- Processed Food

- Sea Bream Market

Sea Bream Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Sea Bream Market is segmented by Product Type (Wild-caught, Farmed/Aquaculture), Nature (Whole, Fillets, Gutted, Others), End-user (Food Service / HoReCa, Food Processing Industry, Household Retail, Animal Feed / Aquafeed, Others), and Regional Analysis, 2026 - 2033

Sea Bream Market Share and Trends Analysis

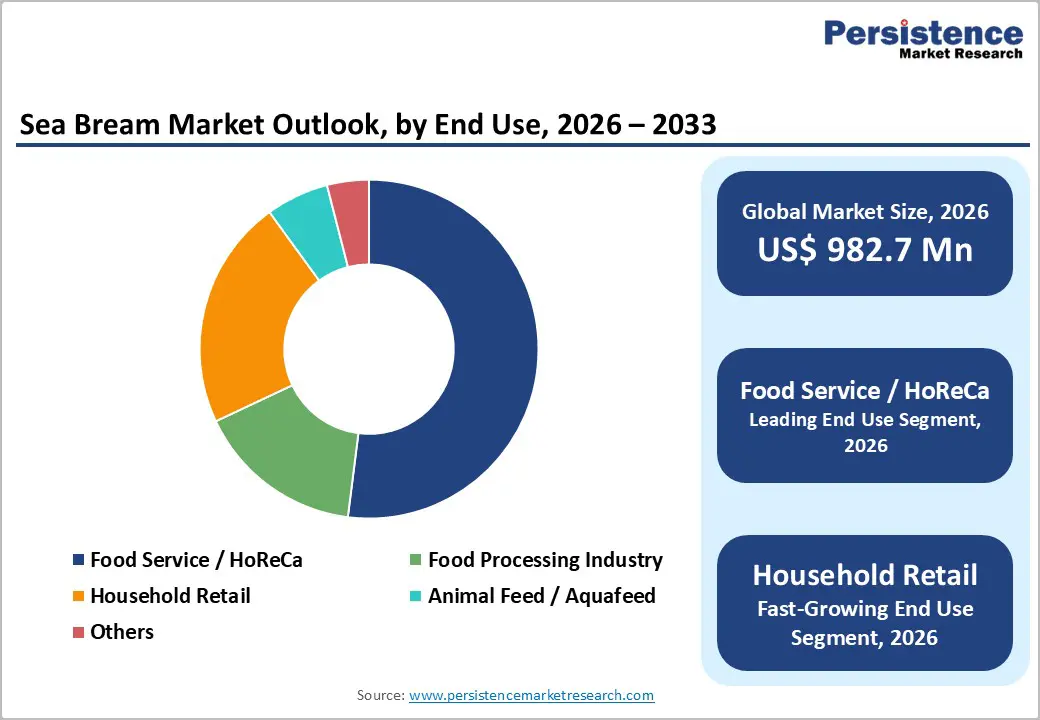

The global sea bream market size is expected to be valued at US$ 982.7 million in 2026 and projected to reach US$ 1,673.3 million by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

The market expansion is primarily driven by the escalating global demand for lean protein sources and the rapid technological maturation of offshore aquaculture systems. As wild fish stocks face increasing environmental pressure, the transition toward controlled, high-yield farming environments has intensified, ensuring a consistent year-round supply for international markets. This growth is further supported by the rising consumer preference for white fish varieties that offer high nutritional value, including Omega-3 fatty acids and essential minerals, particularly in urbanized regions where healthy dietary habits are becoming a core lifestyle priority.

Key Industry Highlights:

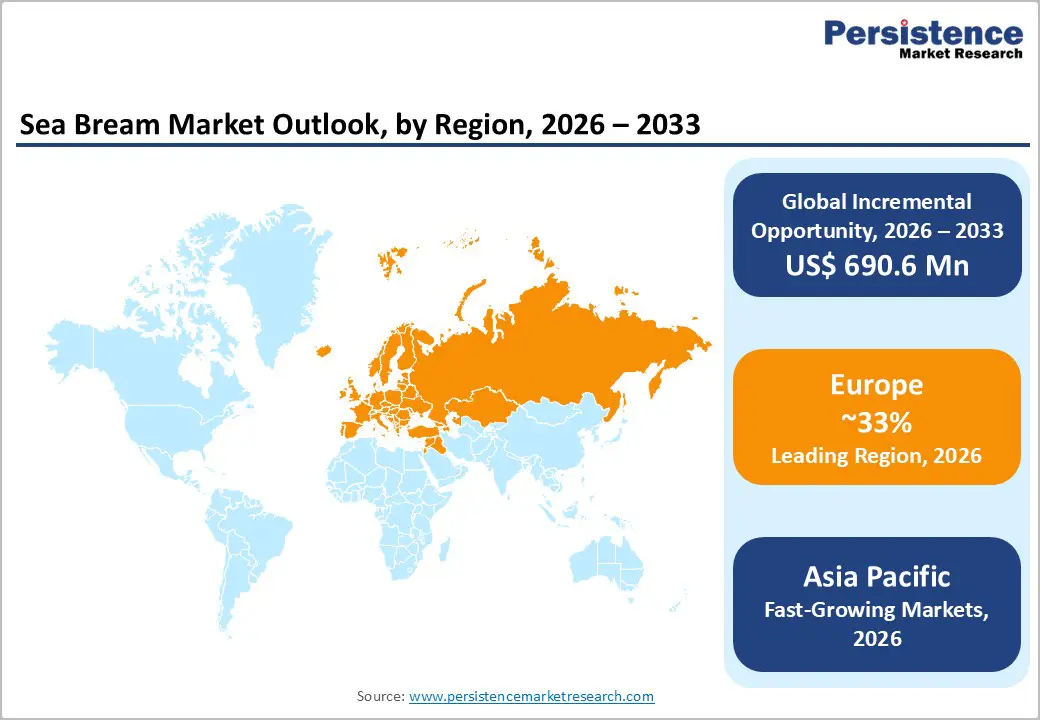

- Leading Region: Europe, holding around 33% market share, supported by strong aquaculture infrastructure, high seafood consumption in Mediterranean countries, and established export networks across Greece, Turkey, and Spain.

- Fastest-Growing Region: Asia Pacific, driven by rising disposable incomes, expanding cold-chain logistics, strong cultural demand for sea bream in Japan and China, and rapid modernization of seafood retail channels.

- Fastest-Growing Form Segment: Fillets, fueled by rising demand for convenient, ready-to-cook seafood products among household consumers and increasing retail availability of deboned, vacuum-packed portions.

- Leading Source Segment: Farmed/Aquaculture Sea Bream, dominating global supply due to consistent quality, controlled production cycles, year-round availability, and scalability compared to limited wild catches.

- Market Drivers: Rising demand for premium lean seafood proteins in the global foodservice sector is accelerating sea bream adoption as an affordable yet high-quality menu option for restaurants and hospitality chains.

- Opportunities: Rapid expansion of ready-to-cook sea bream fillets in retail markets, supported by advanced chip packaging technologies, sustainability certifications, and growing home-chef cooking trends.

- Key Developments: In June 2025, Buan Fisheries Cooperative released over 316,000 sea bream fingerlings in South Korea to support marine resource sustainability. In May 2025, Blue Waters showcased Premium Omani Sea Bream at HORECA Oman 2025, highlighting its focus on premium aquaculture products for the hospitality sector.

| Key Insights | Details |

|---|---|

| Global Sea Bream Market Size (2026E) | US$ 982.7 Mn |

| Market Value Forecast (2033F) | US$ 1,673.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 7.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Dynamics

Driver - Rising Demand for Premium Lean Proteins in the Global Foodservice Sector

The primary driver for the sea bream industry is the significant shift in the HoReCa (Hotel, Restaurant, and Cafe) sector toward high-quality, versatile white fish. According to the Food and Agriculture Organization (FAO), sea bream is highly valued in Mediterranean and Asian cuisines for its delicate flavor and firm texture, making it a staple for professional chefs. As global tourism and fine-dining experiences recover and expand, the demand for sustainably sourced fish has spiked. Major aquaculture players like Kiliç Seafood and PHILOSOFISH S.A. are leveraging advanced logistics to provide fresh, high-grade sea bream to international restaurant chains. This institutional demand ensures high volume movement, as sea bream is often positioned as an affordable yet premium alternative to more expensive species like sea bass or snapper.

Restraints - Stringent Environmental Regulations and Coastal Zoning Laws

Aquaculture operations, particularly in Europe, face rigorous scrutiny regarding their environmental footprint and impact on local ecosystems. The European Commission maintains strict guidelines on nutrient discharge, escapes, and the use of veterinary medicines in fish farms to prevent the degradation of coastal waters. These regulations often limit the number of available sites for new farm installations, creating a bottleneck for capacity expansion. Furthermore, conflicts with the tourism industry over the use of coastal space can lead to lengthy permitting processes. Such regulatory hurdles and zoning constraints can delay project timelines for companies like True North Seafood Co. Ltd., potentially slowing down the entry of new participants into the market and limiting the volume growth in traditionally dominant production hubs.

Opportunity - Rapid Expansion of Ready-to-Cook (RTC) Fillets in Household Retail

The Household Retail segment represents a massive opportunity as the fastest-growing end-use category through 2033. Modern consumers are increasingly seeking convenience without compromising on health, leading to a surge in demand for skin-on, deboned, and pre-marinated sea bream Fillets. According to reports from the National Fisheries Institute (NFI), the home-chef trend is encouraging supermarkets to stock premium, vacuum-packed fish portions that are easy to prepare. Companies that invest in high-tech processing and MAP (Modified Atmosphere Packaging) technology can capture this high-margin retail segment. By providing clear traceability and sustainability labels such as ASC or MSC certifications brands can build trust with health-conscious shoppers who are willing to pay a premium for verified sustainable products.

Category-wise Analysis

Product Type Insights

The Farmed/Aquaculture segment is the dominant force in the market, capturing the vast majority of the revenue share. This leadership is justified by the consistency in size, quality, and supply that aquaculture provides compared to the Wild-caught segment. While wild sea bream is often sought after in high-end gourmet circles for its perceived superior taste, the volume is strictly limited by fishing quotas and seasonal availability. Consequently, the industrial-scale operations of aquaculture giants ensure that sea bream remains a globally accessible commodity. As the industry moves toward Organic Farmed certifications, the gap between farmed and wild-caught perceptions is narrowing, allowing farmed products to command higher price points in premium Specialty Stores.

Nature Insights

The whole fish segment continues to hold a leading position in 2025, particularly in traditional Mediterranean and Middle Eastern markets where the fish is typically grilled or baked in its entirety. This format is favored in the Food Service / HoReCa channel for its visual appeal in restaurant presentations. However, the Fillets segment is identified as the fastest growing segment through 2032. The shift is driven by the Western consumer's demand for convenience and the reduction of food waste. Processed fillets eliminate the need for cleaning and deboning at home, making sea bream more attractive to younger demographics. Manufacturers are increasingly utilizing advanced skinning and portioning machines to meet the high standards of the Food Processing Industry.

Regional Insights

Europe Sea Bream Market Trends and Insights

Europe currently holds the leading market share of 33% in 2025, underpinned by a deep-rooted cultural affinity for Mediterranean seafood and a highly mature aquaculture infrastructure. Greece, Turkey, and Spain are the primary production hubs, with Turkey being the largest exporter of sea bream to the European Union. The region benefits from a highly coordinated regulatory framework that ensures product safety and environmental compliance.

Innovation in the European market is focused on sustainability and product differentiation. There is a notable trend toward antibiotic-free and non-GMO farmed fish, catering to the stringent demands of European retailers. The presence of key industry associations like Federation of European Aquaculture Producers (FEAP) facilitates knowledge sharing and technical standards. Furthermore, the strong integration of sea bream into the regional Food Service industry, combined with the high per-capita consumption of seafood in Mediterranean countries, ensures that Europe remains the strategic heart of the global sea bream trade.

Asia Pacific Sea Bream Market Trends and Insights

Asia Pacific is projected to be the fastest growing segment globally, with a high CAGR through 2032. This rapid expansion is primarily driven by the massive population bases and rising disposable incomes in China, Japan, and South Korea. Japan has a long history of consuming red sea bream (Madai), which is considered a symbol of good luck and is essential for traditional celebrations.

Growth dynamics in the region are shifting as modern retail formats replace traditional wet markets. The manufacturing advantages in countries like Vietnam and Thailand for seafood processing are also attracting global players to set up regional hubs. In China, the rapid growth of the Cold Chain logistics industry is enabling the distribution of fresh sea bream to inland cities, far beyond the coastal provinces. As the region's aquaculture technology catches up with European standards, Asia Pacific is expected to transition from a major importer to a significant producer, fundamentally altering the global supply landscape.

Competitive Landscape

The Sea Bream Market exhibits a moderately consolidated structure, where a few large-scale aquaculture corporations hold significant influence over global supply chains. Key market leaders like Maruha Nichiro Corporation, Kiliç Seafood, and Bakkafrost dominate the industry through vertical integration controlling everything from hatchery operations and feed production to processing and global distribution. These companies employ strategies focused on geographic expansion, technological innovation in RAS, and strategic acquisitions of smaller local farms to consolidate their market position. Key differentiators include the ability to provide consistent year-round supply and the attainment of global sustainability certifications. Emerging business model trends show a move toward Direct-to-Retail partnerships, where producers work directly with supermarket chains to shorten the supply chain and ensure maximum product freshness.

Key Developments:

- In June 2025, the Buan Fisheries Cooperative released 316,100 sea bream fingerlings into the coastal waters of Wido-myeon, Buan-gun, as part of an initiative to strengthen sea bream resource cultivation and support long-term marine stock sustainability.

- In May 2025, Blue Waters showcased its Premium Omani Sea Bream at HORECA Oman 2025, highlighting the company’s focus on high-quality aquaculture products and expanding market visibility within the hospitality and foodservice sector.

Companies Covered in Sea Bream Market

- Maruha Nichiro Corporation

- Kılıç Seafood

- P/F Bakkafrost

- Tumay Seafood

- GRUPO DELFÍN

- Dalga Seafood

- True North Seafood Co. Ltd.

- PHILOSOFISH S.A.

- Eastern Fish Company

- Galaxidi Marine Farm

- Corfu Sea Farm S.A.

- Others

Frequently Asked Questions

The global Sea Bream market is projected to be valued at US$ 982.7 Mn in 2026.

Rising Demand for Premium Lean Proteins in the Global Foodservice Sector is a major factor driving the global Sea Bream market.

The Global Sea Bream market is poised to witness a CAGR of 7.9% between 2026 and 2033.

Rapid Expansion of Ready-to-Cook (RTC) Fillets in Household Retail is a significant opportunity in the Sea Bream market.

Major players in the Global Sea Bream market include Maruha Nichiro Corporation, P/F Bakkafrost, GRUPO DELFÍN, Dalga Seafood, True North Seafood Co. Ltd., Eastern Fish Company, and others.