- Industrial Goods & Service

- Steel Wire Rod Market

Steel Wire Rod Market Size, Share, and Growth Forecast 2026 - 2033

Steel Wire Rod Market by Product Type (Low-Carbon Steel Wire Rod, High-Carbon Steel Wire Rod, Alloy Steel Wire Rod, Stainless Steel Wire Rod), Diameter Size (≤ 5.5 mm, 5.5 mm - 10 mm, 10 mm - 16 mm, ≥ 16 mm), End-user (Construction & Infrastructure, Automotive & Transportation, Manufacturing & Heavy Machinery, Energy & Utilities, Oil & Gas, Others), and Regional Analysis, 2026 - 2033

Steel Wire Rod Market Size and Trend Analysis

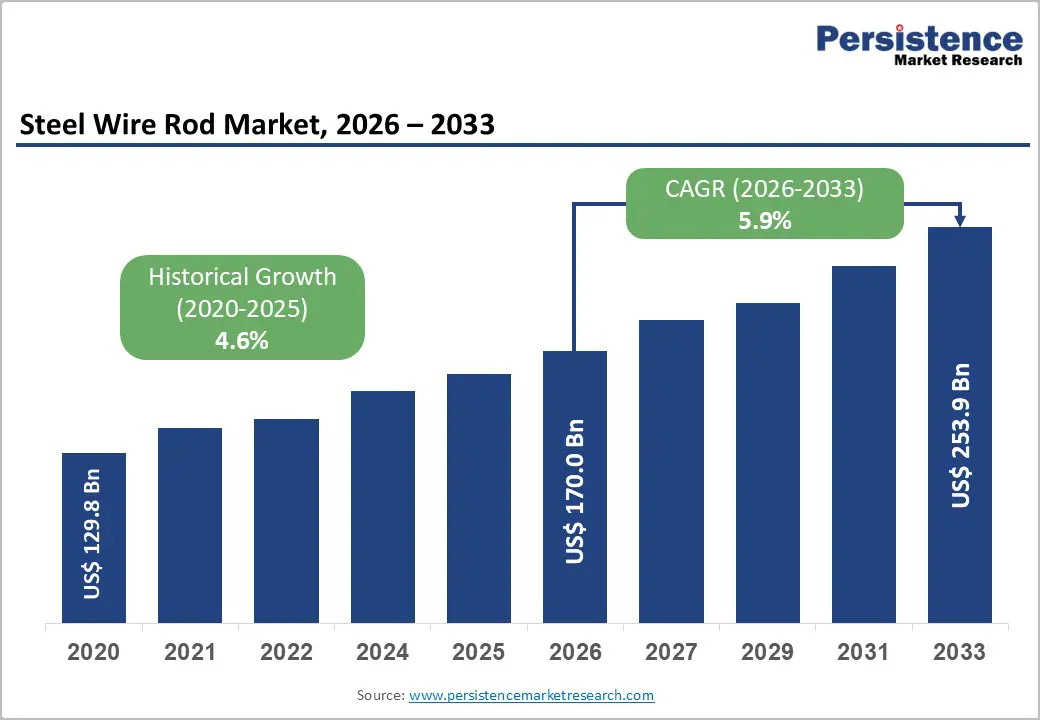

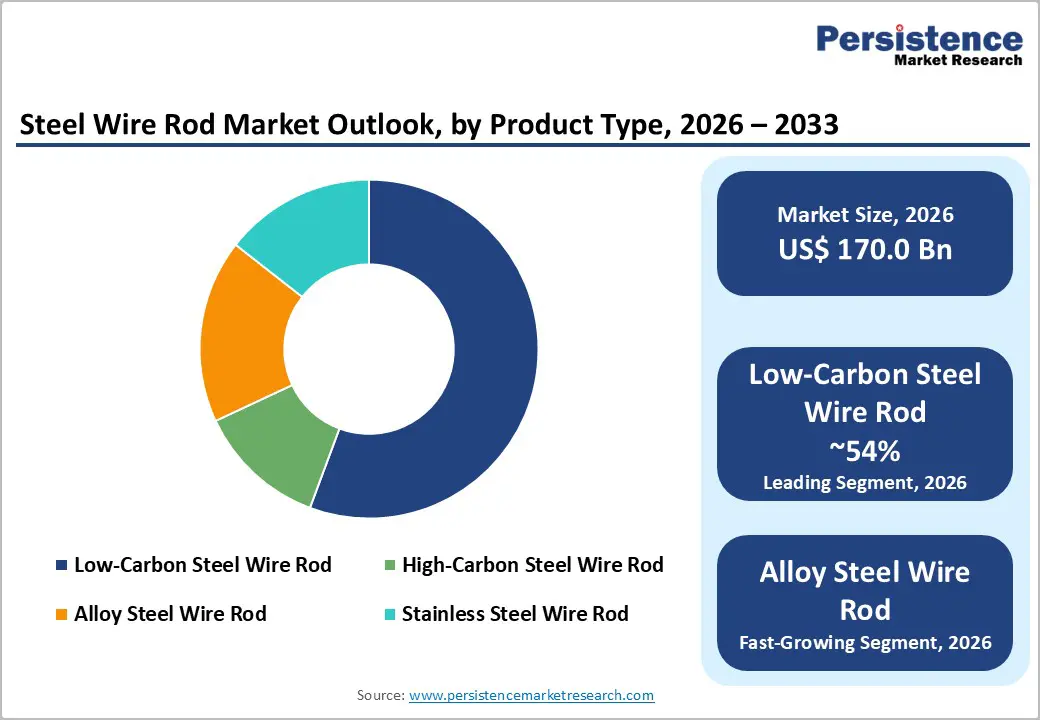

The global steel wire rod market size is likely to be valued at US$ 170.0 billion in 2026 and is expected to reach US$ 253.9 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033.

Robust global construction and infrastructure investment, surging automotive production volumes, and the accelerating deployment of energy transmission and renewable power infrastructure are the primary drivers underpinning the steel wire rod market expansion.

Key Industry Highlights:

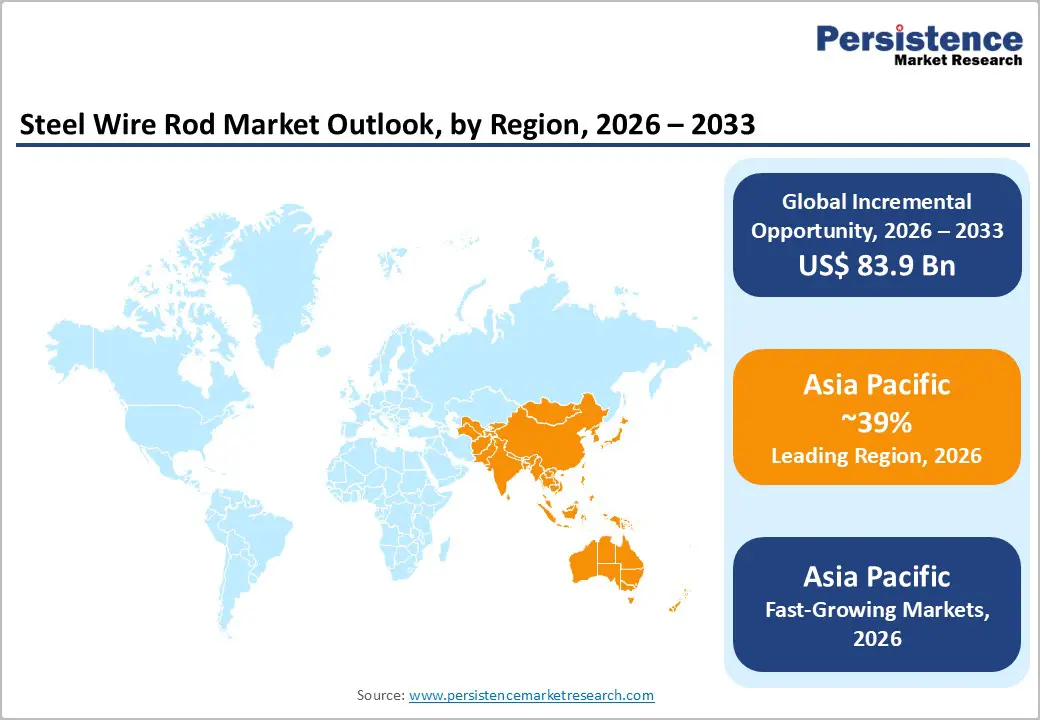

- Leading Region: Asia Pacific dominates the global steel wire rod market, accounting for 39% share, led by China's output exceeding 250 million tonnes annually and India's rapidly expanding steel production capacity targeting 300 million tonnes by 2030, making the region the undisputed global production and consumption hub.

- Fastest Growing Region: Asia Pacific, specifically India, with a rising CAGR of 7.1%, is the fastest growing regional market, driven by the government's 300 million tonne steel capacity target, the National Infrastructure Pipeline, and surging domestic automotive production, creating robust incremental wire rod demand through the forecast period.

- Dominant Segment: Low-Carbon Steel Wire Rod leads the product type segment with approximately 54% market share, underpinned by its indispensable role as feedstock for construction wire mesh, PC strand, and general-purpose drawn wire across the world's largest building and infrastructure markets.

- Fastest Growing Segment: Alloy Steel Wire Rod is the fastest growing product sub-segment, driven by surging automotive production recovery, BEV platform component demand, and renewable energy infrastructure applications requiring high-tensile and corrosion-resistant specialty wire rod grades.

- Key Opportunity: Green steel and low-carbon wire rod represent the highest-value strategic opportunity, as automotive and construction buyers commit to net-zero supply chains under SteelZero and scope-3 targets, enabling premium pricing for hydrogen-DRI and EAF-based low-carbon wire rod producers through 2033.

| Key Insights | Details |

|---|---|

| Steel Wire Rod Market Size (2026E) | US$ 170.0 Billion |

| Market Value Forecast (2033F) | US$ 253.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 4.6% CAGR |

DRO Analysis

Drivers - Global Construction Boom and Infrastructure Investment Driving Structural Wire Rod Demand

Construction and infrastructure development remain the largest drivers of global steel wire rod demand, particularly for low-carbon grades used in applications such as concrete reinforcement mesh, prestressed concrete (PC) wire and strand, and binding wire for rebar. Demand is rising rapidly as global construction activity accelerates, especially across Asia, the Middle East, and Africa.

According to the Global Infrastructure Hub, an initiative of the G20, the global infrastructure investment gap is expected to reach approximately US$ 15 trillion by 2040, highlighting the long-term demand potential for steel-based inputs. In the United States, the Infrastructure Investment and Jobs Act (IIJA) is directing over US$ 1.2 trillion toward transport, utilities, and digital infrastructure projects. These developments are significantly increasing the consumption of structural steel and downstream wire rod products, reinforcing the critical role of construction in sustaining global market growth.

Automotive Industry Recovery and Electrification Sustaining High-Carbon and Alloy Wire Rod Demand

The automotive sector continues to be a major demand driver for high-carbon and alloy steel wire rod, which is widely used in applications such as tire cord, springs, suspension components, fasteners, bearing wire, and precision-engineered parts. Global vehicle production has shown a strong recovery, with the International Organization of Motor Vehicle Manufacturers (OICA) reporting approximately 93.5 million units produced in 2023. The shift toward battery electric vehicles (BEVs) is further strengthening demand rather than reducing it, as EV platforms require advanced high-performance alloy wire rod for motor shafts, durable fasteners, and modern suspension systems. Additionally, the expansion of EV charging infrastructure and grid modernization initiatives is creating new demand for wire rod in applications like energy cable armouring and utility pole support systems, thereby supporting sustained market growth.

Restraints - Global Steel Overcapacity and Structural Oversupply Depressing Wire Rod Prices

Ongoing global steel overcapacity, largely concentrated in China, which produces over 50% of the world’s crude steel, continues to place downward pressure on wire rod prices. According to the World Steel Association, global steel capacity utilization has remained below 80% for several years, resulting in a persistent supply-demand imbalance. This structural oversupply reduces pricing power for producers, compresses profit margins, and limits investments in advanced production technologies and capacity upgrades.

It contributes to increasing trade tensions, leading to the imposition of anti-dumping duties by regions such as the European Union and the United States on imported wire rod products. These trade barriers further complicate global market dynamics and create uncertainty for producers operating in export-dependent markets, ultimately restraining overall industry profitability and long-term growth potential.

Rising Energy Costs and Decarbonization Compliance Costs Pressuring Steelmakers

Steel wire rod production is highly energy-intensive, particularly through the blast furnace-basic oxygen furnace (BF-BOF) route, which consumes around 18-20 gigajoules of energy per tonne of crude steel. Rising energy costs, especially during the 2022-2023 energy crisis in Europe, have significantly increased production expenses for steelmakers. At the same time, stricter environmental regulations are adding further financial pressure.

Policies such as the European Union Emissions Trading System (ETS) and the Carbon Border Adjustment Mechanism (CBAM) are increasing compliance costs for carbon-intensive steel production. These regulatory measures are aimed at reducing emissions, but also challenge the competitiveness of European producers compared to manufacturers in regions with less stringent carbon pricing. As a result, steelmakers are facing growing pressure to balance cost efficiency with sustainability goals.

Opportunities - Green Steel and Low-Carbon Wire Rod for Sustainability-Committed End-User Industries

The global shift toward decarbonization is creating significant opportunities for low-carbon or “green” steel wire rod produced using hydrogen-based direct reduced iron (H-DRI) or electric arc furnace (EAF) technologies powered by renewable energy. Leading automotive manufacturers such as Volkswagen Group, BMW AG, and Volvo Cars have set ambitious Scope 3 emission reduction targets, requiring their supply chains to transition to low-carbon materials.

Initiatives like SteelZero, a global coalition of steel buyers, have committed organizations with over US$ 30 billion in annual steel procurement to sourcing 100% net-zero steel by 2050. This growing demand for sustainable materials allows wire rod producers investing in green technologies to command premium pricing and secure long-term supply agreements. As sustainability becomes a core purchasing criterion, companies adopting low-carbon production methods are expected to gain a strong competitive advantage.

Renewable Energy Infrastructure Build-Out Creating New Demand for Specialty Wire Rod Grades

The rapid expansion of renewable energy infrastructure is generating strong demand for specialty steel wire rod across various applications. These include wind turbine tower anchor bolts, solar panel mounting fasteners, high-voltage direct current (HVDC) transmission cable armouring, and overhead power line conductor core wires. The International Energy Agency (IEA) projects that global renewable energy capacity will increase by more than 5,500 GW between 2023 and 2030 under its net-zero scenario.

This large-scale expansion of wind, solar, and grid infrastructure is driving demand for high-strength, corrosion-resistant wire rod grades. Steel manufacturers specializing in advanced alloy and stainless steel wire rod are well-positioned to benefit from this trend. As governments and industries continue to prioritize clean energy investments, this segment offers long-term, policy-driven growth opportunities for wire rod producers.

Category-wise Analysis

By Product Type Insights

Low-carbon steel wire rod leads the product type segment, accounting for approximately 54% of total market revenue. Typically containing less than 0.25% carbon, this grade is widely used across the construction and infrastructure sector as a primary input for products such as reinforcing wire mesh, binding wire, nail wire, and general-purpose drawn wire. Its dominance is largely driven by the massive scale of global construction activities, particularly in high-growth regions such as China, India, and Southeast Asia. These regions contribute significantly to global building construction output. The World Steel Association consistently identifies construction as the largest consumer of steel worldwide, accounting for around 52% of total steel usage. Within this ecosystem, wire rod plays a critical role as a foundational material, supporting a wide range of structural and non-structural applications across construction value chains.

By Diameter Size Insights

The 5.5 mm to 10 mm diameter range represents the largest segment in the steel wire rod market, contributing approximately 48% of total revenue based on diameter classification. This range includes the most commonly used and versatile wire rod sizes, starting from the standard 5.5 mm coils produced by most wire rod mills to larger diameters like 8 mm and 10 mm.

These sizes are widely used in applications such as reinforcing wire, general wire drawing, and cold heading processes for fastener production. The 5.5 mm wire rod is considered a benchmark product globally and serves as the primary feedstock for a wide range of downstream wire products across industries. Its high level of standardization and widespread availability ensures efficient production, easy trade, and strong market liquidity, making it essential for maintaining consistent mill operations across different regions.

By End-user Insights

Construction and infrastructure remain the largest end-use segment in the steel wire rod market, accounting for approximately 49% of total consumption. Steel wire rod is widely used in various downstream applications, including prestressed concrete (PC) wire and strand for bridges and slabs, welded wire reinforcement (WWR) mesh for structural applications, stay cables for suspension bridges, and mechanical splicing wire for rebar connections.

According to the World Bank, global infrastructure investment is expected to exceed US$ 94 trillion between 2016 and 2040, emphasizing the long-term importance of this sector. Rapid urbanization, particularly in Asia and Africa, continues to drive significant demand for construction materials. As cities expand and infrastructure projects increase, the reliance on wire rod products remains strong, ensuring that construction continues to dominate market demand throughout the forecast period.

Regional Insights

North America Steel Wire Rod Market Trends

North America is a key regional market for steel wire rod, led by the United States as both a major producer and consumer. Strong demand from the construction sector, supported by long-term infrastructure programs such as the Infrastructure Investment and Jobs Act (IIJA), continues to drive market growth. The region also benefits from a well-established automotive manufacturing base, particularly in the Midwest. Major domestic producers, including Nucor Corporation, Gerdau North America, and ArcelorMittal USA, gain competitive advantages from Section 232 tariffs, which impose a 25% duty on steel imports. These measures protect local manufacturers from low-cost foreign competition. Additionally, investments in electric arc furnace (EAF) technology have improved both cost efficiency and environmental performance. In Canada, demand is supported by automotive activity in Ontario and construction growth in urban areas, while USMCA regulations strengthen regional steel consumption.

Europe Steel Wire Rod Market Trends

Europe represents a mature yet technologically advanced steel wire rod market, with Germany serving as the region’s leading production and consumption hub due to its strong automotive and industrial base. Key manufacturers such as ArcelorMittal, CELSA Group, and voestalpine AG supply a diverse range of industries, including automotive, construction, and engineering.

The introduction of the Carbon Border Adjustment Mechanism (CBAM) is reshaping trade dynamics by increasing costs for high-carbon imports while encouraging domestic investment in green steel production. Countries like France and Spain maintain active wire rod processing industries, while the United Kingdom relies on imports to support its manufacturing sector. However, European steelmakers face ongoing challenges from high energy costs and carbon pricing under the EU ETS. This has accelerated investments in hydrogen-based steelmaking and EAF technologies, positioning the region for a transition toward sustainable production.

Asia Pacific Steel Wire Rod Market Trends

Asia Pacific dominates the global steel wire rod market, accounting for the majority of both production and consumption. China leads the region and the world, producing over 250 million tonnes of wire rod annually, according to the China Iron & Steel Association (CISA). This output exceeds the combined production of all other regions, driven by large-scale urbanization and infrastructure development. Despite fluctuations in the real estate sector, domestic demand remains strong. India is emerging as the fastest-growing market, with the government targeting 300 million tonnes of steel production capacity by 2030. Major players such as Tata Steel, JSW Steel, and SAIL are expanding capacity to meet rising demand. Meanwhile, Japan and South Korea focus on high-quality specialty wire rod production, with companies like Nippon Steel Corporation and POSCO supplying advanced materials for automotive and energy applications.

Competitive Landscape

The global steel wire rod market is moderately fragmented at the international level, with leadership concentrated among large integrated steel producers such as ArcelorMittal, Nippon Steel Corporation, POSCO, and Jiangsu Shagang Group. These companies operate large-scale production facilities across multiple regions, enabling them to serve diverse markets efficiently. However, regional markets tend to be more consolidated, with a few dominant players controlling significant market share.

Key competitive factors include advanced metallurgical capabilities, proximity to key customers in automotive and construction sectors, and access to cost-efficient raw materials such as scrap for electric arc furnace production. Increasingly, companies are focusing on vertical integration into downstream processing, investments in green steel technologies, and digital manufacturing systems to improve quality control and traceability. These strategies are shaping the future competitive landscape of the steel wire rod industry.

Key Developments:

- In January 2025, ArcelorMittal initiated production at its Dunkirk DRI-EAF facility in France, marking a major step in low-carbon steelmaking. The plant produces slabs and long products, including wire rod feedstock, achieving nearly 50% lower carbon emissions compared to traditional BF-BOF processes.

- In September 2024, Nippon Steel completed upgrades at its Kimitsu Works wire rod mill in Japan, increasing capacity for high-tensile automotive-grade wire rod. The expansion supports tire cord and spring applications, strengthening its position in premium export markets across Asia and North America.

- In March 2023, Tata Steel commissioned a new wire rod block mill at its Jamshedpur facility, enabling high-speed production of 5.5 mm to 16 mm wire rod coils. The expansion supports rising demand from India’s construction and industrial wire drawing sectors.

Companies Covered in Steel Wire Rod Market

- ArcelorMittal

- Nippon Steel Corporation

- POSCO

- Tata Steel Limited

- Gerdau S.A.

- EVRAZ plc

- Jiangsu Shagang Group

- Anyang Iron & Steel Group

- Emirates Steel Industries

- Mechel PAO

- NSSMC

- Central Wire Industries

- Fagersta Stainless

- Danieli

- SMS Group

- Nucor Corporation

- JSW Steel Limited

- Baowu Steel Group

Frequently Asked Questions

The global Steel Wire Rod Market is valued at US$ 170.0 Billion in 2026 and is projected to reach US$ 253.9 Billion by 2033, growing at a CAGR of 5.9% over the forecast period from 2026 to 2033.

The primary growth drivers are robust global construction and infrastructure investment, anchored by the U.S. Infrastructure Investment and Jobs Act (IIJA) and the G20 Global Infrastructure Hub's estimated US$ 15 trillion investment gap through 2040, and the recovery and electrification of global automotive production, which drives demand for high-carbon and alloy wire rod for tire cord, springs, and fasteners.

Low-Carbon Steel Wire Rod leads the product type segment with approximately 54% market share, driven by its critical role as the primary feedstock for construction wire mesh, PC wire and strand, binding wire, and general drawn wire products consumed across the world's largest building and infrastructure markets.

Asia Pacific is the dominant region, anchored by China's wire rod output exceeding 250 million tonnes annually and India's rapidly expanding steel production capacity targeting 300 million tonnes by 2030, collectively making Asia Pacific the overwhelming global center of wire rod production and consumption.

The most significant strategic opportunity is green steel and low-carbon wire rod production. As automotive OEMs and construction buyers commit to net-zero scope-3 supply chains, supported by SteelZero and EU CBAM regulatory frameworks, producers investing in hydrogen-DRI and EAF-based steelmaking can command sustainable price premiums and long-term supply agreements.

Leading companies include ArcelorMittal, Nippon Steel Corporation, POSCO, Tata Steel Limited, Gerdau S.A., Jiangsu Shagang Group, Nucor Corporation, JSW Steel Limited, Baowu Steel Group, EVRAZ plc, and Emirates Steel Industries, among others.