- Advanced Materials

- Steel Wire Market

Steel Wire Market Size, Share, and Growth Forecast, 2026 - 2033

Steel Wire Market By Product Type (Carbon Steel, Stainless Steel, Others), Process Type (Hot Rolled, Cold Rolled, Others), End-user, and Regional Analysis for 2026 - 2033

Steel Wire Market Size and Trends Analysis

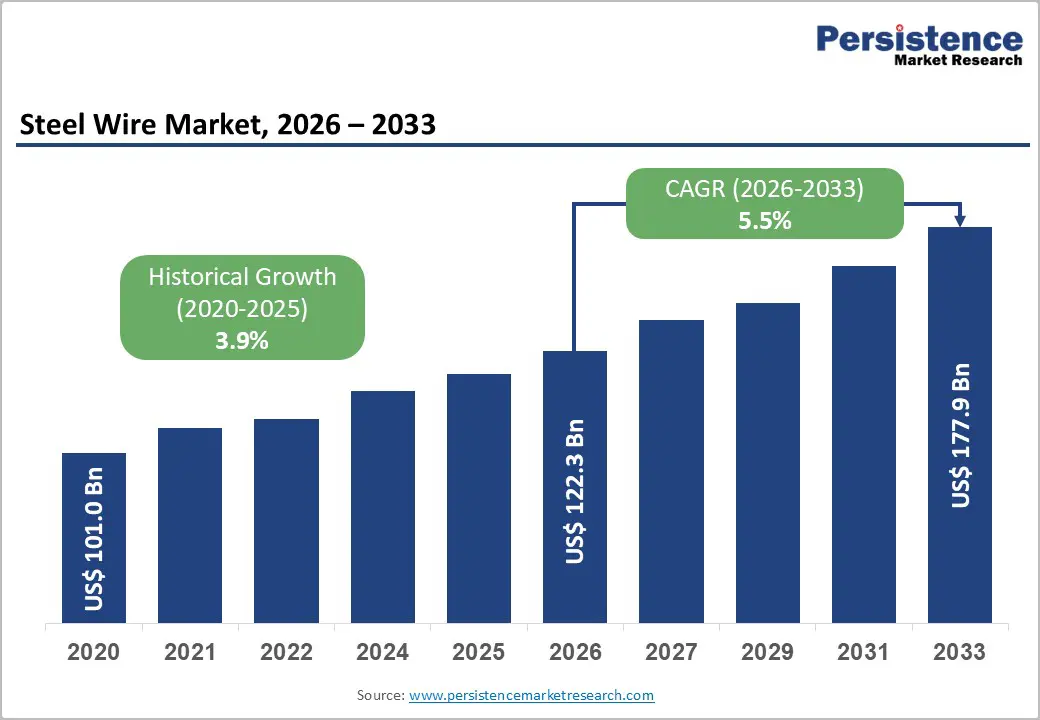

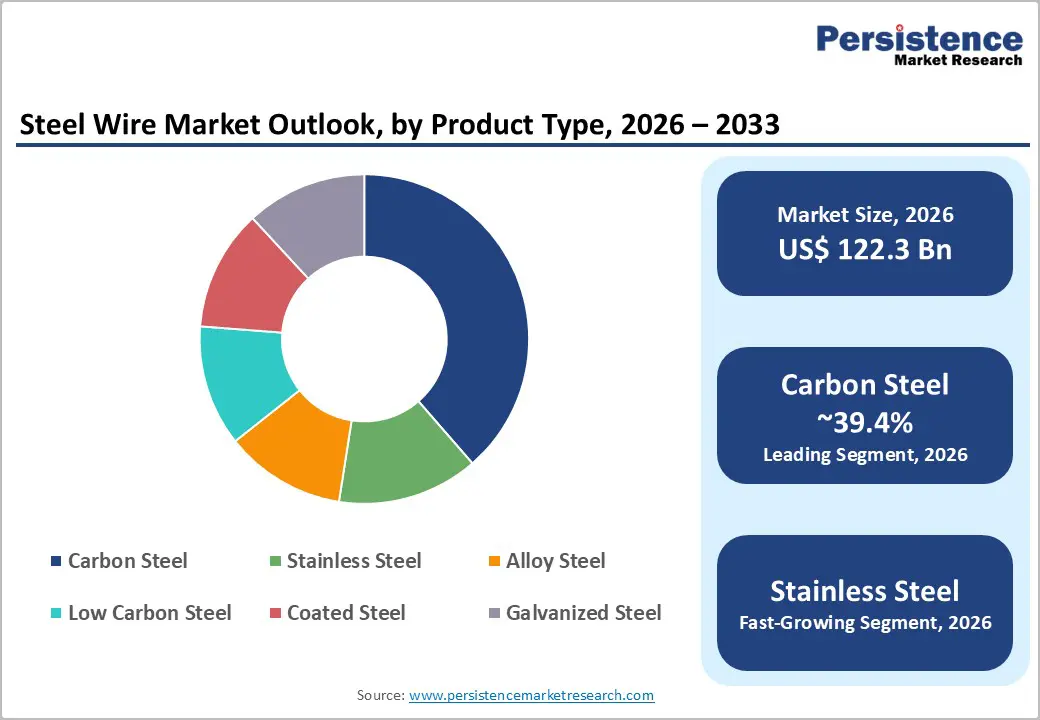

The global steel wire market size is likely to be valued at US$ 122.3 billion in 2026 and is expected to reach US$177.9 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033, driven by large-scale infrastructure development, expanding automotive manufacturing, and rising demand from energy and industrial sectors.

Steel wire remains a critical intermediate material used in reinforcement, cables, springs, and precision mechanical components. Asia Pacific dominates global consumption due to strong construction and manufacturing output, while North America and Europe maintain strong demand for specialty and high-performance wire products. Raw-material price volatility and trade regulations present short-term challenges, though technological upgrades and premium alloy applications continue to improve long-term profitability prospects for industry participants.

Key Industry Highlights:

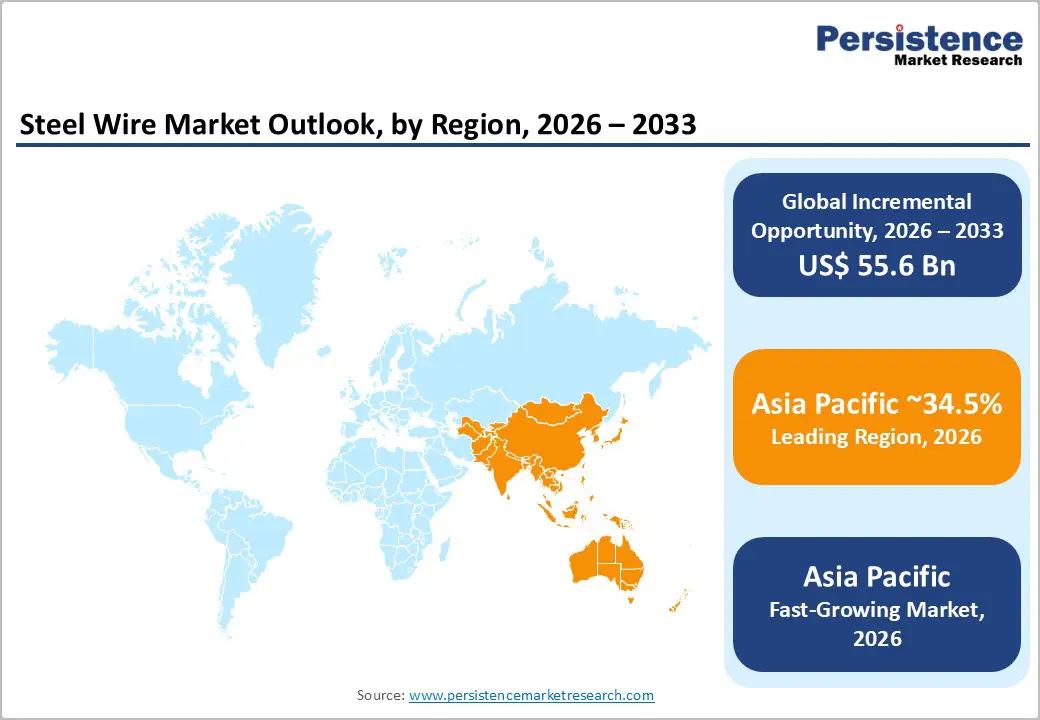

- Leading Region: Asia Pacific dominates the market, accounting for approximately 34.5% of market share, driven by large-scale infrastructure development, strong manufacturing capacity in China, and rising industrial demand across India and Southeast Asia.

- Fastest-growing Region: Asia Pacific is also projected to be the fastest-growing regional market, supported by rapid urbanization, expansion of transportation networks, and increasing automotive and manufacturing activity across China, India, Vietnam, and Indonesia.

- Investment Plans: Steel manufacturers are investing heavily in advanced wire processing technologies, capacity expansions, and low-carbon steel production, particularly in North America and Europe. Companies are upgrading cold-drawing lines, galvanizing facilities, and digital quality monitoring systems to support high-value applications in automotive, renewable energy, and infrastructure sectors.

- Dominant Product Type: Carbon steel wire is anticipated to lead, representing approximately 39.4% of market share, supported by its affordability, mechanical strength, and widespread use in construction reinforcement, fencing systems, and industrial applications.

- Leading Process Type: Hot-rolled steel wire is estimated to dominate with around 41.1% of market share, as hot rolling provides high production efficiency and serves as the primary feedstock for downstream wire drawing and industrial processing.

| Key Insights | Details |

|---|---|

| Steel Wire Market Size (2026E) | US$122.3 Bn |

| Market Value Forecast (2033F) | US$177.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Infrastructure Expansion and Global Construction Activity

Global infrastructure investment is one of the most significant drivers for steel wire demand. Steel wire is widely used in construction reinforcement, prestressed concrete systems, fencing, bridge cables, and structural support components. Governments worldwide are expanding infrastructure spending to support urbanization, transportation networks, and housing development. Public infrastructure programs covering highways, rail systems, and smart-city projects require substantial volumes of wire rods and reinforcement wires. Construction remains the largest end-use segment, accounting for approximately 39.8% of total steel wire demand, reflecting its critical role in structural integrity and load-bearing applications. The construction sector’s long-term growth trajectory is driven by rapid urbanization and population expansion in emerging economies. Developing regions continue to invest in residential buildings, industrial parks, and large infrastructure corridors. As a result, demand for carbon steel wire, galvanized reinforcement wires, and prestressing strands remains strong. For manufacturers, proximity to major construction markets improves logistics efficiency and reduces costs, giving regional wire producers a strategic advantage.

Automotive Electrification and Industrial Manufacturing Growth

Automotive manufacturing represents a key demand center for high-performance steel wires. Steel wire is used in springs, seat frames, tire reinforcement, fasteners, cables, and suspension components. The global shift toward electric vehicles has increased demand for specialized wire products used in electric motors, charging infrastructure, and precision mechanical assemblies. Electrification requires materials with improved tensile strength, corrosion resistance, and fatigue durability. This trend supports growth in stainless steel and alloy wire segments, which offer higher mechanical performance compared with conventional carbon wire. Automotive component manufacturers increasingly require cold-drawn precision wires with strict dimensional tolerances and certified quality systems. Industrial manufacturing growth also contributes to steel wire consumption, particularly in machinery, robotics, and heavy equipment sectors. As automation expands across manufacturing facilities, the need for durable mechanical components continues to grow. These trends shift the market toward higher-value specialty wire products that command premium pricing and higher margins.

Energy Infrastructure and Power Transmission Expansion

Energy infrastructure modernization represents another major growth driver. Steel wires are used in power transmission cables, offshore energy installations, oil and gas drilling equipment, and wind turbine systems. As countries invest in renewable energy and grid expansion, demand for high-tensile and corrosion-resistant wire products increases. Transmission networks require durable conductor cores and reinforcement wires capable of operating under high mechanical stress. Offshore wind installations also rely on specialized wire ropes for turbine support structures and anchoring systems. Similarly, oil and gas drilling operations require strong wire ropes for lifting equipment, subsea operations, and well-maintenance systems. Energy infrastructure projects typically operate on multi-year timelines, providing stable demand for specialized steel wire suppliers. Manufacturers capable of meeting stringent industry certifications and performance standards gain access to long-term contracts with utility companies and energy developers.

Barrier Analysis - Raw Material Price Volatility and Trade Policies

Steel wire manufacturers depend heavily on wire rod feedstock, making them highly sensitive to fluctuations in steel prices. Variations in raw material costs, including iron ore and scrap steel, directly affect production expenses and profit margins. Price swings exceeding 10% within short periods can significantly impact profitability for producers that lack integrated steelmaking operations. Trade policies and tariffs also influence market dynamics. Import duties and anti-dumping measures introduced by several governments have altered international supply chains. These policies increase uncertainty for manufacturers relying on cross-border raw-material procurement. As a result, companies increasingly pursue localized production strategies or long-term supply agreements to stabilize input costs.

High Capital Requirements and Technological Barriers

The steel wire industry requires substantial capital investment in rolling mills, cold-drawing equipment, coating facilities, and quality testing laboratories. Modern production lines must meet strict performance standards and regulatory requirements, especially for automotive and energy applications. Establishing a new cold-drawing facility or coating line can require significant financial investment, depending on capacity and technology sophistication. Smaller producers often struggle to finance such upgrades, limiting their ability to compete in high-value specialty segments. As a result, many mid-scale producers remain concentrated in commodity-grade carbon wire markets where pricing pressure is higher, and profit margins are lower.

Opportunity Analysis - Growth in Premium Stainless and Alloy Steel Wire

Premium stainless steel and alloy wire segments represent one of the most attractive opportunities in the industry. These products are widely used in automotive components, aerospace systems, medical devices, and chemical processing equipment, where corrosion resistance and durability are essential. Stainless and alloy wires typically command higher average selling prices than conventional carbon wires due to their advanced material properties and manufacturing complexity. Companies that invest in advanced cold-drawing technology, heat treatment processes, and surface finishing capabilities can enter higher-margin market segments. As industrial applications demand longer service life and improved reliability, premium wire products continue to gain market share.

Value-Added Services and Smart Wire Technologies

Manufacturers are increasingly exploring digital solutions and service-based business models to differentiate their offerings. Smart wire systems integrated with sensors allow real-time monitoring of structural loads, wear conditions, and fatigue performance in industrial equipment. Such technologies are particularly valuable in mining, construction cranes, offshore energy platforms, and heavy lifting operations. Predictive maintenance solutions based on sensor data help operators reduce downtime and improve safety. Beyond technology integration, companies are also expanding value-added services such as customized wire solutions, pre-cut bundles, and technical support for infrastructure projects. These services strengthen long-term customer relationships and improve supplier differentiation in competitive markets.

Emerging Market Manufacturing and Local Production

Rapid urbanization and industrialization in emerging economies create substantial demand for steel wire products. Infrastructure expansion, transportation networks, and manufacturing growth drive long-term consumption of construction-grade wire and industrial cables. Localized manufacturing provides cost advantages by reducing transportation expenses and avoiding import tariffs. Establishing production facilities near major construction clusters and industrial zones improves delivery speed and operational efficiency. Emerging economies in Asia and parts of Africa are increasingly investing in domestic steel production capacity. These developments create opportunities for global wire manufacturers to establish regional partnerships, joint ventures, or localized production hubs to capture new demand.

Category-wise Analysis

Product Type Insights

Carbon steel wire is anticipated to account for approximately 39.4% of the market share in 2026, making it the largest product segment by volume and revenue. Carbon steel wires are widely used in construction reinforcement, industrial equipment, fencing, and general-purpose engineering applications due to their affordability and strong mechanical properties. Major infrastructure projects, including bridge construction, reinforced concrete structures, and cable systems, consume significant volumes of carbon steel wire. For example, high-tensile carbon steel wires are used in pre-stressed concrete strands for highways, railways, and high-rise buildings, particularly in rapidly urbanizing economies such as China and India.

Manufacturers prefer carbon steel wire for applications where corrosion resistance or specialized performance characteristics are not essential. The availability of raw materials and efficient mass production processes allows producers to supply large volumes at competitive prices. Large integrated steel producers such as ArcelorMittal and Nippon Steel manufacture extensive carbon wire rod portfolios used in construction and industrial supply chains, reinforcing the segment’s leadership position.

Stainless steel wire is the fastest-growing segment due to its superior corrosion resistance, strength, and durability. Stainless wires are widely used in automotive systems, food processing equipment, chemical plants, marine infrastructure, and medical devices, where hygiene and corrosion protection are critical. For instance, stainless steel is commonly used in surgical instruments, orthodontic devices, and filtration systems in the healthcare and pharmaceutical industries. Industrial sectors increasingly require materials capable of withstanding harsh environmental conditions, including high humidity, temperature fluctuations, and exposure to chemicals. Stainless steel wires provide longer service life and improved reliability, making them suitable for demanding applications such as oil refineries, desalination plants, and offshore energy installations. The growing adoption of electric vehicles and precision engineering components also drives demand for high-quality stainless and alloy wires used in battery structures, fasteners, and lightweight assemblies.

Process Type Insights

Hot-rolled processing is anticipated to account for about 41.1% of the market share in 2026, making it the most widely used manufacturing method. Each process affects the final mechanical properties, surface quality, and application suitability of the wire, allowing producers to meet the varying performance requirements of industrial end users. Hot rolling produces wire rods that serve as feedstock for further processing, including drawing, coating, or galvanizing. The method allows efficient large-scale production and is commonly used for construction-grade wires, industrial cables, fencing products, and reinforcement materials.

Steel mills with integrated rolling facilities, such as Tata Steel, POSCO, and JFE Steel, operate high-capacity hot rolling lines capable of producing millions of tons of wire rods annually. These products are widely used in infrastructure projects, including bridges, suspension cables, and reinforced concrete structures. Hot-rolled wires offer high production efficiency and relatively low manufacturing costs, making them suitable for large infrastructure projects and mass-market industrial applications.

Cold-rolled and cold-drawn wire represents the fastest-growing segment within the processing category. Cold processing improves dimensional accuracy, tensile strength, and surface finish by drawing the wire through precision dies at controlled temperatures. These characteristics are essential for precision components used in automotive manufacturing, industrial machinery, aerospace parts, and electronic equipment. Cold-drawn wires are commonly used in fasteners, springs, precision shafts, and high-performance cables.

For example, automotive manufacturers rely on cold-drawn steel wires for engine valve springs, suspension systems, and safety-critical components that require high fatigue resistance. The rise of automation, robotics, and electric vehicle production has significantly increased demand for precision wire components with strict quality specifications. As a result, many steel producers are investing in advanced multi-stage cold-drawing machines, surface treatment technologies, and heat-treatment systems to expand their capabilities in high-value wire manufacturing.

Regional Insights

North America Steel Wire Market Trends - Infrastructure Modernization and Power Grid Expansion Driving High-Strength Wire Demand

North America represents a technologically advanced steel wire market characterized by strong demand from infrastructure development, automotive manufacturing, and energy sector investments. The region accounts for a significant share of global steel wire consumption, with the U.S. serving as the largest market due to its extensive construction sector, large automotive manufacturing base, and strong industrial ecosystem. Federal infrastructure programs, including the U.S. Infrastructure Investment and Jobs Act, allocate hundreds of billions of dollars toward transportation networks, bridges, and utilities modernization. These projects require large volumes of steel wire for reinforcement cables, suspension bridge strands, and pre-stressed concrete systems used in highways and railway infrastructure. Infrastructure modernization programs continue to drive demand for high-strength steel wire products across the region. Bridge rehabilitation projects, railway electrification, and power transmission upgrades all rely heavily on galvanized and high-tensile wire products.

For instance, companies such as Insteel Industries, a leading U.S. manufacturer of pre-stressed concrete strand and welded wire reinforcement, have expanded production capabilities to support growing infrastructure demand. The expansion of renewable energy infrastructure in North America also contributes to increased steel wire demand. Wind turbine installations require specialized wire components for structural reinforcement, anchoring systems, and cable assemblies. Large renewable energy developers in the U.S. increasingly rely on high-strength galvanized wires capable of withstanding extreme environmental conditions. Companies such as Prysmian Group, which operates major cable manufacturing facilities in North America, have expanded their production of transmission cables and high-performance wire components used in power grid modernization and offshore wind energy projects.

Investment activity in North America increasingly focuses on upgrading manufacturing capabilities. Steel producers are investing in advanced cold-drawing technologies, automated coating facilities, and quality testing laboratories to improve product consistency and performance. In recent years, companies have also integrated digital monitoring systems into wire manufacturing processes to optimize production efficiency and predictive maintenance for heavy industrial equipment. As a result, North America continues to maintain stable and technologically advanced market growth, supported by infrastructure investments, energy transition initiatives, and a robust industrial manufacturing base.

Europe Steel Wire Market Trends - Automotive Engineering and Low-Carbon Steel Innovation Shaping Advanced Wire Production

Europe represents a highly specialized steel wire market characterized by strong emphasis on technological innovation, sustainability, and advanced manufacturing capabilities. Countries such as Germany, the U.K., France, and Spain represent key consumption centers for high-performance steel wire products used in automotive production, industrial machinery, and energy infrastructure. Germany plays a central role in the European steel wire market due to its strong automotive and engineering sectors.

Automotive manufacturers require precision wire products used in suspension springs, control cables, safety systems, and reinforcement components. Major steel producers such as thyssenkrupp AG and Saarstahl AG supply high-strength wire rod and specialty steel wire used by automotive manufacturers across Europe. For example, Saarstahl has expanded production of ultra-high-strength wire rod used in safety-critical automotive components and high-performance springs. The strong presence of automotive manufacturers, including BMW Group and Volkswagen AG, further supports demand for advanced wire materials used in vehicle engineering and lightweight structural systems.

European regulations promoting low-carbon steel production have significantly influenced manufacturing strategies across the region. The European Union’s Green Deal and decarbonization policies encourage steel producers to reduce emissions through the adoption of electric arc furnace technology and the increased use of recycled scrap metal. In response, companies such as ArcelorMittal have launched initiatives to develop low-carbon steel production technologies across Europe. These initiatives are expected to influence downstream steel wire production by enabling manufacturers to offer environmentally responsible steel products that align with European sustainability targets.

European companies are also actively investing in advanced alloy development and materials research. Steel producers and engineering firms collaborate with research institutions to improve material strength, corrosion resistance, and fatigue performance in high-performance wire products. For example, Bekaert, headquartered in Belgium, continues to expand its portfolio of advanced steel wire solutions used in automotive reinforcement, industrial cables, and construction applications. Bekaert’s research initiatives focus on improving durability and reducing material weight, supporting the automotive sector’s transition toward energy-efficient vehicle designs.

Asia Pacific Steel Wire Market Trends - Large-Scale Infrastructure Growth and Industrial Expansion Fueling Steel Wire Consumption

Asia Pacific is projected to lead the market, accounting for approximately 34.5% of market share in 2026, and representing the fastest-growing regional market. Rapid industrialization, urbanization, and infrastructure development drive strong consumption of steel wire products across construction, manufacturing, automotive, and energy sectors. China remains the largest producer and consumer of steel wire globally due to its extensive construction sector and massive industrial manufacturing base. Large infrastructure programs, including high-speed railway expansion, urban transit systems, and residential construction projects, generate strong demand for reinforcement wires, industrial cables, and structural steel products.

Chinese steel producers such as China Baowu Steel Group and HBIS Group operate large integrated steel plants that produce wire rod feedstock used for downstream steel wire manufacturing. These companies have also invested in advanced rolling and wire processing facilities to improve product quality and expand export capacity for specialty wire products used in international markets.

India represents another rapidly expanding market for steel wire consumption. Government programs focused on infrastructure development, including highway expansion, railway modernization, and urban housing construction, are increasing demand for steel reinforcement materials. The Indian government’s initiatives, such as “Make in India” and large-scale infrastructure investments, have encouraged domestic steel producers to expand wire rod production. Companies such as Tata Steel and JSW Steel have invested in expanding wire rod mills and downstream processing facilities to serve growing domestic demand for construction-grade and industrial wire products. Tata Steel, for instance, has enhanced production capabilities at its Jamshedpur facility to supply high-tensile wire rod used in construction and automotive manufacturing. Investment activity across the Asia Pacific region focuses on expanding steel production capacity, upgrading rolling mills, and improving wire drawing technologies.

Many companies are also integrating automation and digital monitoring systems to improve production efficiency and product quality. The region’s combination of large infrastructure spending, strong manufacturing growth, and expanding industrial ecosystems ensures that Asia Pacific will remain the most influential region in the global steel wire market over the coming decade.

Competitive Landscape

The global steel wire market demonstrates a mixed structure combining large integrated steel producers with numerous regional wire manufacturers. Commodity wire production is relatively fragmented, with many small and mid-sized manufacturers supplying local construction markets. The specialty wire segment is more concentrated among technologically advanced companies capable of producing high-performance stainless, alloy, and coated wires.

These companies often operate integrated production systems that include steelmaking, rolling, drawing, and finishing processes. Competition is based on manufacturing efficiency, product quality, technological innovation, and geographic reach. Companies with global distribution networks and advanced processing technologies maintain strong positions in high-value applications such as automotive, energy, and industrial machinery. Leading companies focus on product innovation, geographic expansion, vertical integration, and operational efficiency. Strategic partnerships with automotive and energy companies also strengthen supply chain integration and long-term customer relationships.

Key Industry Developments:

- In June 2025, ArcelorMittal completed the acquisition of Nippon Steel Corporation’s stake in AM/NS Calvert, gaining full ownership of the advanced steel processing facility in the U.S. The move strengthens ArcelorMittal’s capability in high-value steel products and supports supply to automotive and industrial sectors that utilize specialty wire and steel components.

- In November 2025, Bekaert signed a partnership agreement with EMSTEEL to develop sustainable high-end steel solutions manufactured in the UAE, focusing on advanced wire and reinforcement technologies for infrastructure and construction markets across the Middle East and North Africa.

Companies Covered in Steel Wire Market

- ArcelorMittal

- Bekaert

- Nippon Steel Corporation

- Tata Steel Limited

- POSCO Holdings

- JFE Steel Corporation

- Kobe Steel Ltd.

- Baowu Steel Group

- Nucor Corporation

- Voestalpine AG

- JSW Steel Ltd.

- Hyundai Steel Company

- Kiswire Ltd.

- WireCo WorldGroup

- Usha Martin Limited

- Heico Wire Group

- Bridon-Bekaert Ropes Group

- Dorstener Wire Tech

Frequently Asked Questions

The global steel wire market is estimated to reach US$122.3 billion in 2026.

The global steel wire market is projected to reach US$177.9 billion by 2033.

Key trends include growing adoption of stainless and specialty alloy wires, increasing investments in advanced cold-drawing technologies, expansion of renewable energy infrastructure, and development of low-carbon steel production methods.

Carbon steel wire is the leading product segment, accounting for approximately 39.4% of global consumption, primarily due to its cost efficiency and widespread use in construction, fencing, and general industrial applications.

The steel wire market is projected to grow at a CAGR of 5.5% between 2026 and 2033.

Major companies include ArcelorMittal, Bekaert, Nippon Steel Corporation, Tata Steel Limited, and POSCO Holdings.