- Executive Summary

- Global Silicon Carbide Fibers Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Mn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Product Lifecycle Analysis

- Global Parent Market Overview

- Silicon Carbide Fibers Market: Value Chain

- List of Raw Form Supplier

- List of Manufacturers

- List of Distributors

- List of End Use Industry Industries

- Profitability Analysis

- Forecast Factors - Relevance and Impact

- Covid-19 Impact Assessment

- PESTLE Analysis

- Porter Five Force’s Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Form Landscape

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- Other Macro-economic Factors

- Price Trend Analysis, 2020 - 2033

- Key Highlights

- Key Factors Impacting Product Prices

- Prices By Product Type /Form/Usage

- Regional Prices and Product Preferences

- Global Silicon Carbide Fibers Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Market Size and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) Analysis and Forecast

- Historical Market Size Analysis, 2020-2025

- Current Market Size Forecast, 2020-2033

- Global Silicon Carbide Fibers Market Outlook: Service Type

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis By Product Type , 2020 - 2025

- Current Market Size (US$ Mn) Forecast By Product Type , 2026 - 2033

- Amorphous

- Crystalline

- Market Attractiveness Analysis: Product Type

- Global Silicon Carbide Fibers Market Outlook: Form

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis By Form, 2020 - 2025

- Current Market Size (US$ Mn) Forecast By Form, 2026 - 2033

- Continuous Fibers

- Woven Fibers

- Other Forms

- Market Attractiveness Analysis: Form

- Global Silicon Carbide Fibers Market Outlook Usage

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis By Usage, 2020 - 2025

- Current Market Size (US$ Mn) Forecast By Usage, 2026 - 2033

- Composite Applications

- Non-Composite Applications

- misc.

- Market Attractiveness Analysis: Usage

- Global Silicon Carbide Fibers Market Outlook End Use Industry

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis By End Use Industry, 2020 - 2025

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 - 2033

- Aerospace & Defense

- Automotive

- Energy & Power

- Electronics & Semiconductor

- Miscellaneous

- Market Attractiveness Analysis: End Use Industry

- Key Highlights

- Global Silicon Carbide Fibers Market Outlook Region

- Key Highlights

- Historical Market Size (US$ Mn) Analysis By Region, 2020 - 2025

- Current Market Size (US$ Mn) Forecast By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Silicon Carbide Fibers Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Form

- By Usage

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- U.S.

- Canada

- Current Market Size (US$ Mn) Forecast By Product Type , 2026 - 2033

- Amorphous

- Crystalline

- Current Market Size (US$ Mn) Forecast By Form, 2026 - 2033

- Continuous Fibers

- Woven Fibers

- Other Forms

- Current Market Size (US$ Mn) Forecast By Usage, 2026 - 2033

- Composite Applications

- Non-Composite Applications

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 - 2033

- Aerospace & Defense

- Automotive

- Energy & Power

- Electronics & Semiconductor

- Miscellaneous

- Market Attractiveness Analysis

- Europe Silicon Carbide Fibers Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Form

- By Usage

- By End Use Industry

- By Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Türkiye

- Rest of Europe

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- U.S.

- Canada

- Current Market Size (US$ Mn) Forecast By Product Type , 2026 - 2033

- Amorphous

- Crystalline

- Current Market Size (US$ Mn) Forecast By Form, 2026 - 2033

- Continuous Fibers

- Woven Fibers

- Other Forms

- Current Market Size (US$ Mn) Forecast By Usage, 2026 - 2033

- Composite Applications

- Non-Composite Applications

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 - 2033

- Aerospace & Defense

- Automotive

- Energy & Power

- Electronics & Semiconductor

- Miscellaneous

- Market Attractiveness Analysis

- East Asia Silicon Carbide Fibers Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Form

- By Usage

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- China

- Japan

- South Korea

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- U.S.

- Canada

- Current Market Size (US$ Mn) Forecast By Product Type , 2026 - 2033

- Amorphous

- Crystalline

- Current Market Size (US$ Mn) Forecast By Form, 2026 - 2033

- Continuous Fibers

- Woven Fibers

- Other Forms

- Current Market Size (US$ Mn) Forecast By Usage, 2026 - 2033

- Composite Applications

- Non-Composite Applications

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 - 2033

- Aerospace & Defense

- Automotive

- Energy & Power

- Electronics & Semiconductor

- Miscellaneous

- Market Attractiveness Analysis

- South Asia & Oceania Silicon Carbide Fibers Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Form

- By Usage

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- U.S.

- Canada

- Current Market Size (US$ Mn) Forecast By Product Type , 2026 - 2033

- Amorphous

- Crystalline

- Current Market Size (US$ Mn) Forecast By Form, 2026 - 2033

- Continuous Fibers

- Woven Fibers

- Other Forms

- Current Market Size (US$ Mn) Forecast By Usage, 2026 - 2033

- Composite Applications

- Non-Composite Applications

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 - 2033

- Aerospace & Defense

- Automotive

- Energy & Power

- Electronics & Semiconductor

- Miscellaneous

- Market Attractiveness Analysis

- Latin America Silicon Carbide Fibers Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Form

- By Usage

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- U.S.

- Canada

- Current Market Size (US$ Mn) Forecast By Product Type , 2026 - 2033

- Amorphous

- Crystalline

- Current Market Size (US$ Mn) Forecast By Form, 2026 - 2033

- Continuous Fibers

- Woven Fibers

- Other Forms

- Current Market Size (US$ Mn) Forecast By Usage, 2026 - 2033

- Composite Applications

- Non-Composite Applications

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 - 2033

- Aerospace & Defense

- Automotive

- Energy & Power

- Electronics & Semiconductor

- Miscellaneous

- Market Attractiveness Analysis

- Middle East & Africa Silicon Carbide Fibers Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Form

- By Usage

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Current Market Size (US$ Mn) Forecast By Country, 2026 - 2033

- U.S.

- Canada

- Current Market Size (US$ Mn) Forecast By Product Type , 2026 - 2033

- Amorphous

- Crystalline

- Current Market Size (US$ Mn) Forecast By Form, 2026 - 2033

- Continuous Fibers

- Woven Fibers

- Other Forms

- Current Market Size (US$ Mn) Forecast By Usage, 2026 - 2033

- Composite Applications

- Non-Composite Applications

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 - 2033

- Aerospace & Defense

- Automotive

- Energy & Power

- Electronics & Semiconductor

- Miscellaneous

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Apparent Production Capacity

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- SGL Carbon

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- SGL Carbon

- NGS Advanced Fibers Co., Ltd.

- Nippon Carbon Co., Ltd.

- UBE Corporation

- Specialty Materials, Inc.

- COI Ceramics, Inc.

- Matech

- BJS Ceramics GmbH

- Suzhou Saifei Group Ltd.

- American Elements

- Nanoshel LLC

- Haydale Graphene Industries Plc

- SkySpring Nanomaterials, Inc.

- NINGXIA ANTELI CARBON MATERIAL CO. LTD

- SGL Carbon

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Advanced Materials

- Silicon Carbide Fibers Market

Silicon Carbide Fibers Market Size, Share, and Growth Forecast, 2026 - 2033

Silicon Carbide Fibers Market by Product Type (Amorphous SiC Fibers, Crystalline SiC Fibers), Form (Continuous Fibers, Woven Fibers, Other Forms), Usage (Composite Applications, Non-Composite Applications) Industry (Aerospace & Defense, Automotive, Energy & Power, Electronics & Semiconductor, Miscellaneous) and Regional Analysis for 2026 - 2033

Silicon Carbide Fibers Market Size and Trends Analysis

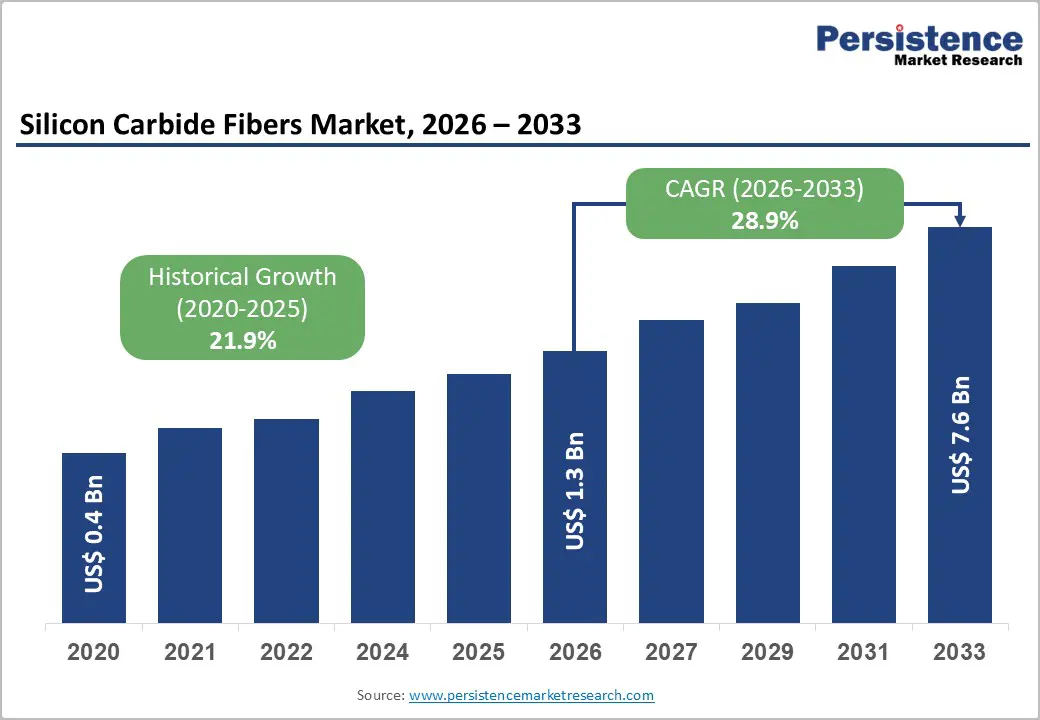

The global silicon carbide fibers market size is likely to be valued at US$ 1.3 billion in 2026 and is projected to reach US$ 7.6 billion by 2033, growing at a CAGR of 28.9% between 2026 and 2033.

This exceptional growth trajectory reflects the convergence of three critical demand drivers: aerospace and defense modernization requiring advanced thermal materials, automotive electrification demanding precision components for high-temperature applications, and renewable energy infrastructure expansion necessitating durable materials for extreme operating environments.

Key Industry Highlights:

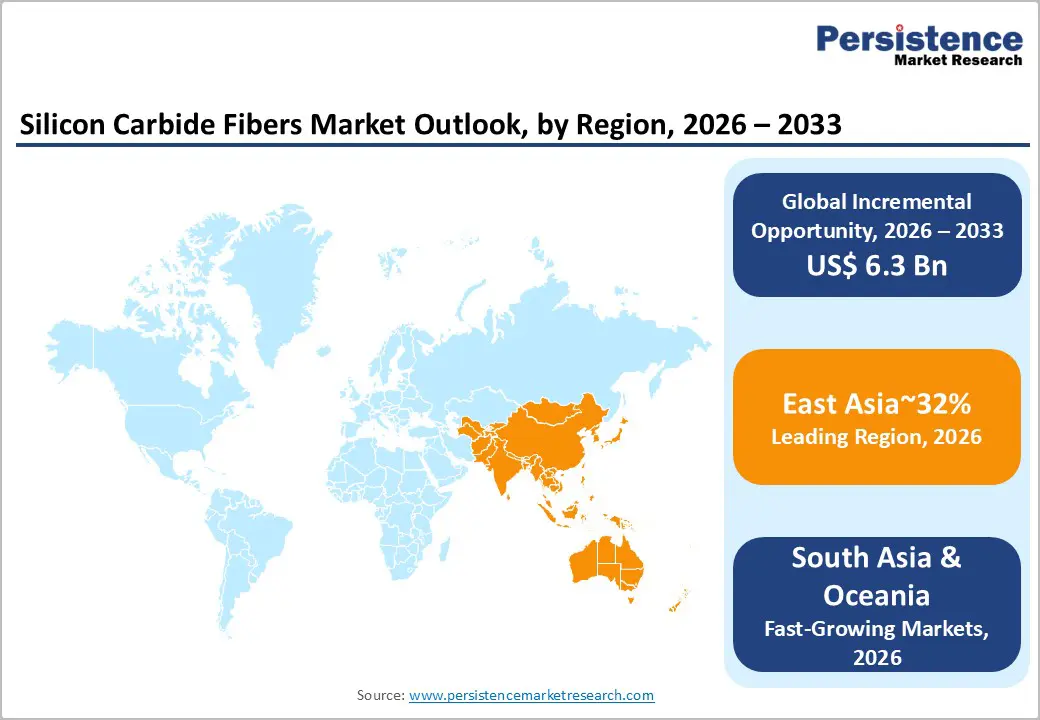

- Regional Leadership: East Asia leads the Global Silicon Carbide (SiC) Fibers Market with ~32% share, supported by Japan’s dominant SiC fiber manufacturing base and expanding aerospace, defense, and advanced materials programs across China and South Korea.

- Leading Product Segment: Crystalline silicon carbide fibers dominate with ~60% share, reflecting their superior high-temperature stability, creep resistance, and qualification for aerospace and defense ceramic-matrix composite applications.

- Fastest-Growing Product Type: Amorphous SiC fibers are the fastest-growing segment, benefiting from lower manufacturing costs and rising adoption in automotive thermal management, electronics, and industrial applications.

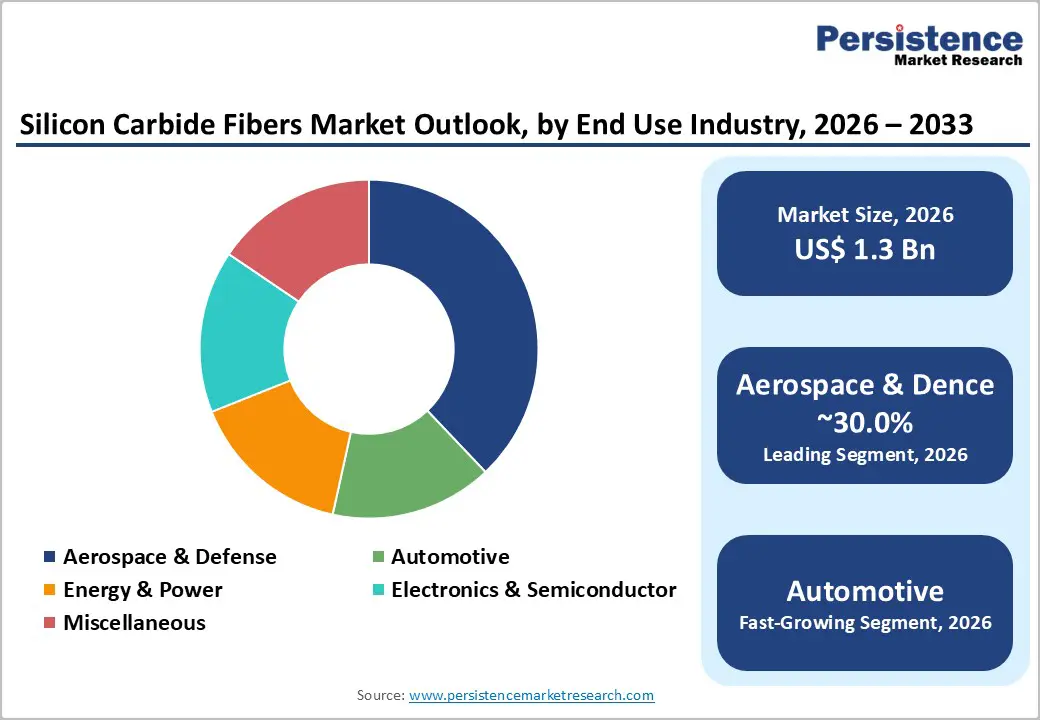

- Leading Industry: Aerospace & Defense remains the largest end-use segment with ~30% share, supported by long-term aircraft production cycles, propulsion system upgrades, and sustained government-funded R&D programs.

| Key Insights | Details |

|---|---|

| Silicon Carbide Fibers Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 7.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 28.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 21.9% |

Market Dynamics

Growth Drivers

Aerospace and Defense Propulsion System Advancement and Material Performance Requirements

The aerospace and defense sectors represent the primary catalysts for silicon carbide fiber adoption, driven by the imperative to develop lighter, thermally superior propulsion systems capable of sustained operation at elevated temperatures while minimizing weight and fuel consumption. The European aerospace and defence industry generated €325.7 billion in turnover in 2024, representing a 10.1% year-on-year increase and accounting for 24.4% of the global aerospace and defence market.

The defence sector specifically achieved €183.4 billion in turnover, reflecting 13.8% year-on-year growth, with military aeronautics accounting for 240,000 jobs and experiencing 10.1% employment expansion. These metrics underscore sustained investment in advanced aerospace systems incorporating ceramic matrix composite components manufactured from silicon carbide fibers. The U.S. aerospace and defense industry generated nearly US$995 billion in total business activity during 2024, supporting 914,000 direct employees with an average annual wage of US$115,000 56% above the national average, reflecting the sector's skill-intensive nature and capital intensity.

The silicon carbide fibers market demand stems directly from next-generation turbofan engine development, military aircraft modernization programs, and advanced propulsion system requirements across North America, Europe, and the Asia-Pacific regions. GE Aviation's investment of over US$200 million in silicon carbide fiber production facilities in Huntsville, Alabama, exemplifies the aerospace sector's commitment to establishing reliable domestic supply chains and achieving high-volume production capability. Government-funded research and development initiatives focused on advanced materials development create explicit incentives for the commercialization of silicon carbide fibers and for capacity expansion. The sustained demand visibility across decades-long aircraft development and procurement cycles provides structural support for the Silicon Carbide Fibers Market throughout the forecast period.

Automotive Industry Electrification and Thermal Management System Complexity

The automotive sector's transition toward electric and hybrid-electric powertrains creates unprecedented demand for materials capable of managing elevated thermal loads and providing lightweight structural performance. Global car registrations increased 5% in the first half of 2025, led by China's 12% growth, while the European Union saw a modest 2.4% decline amid regulatory transitions and energy cost pressures. The shift toward zero-emission vehicles and 800-volt battery architectures fundamentally transforms thermal management requirements, as power electronics generating elevated heat loads require advanced cooling solutions and thermal protection systems. The commercial vehicle market experienced regional variation, with European van production declining 6.8%, while the truck and bus segments faced ongoing challenges related to fleet renewal and transition costs for zero-emission vehicles.

The silicon carbide fibers market is expanding in automotive applications due to emerging requirements for thermal barriers, heat exchanger components, and electrical insulation materials in high-temperature zones of EV powertrains. Weak demand from the wind and semiconductor segments reported by SGL Carbon during 2024 and early 2025 reflects current supply-demand imbalances, yet the underlying automotive industry transformation toward electrification creates medium-term tailwinds for the adoption of advanced materials. As automotive manufacturers complete platform transitions and stabilize EV production, procurement of specialized thermal management materials is expected to accelerate, supporting sustained expansion of the silicon carbide fibers market.

Energy Transition Infrastructure and Renewable Power System Development

The global energy transition, accelerating renewable capacity deployment and modernizing conventional power generation systems, creates substantial demand for materials capable of withstanding extreme thermal and chemical operating conditions. According to the International Energy Agency, clean energy deployment accelerated sharply, with more than 560 GW of renewable capacity added in 2023 and annual investment approaching US$2 trillion, nearly double fossil fuel supply investment. China accounted for 60% of new renewable capacity in 2023, with solar photovoltaic generation projected to exceed the total electricity demand of the United States by the early 2030s. This unprecedented deployment scale creates demand for advanced materials in solar thermal receivers, heat exchangers in concentrated solar power facilities, and components within next-generation nuclear power systems.

Silicon carbide fibers market benefits from energy infrastructure modernization across multiple vectors: wind turbine high-temperature components, gas turbine upgrades enabling higher operating temperatures, hydrogen production and processing equipment, and thermal management systems in advanced power generation platforms.

The IEA indicates that fossil fuel demand is expected to peak within the decade as emerging economies, particularly India, Southeast Asia, the Middle East, and Africa, drive growth in energy services through electrification and renewable deployment. This structural transition toward clean energy systems fundamentally increases demand for materials providing exceptional thermal stability, oxidation resistance, and durability within demanding industrial applications, positioning silicon carbide fibers as critical enablers of energy transition infrastructure development.

Market Restraining Factors

Manufacturing Capacity Constraints and Global Supply Bottlenecks

Despite strong demand signals, silicon carbide fiber production capacity remains severely constrained, creating a critical supply bottleneck that limits market penetration across emerging applications. Global manufacturing capacity remains concentrated among limited suppliers, with production volumes insufficient to satisfy demand across aerospace, defence, automotive, and energy sectors simultaneously.

The capital-intensive nature of SiC fiber production, requiring specialized chemical vapour deposition or polymer precursor pyrolysis facilities that exceed US$200 million in investment, creates formidable barriers to capacity expansion. Extended facility construction timelines (typically 3-5 years) create structural lags between demand recognition and capacity availability. SGL Carbon's Carbon Fibers business unit posted negative adjusted EBITDA of approximately €27 million in 2024, highlighting manufacturing profitability challenges inherent to advanced fiber production. These structural supply constraints effectively limit market expansion despite strong end-customer demand signals across aerospace, defense, and emerging automotive applications.

Opportunity - Commercial Aerospace and Hypersonic Vehicle Platform Development

Commercial spacecraft manufacturers and hypersonic vehicle developers represent emerging application domains with substantial potential for silicon carbide fiber demand, addressing markets currently underserved by existing aerospace and defense suppliers. Reusable spacecraft platforms under development by multiple operators require thermal protection systems and hot-structure components capable of withstanding multiple launch cycles and extreme re-entry thermal loads, previously addressed only with single-use expendable materials. The rapid commercialization of space access through suborbital and orbital vehicle operators creates new demand vectors distinct from traditional defense and commercial aviation markets.

Silicon carbide fiber market opportunities extend to advanced thermal protection system development, where ceramic matrix composite materials incorporating SiC fibers offer superior performance compared to conventional insulation materials.

The technical feasibility validation of carbon fiber-reinforced silicon-carbide composites for reusable spacecraft thermal protection demonstrates a commercialization pathway for emerging applications. As regulatory frameworks for commercial space operations stabilise and insurance/certification requirements mature, the economic justification for investment in advanced materials strengthens substantially, potentially unlocking significant new demand volumes. Hypersonic vehicle development programs across government and emerging commercial sectors are anticipated to generate procurement opportunities as platforms transition from development to operational deployment phases, creating multi-decade demand visibility extending through the 2030s and beyond.

Industrial Decarbonization and Advanced Manufacturing Process Optimization

Manufacturers across energy-intensive industrial sectors face mounting pressure to achieve carbon neutrality objectives while maintaining competitive production economics, a dual imperative creating substantial opportunities for materials enabling operational efficiency improvements and thermal performance optimization. Industrial furnaces, chemical processing equipment, and thermal processing systems incorporating silicon carbide fiber components enable temperature increases of 50-100°C, translating directly into energy efficiency improvements and reduced carbon footprints. Advanced heat recovery systems utilising SiC composite materials extract waste heat at elevated temperatures previously unrecoverable with conventional materials, converting thermal energy back into productive use within industrial processes.

The silicon carbide fibers market expansion within industrial decarbonization pathways encompasses multiple complementary applications: high-temperature heat exchangers optimized for elevated operating temperatures, thermal barrier coatings that extend equipment service life while reducing energy consumption, and structural components for hydrogen production and hydrogen-fueled power generation systems.

Hydrogen economy development represents a particularly significant opportunity, as hydrogen production facilities and hydrogen-fueled power generation systems require materials capable of withstanding aggressive chemical environments at elevated temperatures, precisely the performance envelope where silicon carbide fiber composites demonstrate clear technical and economic advantages. Government decarbonization targets, carbon pricing mechanisms, and industrial modernization cycles collectively create multi-decade opportunities for silicon carbide fiber adoption across diverse industrial applications, distinct from traditional aerospace and defense sectors and addressable through emerging lower-cost manufacturing technologies under development.

Category-wise Analysis

Product Type Insights

Crystalline SiC Fibers dominate the silicon carbide fibers market with 60% share in 2026, reflecting superior high-temperature performance, exceptional creep resistance, and mechanical strength required for aerospace and defense applications where thermal extremes and structural integrity demands justify premium material costs. Crystalline silicon carbide fibers exhibit a fine crystalline microstructure with minimal oxygen content, enabling strength maintenance at temperatures exceeding 1,400°C and demonstrating outstanding creep resistance over extended operational periods critical for turbine engine applications. The crystalline fiber segment's dominance reflects decades of aerospace qualification achievements, established supply chain integration with major original equipment manufacturers, and proven performance track records across commercial turbofan engines and military aircraft propulsion systems.

Amorphous SiC Fibers represent the fastest-growing product category, expanding as manufacturing costs decline and new applications in moderate-temperature regimes (500-1,000°C) validate alternative material properties and manufacturing approaches. Amorphous silicon carbide exhibits isotropic material properties, demonstrates improved processability via chemical vapor deposition at lower temperatures, and enables cost reduction through simplified manufacturing workflows compared to crystalline fiber production methods. This segment's growth acceleration is particularly pronounced in emerging electronics applications, photonics platforms, and preliminary automotive thermal management components, where cost optimization supersedes maximum thermal performance requirements. As amorphous SiC fiber technology reaches manufacturing maturity and production costs decline substantially, addressable markets are anticipated to expand into industrial equipment, renewable energy systems, and emerging markets currently constrained by the affordability of crystalline fibers.

Industry Insights

Aerospace & defense holds a commanding 30% market share in 2026, reflecting the sector's unique combination of exceptional thermal performance requirements, stringent reliability standards, and financial capacity to invest in premium materials for mission-critical applications. The commercial turbofan engine market represents the primary driver, with next-generation platforms incorporating ceramic matrix composite turbine shroud liners and thermal protection components manufactured from silicon carbide fibers. Military aviation modernization programs across North America, Europe, and the Asia-Pacific region drive sustained demand for advanced propulsion systems incorporating CMC components, offering weight reduction and thermal performance advantages.

The U.S. aeronautics and aircraft sector employed 468,000 direct personnel in 2024, reflecting the capital-intensive nature and scale of aerospace manufacturing. European military aeronautics employment reached 240,000, marking 10.1% year-on-year expansion driven by defence modernization initiatives.

Automotive emerges as the fastest-growing end-use segment, driven by electrification-related thermal management demands, weight reduction imperatives, and emerging structural applications in next-generation vehicle architectures. While automotive demand currently divides between silicon carbide semiconductors (power electronic devices for EV powertrains) and structural composite applications, silicon carbide fiber adoption is anticipated to accelerate substantially as thermal management systems become increasingly critical to electric vehicle performance, longevity, and consumer value perception. Battery thermal management systems, electric motor high-temperature components, and heat recovery systems represent near-term applications where SiC fiber composites provide clear performance and efficiency advantages

Regional Insights and Trends

North America Silicon Carbide Fibers Market Trends

North America commands 28% of the global silicon carbide fibers market share, corresponding to approximately US$365 million in market value during 2026, with projections reaching US$2.13 billion by 2033. The United States dominates the North American market through concentration of aerospace and defense manufacturing, with major airframe manufacturers, engine developers, and defense prime contractors driving sustained demand for advanced materials supporting next-generation platform development.

The U.S. aerospace and defense sector generated nearly US$995 billion in total business activity in 2024, with direct output of US$556 billion and supply chain contributions of US$439 billion, for a total economic value of US$443 billion, equivalent to 1.5% of U.S. nominal GDP.

Strategic government investment in domestic silicon carbide fiber production capacity exemplifies policy prioritization of supply chain security and defense industrial base resilience. GE Aviation's US$200 million investment in Huntsville, Alabama, manufacturing facilities represents the primary commercial-scale SiC fiber production operation in North America, establishing a reliable domestic supply supporting both commercial turbofan engine production and government aerospace and defense programs. Federal research and development funding for advanced materials technology development and manufacturing innovation continues to support silicon carbide fibre commercialisation and capacity expansion initiatives. The North American market's maturity, presence of global aerospace prime contractors, and government procurement frameworks create structural demand visibility extending for decades into the future, supporting sustained expansion of the Silicon Carbide Fibers Market.

Asia Pacific Silicon Carbide Fibers Market Trends

East Asia commands 32% of the global silicon carbide fibers market share, representing the fastest-growth regional market with particular strength in Japan and emerging momentum in China and South Korea. Japan hosts the world's largest commercial silicon carbide fiber manufacturing capacity, positioning the country as a critical supplier to global aerospace programs and emerging automotive applications. Japan's dominant position reflects decades of expertise in advanced ceramic materials, established relationships with international aerospace original equipment manufacturers, and government industrial policy that prioritizes advanced composite technology development and manufacturing excellence.

China's rapidly expanding aerospace manufacturing base creates substantial structural growth opportunities for silicon carbide fibers as domestic aircraft manufacturers and engine developers incorporate advanced materials into next-generation platform programs. China's defence production reached INR 1.54 lakh crore in FY 2024-25, marking the highest-ever level, while defence exports surged to INR 23,622 crore from under INR 1,000 crore in 2014, now extending to over 100 countries, including the United States and France.

India's aerospace and defence sector is experiencing exceptional growth momentum, driven by government initiatives that emphasize self-reliance and indigenous technology development. The Defence Acquisition Procedure 2020 and Defence Procurement Manual 2025 prioritise indigenous design, development, and manufacturing while establishing unified procurement frameworks, accelerating technology development, and system deployment. The region's cost-competitive manufacturing environment, expanding skilled workforce base, and government support for advanced technology commercialization position East Asia as the primary location for emerging silicon carbide fiber applications and manufacturing capacity expansion throughout the forecast period.

Europe Silicon Carbide Fibers Market Trends

Europe holds 26% of the global silicon carbide fibers market share, valued at approximately US$338 million in 2026, with projections reaching US$1.98 billion by 2033. The European aerospace and defence industry generated €325.7 billion in turnover in 2024, representing 10.1% year-on-year growth and accounting for 24.4% of the global aerospace and defence market. Employment within the aerospace and defence sector reached 1.103 million employees across European nations, with a broader economic impact supporting 4.2 million jobs when including direct, indirect, and induced employment effects.

The European defence industry achieved a turnover of €183.4 billion in 2024, reflecting 13.8% year-on-year growth driven by heightened geopolitical tensions and renewed focus on defence industrial base expansion and strategic autonomy. Military aeronautics employment expanded by 10.1% to 240,000, reflecting robust defence-sector capacity expansion and technology modernisation initiatives. European regulatory emphasis on sustainability, lifecycle carbon accounting, and circular economy principles creates distinctive market characteristics compared to North American and Asian regions, potentially favoring advanced materials with superior weight-to-performance ratios and extended operational lifespans that support lifecycle cost optimization.

Competitive Landscape

The global silicon carbide fibers market is consolidated, with leading players including SGL Carbon, NGS Advanced Fibers Co., Ltd., Nippon Carbon Co., Ltd., UBE Corporation, Speciality Materials, Inc., and COI Ceramics, Inc. These companies dominate the market through advanced R&D capabilities, strong supply chains, and long-standing relationships with key industries, including aerospace, defense, and electronics.

Market competition is largely based on fiber quality, thermal and mechanical performance, and the ability to offer customized solutions for high-temperature and high-strength applications. High technological and capital requirements limit new entrants, while collaborations, capacity expansions, and product innovations strengthen the position of top players. Although some smaller regional players exist, the market remains concentrated, with pricing and technological trends heavily influenced by these leading companies. Continuous and woven fiber forms, along with specialized applications, further enhance competitors' differentiation.

Key Industry Developments

- February 18, 2025, SGL Carbon announced the restructuring of its loss-making Carbon Fibers business unit, closing unprofitable sites and focusing on a profitable core portfolio. Despite weak demand from wind and automotive sectors, the restructuring signalled consolidation and supply rationalisation in the silicon carbide fibers segment, aimed at restoring long-term profitability.

- March 2023, Nippon Carbon Co., Ltd. Nippon Carbon expanded production capacity for its Hi-Nicalon™ SiC fibers to support rising demand from aerospace and nuclear energy applications. The move strengthened supply security for high-purity, high-temperature-resistant SiC fibers, reinforcing the company’s position in advanced ceramic matrix composites.

Companies Covered in Silicon Carbide Fibers Market

- SGL Carbon

- NGS Advanced Fibers Co., Ltd.

- Nippon Carbon Co., Ltd.

- UBE Corporation

- Specialty Materials, Inc.

- COI Ceramics, Inc.

- Matech

- BJS Ceramics GmbH

- Suzhou Saifei Group Ltd.

- American Elements

- Nanoshel LLC

- Haydale Graphene Industries Plc

- SkySpring Nanomaterials, Inc.

- NINGXIA ANTELI CARBON MATERIAL CO. LTD

Frequently Asked Questions

The global silicon carbide fibers market is projected to be valued at US$ 1.3 Bn in 2026.

The Crystalline SiC Fibers segment is expected to account for approximately 60% of the Global Silicon Carbide Fibers Market by Use Industry in 2026.

The market is expected to witness a CAGR of 28.9% from 2026 to 2033.

Silicon Carbide Fibers Market growth is driven by rising adoption of high-temperature, lightweight ceramic matrix composites in aerospace and defense propulsion systems, expanding electrification and thermal management needs in automotive platforms, and accelerating global energy transition investments requiring durable materials for advanced power generation and renewable energy infrastructure.

Key market opportunities in the Silicon Carbide Fibers Market arise from emerging demand in commercial spaceflight and hypersonic vehicle platforms for reusable thermal protection systems, alongside industrial decarbonization initiatives driving adoption of high-temperature SiC composites in energy-efficient manufacturing, hydrogen infrastructure, and advanced heat recovery systems.

Key players in the Silicon Carbide Fibers Market include SGL Carbon, Nippon Carbon Co., Ltd., UBE Corporation, NGS Advanced Fibers Co., Ltd., COI Ceramics, Inc., and BJS Ceramics GmbH.