- Metalworking & Fabrication

- Scrap Metal Shredder Market

Scrap Metal Shredder Market Size, Share, and Growth Forecast, 2026 - 2033

Scrap Metal Shredder Market by Design Type (Diesel, Electric), Operational Type (Mobile, Stationary), Application (Iron and Stainless Steel, Aluminum and Copper), and Regional Analysis 2026 - 2033

Scrap Metal Shredder Market Share and Trends Analysis

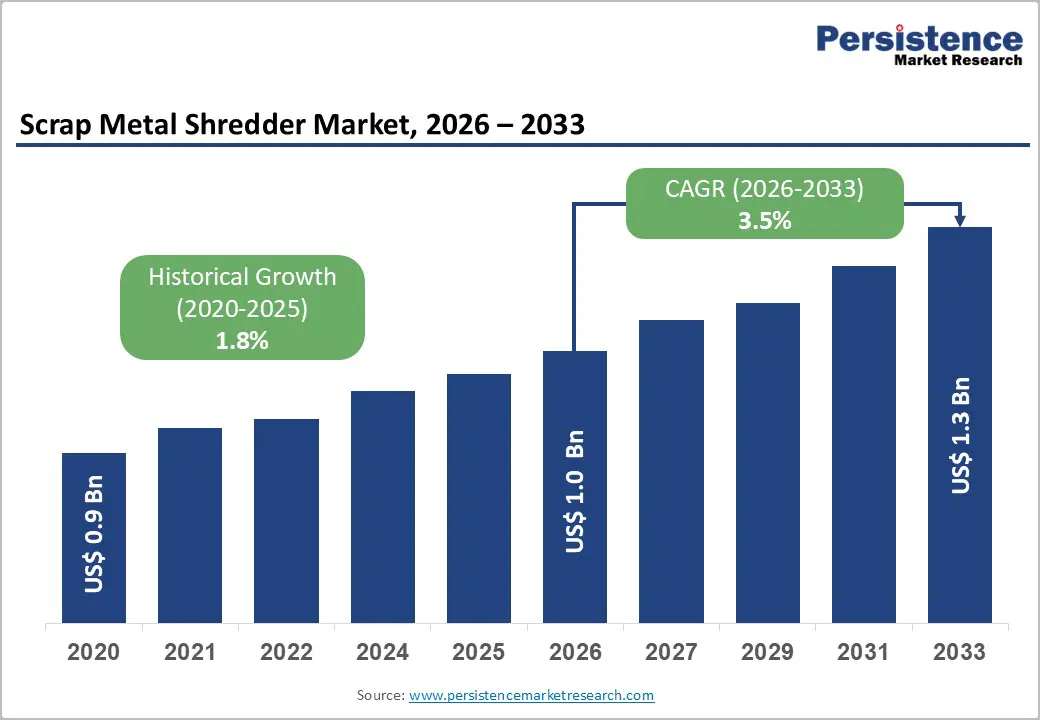

The global scrap metal shredder market size is likely to be valued at US$1.0 billion in 2026 and is expected to reach US$1.3 billion by 2033, growing at a CAGR of 3.5% during the forecast period from 2026 to 2033, driven by the shift toward decarbonization policies, which are pushing steelmakers to adopt scrap-based electric arc furnace production.

As a result, there is a rising demand for large-scale shredding systems and modern processing infrastructure. The market is benefitting from increased use of secondary metals, stricter recycling regulations, and the growing adoption of efficient, high-capacity shredders, supported by more organized scrap collection networks. Challenges such as high capital costs, permitting issues, and fluctuating scrap prices are moderating the pace of development, making it strategic and disciplined.

Key Industry Highlights

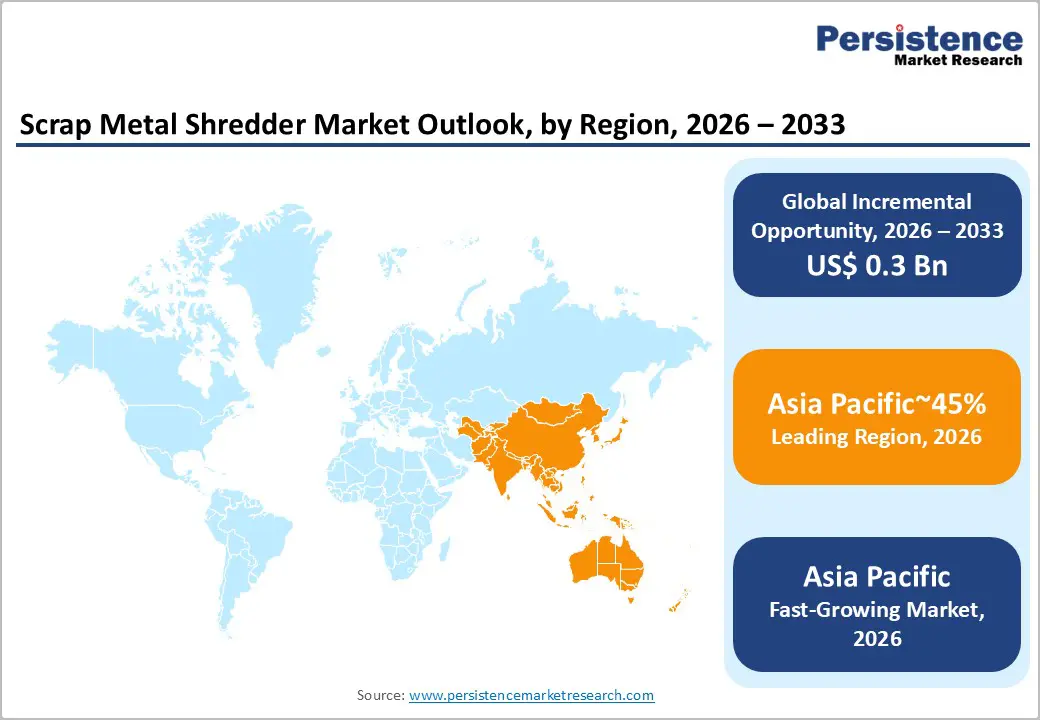

- Leading Region: Asia Pacific with 45% share, anchored by industrialization, urbanization, and robust demand for steel and non-ferrous metals.

- Fastest-growing Region: Asia Pacific to be the fastest-growing, driven by regulatory tightening, infrastructure formalization, and expansion of mobile and greenfield shredding operations.

- Leading Design Type: Diesel-powered shredders to lead with 64% share, supported by high power-to-weight ratios, grid independence, and suitability for dense ferrous scrap processing.

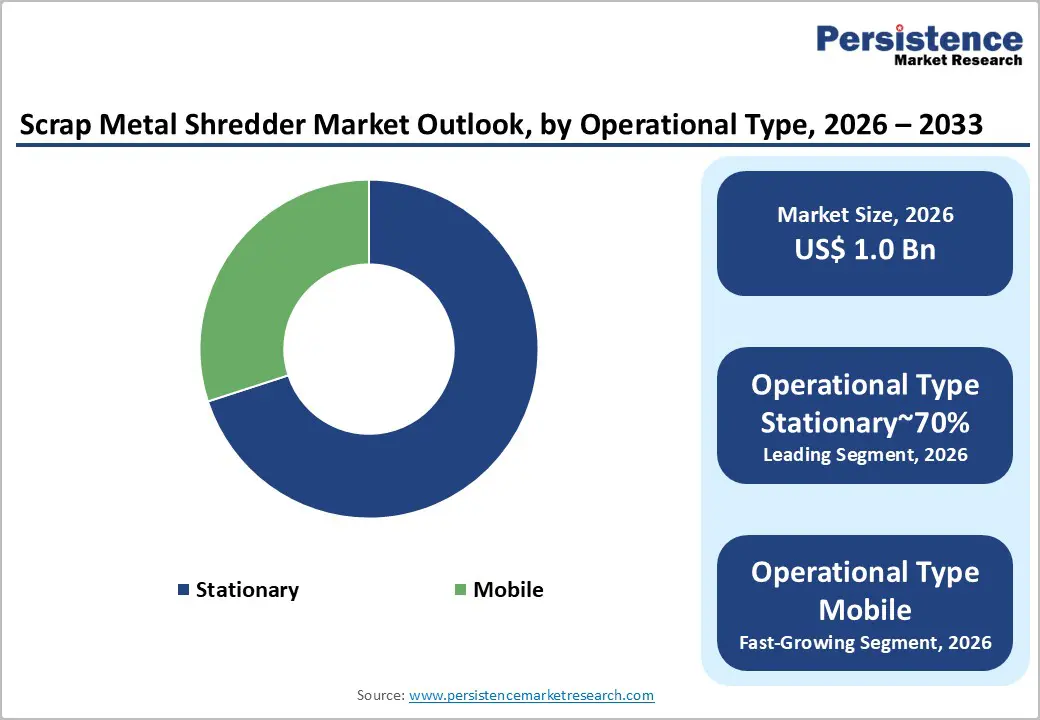

- Leading Operational Type: Stationary shredders to dominate with 70% share, underpinned by massive throughput capacity, integration with downstream sorting, and high-purity output consistency.

| Key Insights | Details |

|---|---|

|

Scrap Metal Shredder Market Size (2026E) |

US$1.0 Bn |

|

Market Value Forecast (2033F) |

US$1.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

1.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Transition to Electric Arc Furnace (EAF) Steelmaking

The steel sector’s structural transition toward electric arc furnace steelmaking is a primary demand driver for scrap shredding infrastructure. EAF routes, capable of operating on near-total scrap feedstock, deliver materially lower carbon intensity than integrated blast furnace pathways, aligning steel production economics with tightening decarbonization mandates. As climate-linked regulation, green procurement policies, and investor scrutiny intensify, steelmakers are reallocating capital toward scrap-centric production models, elevating requirements for consistently processed, contamination-controlled ferrous inputs that meet higher furnace efficiency thresholds.

This shift is translating into sustained growth in shredded scrap demand, particularly higher-grade fractions suitable for automated EAF charging and yield optimization. The projected expansion of scrap utilization volumes over the next decade directly reinforces the installed base requirement for high-capacity shredders with precision separation and throughput stability. As a result, shredder investments are increasingly positioned as enabling assets within low-emissions steel value chains, linking environmental compliance, feedstock quality, and long-term capacity planning.

Volatility in Scrap Supply and End-Market Metal Prices

Volatility across scrap supply chains and downstream metal pricing represents a persistent restraint on shredder market expansion. Operator margins remain tightly coupled to the spread between inbound scrap acquisition costs and outbound processed scrap realizations, both of which fluctuate with global ferrous and non-ferrous price cycles. During periods of compressed metal prices or softened steel mill demand, throughput utilization declines, weakening cash flows, and deferring capital commitments for new shredding lines or capacity upgrades.

Structural uncertainty further compounds this risk profile. Disruptions in collection networks, policy shifts affecting scrap exports and imports, and rising competition from alternative recycling and pre-processing technologies destabilize long-term feedstock visibility. For smaller and mid-scale operators, reliance on spot-market procurement magnifies exposure to these swings, complicating investment underwriting and extending replacement cycles. As a result, scrap and price volatility function as a moderating force on equipment demand, favoring operators with diversified sourcing, contractual off-take, and balance-sheet resilience.

Integration of AI and Smart Sorting Technologies

The integration of AI tools with shredding and sorting equipment creates a practical growth opportunity for metal recyclers. Traditional shredding mainly uses magnets, which often fail to separate valuable non-ferrous metals or fully remove copper from steel scrap. New smart systems use sensors to automatically adjust shredder speed and force during operation, while AI-supported sorting improves material separation after shredding. This results in cleaner scrap output and higher recovery of usable metals, which helps recyclers meet quality requirements from steel producers and reduce value loss.

The opportunity is strongest because many shredders already in use can be upgraded rather than replaced. Retrofit packages allow operators to improve recovery performance without heavy capital spending, making adoption more feasible during uncertain market conditions. For equipment suppliers, this shifts growth toward upgrades, controls, and software rather than only new machine sales. As scrap quality directly impacts selling prices, simple automation and smarter sorting are becoming practical tools to protect margins and improve operational stability.

Category–wise Analysis

Design Insights

Diesel-powered shredders are projected to lead the metal recycling market, accounting for approximately 64% share in 2026, anchored by their high power-to-weight ratios, grid independence, and suitability for remote or off-grid operations. Low-speed, high-torque designs, variable-speed drives, and wear-resistant alloy tooling allow diesel units to process dense ferrous scrap and whole vehicles reliably across both stationary and mobile setups. Regulatory compliance, including EPA Tier 4 Final and EU Stage V emissions standards, has driven innovations such as SCR and DPF integration, enabling diesel units to operate in urban or noise-sensitive areas. Industry leaders such as Metso, ARJES, and Hammel are expanding portfolios with hybrid-ready and telematics-enabled diesel systems, reinforcing dominance through mobility, reliability, and site versatility.

Electric-powered shredders are anticipated to be the fastest-growing segment, driven by decarbonization mandates, operational cost efficiency, and urban deployment viability. Instant full torque, variable-frequency drives, and AI-enabled predictive maintenance enhance precision, throughput, and energy optimization, while hybrid “plug-in” designs allow mobile units to leverage grid power once on-site. Adoption is catalyzed by carbon credit schemes, Extended Producer Responsibility (EPR) laws, and zero-emission requirements in green zones, making electric shredders increasingly attractive for new builds and retrofits. Leading suppliers such as UNTHA Shredding Technology and WEIMA are scaling high-capacity, energy-efficient units, embedding long-term specification advantages and accelerating market penetration across industrial and municipal applications.

Operational Type Insights

Stationary shredders are projected to lead the metal recycling market, accounting for approximately 70% share, driven by their ability to handle massive throughput, integrate with downstream sorting systems, and deliver consistent high-purity outputs. Their dimensional stability, high-power motors, and electric-drive efficiency make them indispensable for processing whole car bodies and heavy scrap at scale. Regulatory frameworks such as the ELV Directive, OSHA/HSE noise standards, and EU Waste Shipment Regulations further entrench stationary dominance by requiring high recovery rates, controlled emissions, and enclosed operations. Industry leaders, including Metso Outotec, Danieli Centro Recycling, and SSI Shredding Systems, are advancing modular and electric solutions, reinforcing TCO advantages, urban compliance, and superior material quality as structural barriers to mobile alternatives.

Mobile shredders are anticipated to be the fastest-growing operational segment, propelled by logistical efficiency, on-demand processing, and infrastructure flexibility. On-site shredding reduces transport costs, densifies scrap, and enables rapid response for SMEs, demolition contractors, and disaster recovery scenarios. Innovations such as track-mounted units, plug-in hybrid drives, remote monitoring, and quick-change rotor tooling enhance operational adaptability across diverse sites. Leading brands, including Arjes, Tana Oy, and Hammel Recycling Technik, are scaling compact high-torque designs and integrated magnetic separation for immediate sorting. Regulatory incentives for emissions, temporary permits, and circular-economy initiatives further accelerate adoption, making mobile units a flexible, low-overhead complement to stationary infrastructure.

Regional Insights

Asia Pacific Scrap Metal Shredder Market Trends

Asia Pacific is projected to remain the largest and fastest-expanding volume market for scrap metal shredders, accounting for approximately 45% market share in 2026, supported by industrialization, urbanization, and rising steel and non-ferrous metal demand. China continues to anchor regional scale as domestic scrap utilization increases following the foreign waste ban, while Japan and South Korea reflect structural maturity through advanced recycling systems and stable replacement demand. India and select ASEAN economies are expected to drive incremental growth, as construction, infrastructure, and automotive activity expand alongside the formalization of scrap collection and processing networks.

Regulatory tightening across environmental performance, workplace safety, and waste management is reshaping equipment demand toward modern shredding systems. India’s enforcement of authorized vehicle scrapping facilities from 2024 is accelerating the shift from manual dismantling to regulated shredding infrastructure, reinforcing policy-led demand. Manufacturing cost advantages and proximity to steel producers support regional deployment, while investment activity increasingly concentrates on greenfield recycling parks, mobile fleet expansion, and joint ventures integrating international technology with local execution capabilities.

North America Scrap Metal Shredder Market Trends

North America, led by the U.S., is expected to remain a mature yet structurally adaptive market, supported by high scrap generation per capita and an established network of processors and EAF-based steel mills. Sustained demand for shredded scrap is reinforced by iron and steel applications, while market value is supported by high-value-per-unit equipment sales rather than volume expansion. Integrated recyclers and mill-owned operations typically deploy high-capacity stationary electric shredders, while independent operators maintain a mixed base of stationary and mobile units to serve regional and niche demand pockets, reflecting infrastructure maturity and operational diversity.

Regulatory oversight under EPA emissions and particulate standards is expected to accelerate replacement-driven demand, particularly the transition from legacy diesel-powered units to high-efficiency electric shredders. Federal infrastructure spending has strengthened demolition scrap flows, supporting utilization rates rather than greenfield capacity. Investment activity is increasingly shaped by private equity consolidation, enabling centralized procurement of high-capacity systems, alongside targeted upgrades in energy efficiency, automation, and environmental compliance aligned with evolving state and federal guidelines.

Europe Scrap Metal Shredder Market Trends

Europe is expected to remain a structurally advanced and regulation-led market for scrap metal shredders, supported by high collection rates for end-of-life vehicles, appliances, and construction waste. Germany, France, Italy, and the U.K. anchor regional demand through mature recycling systems aligned with circular economy objectives. Operators predominantly deploy technologically advanced stationary shredders integrated with downstream separation and environmental controls, reflecting dense urban settings and a strong focus on material purity. Market positioning emphasizes value creation through compliance, efficiency, and lifecycle optimization rather than volume-led expansion.

EU-level regulatory harmonization under the Green Deal and Circular Economy Action Plan continues to shape equipment design, scrap quality standards, and trade flows. Strict noise, dust, and emissions requirements have reinforced innovation in enclosed, sound-dampened systems, consolidating demand around premium European OEMs. Investment activity is primarily modernization-driven, including two-stage shredding configurations to improve non-ferrous recovery and selective capacity additions to accommodate rising post-consumer scrap volumes linked to decarbonization and vehicle electrification trends.

Competitive Landscape

The global scrap metal shredder market is moderately consolidated, led by a small group of established international OEMs and system integrators that shape competitive dynamics in high-capacity and technologically advanced systems. Companies such as Lindemann, SSI, and Hammel hold strong influence due to their proven equipment reliability, deep process expertise, and ability to deliver integrated solutions that combine shredding, downstream separation, digital controls, and long-term service support.

Industry behavior shows growing emphasis on lifecycle services, automation, and digital monitoring, while cost-focused offerings sustain pressure in mid-range applications. Competitive intensity is expected to increase as technology adoption grows and service-driven differentiation becomes more crucial.

Key Industry Developments:

- In May 2024, UNTHA launched next-generation RS class shredders to improve maintenance efficiency and meet stricter European noise compliance standards.

- In April 2024, Zato expanded its U.S. footprint as its Blue Devil twin-shaft shredder gained steel-feedstock installations, signaling a shift away from maintenance-heavy hammer mills.

- In August 2024, India accelerated scrappage infrastructure as the RVSF count crossed 110, triggering policy-driven demand for vehicle shredding equipment.

Companies Covered in Scrap Metal Shredder Market

- Lindemann GmbH

- Zato

- Metso Corporation (Metso Metal Recycling legacy)

- Danieli Centro Recycling (Danieli Group)

- ANDRITZ AG

- SSI Shredding Systems, Inc

- BHS-Sonthofen GmbH

- Erdwich Zerkleinerungs-Systeme GmbH

- Jiangsu Wanshida Hydraulic Machinery

- JMC Recycling Systems Ltd.

- Hammermills International LLC

- Bano Recycling S.r.l.

- Hammel Recyclingtechnik GmbH

- UNTHA Shredding Technology

- Granutech-Saturn Systems

- Terex Ecotec

- ECO Technic

Frequently Asked Questions

The global scrap metal shredder market is projected to be valued at US$1.0 billion in 2026 and is expected to reach US$1.3 billion by 2033.

The scrap metal shredder market is driven by the transition toward electric arc furnace steelmaking, stricter decarbonization mandates, rising metal recycling intensity, and government-led scrappage and circular economy policies.

The scrap metal shredder market is expected to grow at a CAGR of 3.5% between 2026 and 2033, supported by expanding scrap-based steel production and organized recycling infrastructure.

Key opportunities include AI-enabled shredding systems, smart sorting and retrofit solutions, low-noise equipment for urban facilities, and intelligent maintenance platforms to improve uptime and scrap quality.

Major players include Lindemann, Metso (Metal Recycling), Danieli Centro Recycling, ANDRITZ, SSI Shredding Systems, Hammel Recyclingtechnik, UNTHA, Granutech-Saturn Systems, Zato, and Terex Ecotec.