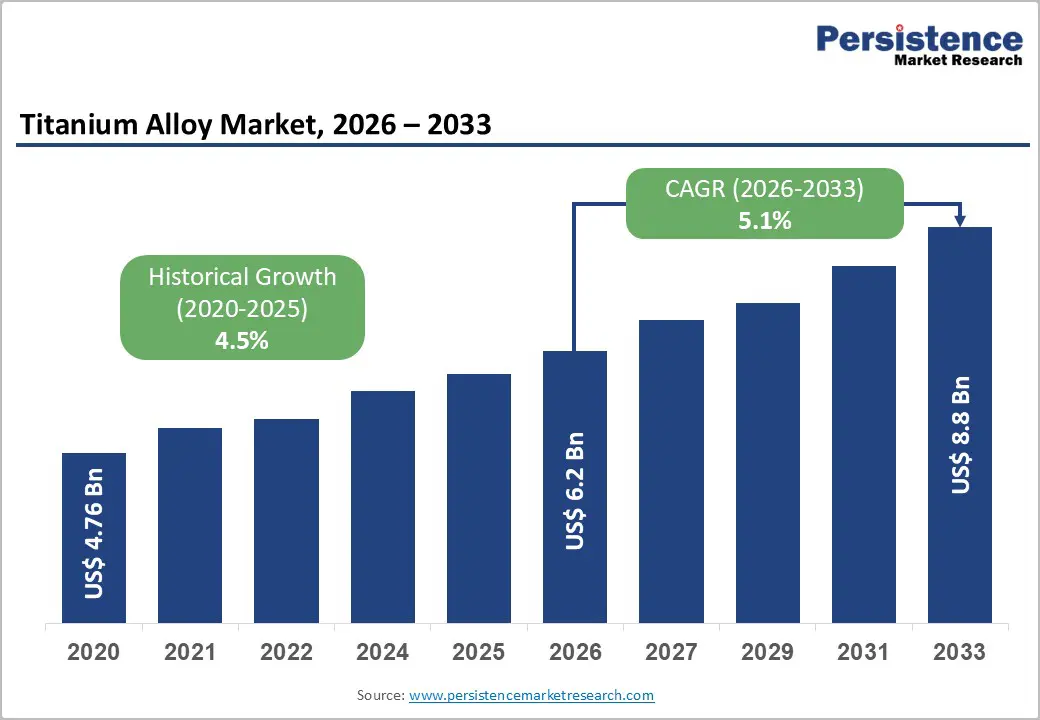

The global titanium alloy market is valued at US$ 6.2 Bn in 2026 and is projected to reach US$ 8.8 Bn by 2033, growing at a CAGR of 5.1% over 2026 - 2033.

The market's robust trajectory is primarily propelled by the accelerating pace of global commercial aircraft production, where titanium alloys are indispensable for airframes, engine components, and landing gear due to their unmatched strength-to-weight ratio. Concurrently, a rapidly aging global population is driving sustained demand for orthopedic and dental implants, where titanium's biocompatibility and osseointegration properties make it the material of choice. Growing defense modernization budgets across major economies, coupled with industrial applications in chemical processing and power generation, further anchor broad-based demand growth across the forecast period.

Key Market Highlights

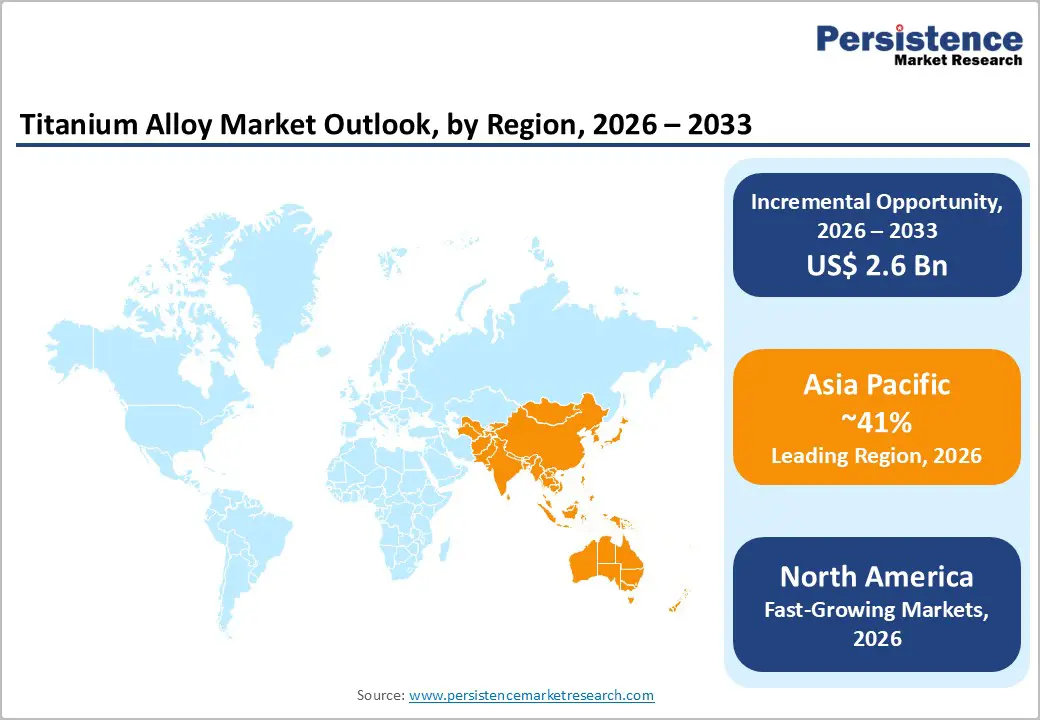

- Leading Region: Asia Pacific leads the global Titanium Alloy market with approximately 41% share, driven by China's dominant role in titanium production and rapidly expanding aerospace and defense programs in China, Japan, and India.

- Fastest Growing Region: North America is the fastest growing region, driven by the U.S., as the most technologically advanced and commercially significant region. Its growth is supported by the strong presence of major aerospace and defense contractors, including Boeing, Lockheed Martin, Northrop Grumman, and SpaceX, which are among the largest consumers of aerospace-grade titanium alloys.

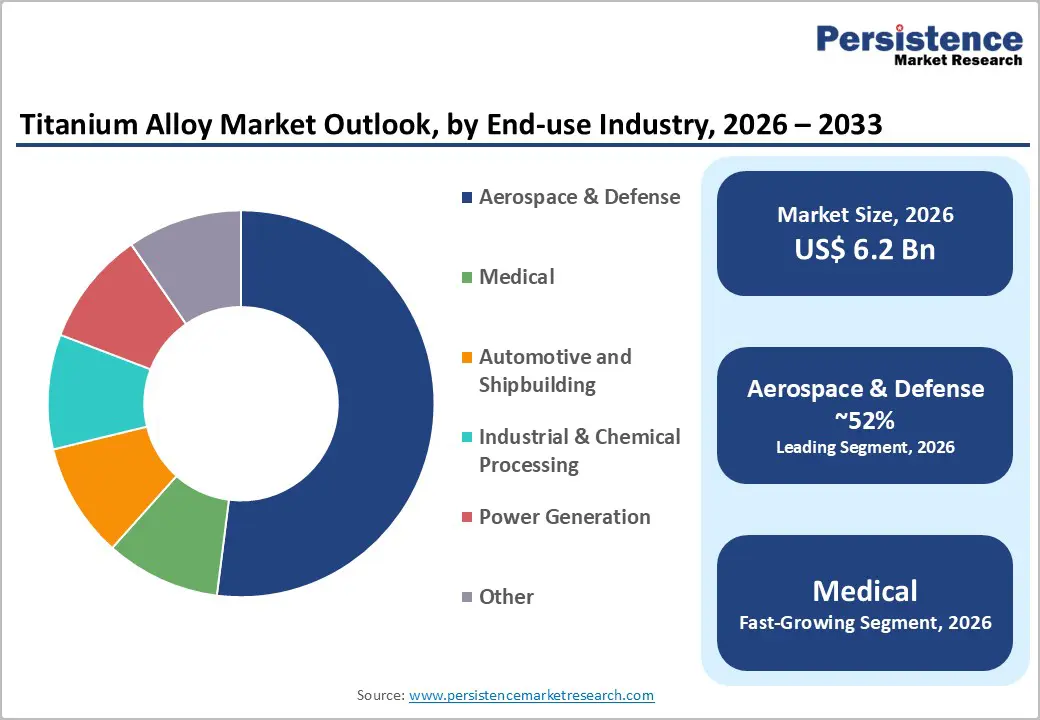

- Dominant Segment: Alpha-Beta Alloys dominate the Microstructure category with approximately 52% market share, led by Ti-6Al-4V, which is the globally preferred alloy grade across aerospace, medical, and industrial applications.

- Fastest Growing Segment: The Medical end-use segment is the fastest growing, projected at a CAGR of approximately 7.35% through 2033, driven by rising orthopedic and dental implant demand and accelerating adoption of additive manufacturing-enabled patient-specific titanium implants.

- Key Market Opportunity: Additive manufacturing integration represents the most transformative opportunity, enabling near-net-shape titanium components with reduced material waste, unlocking new addressable markets in medical devices, hypersonic aerospace, and defense applications globally.

| Key Insights | Details |

|---|---|

| Titanium Alloy Market Size (2026E) | US$ 6.2 Bn |

| Market Value Forecast (2033F) | US$ 8.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.5% |

Market Dynamics

Driver - Surging Aerospace & Defense Production Fueling Titanium Alloy Demand

The primary driver of the Titanium Alloy market is the substantial escalation in global commercial aircraft manufacturing. Boeing’s long-term outlook projects the delivery of more than 41,000 new aircraft by 2041, ensuring a sustained and robust demand cycle for titanium alloys. These alloys account for approximately 9-15% of the structural weight in advanced aircraft platforms, including the Boeing 787 Dreamliner and Airbus A350 XWB. By late 2024, global aircraft backlogs exceeded 17,000 units, with IATA indicating an estimated 14-year waiting period for new deliveries.

Concurrently, rising global defense expenditures, particularly among NATO member states, are accelerating procurement of fighter jets and naval platforms. As fighter aircraft require significantly higher titanium content, defense programs further reinforce long-term, compounded growth across the Titanium Alloy market.

Expanding Medical Implant Applications Supported by Aging Demographics

Titanium alloys, most notably Ti-6Al-4V (Grade 5) and Ti-6Al-4V ELI (Grade 23), remain the preferred materials for orthopedic, spinal, dental, and cardiovascular implants due to their superior biocompatibility, strong osseointegration characteristics, and high corrosion resistance in physiological environments. According to the World Health Organization, the global population aged 60 years and above is expected to exceed 2.1 billion by 2050, a demographic segment with an increasing prevalence of musculoskeletal conditions requiring joint replacements and spinal interventions.

In the United States, the American Academy of Orthopaedic Surgeons reports that hip and knee replacement procedures surpass 1.5 million annually, with steady growth projected over the next decade. Additionally, the adoption of additive manufacturing for customized titanium implants is further strengthening demand across dental, craniofacial, and orthopedic applications.

Restraints - High Production Costs and Energy-Intensive Processing

Titanium extraction and alloy processing remain among the most energy-intensive metallurgical operations globally. The Kroll Process, the dominant commercial method for producing titanium sponge, requires substantial energy inputs, specialized infrastructure, and controlled atmosphere conditions. As a result, titanium alloys cost significantly more than competing materials such as aluminum or advanced high-strength steels. Raw titanium metal prices peaked at approximately US$ 19.28 per kilogram in May 2024, compared to a January 2024 average of US$ 7.68 per kilogram, illustrating significant price volatility. These elevated and unpredictable cost structures limit adoption in cost-sensitive sectors and create margin pressures for manufacturers, posing a persistent restraint on market expansion.

Geopolitical Supply Chain Vulnerabilities and Raw Material Concentration

The titanium alloy supply chain is characterized by a high degree of geographic concentration, creating systemic vulnerability. China currently supplies over 75% of the world's titanium metals, up from less than 40% in 2019, while Russia, through VSMPO-AVISMA, has historically accounted for a majority of aerospace-grade titanium supplied to Western OEMs. Geopolitical tensions and trade disruptions have exposed the fragility of these supply chains, forcing aerospace primes like Boeing and Airbus to seek alternative sources, a process that can take up to 10 years for aerospace qualification. This concentration risk constrains supply responsiveness, creates pricing unpredictability, and dampens near-term capacity expansion plans across the industry.

Opportunities - Additive Manufacturing Unlocking New Design Frontiers and Cost Efficiencies

Additive manufacturing (AM) represents a highly transformative advancement for the Titanium Alloy market, enabling near-net-shape component production with significantly reduced material waste, an essential advantage given titanium’s high raw material cost. Technologies such as Selective Laser Melting (SLM), Electron Beam Melting (EBM), and Directed Energy Deposition (DED) facilitate the fabrication of complex lattice and hollow structures essential for next-generation aerospace platforms, including advanced jet engines and hypersonic systems.

AM substantially lowers lead times and buy-to-fly ratios, improving overall production economics. Its growing adoption in aerospace, defense, and medical device manufacturing, particularly for customized spinal and dental implants, is expanding commercial opportunities for titanium alloy producers. Industry momentum is reinforced by strong growth in the metal AM market, with titanium among the most widely used materials.

Expanding Use of Titanium Alloys in Renewable Energy and Desalination Infrastructure

The global energy transition is creating a structurally significant and enduring demand pathway for titanium alloys beyond their traditional aerospace and medical applications. Rapid expansion of seawater desalination facilities across the Middle East, North Africa, and coastal Asia is driving substantial use of titanium heat-exchanger tubes and condenser components due to the alloy’s exceptional resistance to chloride-induced corrosion. As global desalination capacity exceeded 100 million cubic meters per day in 2024, this requirement continues to intensify.

Simultaneously, offshore wind turbines and tidal energy platforms increasingly incorporate titanium in fasteners, shafts, and critical marine-grade structural elements. With global clean-energy investment projected to surpass USD 2 trillion annually by 2026 and offshore wind capacity expected to expand by more than 300 GW between 2024 and 2030, these infrastructure developments are generating sustained, incremental demand for corrosion-resistant titanium alloys.

Category-wise Analysis

Microstructure Insights

Within the Microstructure category, Alpha-Beta Alloys hold a dominant position, accounting for roughly 52% of the global titanium alloy market revenue. This leadership is attributed to their exceptional versatility, as they provide an optimal combination of strength, ductility, formability, and elevated-temperature resistance, capabilities not achieved by Alpha or Beta alloys alone. The most significant commercial grade, Ti-6Al-4V (Grade 5), represents over half of global titanium alloy consumption and is widely utilized in aerospace airframes, jet engine parts, orthopedic implants, and marine structures.

Major aircraft programs such as the Airbus A320 and Boeing 787 are among the largest users of this alloy class. In contrast, Beta Alloys constitute the fastest-growing segment, projected to expand at approximately 7.8% CAGR, driven by their superior cold formability and high strength-to-weight benefits in advanced airframe and medical implant applications.

Industry Insights

The Aerospace & Defense sector remains the predominant end-use segment, accounting for approximately 52% of the global Titanium Alloy market. This leadership reflects the essential role of titanium in both commercial and military aircraft, where its superior strength-to-weight characteristics enable higher payload capacity and improved fuel efficiency. Modern wide-body platforms, such as the Boeing 787 Dreamliner, incorporate titanium alloys in nearly 15% of their structural weight, while fifth-generation fighter jets rely on even greater proportions due to stringent performance requirements.

Ongoing fleet renewal, supported by increasingly stringent ICAO fuel-efficiency regulations, continues to drive procurement. In contrast, the Medical segment represents the fastest-growing category, propelled by rising demand for orthopedic, dental, and spinal implants, along with rapid adoption of 3D-printed, patient-specific titanium implants across major global markets.

Regional Insights

North America Titanium Alloy Market Trends

North America remains the most technologically advanced and commercially significant region in the Titanium Alloy market, accounting for nearly 35% of global aerospace titanium demand. Its leadership is supported by the strong presence of major aerospace and defense contractors, including Boeing, Lockheed Martin, Northrop Grumman, and SpaceX, which are among the largest consumers of aerospace-grade titanium alloys.

The U.S. Department of Defense’s expanding focus on hypersonic weapons and sixth-generation fighter programs is further increasing titanium procurement requirements, with military platforms representing approximately 55% of titanium usage in the U.S. aerospace sector. On the supply side, policy-driven initiatives to restore domestic titanium sponge production are advancing, led by developments such as ATI Inc.’s commissioning of a 12,500-ton billet forging press in 2024. Additionally, strong demand from leading medical implant manufacturers reinforces North America’s role as an innovation hub for titanium applications.

Europe Titanium Alloy Market Trends

Europe accounts for roughly 27% of the global aerospace titanium market, supported by the strong presence of major industry players such as Airbus, Rolls-Royce, Safran, and MTU Aero Engines within the region’s integrated aerospace supply chain. Germany is projected to grow at a 6.1% CAGR through 2035, driven by advancements in high-purity batch melting and the adoption of laser-based additive manufacturing for titanium components.

Regulatory frameworks under EASA and the EU Green Deal are accelerating the use of lightweight titanium structures in next-generation hydrogen-propulsion aircraft. The United Kingdom remains a key processing hub, with recycled titanium representing 18% of its aerospace titanium volume in 2024. France and Spain contribute through their roles in Airbus production, while regional diversification away from Russian feedstock is increasing demand for titanium semi-finished products from Japan, the Middle East, and European suppliers.

Asia Pacific Titanium Alloy Market Trends

Asia Pacific is the largest consuming region for titanium alloys, accounting for approximately 41% of the global market share. China alone supplies more than 75% of global titanium metal and has expanded titanium component output by 43% between 2021 and 2024 across key industrial provinces. Growing domestic aerospace programs, including COMAC’s C919 and next-generation military platforms such as the J-36 fighter jet, are driving substantial demand for aerospace-grade titanium.

Government-supported producers, led by Western Superconducting Technologies (WST) and Baoji Titanium Industry, continue to strengthen vertical integration from sponge production to forged components. Japan remains a critical supplier to Western OEMs, with Toho Titanium and OSAKA Titanium Technologies increasing sponge capacity to offset reduced Russian supply. India is projected to grow at 6.6% CAGR through 2035, supported by ISRO and DRDO demand, while ASEAN’s expanding MRO ecosystem and rising air-travel requirements further enhance regional consumption.

Competitive Landscape

The global Titanium Alloy market is characterized by moderate consolidation, with the top five manufacturers accounting for nearly 73% of total market share. The competitive landscape is led by vertically integrated producers that manage the entire value chain, from titanium sponge production to finished mill products and engineered components. Their strategic focus includes securing long-term supply contracts with major aerospace OEMs, expanding advanced melting and forging capabilities, and incorporating additive manufacturing to address high-margin medical and defense applications. Competitive differentiation is increasingly driven by proprietary alloy formulations, recycling initiatives, and geopolitical supply-chain diversification, while smaller regional firms concentrate on cost-sensitive automotive, marine, and industrial chemical processing niches.

Key Market Developments

- June 2025: ATI Inc. brought online a state-of-the-art facility in Pageland, South Carolina to produce titanium alloy sheet. Technically challenging to produce, this material is critical to airframe manufacturers, bringing strength and durability to aerostructure components and assemblies.

- March 2024: ATI Inc. commissioned a 12,500-ton billet forging press at its Pennsylvania facility and secured a five-year titanium supply agreement with Airbus valued at over US$ 1 Bn, significantly expanding its European aerospace market presence.

- September 2024: Amnovis, a specialist in 3D-printed titanium implants, announced the milestone delivery of over 50,000 titanium-based implants since 2021, underlining the rapid commercial scaling of additive manufacturing in the titanium medical segment.

Top Companies in Titanium Alloy Market

- VSMPO-AVISMA Corporation (Verkhnaya Salda, Russia) is the world's largest integrated titanium producer, historically supplying over 30% of global aerospace-grade titanium demand. The company maintains deep long-term partnerships with Boeing, Airbus, Rolls-Royce, and multiple defense contractors. Despite geopolitical headwinds from Russia's war in Ukraine and resulting Western sanctions scrutiny, VSMPO-AVISMA has expanded cooperation with Chinese aerospace manufacturers and continues to be a dominant force in global titanium supply. Its vertically integrated operations, from titanium ore through to precision aerospace forgings, underpin its competitive moat.

- ATI Inc. (Pittsburgh, U.S.) is the leading Western producer of aerospace-grade titanium alloys, with approximately 66% of its revenue derived from aerospace and defense applications. The company has made substantial capital investments in forging and melting capacity, most notably a new 12,500-ton press commissioned in 2024. ATI's long-term supply agreements with both Boeing and Airbus, combined with its proprietary alloy development capabilities, position it as the primary beneficiary of the Western aerospace industry's strategic decoupling from Russian titanium supply.

- Howmet Aerospace Inc. (Pittsburgh, U.S.) (formerly part of Arconic) is a world leader in engineered titanium components for aerospace propulsion and structural applications. The company recorded 17% commercial aerospace sales growth in Q3 2024 on the back of surging engine demand from both commercial and defense customers. Howmet's proprietary titanium alloy formulations, designed for extreme-temperature turbine applications, combined with its global manufacturing footprint across the U.S., Europe, and Asia, give it a differentiated competitive position.

Companies Covered in Titanium Alloy Market

- VSMPO-AVISMA Corporation

- ATI Inc.

- TIMET

- Precision Castparts Corp.

- Howmet Aerospace Inc.

- Toho Titanium Co., Ltd.

- OSAKA Titanium Technologies Co., Ltd.

- Kobe Steel, Ltd.

- Western Superconducting Technologies Co., Ltd.

- Baoji Titanium Co., Ltd.

- Hermith GmbH

Frequently Asked Questions

The global Titanium Alloy market is valued at US$ 6.2 Bn in 2026 and is projected to reach US$ 8.8 Bn by 2033, expanding at a CAGR of 5.1% over the forecast period 2026-2033. This growth is driven by robust aerospace demand, expanding medical implant applications, and sustained industrial usage across multiple verticals.

The foremost demand driver is the accelerating global aircraft production cycle, with Boeing forecasting delivery of over 41,000 new aircraft by 2041. This is complemented by rising orthopedic and dental implant demand from aging global populations, particularly in North America, Europe, and the Asia Pacific, alongside growing defense expenditure across NATO and Indo-Pacific member states.

Alpha-Beta Alloys hold the dominant position in the Microstructure category, representing approximately 52% of global market share. Their dominance is driven by the widespread application of Ti-6Al-4V (Grade 5), the world's most commercially utilized titanium alloy, across aerospace airframes, jet engine components, and orthopedic implants.

Asia Pacific leads the global Titanium Alloy market with approximately 41% of total market share, driven by China's dominant position in titanium sponge and alloy production, Japan's critical role in aerospace supply chains for Boeing and Airbus, and India's rapidly growing aerospace and defense industrial base.

The most significant opportunity lies in the integration of additive manufacturing (metal 3D printing) technologies, which enable near-net-shape titanium components with minimal waste and allow patient-specific implant designs for the medical sector. Strategic supply chain diversification, away from Russian and Chinese sources, also presents a major opportunity for producers in Japan, India, the Middle East, and the Western world.

Key players in the global Titanium Alloy market include VSMPO-AVISMA Corporation, ATI Inc., TIMET, Howmet Aerospace Inc., Toho Titanium Co., Ltd., OSAKA Titanium Technologies Co., Ltd., Kobe Steel, Ltd., Western Superconducting Technologies Co., Ltd., Baoji Titanium Co., Ltd., and Hermith GmbH, among others.