- Medical Devices

- Respiratory Diagnostics Market

Respiratory Diagnostics Market Size, Share, and Growth Forecast, 2026 – 2033

Respiratory Diagnostics Market by Test Type (Mechanical, OSA, Imaging, Molecular Test), by Disease (Tuberculosis, COPD, Lung Cancer), by Diagnosis Type (Syndromic, Aetiological, Prognosis), and Regional Analysis 2026 – 2033.

Respiratory Diagnostics Market Share and Trends Analysis

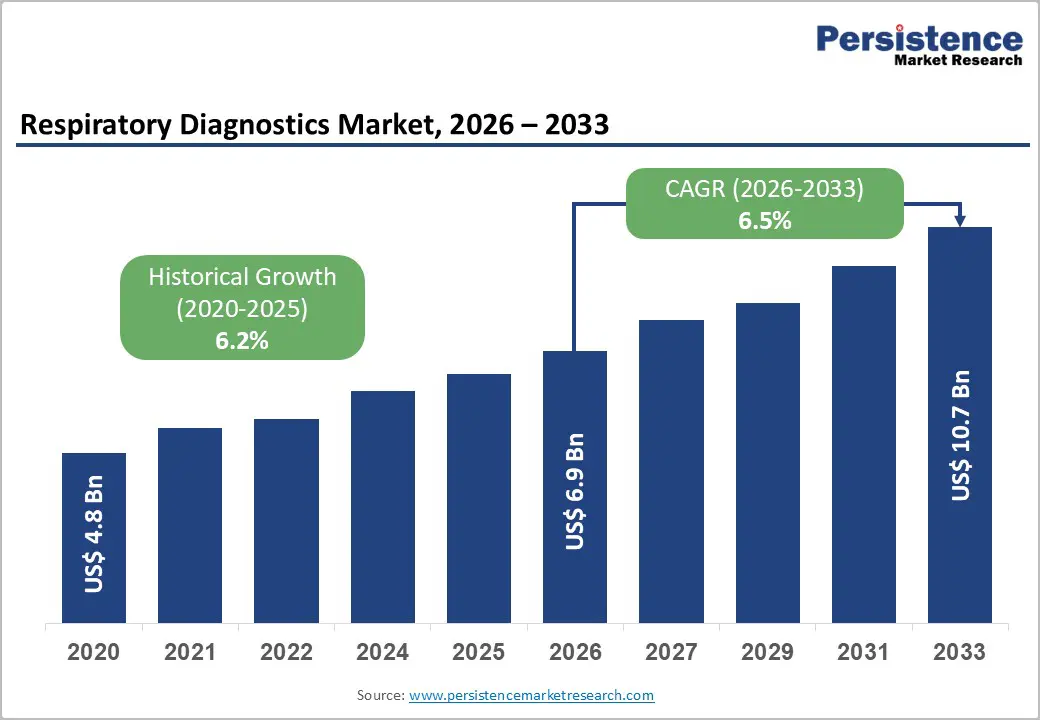

The global respiratory diagnostics market size is likely to be valued at US$ 6.9 billion in 2026 and is projected to reach US$ 10.7 billion by 2033, growing at a CAGR of 6.5% during the forecast period from 2026 to 2033, driven by the rising global prevalence of chronic respiratory diseases (CRDs), such as COPD and asthma, which necessitate frequent and accurate diagnostic interventions.

The respiratory diagnostics market is experiencing sustained expansion driven by escalating disease burden, demographic shifts, and transformative technological innovation. The integration of artificial intelligence (AI) in medical imaging and the shift toward decentralized molecular testing are significantly reducing turnaround times and improving diagnostic accuracy.

Key Industry Highlights:

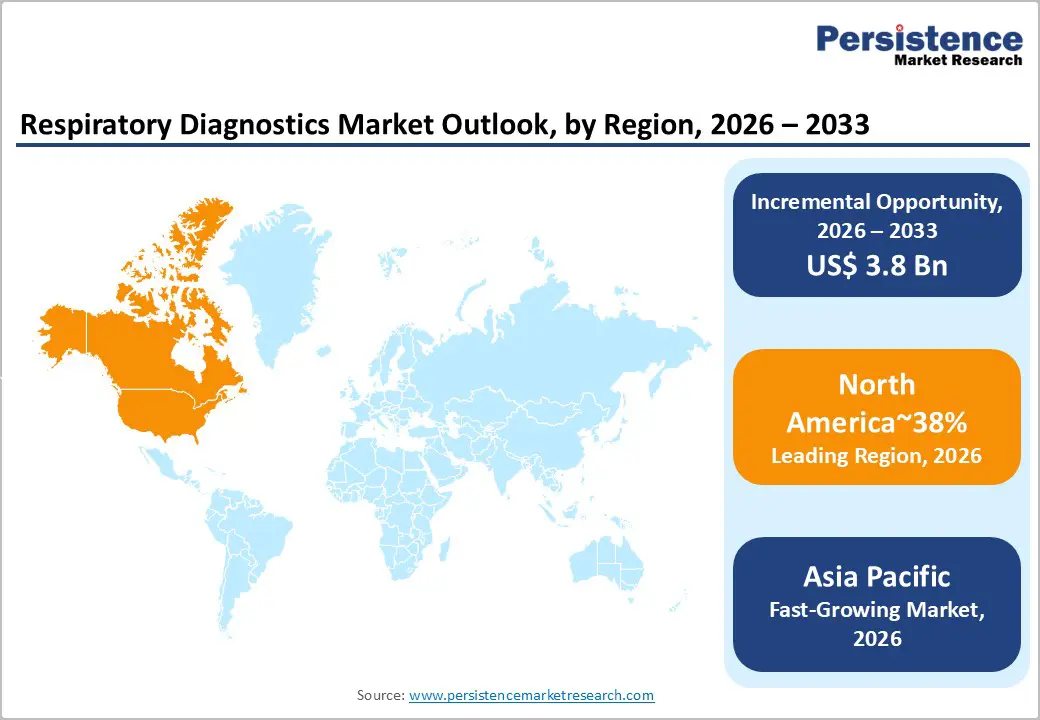

- Leading Region: North America is expected to lead, supported by advanced diagnostic infrastructure accounting for over 38% of the global market share in 2026, high adoption of premium respiratory diagnostics, and strong integration of molecular and digital testing platforms across healthcare systems.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, aging populations, rising respiratory disease burden, and sustained investments in healthcare infrastructure and diagnostic capacity expansion.

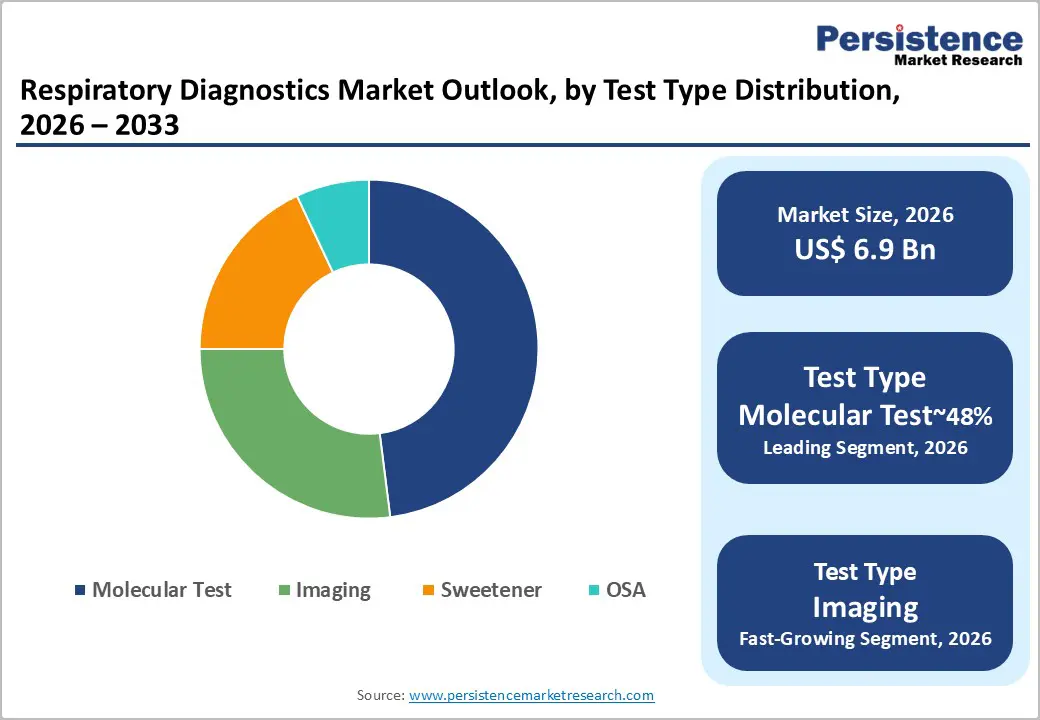

- Leading Test Type: Molecular testing is expected to lead with around 48% share in 2026, reflecting its established role in accurate pathogen detection across hospital laboratories, emergency care, and reference labs.

- Leading Diagnosis Type: Aetiological diagnosis is expected to lead with approximately 51% share in 2026, underpinned by its use in precision-guided therapy and antimicrobial stewardship across hospitals and outpatient clinics.

| Key Insights | Details |

|---|---|

|

Respiratory Diagnostics Market Size (2026E) |

US$6.9 Bn |

|

Market Value Forecast (2033F) |

US$10.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.2% |

Market Dynamics–Growth, Barrier, and Opportunity Analysis

Growth Analysis – Rapid Evolution of Molecular Diagnostics and Point-of-Care Testing

Molecular diagnostics and artificial intelligence integration are structurally elevating respiratory testing sophistication, shifting the market toward data-driven, rapid decision frameworks. AI-enabled platforms are improving diagnostic sensitivity and interpretive accuracy, reinforcing the clinical value of syndromic testing models that enable simultaneous pathogen detection from single samples. The transition of PCR-based multiplex assays, next-generation sequencing, and advanced imaging from research settings into routine clinical workflows is compressing diagnostic timelines and strengthening acute respiratory disease management. These technologies are increasingly embedded within integrated digital diagnostic ecosystems that link instruments, assays, and analytics, enabling automated interpretation, workflow standardization, and scalable deployment across hospital networks.

This technological evolution is displacing traditional culture-based methods in favor of rapid molecular diagnostics, particularly in high-throughput and decentralized care environments. Multiplex PCR and miniaturized point-of-care systems are reducing turnaround times from days to hours, directly impacting length of stay, antimicrobial stewardship, and care efficiency. Regulatory validation of rapid molecular platforms and rising clinical reliance on real-time diagnostic outputs are reinforcing adoption across emergency, primary, and outpatient settings, while capital intensity and system integration complexity continue to shape uneven adoption trajectories across regions.

Barrier Analysis – Professional Workforce Limitations and Regulatory Complexity

Professional workforce constraints and regulatory complexity are emerging as material structural headwinds within advanced respiratory diagnostics. Molecular and imaging platforms require specialized technical expertise across assay handling, data interpretation, and system maintenance, while persistent shortages of trained personnel in emerging and mid-income regions are constraining diagnostic scale-up. These skills gaps limit the effective use of high-throughput molecular systems, reducing returns on capital investment and slowing penetration beyond tertiary care centers, despite rising disease burden and clinical demand for rapid diagnostics.

Regulatory requirements further intensify market friction through stringent clinical validation protocols, post-market surveillance obligations, and extensive quality documentation. Fragmented regulatory frameworks across regions prevent harmonized approvals, increasing time-to-market and forcing manufacturers to maintain parallel compliance strategies. This regulatory asymmetry elevates operating costs, complicates cross-border manufacturing and distribution, and favors scaled players with established compliance infrastructure. As a result, market expansion remains uneven, with adoption velocity closely tied to regulatory maturity, workforce availability, and institutional readiness rather than purely technological capability.

Opportunity Analysis – AI Integration in Imaging and Molecular Diagnostics

AI integration across imaging and molecular diagnostics is expanding the addressable value pool by repositioning respiratory testing platforms as productivity and decision-optimization assets rather than standalone diagnostic tools. Algorithms enabling automated image reconstruction, pathogen identification, and risk stratification are delivering measurable gains in diagnostic accuracy and throughput, supporting premium pricing and platform differentiation. Hospital systems are increasingly prioritizing AI-enabled CT, MRI, and syndromic molecular workflows to compress reporting timelines, standardize interpretation, and mitigate skilled labor constraints. Regulatory clearances, including FDA 510(k) pathways and CE marking, are reducing commercialization friction for validated AI solutions, accelerating procurement cycles, and reinforcing adoption across acute care, emergency, and centralized laboratory environments.

In January 2025, Roche launched Cobas Pulse, an AI-powered POC platform for real-time biomarker analysis. The launch accelerated the adoption of POC molecular diagnostics, improving sensitivity for respiratory pathogens and aligning with the fastest-growing test type and opportunity segments in decentralized testing. This development underscores the strategic convergence of AI capability, point-of-care deployment, and regulatory readiness as a durable growth lever, particularly in systems seeking decentralized diagnostics without sacrificing analytical performance.

Category–wise Analysis

Test Type Insights

Molecular testing is anticipated to dominate the respiratory diagnostics market, accounting for approximately 48% share in 2026, supported by its entrenched role as the clinical gold standard across hospital laboratories, emergency departments, and centralized reference labs. Adoption remains anchored by superior sensitivity and specificity for differentiating viral and bacterial etiologies, with providers prioritizing diagnostic certainty, reimbursement eligibility, and antimicrobial stewardship in high-throughput care pathways.

Ongoing platform evolution, including syndromic panels, AI-assisted result interpretation, cartridge miniaturization, and near-patient molecular workflows, continues to reinforce replacement cycles and utilization intensity. Vendors such as Roche (cobas), bioMérieux (BioFire), Cepheid (GeneXpert), and Abbott (ID NOW) are expanding integrated platforms and menu breadth to lock in laboratory workflows and long-term reagent contracts.

Imaging is projected to be the fastest-growing segment, driven by unmet needs in rapid triage, disease severity stratification, and limitations of symptom-only assessment across emergency care, inpatient wards, and critical care pathways. Growth is being catalyzed by AI-enabled computer-aided detection, portable and ultra-mobile imaging systems, and multimodal integration with laboratory data, which materially improve diagnostic speed, throughput, and care coordination.

Accelerating adoption is supported by embedded AI triage tools, cloud-enabled image workflows, and digital twins that lower operational friction for time-constrained clinical teams. Companies, including GE HealthCare, Siemens Healthineers, Butterfly Network, and Shimadzu, are scaling AI-integrated imaging platforms and bedside modalities to capture early-cycle demand and embed switching costs.

Diagnosis Type Insights

Aetiological diagnosis is expected to remain the dominant diagnosis type within the respiratory diagnostics market, accounting for approximately 51% share in 2026, underpinned by its entrenched role in precision-guided therapy, antimicrobial stewardship, and reimbursement-qualified care pathways across hospitals, emergency departments, and outpatient clinics. Adoption remains anchored by clinical reliability in pathogen confirmation and rapid antimicrobial susceptibility insights, with providers prioritizing treatment accuracy, reduced empiric prescribing, and length-of-stay control in high-acuity settings. Ongoing platform evolution, including ultra-comprehensive one-swab panels, rapid AST workflows, host-response augmentation, and EHR-integrated decision support, continues to reinforce utilization intensity and repeat testing.

Vendors such as bioMérieux (FilmArray), Cepheid (GeneXpert), Roche, T2 Biosystems, and DiaSorin/Luminex are expanding menus and informatics to lock in laboratory workflows and service contracts. This combination of mature infrastructure, data interoperability, and predictable clinical demand sustains leadership in aetiological diagnosis.

Syndromic diagnosis is projected to be the fastest-growing, driven by diagnostic complexity, overlapping symptom profiles, and performance limits of sequential testing across urgent care, ICUs, and near-patient settings. Growth is being catalyzed by closed, sample-to-result multiplex systems, AMR-inclusive ICU panels, and AI-assisted panel selection, materially improving time-to-therapy, negative predictive value, and unit economics. Accelerating adoption is supported by CLIA-waived multiplexing, decentralized deployment in retail clinics, and cloud-linked surveillance workflows that lower operational friction for frontline teams.

Companies including bioMérieux, QIAGEN, Cepheid, Roche, and Hologic/Mobidiag are scaling modular panel portfolios and fast-turnaround platforms to capture early-cycle demand and embed switching costs. As reimbursement alignment, regulatory validation, and workforce familiarity improve, syndromic diagnosis is expected to outpace overall market growth.

Regional Insights

North America Respiratory Diagnostics Market Trends

North America is projected to remain the largest respiratory diagnostics market, accounting for approximately 38% of total revenue in 2026, with the U.S.as the primary contributor due to its advanced innovation ecosystem and concentration of major industry players, including Abbott and Thermo Fisher. The region’s leadership is structurally reinforced by robust healthcare infrastructure, high per-capita medical expenditure, and an integrated system that supports the adoption of molecular, syndromic, and imaging diagnostics.

Hospital and laboratory consolidation further standardizes protocols and enhances throughput, ensuring volume stability and predictable revenue streams across acute and chronic care pathways. The regulatory environment under the FDA, including 510(k) and de novo pathways, enables expedited deployment of validated technologies, while CMS and commercial reimbursement establish clear commercial viability signals, collectively sustaining long-term market leadership.

Growth momentum is supported by the rising chronic respiratory disease prevalence, aging populations, and increasing public health awareness, which drive the adoption of point-of-care molecular platforms and syndromic panels. The rapid transition toward AI-integrated diagnostic systems, alongside the expansion of home-based OSA testing, reinforces structural demand. Government initiatives, such as CDC surveillance programs and NIH-funded research, further accelerate innovation and adoption, positioning North America as both a revenue leader and a strategically advanced region for respiratory diagnostics.

Structural demand is reinforced by hospital and laboratory consolidation, which standardizes diagnostic protocols and enhances throughput, sustaining both volume and revenue stability across acute and chronic care settings.

Europe Respiratory Diagnostics Market Trends

Europe is expected to remain a structurally significant respiratory diagnostics market, supported by mature healthcare infrastructure, high adoption of advanced diagnostic technologies, and strong regulatory harmonization. Germany, the U.K., and France, underpinned by established hospital networks, preventive care programs, and centralized public health initiatives such as tuberculosis screening and integrated COPD management. Germany leads manufacturing and R&D in imaging and mechanical diagnostic tools, while the UK emphasizes NHS-sponsored diagnostic expansion aligned with the needs of an aging population.

Across the region, healthcare systems prioritize cost-effectiveness and evidence-based adoption, reinforcing consistent demand for validated molecular, imaging, and mechanical diagnostic platforms. Pan-European surveillance networks further support standardized diagnostic utilization and strengthen structural market stability.

Market expansion is driven by demographic and environmental factors, including aging populations, historical smoking prevalence, and occupational respiratory disease burdens, particularly in Germany, Italy, and Spain. Urban air pollution contributes to elevated COPD and asthma incidence, sustaining testing volumes. European investment in pulmonary diagnostic innovation, supported by EU research funding mechanisms and harmonized regulatory pathways under IVDR and CE marking, facilitates technology adoption and cross-border market access.

Collectively, Europe’s regulatory clarity, public health initiatives, and infrastructure sophistication position the region as a strategically stable and policy-driven market within the global respiratory diagnostics landscape.

Asia Pacific Respiratory Diagnostics Market Trends

Asia Pacific is the fastest-growing regional market for respiratory diagnostics, driven by large populations, rapid urbanization, and rising respiratory disease prevalence. China and India serve as the primary growth engines, supported by government investments in healthcare infrastructure, modernization of hospital systems, and increasing access to diagnostic services. The region benefits from substantial manufacturing advantages, with ASEAN countries serving as production hubs for global players.

Market expansion is further supported by rising middle-class populations, greater healthcare spending, and increasing patient demand for private diagnostic services, particularly for sleep apnea (OSA) and lung cancer screening. The shift from traditional microscopy to modern molecular diagnostics, including PCR and syndromic platforms, reinforces structural adoption and accelerates deployment across both hospital and point-of-care settings.

Growth is catalyzed by environmental and demographic factors, including urban industrialization, elevated air pollution, and high TB and COPD prevalence, which collectively sustain testing volumes. Government-led initiatives, such as India’s National Health Mission and regional respiratory disease surveillance programs, enhance diagnostic capacity and standardize care pathways. Japan demonstrates advanced adoption driven by aging populations and sophisticated healthcare systems, while cost-sensitive markets in Southeast Asia encourage development of affordable, resource-appropriate diagnostic platforms.

Strategic partnerships between multinational manufacturers and regional distributors facilitate localization and market entry, positioning the Asia Pacific as a high-growth region with strong structural demand, expanding infrastructure, and increasing adoption of modern respiratory diagnostic technologies across public and private healthcare sectors.

Competitive Landscape

The global respiratory diagnostics market is moderately consolidated, with the top five players, Roche, Abbott, Thermo Fisher Scientific, Philips, and ResMed, controlling approximately 55% of total market revenue. Market leadership is underpinned by extensive distribution networks, broad product portfolios, and deep R&D pipelines, while competitive advantage increasingly depends on integrated digital ecosystems that connect diagnostic hardware with advanced data analytics. Premium positioning in developed healthcare systems is reinforced by technology differentiation, including molecular assay innovation and AI-enabled diagnostic platforms, which enhance clinical accuracy and workflow efficiency.

The remaining market is fragmented, comprising specialized regional players that focus on niche applications such as portable spirometry, point-of-care testing, and cost-efficient molecular diagnostics for emerging markets. Strategic competition emphasizes geographic expansion, strategic partnerships, and the adoption of technology-enabled services. Forward-looking dynamics suggest continued convergence toward AI-integrated molecular diagnostics, platform interoperability, and digital monitoring solutions, with moderate consolidation, such as established multinationals leveraging scale and technological differentiation to maintain dominance.

Key Industry Developments:

- In October 2025, Thermo Fisher Scientific acquired Clario Holdings to expand respiratory assessment capabilities. Strengthened the diagnostic ecosystem by integrating advanced respiratory endpoint data and wearable capture technology into clinical research and patient monitoring.

- In June 2024, Roche received FDA emergency use authorization for a rapid 4-in-1 molecular respiratory test. Enables healthcare professionals to provide a definitive diagnosis for four major viruses in just 20 minutes, facilitating immediate clinical decisions in urgent care settings.

- In January 2024, Philips entered into an FDA Consent Decree to establish a compliance roadmap for respiratory device restoration. Provides a transparent regulatory pathway for the company to restore its market position in the U.S. sleep and respiratory care segments while prioritizing patient safety.

Companies Covered in Respiratory Diagnostics Market

- Abbott Laboratories

- Becton Dickinson and Company

- Thermo Fisher Scientific

- GE HealthCare

- Koninklijke Philips N.V.

- Siemens Healthineers

- Roche Diagnostics

- BioMérieux

- Bio-Rad Laboratories

- Danaher Corporation

- Quidel

- PerkinElmer

- Luminex

- ResMed

- NDD Medical Technologies

- Drägerwerk AG

- Cosmed

- Vyaire Medical

- Masimo

- Hologic

Frequently Asked Questions

The global respiratory diagnostics market is projected to be valued at US$6.9 billion in 2026 and is expected to reach US$10.7 billion by 2033, reflecting sustained diagnostic demand worldwide.

Demand is rising due to the increasing prevalence of chronic respiratory diseases such as COPD and asthma, aging populations, and the growing need for accurate, repeatable diagnostic interventions across acute and chronic care settings.

The respiratory diagnostics market is expected to grow at a CAGR of 6.5% between 2026 and 2033, supported by molecular diagnostics expansion and AI-enabled imaging integration.

The fastest growth opportunities are emerging in Asia Pacific, driven by urbanization, rising respiratory disease burden, expanding healthcare infrastructure, and increasing diagnostic capacity investments.

Key players include Abbott Laboratories, Becton Dickinson and Company, Thermo Fisher Scientific, Roche Diagnostics, Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., bioMérieux, Danaher Corporation, Bio-Rad Laboratories, Quidel, and Hologic, among others.