- Processed Food

- Processed Crabstick Market

Processed Crabstick Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

The Processed Crabstick Market is segmented by Form (Frozen, Chilled, Ambient/Retort Packs, Others), by End Use (Food Service, HoReCa, Food Manufacturing, Household Retail), by Sales Channel (Supermarkets / Hypermarkets, Specialty Stores, Convenience Stores, Online Retail, Others), and Regional Analysis, 2026 - 2033

Processed Crabstick Market Share and Trends Analysis

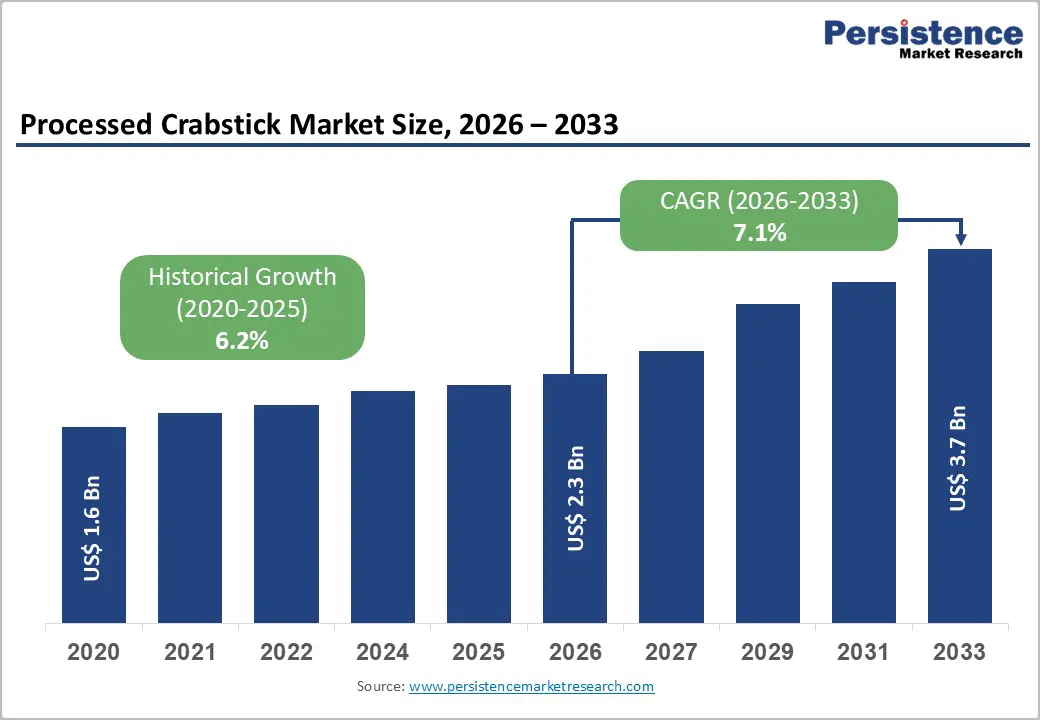

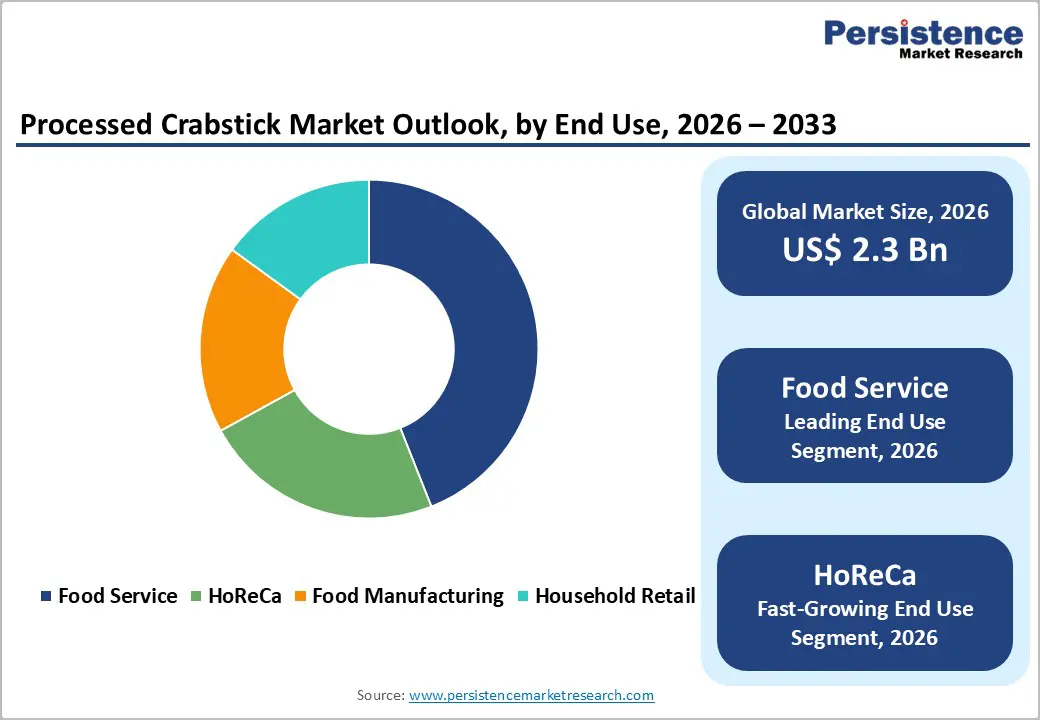

The global processed crabstick market size is expected to be valued at US$ 2.3 billion in 2026 and projected to reach US$ 3.7 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

Market growth is primarily driven by rising demand for affordable, high-protein seafood alternatives and by the rapid expansion of the sushi and ready-to-eat snack sectors globally. As a versatile surimi-based product, crabsticks offer a cost-effective solution for both commercial kitchens and home consumers seeking the organoleptic profile of shellfish without the premium price tag. This transition is further supported by advancements in cryoprotectant technology and vacuum-packaging, which have significantly extended shelf life and improved texture retention, ensuring a robust growth trajectory across diverse culinary landscapes.

Key Industry Highlights:

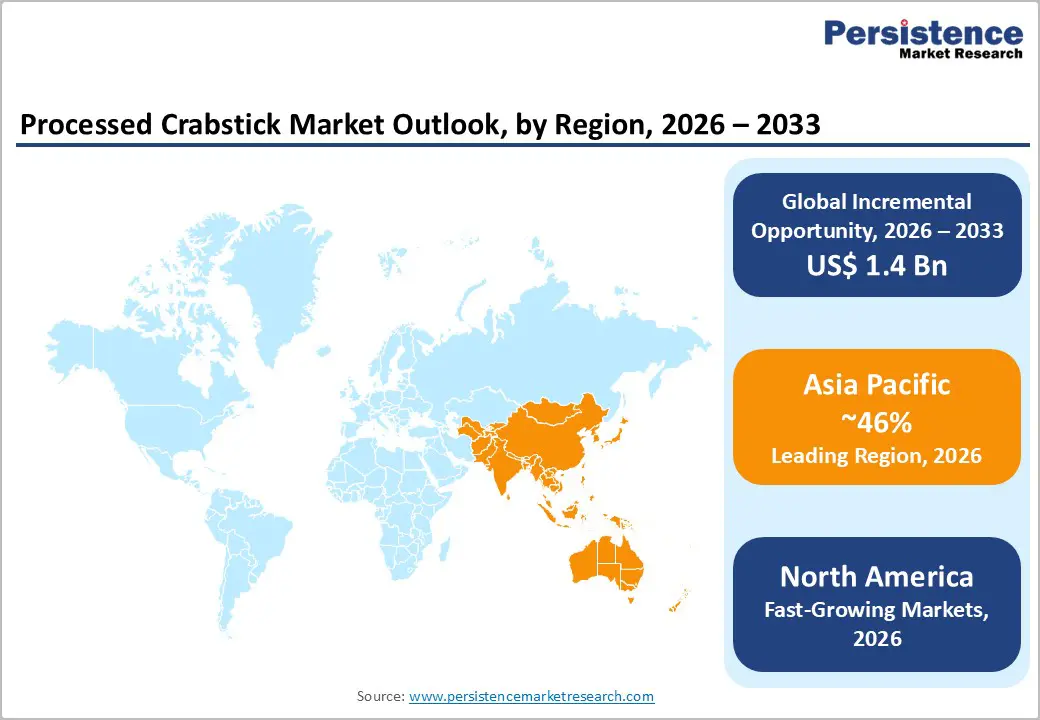

- Leading Region: Asia Pacific, holding 46% market share, supported by deep-rooted surimi consumption traditions, strong seafood processing infrastructure in China, Thailand, and Vietnam, and technological leadership from Japanese producers setting global quality benchmarks.

- Fastest-Growing Region: North America, fueled by abundant Alaska pollock resources, the rising popularity of convenient seafood snacks, and growing consumer interest in high-protein, low-calorie seafood alternatives.

- Leading Form Segment: Frozen crabsticks dominate the market as they enable long-distance shipping, maintain texture integrity during storage, and remain the preferred format for global foodservice and food manufacturing supply chains.

- Growth Indicators: Expanding global popularity of Japanese cuisine and sushi culture continues to boost demand for surimi crabsticks as a standardized, affordable seafood ingredient across both foodservice and retail channels.

- Opportunities: Rising demand for chilled and ambient retort-pack crabsticks opens new avenues in convenience retail and in emerging markets, where ready-to-eat seafood snacks and limited cold-chain infrastructure creates growth potential for ready-to-eat seafood snacks.

- Key Developments: In February 2026, Maruha Nichiro Corporation announced plans to increase U.S. imitation crabmeat production to 16,500 tons by 2026. In August 2025, Blue Star Foods Corp partnered with KeHE Distributors to launch its flagship crab meat pouch nationwide.

| Key Insights | Details |

|---|---|

| Processed Crabstick Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 3.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Dynamics

Driver - Growing Global Popularity of Japanese Cuisine and Sushi Culture

The primary driver for the processed crabstick industry is the mainstreaming of Japanese culinary trends, particularly the proliferation of sushi outlets and grab-and-go seafood rolls. According to the Japan External Trade Organization (JETRO), the number of Japanese restaurants outside Japan has increased significantly over the last decade. Processed crabsticks, or kanikama, are a foundational ingredient in popular fusion dishes like the California roll. This demand is not limited to high-end dining but has penetrated the mass market through franchised sushi kiosks and supermarket deli counters. Brands like Sugiyo Co., Ltd. and Osaki Kamaboko Co., Ltd. have capitalized on this by providing standardized, high-quality surimi sticks that meet the texture requirements of professional sushi chefs, driving consistent volume growth in the Food Service segment.

Restraints - Stringent Labelling Regulations and Consumer Perception Challenges

A significant barrier to market expansion is the increasing regulatory scrutiny regarding the naming and labeling of imitation seafood. In several jurisdictions, including the European Union and the United States, the Food and Drug Administration (FDA) mandates clear labeling to distinguish surimi-based products from genuine shellfish to prevent consumer deception. Furthermore, as the clean label movement gains momentum, some health-conscious consumers remain skeptical of the additives used in processed seafood, such as polyphosphates, sorbitol, and artificial flavorings. These perception challenges can deter a segment of the population that prioritizes minimally processed whole foods. Companies are forced to invest heavily in R&D to develop additive-free or natural-dye alternatives, which can increase production costs and impact final retail pricing.

Opportunity - Expansion of Chilled and Ambient Retort Packs for Convenience

There is a burgeoning opportunity for market participants to diversify their packaging formats beyond traditional frozen blocks. Ambient/Retort Packs and high-pressure processed (HPP) chilled packs are identified as high-growth areas, particularly for the Convenience Stores channel. These formats eliminate the need for lengthy thawing processes, making crabsticks an ideal instant snack for office workers and students. As per a study from Persistence Market Research, the demand for on-the-go functional snacks is at an all-time high. Manufacturers that invest in advanced sterilization techniques that maintain the product's delicate flake structure while allowing for room-temperature storage will be able to penetrate emerging markets in Africa and Latin America where cold-chain infrastructure may be less developed.

Category-wise Analysis

Form Insights

The frozen segment remains the leading segment in form, accounting for the largest volume share. Frozen crabsticks are the industrial standard for global export, providing the stability needed for long-distance maritime shipping. Major processors in China and Vietnam utilize large-scale blast-freezing to supply the Food Manufacturing sector. However, the Chilled segment is identified as a rapidly growing area in developed markets. Chilled crabsticks are often perceived by consumers as fresher and more premium, and have found a strong foothold in the pre-packaged salad and deli sections of Supermarkets/Hypermarkets. Ambient/Retort Packs are also seeing niche growth as shelf-stable snacks for outdoor activities and emergency food supplies.

End-user Insights

The Food Service segment is the leading end-use segment, accounting for a dominant 44% market share in 2025. This leadership is justified by the widespread use of crabsticks in the hospitality and catering industries, where they serve as a consistent, low-labor ingredient for buffets and casual dining. The HoReCa (Hotel, Restaurant, and Cafe) segment is projected to be the fastest-growing through 2032. This growth is driven by the increasing integration of seafood snacks into bar menus and appetizer platters. The Household retail segment is also expanding, as home cooks become more comfortable using crabsticks in domestic recipes such as pasta, sandwiches, and home-made sushi, supported by recipe-driven marketing from brands like Kingsun Foods Co., Ltd.

Regional Insights

Asia Pacific Processed Crabstick Market Trends and Insights

Asia Pacific currently holds a 46% market share in 2025, deeply rooted in surimi's cultural heritage. Japan remains the technological pioneer of the industry, with companies like Nippon Suisan Kaisha (Nissui) and Sugiyo Co., Ltd. setting the global standards for quality and innovation. The region benefits from a massive manufacturing base in China, Thailand, and Vietnam, which serves as the factory for the world's processed seafood.

The innovation ecosystem in this region is focused on high-value variants and functional additives. In South Korea and China, demand for premium crabsticks made with higher whitefish content is a major trend. Furthermore, the expansion of modern retail chains in India and ASEAN countries is introducing processed seafood to a new generation of urban consumers. The sheer scale of the population and the long-standing tradition of fish paste products ensure that Asia Pacific remains the primary engine of global market value and production volume.

North America Processed Crabstick Market Trends and Insights

North America is identified as the fastest-growing region for the processed crabstick market through 2033. The market leadership in the United States is driven by the massive Alaska Pollock fishery, which provides the high-grade surimi paste used globally. Organizations like the Association of Genuine Alaska Pollock Producers (GAPP) have been instrumental in rebranding crabsticks as wild-caught whitefish protein to appeal to the health-conscious American consumer.

The innovation ecosystem in North America is characterized by a strong focus on convenience and snackification. The region has seen a surge in the popularity of surimi seafood packs as a high-protein, low-calorie alternative to traditional meat snacks. Regulatory clarity from the FDA regarding sustainable labeling has also boosted consumer confidence. With the rising trend of home-based sushi making and the expansion of the Online Retail channel, the North American market is poised to see significant value growth as brands focus on premiumization and transparent sourcing.

Competitive Landscape

The processed crabstick market exhibits a consolidated structure at the top tier, dominated by a few global giants with highly integrated supply chains. Key market leaders like Nippon Suisan Kaisha, Ltd. (Nissui) and Sugiyo Co., Ltd. control a significant portion of the raw material supply and processing technology. These companies employ strategies focused on vertical integration, global distribution expansion, and strategic partnerships with major retail chains. However, the market remains fragmented at the regional level, with local players like Gadre Marine Export Pvt. Ltd. in India and Yen & Brothers in Taiwan catering to specific regional taste preferences. Key differentiators in the market include the gel strength of the surimi and the precision of the fiber-aligned texture. Emerging business models are increasingly prioritizing Direct-to-Retail supply chains and sustainability-centric branding to differentiate themselves in a crowded commodity-style market.

Key Developments:

- In February 2026, Maruha Nichiro Corporation announced plans to increase its U.S. production of imitation crabmeat to 16,500 tons in 2026, up around 3,300 tons (25%) from 2019.

- In August 2025, Blue Star Foods Corp. partnered with KeHE Distributors to launch its flagship crab meat pouch nationwide.

Companies Covered in Processed Crabstick Market

- Nippon Suisan Kaisha, Ltd.

- Vikings Group Of Companies

- Sugiyo Co., Ltd.

- A.P. Frozen Foods Co., LTD.

- Gadre Marine Export Pvt. Ltd.

- Yen & Brothers Enterprise Co., Ltd.

- Kingsun Foods Co., Ltd.

- Shandong Ayeshan Group Co., Ltd.

- Osaki Kamaboko Co., Ltd.

- Beijing Shipuller Co., Ltd.

- Others

Frequently Asked Questions

The global Processed Crabstick market is projected to be valued at US$ 2.3 Bn in 2026.

The growing global popularity of Japanese Cuisine and Sushi Culture is a major factor driving the global Processed Crabstick market.

The Global Processed Crabstick market is poised to witness a CAGR of 7.1% between 2026 and 2033.

Expansion of Chilled and Ambient Retort Packs for Convenience is a significant opportunity in the Processed Crabstick market.

Major players in the Global Processed Crabstick market include Nippon Suisan Kaisha, Ltd., Vikings Group of Companies, Sugiyo Co., Ltd., A.P. Frozen Foods Co., LTD., Gadre Marine Export Pvt. Ltd., and others.