- Home Care & Utilities

- Robot Vacuum Cleaner Market

Robot Vacuum Cleaner Market Size, Share, and Growth Forecast 2026 - 2033

Robot Vacuum Cleaner Market by Product Type (Floor Vacuum Cleaner, Pool Vacuum Cleaner), by Application (Residential, Commercial, Industrial), by Distribution Channel (Offline, Online), by Regional Analysis, 2026 - 2033

Robot Vacuum Cleaner Market Size and Trend Analysis

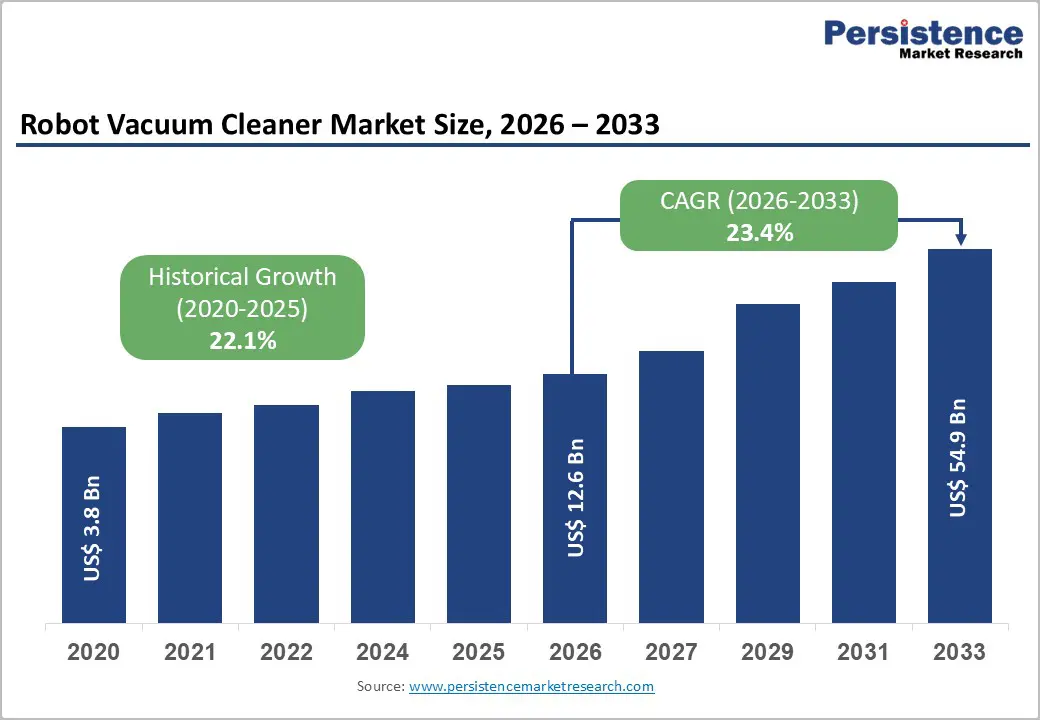

The global robot vacuum cleaner market size is expected to be valued at US$ 12.6 billion in 2026 and projected to reach US$ 54.9 billion by 2033, growing at a CAGR of 23.4% between 2026 and 2033.

Market growth is supported by increasing adoption of smart home technologies and rising demand for automated cleaning solutions that reduce manual effort in busy urban households. Continuous improvements in navigation systems, mapping capabilities, and battery efficiency are enhancing product performance and reliability. Integration with voice assistants and connected home platforms is further strengthening adoption. Additionally, rising hygiene awareness, growing pet ownership, and expanding online retail availability continue to support global demand.

Key Industry Highlights:

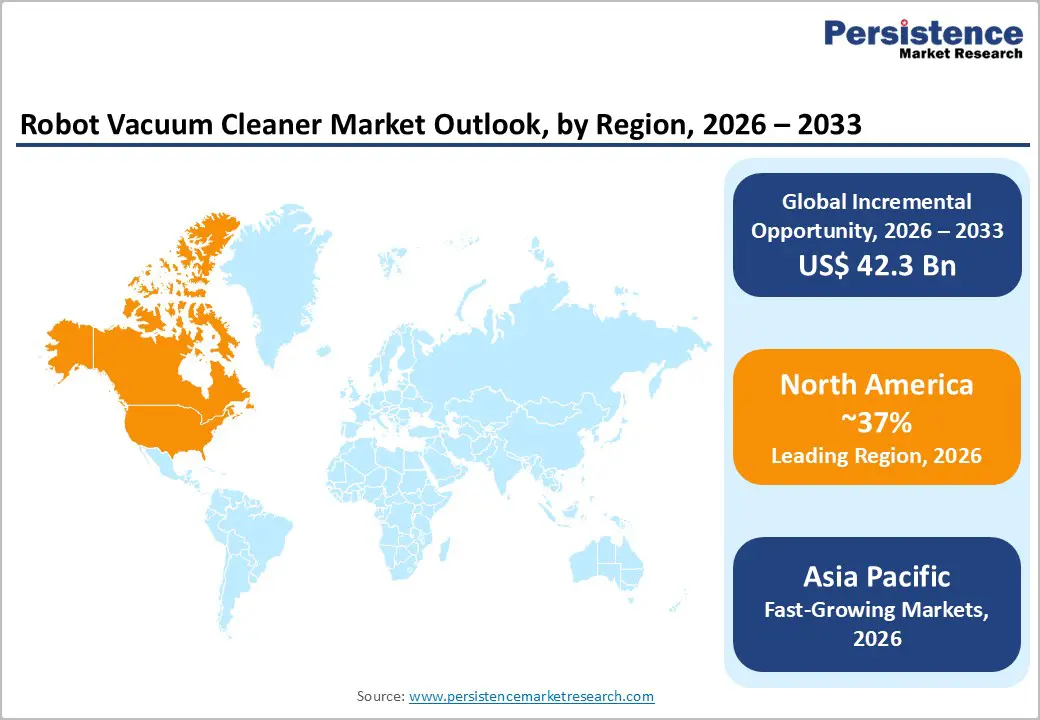

- Leading Region: North America leads the robot vacuum cleaner market with about 37% share driven by high smart home adoption and purchasing power.

- Fastest Growing Region: Asia Pacific holds around 33% share and is the fastest-growing region due to urbanization and rising middle-class demand.

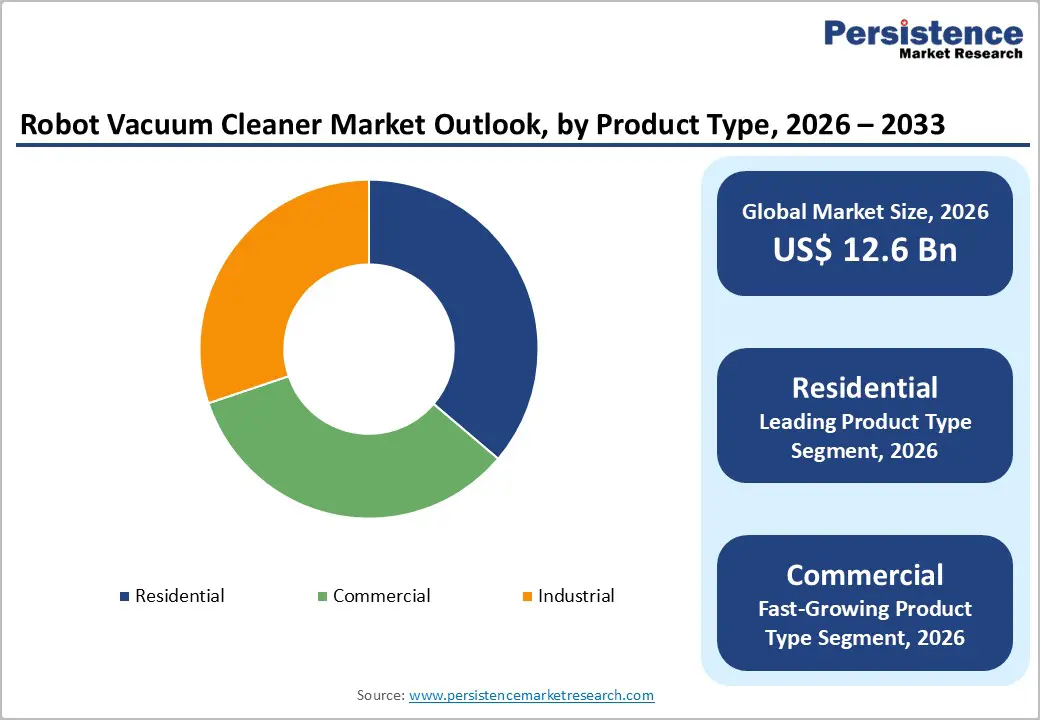

- Leading Product Category: Floor robot vacuum cleaners dominate with nearly 75% share due to widespread residential use.

- Leading Application Segment: Residential applications account for about 65% share as households increasingly adopt automated cleaning devices.

- Key Market Opportunity: Expansion into commercial spaces such as offices, hotels, and retail facilities creates strong growth opportunities for automated cleaning solutions.

| Key Insights | Details |

|---|---|

|

Robot Vacuum Cleaner Size (2026E) |

US$ 12.6 billion |

|

Market Value Forecast (2033F) |

US$ 54.9 billion |

|

Projected Growth CAGR(2026-2033) |

23.4% |

|

Historical Market Growth (2020-2025) |

22.1% |

Market Dynamics

Drivers - Growing Smart Home Ecosystems and Connected Device Integration Increasing Demand for Automated Cleaning Solutions

Rapid adoption of smart home ecosystems is a major driver of robot vacuum cleaner demand, as consumers increasingly integrate automated appliances into connected living environments. Many households now use multiple smart devices, creating a natural ecosystem where robotic cleaning solutions fit seamlessly. Robot vacuums are commonly viewed as among the most practical and visible smart home appliances, delivering everyday convenience.

These devices often integrate with voice assistants and mobile applications, allowing users to schedule cleaning routines, control devices remotely, and automate tasks with minimal effort. The ability to connect with broader home automation platforms enhances usability and perceived value, encouraging adoption among tech-savvy households seeking efficient and time-saving cleaning solutions.

Continuous Advancements in Artificial Intelligence, Sensors, and Navigation Technologies Improving Performance and User Experience

Ongoing technological advancements in robotics, artificial intelligence, and sensor technologies are significantly improving the performance of robot vacuum cleaners. Modern devices use sophisticated navigation systems, mapping tools, and environmental sensors to move efficiently across different floor layouts while avoiding obstacles, enabling more accurate cleaning paths and better coverage.

At the same time, improvements in battery efficiency, self-charging functions, and automated cleaning routines are reducing the need for user intervention. AI-driven object recognition also helps identify household items and obstacles, minimizing operational disruptions. These technological upgrades enhance reliability, improve user satisfaction, and encourage consumers to upgrade to more advanced robotic cleaning solutions.

Restraints - High Initial Purchase Costs and Ongoing Maintenance Expenses Limiting Adoption Among Price-Sensitive Consumer Segments

The relatively high upfront cost of robot vacuum cleaners remains a major restraint, particularly in price-sensitive markets. Advanced models with stronger suction, intelligent navigation, and self-emptying features are priced significantly higher than conventional vacuum cleaners, making them less accessible for many households. Consumers in developing economies often prioritize essential appliances over automated cleaning technologies.

In addition to the initial purchase price, ongoing maintenance expenses can further discourage adoption. Components such as filters, brushes, and batteries require periodic replacement over the product’s lifespan. These additional costs increase the overall cost of ownership, causing some consumers to delay purchasing decisions or avoid upgrading to newer, feature-rich robotic cleaning systems.

Limited Consumer Awareness and Connectivity Infrastructure Challenges Restricting Adoption in Developing Regions

Limited consumer awareness about the functionality and benefits of robot vacuum cleaners remains a challenge in several developing regions. Many potential buyers are unsure whether these devices can effectively clean various floor surfaces, navigate tight spaces, or handle the heavy dust accumulation common in some households.

Infrastructure limitations also restrict the full utilization of connected features in certain areas. Inconsistent internet connectivity and limited access to reliable wireless networks can reduce the effectiveness of app-based controls, mapping, and automated updates. As a result, adoption remains concentrated in urban centers and higher-income communities while broader consumer segments remain underpenetrated.

Opportunities - Rapid Urbanization and Expanding Middle-Class Population in the Asia Pacific Creating Strong Demand for Automated Cleaning Solutions

Asia Pacific presents strong growth potential for the robot vacuum cleaner market, driven by rapid urbanization, rising disposable incomes, and an expanding middle-class population. Increasing apartment living in major cities encourages demand for compact and automated cleaning solutions that can efficiently operate within smaller residential spaces and busy lifestyles.

The growth of e-commerce platforms and digital retail channels is also improving consumer access to smart home appliances across the region. At the same time, increasing awareness of home automation technologies and connected devices is encouraging households to adopt robotic cleaning solutions as part of modern, convenience-focused living environments.

Advancing Artificial Intelligence and Connectivity Enabling Expansion into Commercial and Professional Cleaning Applications

Technological advancements in artificial intelligence, connectivity, and robotics are opening opportunities for robot vacuum cleaners beyond residential use. Businesses such as offices, hotels, retail stores, and facility management companies are increasingly exploring automated cleaning solutions to improve operational efficiency and maintain consistent hygiene standards.

Integration of cloud connectivity, remote monitoring, and fleet management software allows multiple cleaning units to be coordinated across large commercial spaces. These capabilities support centralized scheduling and maintenance management, creating opportunities for vendors to provide advanced service models and expand their presence in professional and commercial cleaning environments.

Category-wise Analysis

Product Type Insights

Floor vacuum cleaners represent the leading product category in the robot vacuum cleaner market, accounting for nearly 75% of global revenue in 2025. Their strong market presence is driven by widespread household use and compatibility with a range of surfaces, including hard floors, tiles, and low-pile carpets. Many leading manufacturers focus primarily on floor-cleaning models equipped with features such as automatic docking, HEPA filtration, smart navigation, and mobile app integration.

Pool vacuum cleaners are emerging as the fastest-growing niche segment as residential pool ownership expands in several regions. Increasing interest in automated pool maintenance solutions is encouraging consumers to adopt robotic pool cleaners that reduce manual effort and improve cleaning efficiency. Product innovation focused on enhanced navigation, stronger suction systems, and improved debris collection is expected to support growth within this specialized segment.

Application Insights

The residential segment dominates the robot vacuum cleaner market, accounting for approximately 65% of global demand in 2025. Household adoption is driven by the need for convenient and time-saving cleaning solutions that can manage dust, debris, and pet hair. Busy lifestyles, dual-income households, and growing awareness of smart home technologies continue to support strong demand for robotic cleaning appliances in residential environments.

Commercial and industrial applications are emerging as the fastest-growing segments as organizations seek automated cleaning solutions to improve efficiency. Offices, hotels, retail spaces, and light industrial facilities are increasingly adopting robotic cleaners to maintain hygiene standards and reduce reliance on manual labor. Expanding awareness of automation and the need for frequent cleaning in shared environments are supporting broader adoption in professional settings.

Distribution Channel Insights

Online distribution channels hold the largest share of robot vacuum cleaner sales, accounting for around 55% of global purchases in 2025. The strong growth of e-commerce platforms and the increasing consumer reliance on digital research contribute to this dominance. Buyers often compare product features, read user reviews, and watch demonstration videos before purchasing, making online marketplaces and brand websites key platforms for reaching potential customers.

Offline channels are emerging as the fastest-growing distribution segment as brands expand their physical retail presence. Electronics stores, appliance retailers, and brand showrooms allow consumers to see product demonstrations and better understand device functionality before making a purchase. Retail expansion, experiential shopping, and improved in-store product displays are helping offline channels remain relevant in the evolving retail landscape.

Regional Insights

North America Robot Vacuum Cleaner Market Trends

North America remains one of the most significant markets for robot vacuum cleaners, accounting for approximately 37% of global revenue. High household purchasing power, strong broadband connectivity, and widespread adoption of smart home technologies support strong regional demand. The United States accounts for the majority of sales in the region, driven by larger residential spaces and consumers' willingness to adopt automated home appliances that improve convenience and efficiency in daily cleaning routines.

Technological innovation and product upgrades play a crucial role in shaping regional demand. Consumers in the region show strong interest in advanced features such as self-emptying docks, hybrid vacuum-mop designs, and seamless integration with smart home ecosystems. The presence of leading technology companies, mature retail infrastructure, and high awareness of connected devices further strengthens the market environment for robotic cleaning solutions.

Europe Robot Vacuum Cleaner Market Trends

Europe demonstrates steady demand for robot vacuum cleaners, supported by strong consumer interest in energy-efficient home appliances and increasing adoption of smart home technologies. Countries including Germany, the United Kingdom, France, and Spain represent major markets where consumers favor high-quality products that comply with strict European safety and energy standards. Residential adoption remains the primary driver of regional demand.

The European market is expected to grow at a CAGR of around 21% over the forecast period. Increasing consumer awareness of automated cleaning solutions, along with the expansion of online retail channels, is encouraging adoption across several countries. In addition, growing interest in compact and efficient household appliances suited for apartments and mixed flooring environments is contributing to continued market expansion across the region.

Asia Pacific Robot Vacuum Cleaner Market Trends

Asia Pacific is emerging as the fastest-growing regional market for robot vacuum cleaners and accounts for roughly 33% of global demand. Rapid urbanization, rising disposable incomes, and a growing middle-class population are key factors supporting adoption. Countries such as China, Japan, and South Korea lead regional consumption, supported by strong domestic manufacturing capabilities and widespread consumer interest in smart home technologies.

The region also benefits from expanding e-commerce platforms that make robotic cleaning products more accessible to a wider consumer base. Increasing awareness of home automation and the growing popularity of connected devices are encouraging adoption among urban households. As more consumers in developing economies gain access to digital marketplaces and smart home technologies, the Asia Pacific market is expected to experience strong and sustained growth.

Competitive Landscape

The global robot vacuum cleaner market is moderately consolidated, with competition driven by a combination of large multinational appliance manufacturers and specialized robotics developers. Companies focus heavily on technological innovation, product reliability, and integration with smart home ecosystems to strengthen their market position. Advanced navigation systems, improved suction performance, automated docking, and intelligent mapping capabilities are key areas where manufacturers differentiate their products.

Alongside established players, several emerging and regional brands compete strongly in mid-range and entry-level price segments, particularly through digital retail channels. Companies are also exploring new revenue strategies such as subscription-based accessory replacements, extended service plans, and software-enabled feature upgrades to enhance customer engagement and long-term value creation.

Key Developments:

- In June 2024, iRobot Corporation introduced a flagship robot vacuum and mop equipped with enhanced AI-based object recognition and an upgraded self-emptying dock, designed to improve automated cleaning performance and target premium smart home users.

- In October 2024, Ecovacs Robotics launched a next-generation robot vacuum cleaner featuring upgraded LiDAR navigation and a slimmer form factor, specifically developed to efficiently clean compact apartments and dense urban residential spaces.

- In January 2025, LG Electronics showcased new commercial-focused robotic floor cleaners at international consumer electronics and cleaning technology exhibitions, highlighting growing opportunities for automated cleaning solutions across offices, retail facilities, and hospitality environments.

Companies Covered in Robot Vacuum Cleaner Market

- iRobot Corporation

- ECOVACS Robotics

- Roborock

- Xiaomi

- Samsung Electronics

- LG Electronics

- Dyson Ltd.

- Dreame Technology

- Midea

- SharkNinja Operating LLC

- Eufy (Anker Innovations)

- ILIFE Innovation Ltd.

- NARWAL

- Philips (Koninklijke Philips N.V.)

- Haier Group Corporation

Frequently Asked Questions

The global robot vacuum cleaner market is expected to reach around US$ 12.6 billion in 2026.

Rapid adoption of smart home technologies and connected devices is a major driver of robot vacuum cleaner demand.

North America currently leads with about 37% share of global revenue due to strong U.S. adoption and smart home infrastructure.

Expansion into commercial and light industrial spaces such as offices, hotels, and retail facilities presents significant growth opportunities.

Key players include iRobot Corporation, Ecovacs Robotics, Roborock, Dyson, Samsung Electronics, LG Electronics, SharkNinja, Neato Robotics, and ILIFE.