- Medical Devices

- Shoulder Replacement Market

Shoulder Replacement Market Size, Share, Growth, and Regional Forecast, 2025 to 2033

Shoulder Replacement Market by Implant Type (Anatomical Shoulder Prosthesis, Reverse Shoulder Prosthesis), by End-user (Hospitals, Ambulatory Surgical Centers, Orthopedic Clinics), by Regional Analysis, from 2026 to 2033

Shoulder Replacement Market Share and Trends Analysis

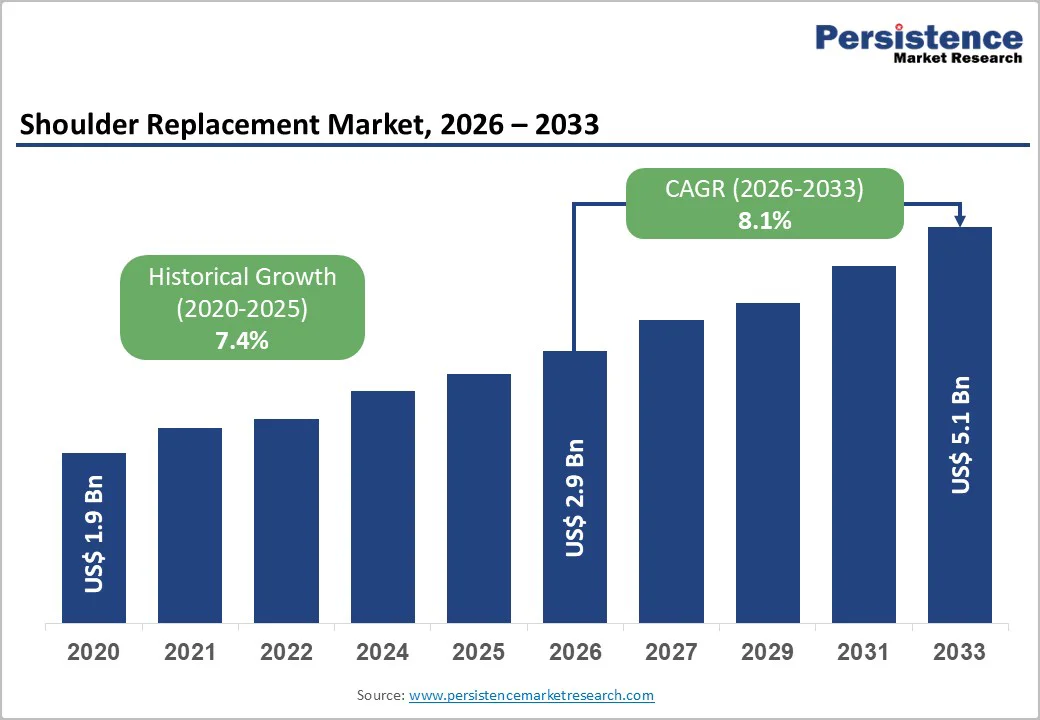

The global shoulder replacement market size is estimated to grow from US$ 2.9 billion in 2026 to US$ 5.1 billion by 2033. The market is projected to record a CAGR of 8.1% from 2026 to 2033.

The rise in incidences of arthritis is a leading cause of disability among adults and the elderly, driving demand for shoulder replacements. According to the National Institute for Health and Care Research (NIHR), 90% of shoulder replacements last at least 10 years, supporting market growth.

According to a 2025 WHO report, the expanding global geriatric population, projected to increase from 1 billion in 2020 to 1.4 billion by 2030, and the growing prevalence of osteoarthritis are further fueling the need for shoulder arthroplasty worldwide.

Key Industry Highlights

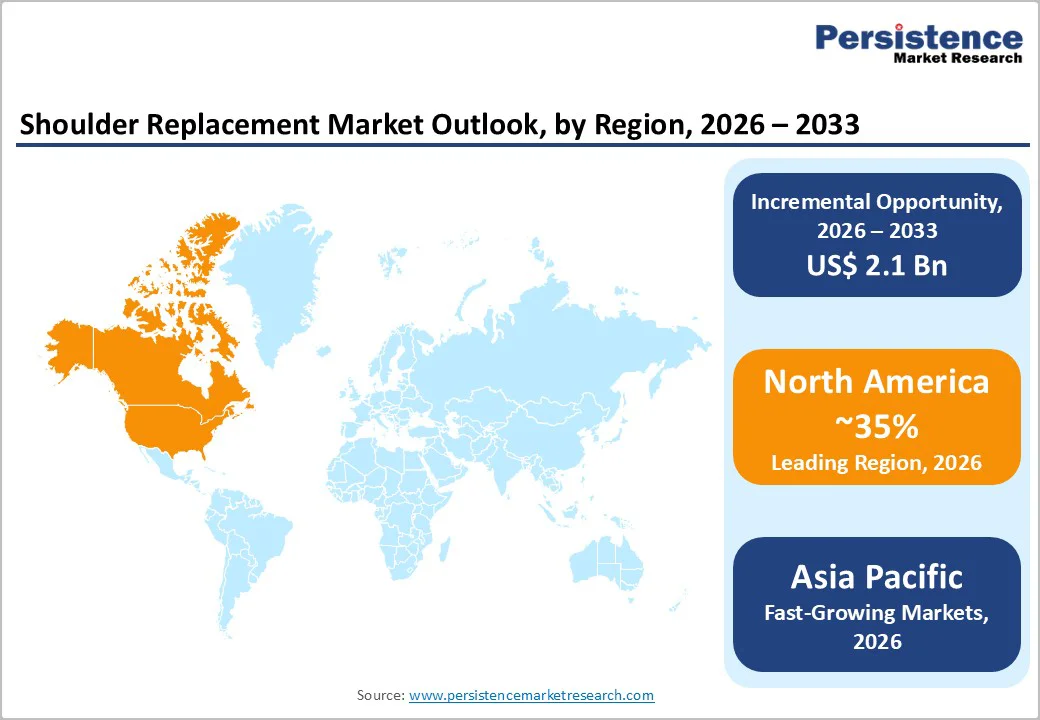

- Leading Region: North America leads the global market, supported by high procedure volumes, strong specialist infrastructure, and early adoption of reverse arthroplasty and robotic-assisted techniques.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by demographic aging, expanding hospital capacity, and improved

- reimbursement, and rising awareness of advanced joint reconstruction options among patients and surgeons.

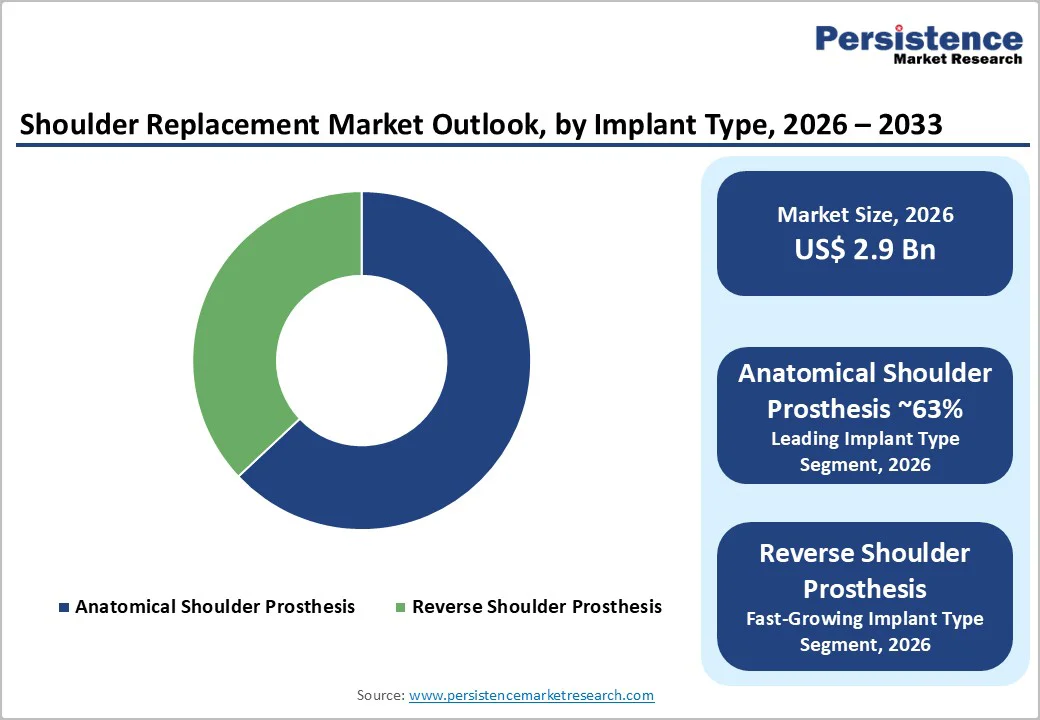

- Dominant Segment: Anatomical shoulder prosthesis remains the dominant segment due to widespread use in patients with intact rotator cuffs and the surge of stemless and bone-preserving designs.

- Fastest Growing Segment: Reverse shoulder prosthesis exhibits the highest growth, driven by expanding indications and improved surgical outcomes.

| Key Insights | Details |

|---|---|

| Shoulder Replacement Market Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 5.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.4% |

Market Dynamics

Driver - Rising Burden of Degenerative and Traumatic Shoulder Conditions

The shoulder replacement market is primarily driven by the growing prevalence of degenerative and traumatic shoulder conditions, particularly among aging populations. Glenohumeral osteoarthritis, rotator cuff tear arthropathy, and complex proximal humerus fractures are increasingly common, creating a substantial patient pool requiring surgical intervention.

Clinical studies indicate that shoulder arthroplasty volumes have more than doubled within a decade in several countries, with annual procedure growth averaging around 14%. Projections suggest that total shoulder replacements could rise by up to 700% by 2040 as surgical indications expand and life expectancy increases.

Reverse shoulder arthroplasty (rTSA) has emerged as the preferred solution for elderly patients with massive cuff tears, fracture sequelae, or failed conservative treatment, offering superior pain relief and improved functional outcomes compared with non-surgical management.

This has led to increased referrals from rheumatology, trauma, and sports medicine specialists to high-volume orthopedic centers where implant utilization is concentrated. The combined effect of rising disease prevalence, expanding indications, and improved surgical outcomes continues to fuel global market growth, creating strong demand for both anatomical and reverse shoulder prostheses, along with associated instruments and surgical support technologies.

Restraints - High Procedure and Implant Costs in Emerging Markets

High costs associated with shoulder replacement procedures and implants remain a significant restraint in emerging markets. Advanced shoulder prostheses, including anatomic and reverse designs, often carry substantial price tags, which, combined with hospitalization and perioperative expenses, limit accessibility for patients in low- and middle-income countries.

Public hospitals and smaller healthcare facilities frequently face budgetary constraints that prevent widespread adoption of premium implants or robotic-assisted surgical systems, despite their clinical advantages. Patients without comprehensive insurance coverage may delay surgery or opt for conservative non-surgical treatments such as corticosteroid injections, physiotherapy, or pain management approaches.

Additionally, high upfront capital requirements for hospitals to procure and maintain specialized instrumentation and navigation systems further limit the availability of procedures. These financial barriers contribute to slower market penetration in price-sensitive regions, creating a disparity between clinical need and access.

Consequently, cost remains a key challenge for manufacturers and healthcare providers aiming to expand shoulder arthroplasty adoption in emerging economies.

Opportunity - Digital, Robotic, and Outpatient Surgery Ecosystem

The integration of digital planning, robotic assistance, and minimally invasive surgical techniques is creating significant opportunities in the shoulder replacement market. Advanced platforms enable precise preoperative planning, accurate component positioning, and reduced intraoperative variability, improving functional outcomes and implant longevity.

For instance, in 2024, both Stryker and Zimmer Biomet received U.S. FDA approvals for robotic-assisted shoulder reconstruction, through the MAKO and ROSA systems, respectively.

Limited commercial rollouts are scheduled for 2025 to generate clinical evidence and support broader adoption. These technologies enable selected procedures to transition from traditional inpatient settings to high-throughput ambulatory surgical centers or short-stay facilities, aligning with trends in total joint arthroplasty.

Hospitals and ASCs can leverage digital and robotic capabilities to enhance operational efficiency, streamline surgical workflow, and improve patient experience. Beyond implants, the ecosystem generates recurring revenue opportunities through software licenses, maintenance contracts, and service agreements.

The convergence of robotics, digital planning, and outpatient care models represents a strategic avenue for market expansion, differentiation, and adoption of premium shoulder replacement solutions in both developed and emerging markets.

Category-wise Analysis

By Implant Type Insights

The anatomical shoulder prosthesis segment is projected to retain about 63% share of the global shoulder replacement market in 2025, supported by strong surgeon preference for restoring natural joint mechanics in patients with intact rotator cuffs and primary osteoarthritis.

Anatomical implants continue to account for nearly two-thirds of market revenue because they preserve bone, deliver reliable functional recovery, and closely mimic native kinematics in well-selected cases. Growth is further reinforced by the shift toward stemless designs, which reduce bone loss, shorten operative time, and simplify future revisions.

Hybrid glenoid components and improved biomaterials have also enhanced durability and fixation outcomes. With widespread adoption of pre-operative CT-based planning and patient-specific instrumentation, anatomical prostheses remain easier to optimize and implant accurately. Together, these trends strengthen this segment’s long-standing leadership despite rising adoption of reverse shoulder systems for massive rotator cuff tears.

By End-user Insights

Hospitals are expected to hold about 41% share of the global shoulder replacement market in 2025, remaining the primary setting for complex and high-acuity cases. Large orthopedic and tertiary-care centers continue to perform the majority of total, reverse, and revision arthroplasties due to stronger infrastructure, advanced imaging capabilities, and availability of ICU services for patients with comorbidities.

Higher procedure volumes and greater use of premium implant systems largely drive hospitals. Multidisciplinary teams, including anesthesiologists, rehabilitation specialists, and perioperative care units, support safer management of frail or elderly patients.

While ambulatory surgical centers and orthopedic clinics are increasingly performing straightforward anatomic procedures as same-day discharge protocols improve, more complex reconstructions, trauma-related replacements, navigation-assisted surgeries, and revision cases remain firmly hospital-centric. These clinical and operational advantages anchor hospitals as the leading end-user segment worldwide.

Region-wise Insights

North America Shoulder Replacement Market Trends

North America remains the largest regional market for shoulder replacement, expected to capture about 35% share by 2025, led by the U.S. High prevalence of osteoarthritis, rotator-cuff tear arthropathy, and trauma-related shoulder conditions, paired with widespread awareness of joint-replacement benefits and broad availability of fellowship-trained shoulder surgeons in specialized centers, supports strong demand.

In 2022, the U.S. recorded 146,715 shoulder replacement procedures, including total, reverse, and revision surgeries. The growing volume reflects rising demand for both traditional and reverse shoulder arthroplasty, thanks to improved implants, better surgical techniques, and expanding access through hospitals and ambulatory-surgical centers.

Well-established healthcare infrastructure and favorable reimbursement systems further support this growth, reinforcing North America’s dominance in global shoulder replacement demand.

Europe Shoulder Replacement Market Trends

Europe represents a mature but strongly innovation-oriented market for shoulder arthroplasty, supported by robust registries in countries such as Germany, the U.K., and the Nordic region that track outcomes and benchmark implant performance.

Meta-analytic work on international trends shows a broad European shift toward increasing use of reverse shoulder arthroplasty across indications, with many health systems standardizing clinical pathways and implants to reduce variability and costs.

Regulatory harmonization under the EU Medical Device Regulation (MDR) has raised evidentiary requirements for safety and performance, prompting manufacturers including Zimmer Biomet, Smith & Nephew, LimaCorporate, and B. Braun Melsungen AG to invest in post-market surveillance, registry collaborations, and design refinements.

Western European markets tend to emphasize quality and long-term survivorship, while Central and Eastern Europe present growth opportunities as hospital infrastructure improves and access to advanced joint reconstruction procedures broadens under public and private funding models.

Asia Pacific Shoulder Replacement Market Trends

Asia Pacific is emerging as one of the most promising markets for shoulder replacement, driven by rapid expansion in healthcare infrastructure, rising disposable incomes, and increasing life expectancy across major countries such as China, India, Japan and those in ASEAN. The region presents strong opportunities for implant manufacturers, as both multinational and domestic companies continue to invest in production, distribution, and physician-training programs.

Within implant types, the anatomical shoulder prosthesis segment is expected to post a robust CAGR of 7.9% through 2025, supported by growing diagnosis and treatment rates for osteoarthritis and trauma-related shoulder disorders. Reverse shoulder prostheses are also witnessing steady adoption, though at a comparatively moderate pace. Medical tourism remains a major catalyst, with competitive procedure costs attracting patients from outside the region.

Additionally, supportive government policies and incentives for local medical-device manufacturing are helping regional players strengthen their presence. Favorable demographics, expanding private hospital chains, and rising awareness about joint restoration procedures collectively reinforce the Asia Pacific’s position as a high-growth destination for shoulder replacement solutions.

Competitive Landscape

The global shoulder replacement market is moderately consolidated, with a small group of multinational orthopedic leaders holding substantial share, complemented by specialized regional manufacturers.

Key players such as Zimmer Biomet, Stryker Corporation, DePuy Synthes, Smith & Nephew, DJO Surgical (Enovis), Arthrex Inc., and Exactech compete through differentiated implant platforms spanning anatomical and reverse systems, stemless options, and convertible designs supported by pre-operative planning software and surgeon education.

Strategic priorities include portfolio expansion into stemless and augmented components, integration with navigation and robotics, targeted acquisitions, and partnerships with high-volume hospitals and orthopedic groups, while emerging companies emphasize niche indications or cost-efficient offerings for high-growth markets.

Key Industry Developments:

- In February 2024, Zimmer Biomet Holdings, Inc., a global medical technology company, announced that the U.S. Food and Drug Administration (FDA) granted 510(k) clearance for the ROSA® Shoulder System for robotic-assisted shoulder replacement procedures.

- In January 2024, Stryker, a global leader in medical technologies, launched its Tornier shoulder arthroplasty portfolio in India, introducing the Perform® Humeral Stem at the Shoulder Conclave in Pune.

Companies Covered in Shoulder Replacement Market

- DePuy Synthes

- DJO Surgical

- Integra LifeSciences

- Smith & Nephew

- Stryker Corporation

- Zimmer Biomet

- Arthrex Inc

- Lima Corporate

- Wright Medical Group

- Exactech and Tornier, Inc.

- B. Braun Melsungen AG

- Others

Frequently Asked Questions

The global shoulder replacement market is projected to be valued at US$ 2.9 Bn in 2026.

Rising osteoarthritis cases, rotator cuff arthropathy, aging populations, and improved implant designs and surgical techniques are collectively accelerating global shoulder replacement demand.

The global market is poised to witness a CAGR of 8.1% between 2026 and 2033.

Opportunities include expanding reverse shoulder systems, integrating digital planning and robotics, and developing affordable implants for rapidly growing, emerging-market procedure volumes.

Key companies include DePuy Synthes, DJO Surgical, Integra LifeSciences, Smith & Nephew, Stryker Corporation, Zimmer Biomet, and Arthrex Inc.