- Metals & Minerals

- Roofing Anchors Market

Roofing Anchors Market Size, Share, and Growth Forecast, 2026 - 2033

Roofing Anchors Market by Roof Type (Flat Roofs, Pitched Roofs, Others), Product Type (Temporary Anchors, Permanent Anchors, Others), Application, and Regional Analysis for 2026 - 2033

Roofing Anchors Market Size and Trends Analysis

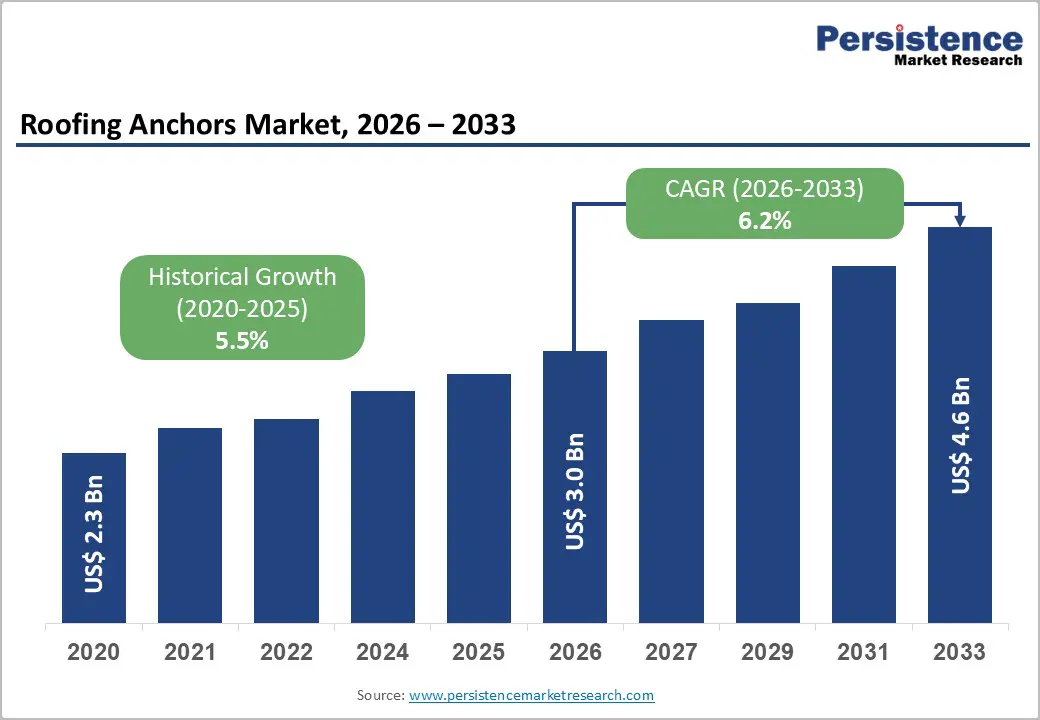

The global roofing anchors market size is likely to be valued at US$3.0 billion in 2026 and is expected to reach US$4.6 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033, driven by regulatory enforcement of fall protection standards, increasing reroofing and maintenance activity, and the adoption of engineered anchorage systems across diverse roof structures.

The mandatory nature of fall protection in construction environments ensures consistent demand, while rising infrastructure investments and urbanization further strengthen the market base. Growth is also supported by technological advancements in anchorage systems, improving installation efficiency and compliance management.

Key Industry Highlights

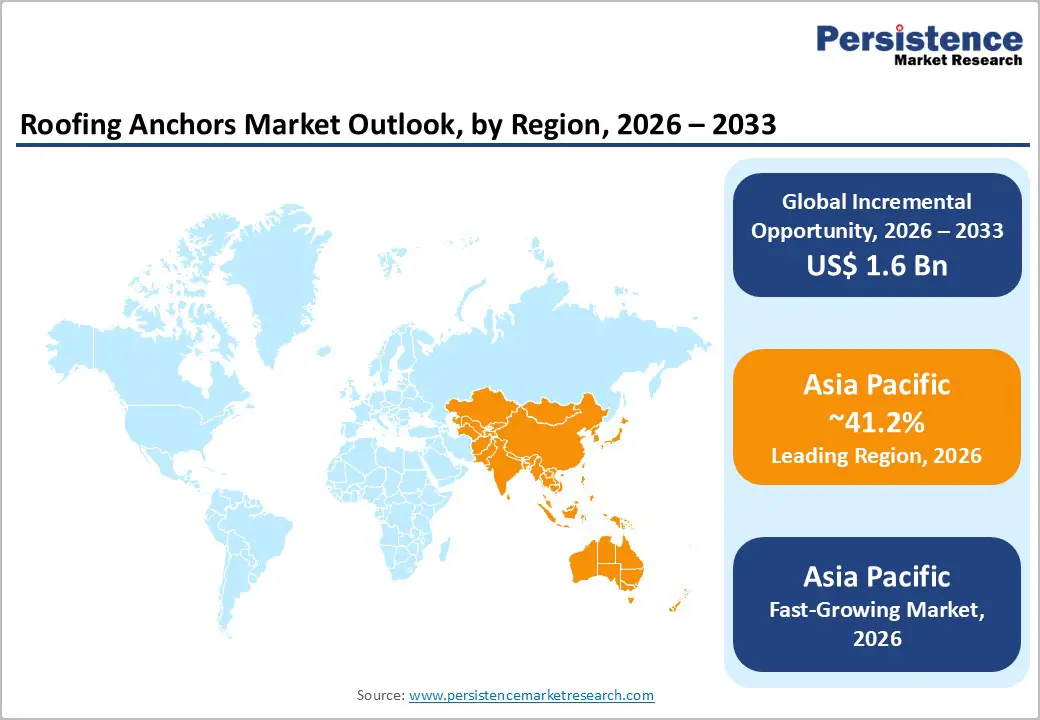

- Leading Region: Asia Pacific is projected to account for 41.2% of the market share, driven by large-scale infrastructure development and rapid urbanization.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by increasing construction activity, evolving safety regulations, and expanding industrial and commercial sectors.

- Investment Plans: Investment is primarily focused on permanent anchorage systems and digital compliance solutions, as companies prioritize lifecycle safety planning, service-based offerings, and technology integration to enhance operational efficiency.

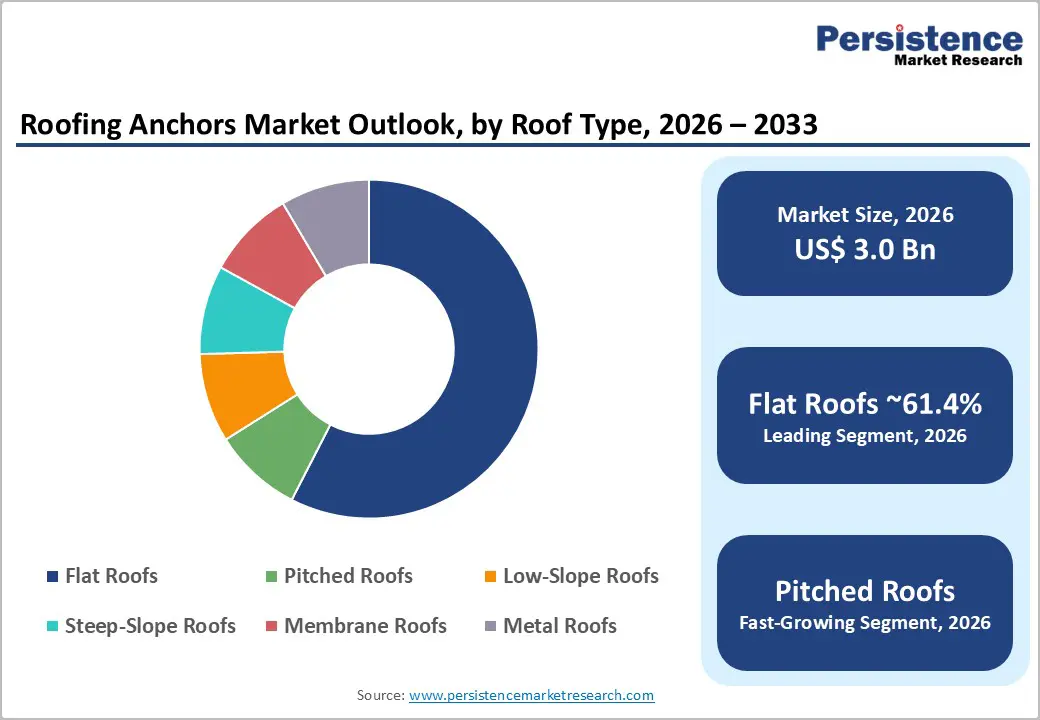

- Dominant Roof Type: Flat roofs are anticipated to dominate with a 61.4% market share, owing to their extensive use in commercial and industrial buildings that require frequent maintenance and safe access systems.

- Leading Application: The commercial segment is estimated to lead with a 37.7% market share, driven by high roof access frequency, strict safety compliance requirements, and the presence of complex rooftop infrastructure.

| Key Insights | Details |

|---|---|

| Roofing Anchors Market Size (2026E) | US$3.0 Bn |

| Market Value Forecast (2033F) | US$4.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

DRO Analysis

Driver Analysis - Regulation-Backed Replacement and Compliance Demand

Stringent fall protection regulations are the most critical driver of roofing anchor demand. In construction activities, fall protection is mandated at defined height thresholds, including roofing operations on both low-slope and steep-slope structures. Regulatory frameworks also recognize the use of permanent and reusable anchors, reinforcing their role across installation, maintenance, and repair cycles. This regulatory environment creates non-discretionary purchasing behavior, ensuring recurring demand regardless of construction cycles. Contractors and building owners must comply with safety standards, leading to consistent procurement of anchorage systems. The market implication is a stable and resilient demand structure, less sensitive to economic volatility compared to other construction components.

Ongoing Construction, Reroofing, and Maintenance Activity

Roofing anchors are closely tied to maintenance and repair cycles rather than new construction alone. Large-scale construction spending and continuous infrastructure upgrades contribute to a substantial base of roofing-related activities. Maintenance-intensive sectors such as commercial buildings, industrial facilities, and institutional infrastructure generate frequent demand for safe roof access solutions. Reroofing projects, which occur at regular intervals due to material wear and environmental exposure, further sustain the need for anchorage systems. This dynamic ensures steady replacement demand, positioning roofing anchors as essential components within lifecycle asset management strategies.

Product Innovation and System-Based Safety Solutions

The market is transitioning toward engineered, system-based anchorage solutions integrated with digital tools. Manufacturers are introducing advanced products that simplify anchor selection, improve installation accuracy, and enhance compliance tracking. Digital tools such as fall clearance calculators and estimation platforms are enabling contractors to optimize system configuration and reduce operational errors. These innovations increase the adoption of premium products, including permanent, non-penetrating, and smart anchors. From a business perspective, this trend supports value-based differentiation, allowing manufacturers to compete on performance, usability, and compliance support rather than price alone.

Restraint Analysis - Roof-Substrate Dependence and Installation Complexity

Anchorage systems require structurally sound attachment points, making installation highly dependent on roof design and condition. Older buildings, lightweight structures, and membrane-based roofs often present challenges in securing compliant anchor points. These constraints increase engineering requirements, installation time, and project costs. In retrofit scenarios, contractors may need alternative solutions such as non-penetrating systems or guardrails, which can limit the adoption of permanent anchors. As a result, installation complexity acts as a barrier, particularly in cost-sensitive or technically constrained projects.

Inspection, Certification, and Lifecycle Compliance Costs

Roofing anchors involve ongoing inspection, certification, and training requirements. Safety-critical equipment must be regularly evaluated to ensure performance and compliance with safety standards. This creates a higher total cost of ownership compared to standard construction hardware. Contractors must allocate resources for documentation, inspections, and workforce training, which can be burdensome for smaller firms. Consequently, compliance-related overhead may delay product upgrades or shift demand toward lower-cost temporary solutions, particularly in fragmented contractor markets.

Opportunity Analysis - Expansion of Permanent Anchors in Lifecycle Building Management

Permanent anchors represent a significant growth opportunity within lifecycle safety planning. Building owners are increasingly prioritizing long-term roof access solutions to support routine maintenance, inspections, and repair activities across commercial, institutional, and industrial assets. Permanent anchorage systems reduce operational friction by eliminating the need for repeated installation and removal, which not only improves efficiency but also minimizes labor risks. These systems are particularly valuable in facilities such as hospitals, warehouses, airports, and data centers, where rooftop access is frequent and must comply with strict safety protocols. As organizations shift toward planned maintenance and asset lifecycle management, the adoption of permanent anchors is supporting higher-value product demand and enabling manufacturers to generate recurring revenue through installation, inspection, certification, and after-sales service contracts.

Integration of Digital Tools and Compliance Services

Integration of digital tools and compliance services is transforming the competitive landscape. Digital transformation is creating new revenue streams beyond traditional hardware sales, with manufacturers increasingly offering software-based tools, training programs, and compliance management solutions alongside anchorage products. These tools help contractors and safety managers select appropriate systems, calculate fall clearance requirements, and ensure proper installation, thereby reducing errors and improving operational safety. In addition, digital platforms enable better documentation and audit readiness, which is critical in regulated environments. For distributors and manufacturers, this shift toward bundled solutions enhances customer engagement and fosters long-term relationships. The ability to combine physical products with digital support and training services is emerging as a key differentiator, particularly in complex or large-scale projects.

Infrastructure Growth in Asia Pacific

Infrastructure growth in Asia Pacific presents the most significant expansion opportunity for the market. With a 41.2% market share, the region leads globally and continues to expand at the fastest pace, driven by rapid urbanization and large-scale infrastructure investments. Increasing construction of commercial buildings, industrial facilities, transportation networks, and smart city projects is generating strong demand for roofing safety systems. Countries such as China, India, and Southeast Asian economies are witnessing substantial growth in logistics hubs, manufacturing units, and high-rise developments, all of which require reliable fall-protection solutions. At the same time, rising awareness of workplace safety and the gradual strengthening of regulatory frameworks are accelerating the adoption of anchorage systems. The region’s well-established manufacturing base also provides cost advantages, enabling both domestic consumption and export-oriented growth, further reinforcing Asia Pacific’s strategic importance in the market.

Category-wise Analysis

Roof Type Insights

Flat roofs are anticipated to lead, accounting for 61.4% of the market share in 2026, maintaining their leadership due to extensive adoption across commercial, industrial, and institutional infrastructure. These roof types are widely used in office buildings, warehouses, manufacturing plants, hospitals, and retail complexes, where large surface areas and accessibility requirements necessitate robust fall-protection systems. Frequent maintenance activities such as HVAC servicing, drainage inspection, waterproofing, and rooftop equipment installation significantly increase the need for reliable anchorage systems. For example, large distribution centers and logistics hubs often require continuous rooftop access for equipment servicing, making permanent anchor systems and horizontal lifelines essential. In addition, flat roofs are commonly used in data centers and shopping malls, where uninterrupted operations demand safe and efficient maintenance protocols. Regulatory alignment further strengthens this segment, as flat and low-slope roofs fall directly under defined fall-protection requirements in construction safety standards. The combination of a large installed base, recurring maintenance cycles, and compliance-driven demand ensures sustained dominance of flat roofs in the roofing anchors market.

Pitched roofs are the fastest-growing, driven primarily by expanding residential construction and increasing reroofing activities. These roofs present unique safety challenges due to their slope, requiring specialized anchorage systems such as ridge anchors, strap anchors, and adjustable roof brackets. Growth is strongly supported by applications such as residential solar panel installations, where technicians must safely access sloped surfaces for mounting and maintenance. For instance, rooftop solar projects in suburban housing developments require secure anchoring points to ensure worker safety during installation.

Similarly, storm-prone regions generate recurring demand for roof repair and replacement, further accelerating the adoption of pitched-roof anchorage solutions. Rising awareness among contractors and homeowners regarding workplace safety and liability is also contributing to increased adoption. As safety regulations and insurance requirements become more stringent, the demand for advanced anchorage systems tailored to pitched roofs is expected to grow steadily.

Application Insights

The commercial segment is anticipated to account for 37.7% of the market share in 2026, driven by the high frequency of roof access and stringent compliance requirements. Commercial buildings such as office complexes, retail malls, hotels, and warehouses require regular maintenance, inspections, and equipment servicing, all of which necessitate reliable anchorage systems. These buildings often feature complex rooftop configurations, including HVAC units, solar installations, and communication equipment, increasing the need for structured fall-protection solutions. For example, large shopping centers and airports rely on permanent anchor systems and guardrails to enable safe maintenance operations without disrupting daily activities. The scale and operational importance of commercial properties make safety compliance a priority, leading to consistent investment in both temporary and permanent anchorage solutions. This sustained demand reinforces the segment’s leading position in the market.

The residential segment is the fastest-growing, supported by increasing reroofing activity, heightened safety awareness, and expanding home improvement projects. Homeowners and contractors are increasingly adopting anchorage systems to meet safety standards and reduce risks during roofing work. Applications such as roof repairs, gutter maintenance, and solar panel installations are key contributors to demand. For instance, the rapid adoption of rooftop solar systems in residential neighborhoods requires secure anchoring solutions for installation crews working on sloped roofs. Additionally, aging housing stock in developed markets is driving reroofing projects, further increasing the need for temporary and reusable anchors. Growing awareness of occupational safety among small contractors and independent workers is also accelerating adoption. As safety regulations become more enforced and insurance requirements tighten, the residential segment is expected to witness sustained growth in anchorage system usage.

Regional Insights

North America Roofing Anchors Market Trends - Compliance-Driven Demand with Digital Safety and Permanent Anchor Adoption

North America represents a mature and highly regulated market driven by strict fall protection standards, particularly under frameworks enforced by agencies such as the Occupational Safety and Health Administration. Regulatory enforcement ensures consistent demand for roofing anchors across construction, maintenance, and repair activities, as compliance is mandatory for contractors and building owners. The region benefits from significant construction spending and a large base of existing buildings requiring regular maintenance. Commercial and industrial sectors remain the primary contributors to demand, supported by advanced safety practices and high compliance awareness.

For example, major logistics and e-commerce warehouse expansions across the U.S. have increased the need for permanent roof anchor systems to support ongoing maintenance of large flat-roof facilities. Innovation plays a critical role in shaping the market. Companies such as Guardian Fall Protection, 3M, and MSA Safety are actively investing in engineered systems and digital tools. Guardian’s 2025 rollout of AI-enabled safety selection tools and fall clearance calculators is a strong example, as it simplifies product selection and improves compliance accuracy for contractors. Investment opportunities are increasingly concentrated in permanent anchors, digital compliance platforms, and service-based safety solutions. The shift toward lifecycle safety planning, particularly in commercial real estate, healthcare facilities, and data centers, is driving demand for integrated anchorage systems that reduce long-term operational risk while improving efficiency.

Europe Roofing Anchors Market Trends - Retrofit-Led Growth with Harmonized Safety Standards and Solar Expansion

Europe’s roofing anchors market is characterized by strong regulatory frameworks and a consistent emphasis on workplace safety compliance. Regulations across the region are relatively harmonized, which allows manufacturers to standardize product offerings and scale across multiple countries. While overall construction activity has shown moderate growth, maintenance, renovation, and retrofit projects continue to drive demand. Countries such as Germany, the U.K., France, and Spain remain key contributors due to their large commercial building stock and strong enforcement of occupational safety standards. For instance, ongoing refurbishment of aging commercial infrastructure in Germany and the U.K. has increased demand for permanent and non-penetrating anchor systems.

Manufacturers such as Kee Safety, Tractel, and Petzl are focusing on engineered solutions tailored to diverse European roof types. Kee Safety’s expansion of rooftop guardrail and walkway systems across industrial and commercial buildings illustrates how companies are adapting to stricter safety expectations without compromising roof integrity. Opportunities are particularly strong in renewable energy and data infrastructure. For example, the rapid expansion of rooftop solar installations across Europe is increasing the need for safe access systems during installation and maintenance. Similarly, the growth of data centers in countries such as Ireland and the Netherlands is driving demand for permanent anchorage systems that support continuous facility management.

Asia Pacific Roofing Anchors Market Trends - High-Growth Market Driven by Urbanization and Infrastructure Development

Asia Pacific is projected to lead the market with a 41.2% market share and is also the fastest-growing region, driven by rapid urbanization, infrastructure expansion, and industrial development. Countries such as China, India, Japan, and ASEAN economies are key growth engines, supported by large-scale construction projects and increasing safety awareness. The region benefits from strong construction activity across commercial, industrial, and infrastructure sectors. For example, large-scale industrial parks and logistics hubs being developed in India and Southeast Asia require extensive roofing systems with integrated safety solutions. At the same time, high-rise commercial developments in China and Japan are driving demand for permanent anchors and engineered fall-protection systems.

Global and regional players such as KStrong, Honeywell, and Tractel are expanding their presence in Asia Pacific through localized manufacturing and distribution networks. KStrong’s strong footprint in India and Southeast Asia highlights how regional production capabilities are improving product availability and cost competitiveness. Investment opportunities are strongest in infrastructure projects, industrial facilities, and commercial buildings that require long-term maintenance solutions. The region’s growth trajectory is supported by large-scale infrastructure investment, evolving regulatory standards, and expanding manufacturing ecosystems, making Asia Pacific the most dynamic market for roofing anchors globally.

Competitive Landscape

The global roofing anchors market is fragmented, with multiple global and regional players competing across product categories. Leading companies include 3M, Honeywell, MSA Safety, Guardian, Kee Safety, Werner, Tractel, Petzl, KStrong, FallTech, Malta Dynamics, and Pelsue.

Competition is driven by product innovation, compliance support, distribution networks, and service capabilities. Companies differentiate through engineered solutions, training programs, and digital tools rather than price alone. Innovation, compliance support, and market expansion define competitive strategies. Companies focus on engineered solutions, digital integration, and training services to differentiate offerings. The shift toward solution-based selling and lifecycle support is emerging as a key trend.

Key Industry Developments

- In May 2025, Honeywell International Inc. announced the completion of the sale of its Personal Protective Equipment (PPE) business to Protective Industrial Products (PIP) for US$ 1.325 billion, aiming to streamline its portfolio and allow PIP to expand its presence in the global safety equipment and fall protection segment.

Companies Covered in Roofing Anchors Market

- 3M

- Honeywell International Inc.

- MSA Safety Incorporated

- Guardian Fall Protection

- WernerCo

- Kee Safety Ltd.

- Tractel Group

- Petzl

- FallTech

- Super Anchor Safety

- Malta Dynamics

- FrenchCreek Production Inc.

- Safe Approach Inc.

- Diversified Fall Protection

- ABS Safety GmbH

- Ferro Anchors Ltd.

Frequently Asked Questions

The global roofing anchors market size is estimated to be US$3.0 billion in 2026.

The roofing anchors market is projected to reach US$4.6 billion by 2033.

Key trends include the growing adoption of permanent anchors for lifecycle safety, increasing use of non-penetrating and engineered systems, and the integration of digital tools for compliance and system selection.

By roof type, flat roofs lead the market with a 61.4% share, primarily due to their widespread use in commercial and industrial buildings requiring frequent maintenance and safe access systems.

The roofing anchors market is expected to grow at a CAGR of 6.2% from 2026 to 2033.

Major players include 3M, Honeywell, MSA Safety, Guardian Fall Protection, and Kee Safety.