- Industrial Goods & Service

- Synchronous Condenser Market

Synchronous Condenser Market Size, Share, and Growth Forecast 2026 - 2033

Synchronous Condenser Market by Cooling Type (Air Cooled, Hydrogen Cooled, Water Cooled), Product Type (New Synchronous Condenser, Refurbished Synchronous Condenser), Reactive Power Rating (Low ≤100 MVAR, Medium 100-250 MVAR, High >250 MVAR), Starting Method (Static Frequency Converter, Pony Motor, Other), End-user (Electrical Utilities, Industrial), and Regional Analysis, 2026 - 2033

Synchronous Condenser Market Size and Trend Analysis

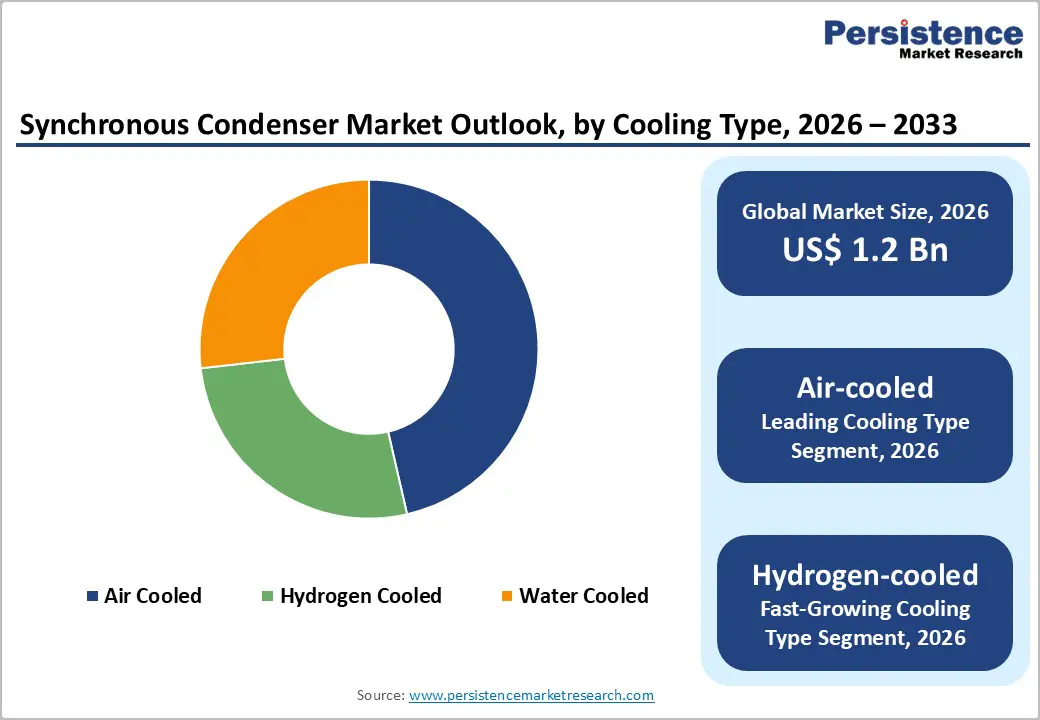

The global synchronous condenser market size is expected to be valued at US$ 1.2 billion in 2026 and is projected to reach US$ 1.5 billion by 2033, growing at a CAGR of 3.6% between 2026 and 2033.

The market's sustained expansion is primarily driven by the accelerating global transition to renewable energy and the resulting demand for grid-stabilization technologies. Global renewable energy capacity surged by a record 15.1% in 2024 to reach 4,448 GW, with wind and solar installations introducing significant voltage variability that synchronous condensers are uniquely equipped to address. Compounding this, global energy investment is projected to reach a record US$ 3.3 trillion in 2025, according to the International Energy Agency (IEA), channeling substantial capital toward grid resilience infrastructure.

The simultaneous decommissioning of inertia-rich conventional thermal power plants across North America and Europe has created an urgent need for reactive power compensation assets, making synchronous condensers an indispensable component of modern power systems.

Key Industry Highlights:

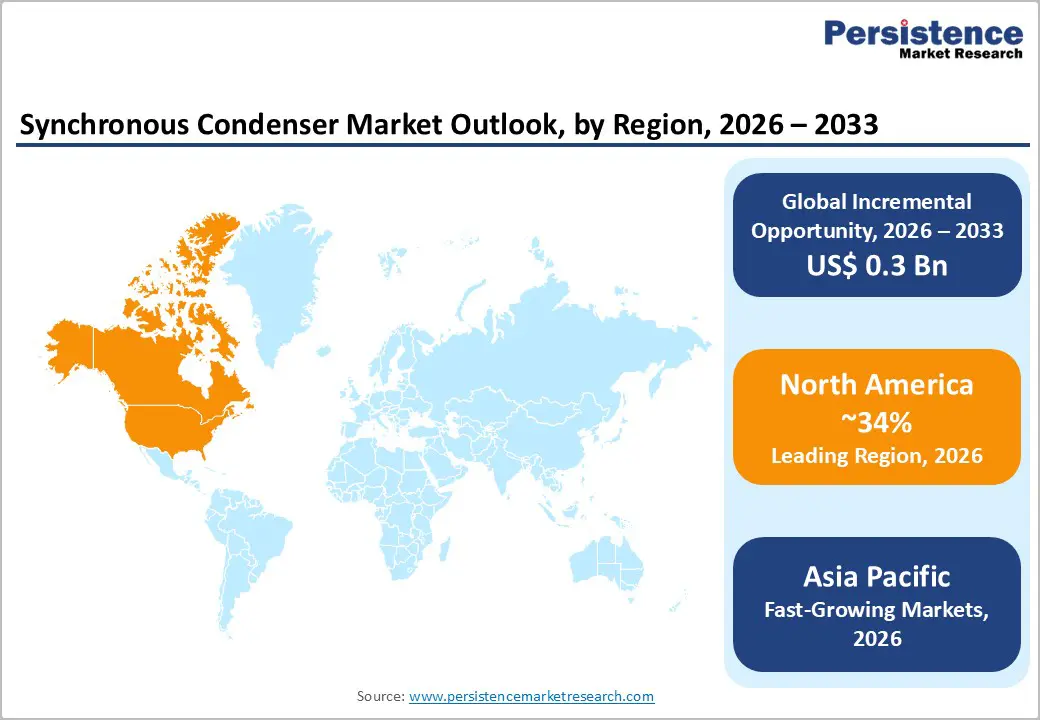

- Leading Region: North America leads the synchronous condenser market with around 34% share, driven by grid modernization, renewable integration, and the retirement of conventional power plants, which are creating strong demand for reactive power and inertia support solutions.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, supported by aggressive renewable energy targets, rising electricity demand, and large-scale grid infrastructure investments across China, India, Japan, and Australia, which are driving increased deployment of synchronous condensers.

- Dominant Segment: Air-cooled synchronous condensers dominate with about 45% share, owing to lower installation complexity, reduced maintenance requirements, and suitability across low- to medium-capacity applications, particularly in regions with water scarcity and strict safety regulations.

- Fastest Growing Segment: Hydrogen-cooled synchronous condensers are the fastest growing segment, driven by demand for high-capacity, high-efficiency systems in large-scale renewable energy zones and bulk transmission networks requiring compact and high power density solutions.

- Key Opportunity: Expansion of HVDC transmission networks presents a major opportunity, as synchronous condensers are essential for reactive power and short circuit support at converter stations, alongside cost-effective refurbishment of decommissioned generators, gaining traction globally.

| Key Insights | Details |

|---|---|

| Synchronous Condenser Market Size (2026E) | US$ 1.2 Billion |

| Market Value Forecast (2033F) | US$ 1.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 3.6% |

| Historical Market Growth (2020 - 2025) | 3.2% |

Market Dynamics

Drivers - Accelerating Renewable Energy Integration, Fueling Reactive Power Demand

The rapid scale-up of intermittent renewable generation is the foremost driver of synchronous condenser demand. Wind and solar power plants produce variable and unpredictable outputs, creating voltage fluctuations and reducing overall grid inertia. In 2024, the United States solar energy sector posted a record-breaking year, with utility-scale solar generation reaching 218.5 TWh, according to the U.S. Energy Information Administration (EIA).

Globally, renewable capacity additions are accelerating, with the International Renewable Energy Agency (IRENA) tracking consistent double-digit annual additions. Synchronous condensers counteract these grid stress conditions by delivering instantaneous reactive power support, system inertia, and short-circuit capacity, capabilities that alternative inverter-based technologies, such as STATCOMs, cannot fully replicate. As grid operators worldwide face stricter reliability standards, the deployment of synchronous condensers has shifted from optional to operationally essential.

Grid Modernization Programs and Retirement of Conventional Generation Assets

Governments and transmission system operators across North America and Europe are implementing ambitious grid modernization programs that structurally favor the deployment of synchronous condensers. The phased retirement of coal and nuclear plants has dramatically reduced native system inertia; in the United Kingdom, for example, the closure of all remaining coal-fired stations by 2025 has prompted National Grid ESO to commission multiple synchronous condenser projects under its Stability Pathfinder initiative.

In the United States, the EIA projected record-high power demand in both 2025 and 2026, driving utilities to invest in infrastructure to deliver reliable reactive power support. Aging transmission infrastructure across multiple regions further necessitates retrofit and upgrade activity, with refurbished synchronous condensers providing a cost-effective pathway to enhanced grid stability and reduced power outages.

Restraints - High Capital Expenditure and Lengthy Installation Lead Times

One of the most significant barriers to market penetration is the substantial upfront capital expenditure associated with synchronous condenser procurement and installation. A single high-capacity unit, particularly in the >250 MVAR reactive power class, can require multi-million-dollar investments including civil works, transformer procurement, and grid integration costs. For utilities in emerging economies or those with constrained capital budgets, this presents a formidable entry barrier. In addition, complex permitting and engineering lead times, often spanning 18 to 36 months from contract award to commissioning, can delay grid stability improvements and disincentivize procurement decisions.

These factors collectively slow market adoption, particularly in regions where alternative, lower-cost technologies such as capacitor banks or static VAR compensators may be evaluated as short-term substitutes.

Competition from Advanced Power Electronic Solutions

The synchronous condenser market faces intensifying competitive pressure from power electronics-based alternatives, most notably Static Synchronous Compensators (STATCOMs) and Static VAR Compensators (SVCs). These inverter-based devices offer faster response times, typically within milliseconds, along with a smaller physical footprint and lower civil engineering requirements, making them attractive for space-constrained urban substations. As semiconductor technologies advance and manufacturing costs fall, the price-performance ratio of STATCOMs continues to improve. While synchronous condensers maintain advantages in inertia provision and short-circuit capacity, grid operators that prioritize voltage control speed over inertia may opt for electronic solutions, limiting incremental demand for rotating machinery-based condensers in certain market segments.

Opportunities - Expansion of HVDC Interconnectors and Long-Distance Renewable Energy Transmission

The global build-out of High-Voltage Direct Current (HVDC) transmission infrastructure represents a compelling growth opportunity for synchronous condenser suppliers. HVDC systems require robust reactive power support and short-circuit capacity at converter stations, a technical niche where synchronous condensers excel.

Projects such as Australia's Central-West Orana Renewable Energy Zone (REZ), for which Siemens Energy was selected in May 2025 to supply synchronous condensers enabling up to 4.5 GW of renewable capacity, exemplify this trend. In Chile, GE Vernova secured a contract in July 2024 to deliver four synchronous condensers for the Ana María and Monte Mina projects, supporting the country's decarbonization strategy. As HVDC interconnectors multiply across Europe, Asia Pacific, and the Americas, demand for grid-side synchronous condensers at AC/DC interface points is expected to generate significant incremental revenue for market participants through 2033.

Refurbishment and Conversion of Decommissioned Generator Assets

The conversion of decommissioned synchronous generators, primarily retired steam turbines and gas turbine generators, into synchronous condensers represents a highly cost-efficient opportunity with a large addressable base. This retrofit approach allows utilities to repurpose existing assets, retaining the rotor, stator, and excitation systems while removing the prime mover. The cost savings versus procuring a new unit can range from 30% to 50%, making refurbishment particularly attractive for budget-constrained grid operators.

In February 2025, Ansaldo Energia secured a US$ 300 million order to design, supply, and commission five 250 MVAR synchronous condensers for grid stabilization in Italy, raising its operational units to 13, reflecting growing utility willingness to invest in large-scale reactive power assets. Market participants offering integrated engineering, procurement, and lifecycle service models for refurbishment projects are well positioned to capture this expanding segment.

Category-wise Analysis

Cooling Type Insights

Among cooling technologies, the air-cooled segment leads the synchronous condenser market, accounting for approximately 45% of total market share in 2025. Air-cooled systems are preferred for their significantly lower installation complexity, minimal ancillary equipment requirements, and reduced maintenance burden compared to hydrogen- or water-cooled alternatives. They are particularly well-suited to geographic regions facing water scarcity or where stringent safety regulations complicate the handling of hydrogen gas. The segment's dominance is further reinforced by its applicability across a wide reactive power range, including low- and medium-MVAR installations that are common in distribution-level and industrial grid reinforcement projects. The hydrogen-cooled segment, however, is the fastest-growing category over the forecast period 2026-2033, driven by the increasing need for high-density, large-capacity synchronous condensers in bulk power transmission and major renewable energy zones where footprint constraints demand superior power-to-volume ratios.

Product Type Insights

The new synchronous condenser segment holds the leading share in the product type category, contributing approximately 55% of market revenue in 2025. New units are preferred for greenfield grid infrastructure projects, offshore wind interconnection, and high-voltage transmission reinforcement programs where performance guarantees, advanced digital monitoring systems, and extended warranty coverage are prioritized. They incorporate the latest design innovations, including improved excitation control, reduced losses, and integration with supervisory control and data acquisition (SCADA) platforms.

Regulatory mandates in Europe and North America requiring provable system inertia and short-circuit levels further support investment in new, certified equipment. The Refurbished Synchronous Condenser segment is the fastest-growing product type, with cost competitiveness and the large available base of retired generator assets across aging power systems in North America and Asia Pacific driving accelerating retrofit activity.

Reactive Power Rating Insights

The High (>250 MVAR) reactive power rating segment leads the market with an estimated share of approximately 40% in 2025. This dominance reflects the increasing deployment of large-scale synchronous condensers in bulk transmission networks, HVDC terminal substations, and major renewable energy zones that require substantial reactive power reserves to maintain voltage stability across wide geographic areas. National Grid in the UK and Terna in Italy have consistently procured high-capacity units, setting a precedent followed by utilities in Australia, Canada, and Chile. The Medium (100-250 MVAR) segment is the fastest growing in this category over 2026-2033, driven by expanding deployment in medium-sized renewable energy clusters, industrial parks, and regional transmission substations across Asia Pacific and Latin America, where power infrastructure scale is growing but has not yet reached bulk transmission requirements.

Starting Method Insights

The Static Frequency Converter (SFC) starting method holds the dominant position in the starting method category, with an estimated market share of approximately 58% in 2025. SFCs offer precise, electronically controlled acceleration of the synchronous condenser rotor to synchronous speed without mechanical stresses associated with pony motor starting. This precision reduces wear on shaft and bearing systems, extends equipment life, and provides smoother grid connection sequences, all of which are critical for high-value, large-MVAR installations. The operational simplicity of SFC-based starting also reduces maintenance requirements and operator skill demands. Transmission system operators and utilities globally have standardized on SFC starting for new installations, particularly for units above 100 MVAR. This segment is supported by the broader deployment of power electronic control systems and smart grid integration platforms that are increasingly co-deployed with synchronous condenser installations.

End-user Insights

The Electrical Utilities segment dominates the end-user category, representing approximately 77% of total market revenue in 2025. Electrical utilities, encompassing transmission system operators, independent transmission companies, and integrated power utilities, are the primary deployers of synchronous condensers globally, driven by regulatory obligations to maintain prescribed voltage profiles, short-circuit levels, and system inertia across transmission networks. The progressive retirement of inertia-providing conventional generators has made reactive power compensation assets a regulatory compliance necessity rather than a discretionary investment for most utilities. The Industrial end-user segment, while smaller in absolute terms, is the fastest-growing category over 2026-2033, expanding at an estimated CAGR of 4.8%. Industrial applications include steel mills, mining operations, chemical plants, and large data center campuses, where power quality, voltage stability, and power factor correction directly impact operational efficiency and equipment longevity.

Regional Insights

North America Synchronous Condenser Market Trends and Insights

North America holds the leading regional share in the synchronous condenser market, contributing approximately 34% of global revenue in 2025. The region's leadership is anchored by large-scale grid modernization programs driven by the retirement of coal, nuclear, and aging gas-fired generation assets across the United States and Canada. The U.S. EIA has confirmed record-high power demand projections for 2025 and 2026, compelling transmission operators to invest in reactive power and inertia solutions to maintain grid reliability. In June 2024, GE Vernova Inc. announced the construction of two 115 kV synchronous condenser facilities to enhance grid stability in New York, under a contract with National Grid's upstate New York business.

Federal policy frameworks, including provisions in the Infrastructure Investment and Jobs Act and renewable portfolio standards adopted by 29 states, are accelerating renewable integration and, by extension, the deployment of complementary grid-stability assets. Canada is similarly active, with Voith announcing a contract to supply a synchronous condenser to a Canadian transmission operator in Q1 2025. Growing adoption of microgrids and high-penetration renewable energy zones, along with HVDC transmission investments, positions North America as a sustained demand center through 2033.

Europe Synchronous Condenser Market Trends and Insights

Europe represents the most mature and policy-driven regional market for synchronous condensers, underpinned by the European Union's mandate to achieve 42.5% renewable energy share in gross final consumption by 2030 under the revised Renewable Energy Directive (RED III). Countries including Germany, the United Kingdom, France, Spain, and Italy are at the forefront of synchronous condenser deployment. In the UK, National Grid ESO's Stability Pathfinder program has commissioned multiple projects including the Rothienorman condenser in North East Scotland, which went operational in January 2025 as the first Pathfinder II project to achieve commercial operation. Ansaldo Energia in February 2025 secured a US$ 300 million contract to deliver five 250 MVAR units for Terna's Italian transmission network.

Germany, as Europe's largest power market and leader in wind and solar energy adoption, is actively deploying synchronous condensers to manage grid fluctuations caused by renewable energy, as its generation mix now exceeds 60% renewables by capacity. Regulatory harmonization through ENTSO-E grid codes mandates minimum short-circuit levels and reactive power capability across member state transmission systems, providing a durable structural tailwind for equipment suppliers across the region.

Asia Pacific Synchronous Condenser Market Trends and Insights

Asia Pacific is the fastest-growing regional market for synchronous condensers over the 2026-2033 forecast period. China, Japan, India, and Australia are the primary growth engines, each pursuing ambitious renewable energy targets that require significant grid-stabilization investments. China's National Development and Reform Commission (NDRC) has set a target of 1,200 GW of wind and solar capacity by 2030, creating an enormous structural demand for reactive power compensation assets in provincial transmission networks. In India, BHEL received a synchronous condenser order from Power Grid Corporation of India in Q2 2025, reflecting the national grid operator's increasing focus on reactive power adequacy as solar and wind penetration rise.

In Australia, Siemens Energy was selected in May 2025 to supply synchronous condensers for the Central-West Orana REZ in New South Wales, supporting up to 4.5 GW of renewable capacity integration. Japan's grid modernization efforts, including Fuji Electric's delivery of synchronous condensers for smart grid pilot projects with major Japanese utilities in Q3 2025, further underscore regional momentum. The combination of rising electricity demand, government-backed infrastructure programs, and manufacturing cost advantages positions Asia Pacific as the most dynamic growth market globally through 2033.

Competitive Landscape

The global synchronous condenser market exhibits a moderately concentrated structure, with a limited number of established players accounting for a significant share of total revenue. Market positioning is influenced by strong technical expertise, proven project execution capabilities, and the ability to deliver integrated solutions across diverse grid environments. High capital intensity, long project cycles, and stringent performance requirements create notable entry barriers, reinforcing the dominance of experienced participants.

Competition is centered on technological differentiation, lifecycle service offerings, and the ability to execute large-scale, multi-unit grid stabilization projects. Key strategies include forming strategic partnerships and joint ventures to enhance project capabilities, expanding into high-growth regions such as Asia Pacific, and investing in digital platforms for predictive maintenance and remote monitoring. Additionally, companies are focusing on modular system designs, hybrid solutions combining mechanical and power electronic technologies, and integration with energy storage systems to improve performance, flexibility, and overall grid reliability.

Key Developments

- February 2025: Ansaldo Energia secured a US$ 300 million order to design, supply, commission, and maintain five 250 MVAR synchronous condensers for Terna's Italian transmission grid over five years, supporting the nation's renewable energy transition.

- May 2025: Siemens Energy was awarded a contract by the ACEREZ consortium to supply and install synchronous condensers for Australia's Central-West Orana REZ in New South Wales, enabling up to 4.5 GW of renewable energy capacity integration.

- May 2025: ANDRITZ and GE Vernova formed a joint venture to install two synchronous condensers at the Bakersfield substation in West Texas, reinforcing grid stability amid growing renewable energy demands across the ERCOT grid.

Companies Covered in Synchronous Condenser Market

- ABB

- Siemens Energy

- IDEAL ELECTRIC POWER CO.

- Ansaldo Energia S.p.A.

- GE Vernova Inc.

- Andritz AG

- Voith

- Fuji Electric

- WEG

- BRUSH

- Hitachi Energy Ltd.

- Mitsubishi Electric Power Products, Inc.

- Doosan Skoda Power

- Bharat Heavy Electricals Limited (BHEL)

- Eaton Corporation

Frequently Asked Questions

The global synchronous condenser market is valued at US$ 1.2 billion in 2026 and is projected to reach US$ 1.5 billion by 2033 at a CAGR of 3.6%.

Key drivers include rising renewable energy integration, retirement of conventional power plants, grid stability requirements, and expansion of HVDC networks.

North America leads with around 34% share, driven by grid modernization and renewable energy policies, while Asia Pacific is the fastest growing region.

Major opportunities include expansion of HVDC interconnectors and conversion of retired generators into synchronous condensers for cost savings.

Key players include ABB, Siemens Energy, GE Vernova, Ansaldo Energia, Andritz, Voith, Fuji Electric, WEG, BRUSH, Hitachi Energy, and Mitsubishi Electric.