- Specialty & Fine Chemicals

- Portland Cement Market

Portland Cement Market Size, Share, and Growth Forecast, 2026 - 2033

Portland Cement Market by Product Type (Ordinary Portland Cement (OPC), OPC Type 1, Others), End-use Industry (Infrastructure, Residential, Others), and Regional Analysis for 2026 - 2033

Portland Cement Market Size and Trends Analysis

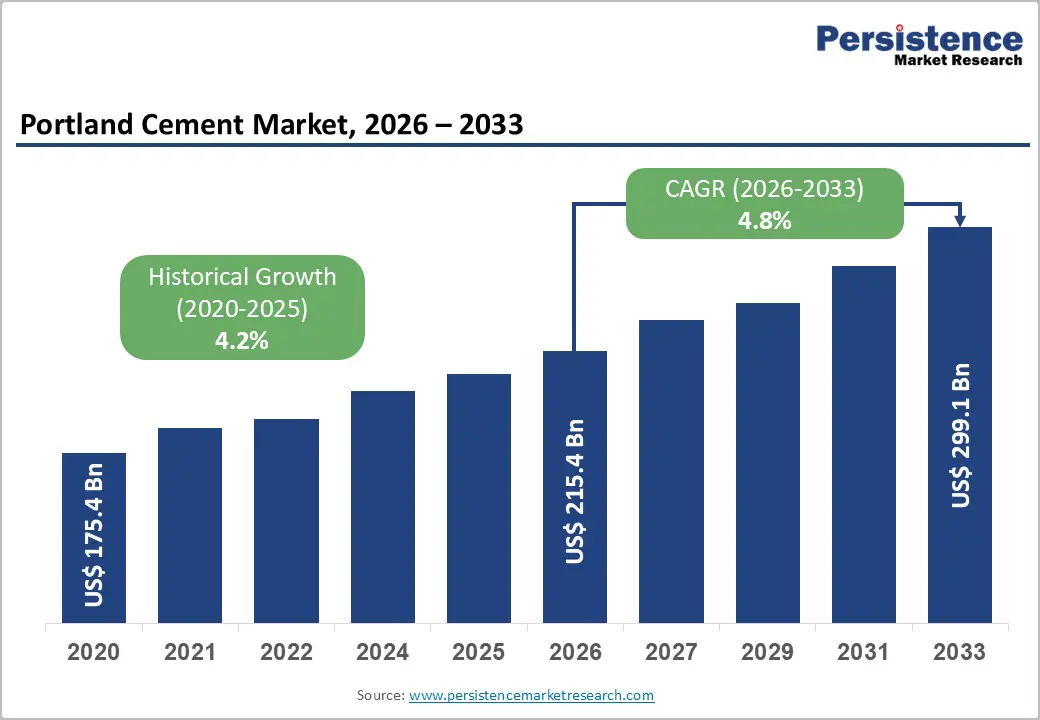

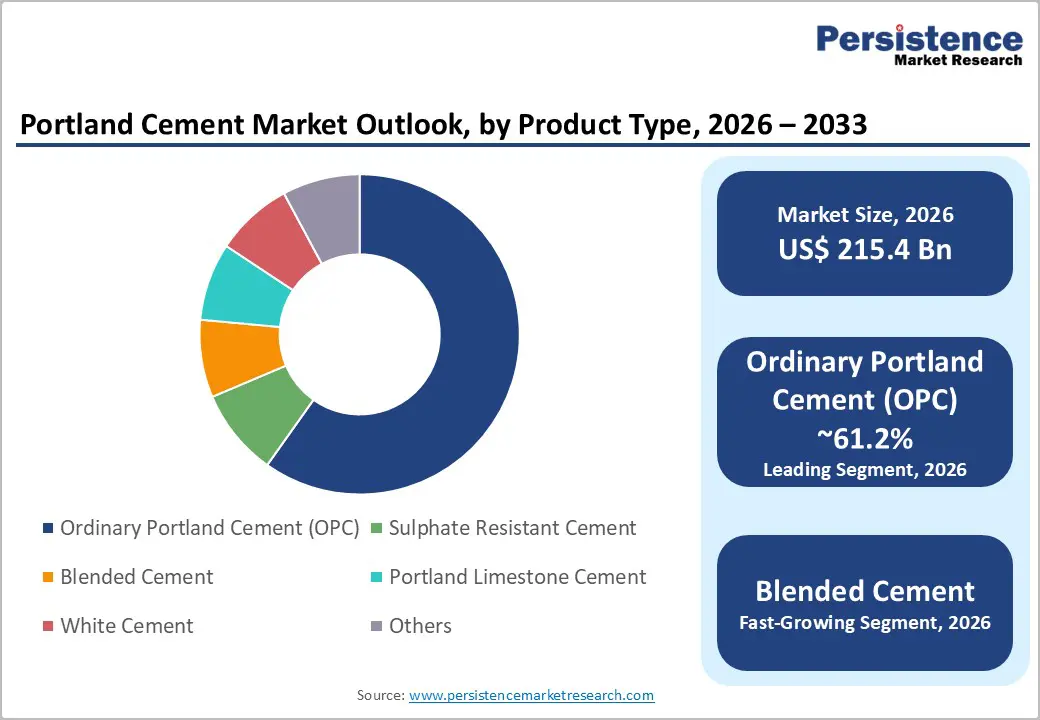

The global portland cement market size is likely to be valued at US$ 215.4 billion in 2026 and is expected to reach US$299.1 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by sustained infrastructure development, population-driven urban construction, and ongoing industrial expansion across emerging economies.

Demand for cement continues to rise in response to transportation projects, housing initiatives, and energy infrastructure development. Producers are also increasingly investing in sustainability initiatives such as blended cement production and alternative fuel technologies to reduce carbon intensity. These factors collectively support stable growth, while evolving environmental standards and construction trends influence long-term market competitiveness.

Key Industry Highlights

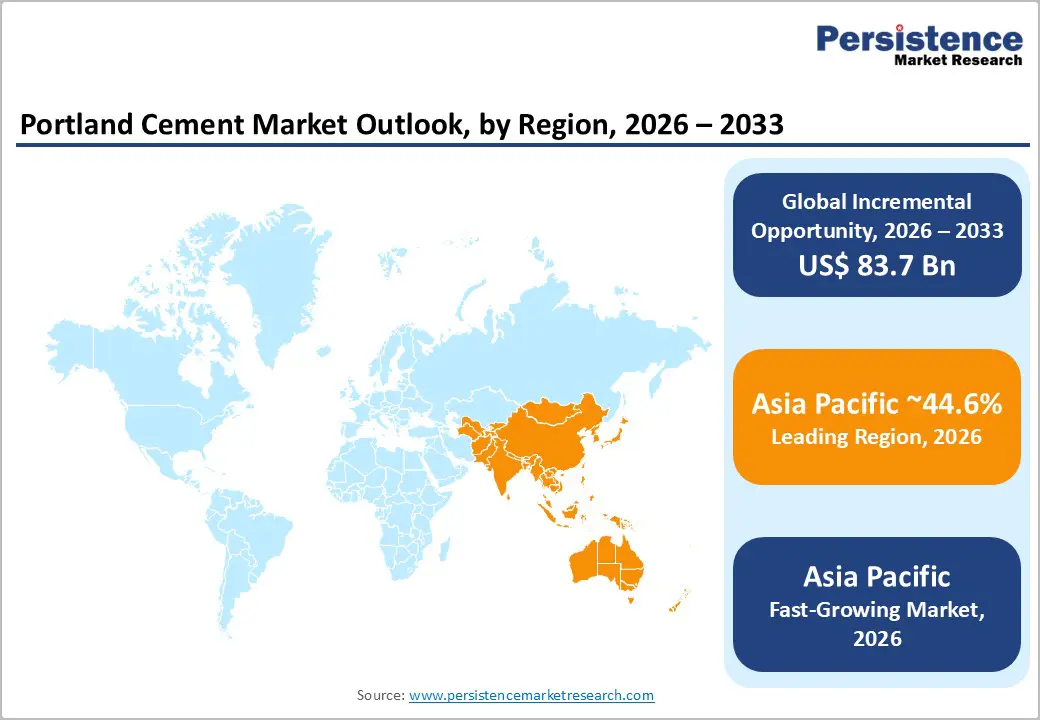

- Leading Region: Asia Pacific is projected to dominate the market, accounting for approximately 44.6% of market share, supported by large-scale infrastructure projects, rapid urbanization, and strong construction activity in China, India, and Southeast Asia.

- Fastest-growing Region: Asia Pacific is also projected to be the fastest-growing regional market, driven by accelerating urban development, government infrastructure programs, and expanding residential construction across emerging economies.

- Investment Plans: Global cement producers are investing heavily in low-carbon cement production, carbon capture technologies, and capacity expansion, particularly in Asia and North America, with sustainability-focused investments expected to influence over 30% of new production upgrades during the forecast period.

- Dominant Product Type: Ordinary Portland Cement (OPC) is anticipated to hold approximately 61.2% of the market share, due to its extensive use in residential, commercial, and infrastructure construction projects.

- Leading End-use Industry: Infrastructure is estimated to account for about 47.3% of market share, driven by large-scale projects such as highways, rail networks, bridges, and urban transportation systems.

| Key Insights | Details |

|---|---|

| Portland Cement Market Size (2026E) | US$215.4 Bn |

| Market Value Forecast (2033F) | US$299.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Infrastructure Expansion in Emerging Economies

Large-scale infrastructure projects across developing regions are a major driver of cement consumption. Governments are investing heavily in highways, rail networks, ports, and energy infrastructure to support economic development and urban expansion. Such projects require extensive volumes of concrete and cement-based materials, ensuring consistent demand from the construction sector. Urban housing programs and industrial development zones further strengthen this demand, particularly in Asia Pacific, Africa, and parts of Latin America. As governments prioritize infrastructure modernization and transportation connectivity, cement producers benefit from long-term supply contracts and stable demand patterns, supporting steady market growth through 2033.

Growing Demand for Sustainable and Low-Carbon Cement

Environmental concerns and stricter emissions regulations are encouraging cement manufacturers to develop lower-carbon products. Cement production is energy-intensive and generates significant carbon emissions during clinker manufacturing. To address this challenge, producers are investing in blended cements, alternative fuels, and energy-efficient kilns. The adoption of supplementary cementitious materials such as slag and fly ash helps reduce clinker usage while maintaining product performance. Construction companies and public infrastructure projects increasingly prioritize sustainable building materials, creating opportunities for producers that offer environmentally responsible cement solutions.

Industry Consolidation and Strategic Expansion

The global cement industry has experienced consolidation as large multinational companies expand their production networks and diversify product portfolios. Strategic acquisitions and partnerships allow companies to strengthen their regional presence and improve supply chain efficiency. By acquiring building-solutions companies and regional cement producers, major industry participants can offer integrated construction materials and services. This strategy improves operational scale, enhances distribution networks, and supports product innovation. Consolidation also helps companies optimize production capacity and maintain pricing stability in competitive regional markets.

Barrier Analysis - High Energy Consumption and Rising Production Costs

Cement manufacturing is highly energy-intensive, requiring large quantities of fuel and electricity during clinker production. Fluctuations in fuel prices, particularly coal and natural gas, directly impact production costs and profitability. Raw materials such as limestone, gypsum, and additives also contribute to operational expenses. Rising energy costs can significantly reduce margins, particularly for smaller manufacturers with limited access to energy-efficient technology. In some regions, prolonged increases in fuel prices may lead to production curtailments or plant shutdowns, limiting supply capacity.

Regulatory and Environmental Compliance Challenges

Environmental regulations governing carbon emissions and industrial pollution are becoming increasingly stringent in many countries. Compliance with these regulations requires substantial investments in emission-control systems, energy-efficient equipment, and alternative fuel technologies. Producers operating in regions with strict environmental policies face higher production costs and additional administrative requirements. Trade regulations and carbon pricing mechanisms may also influence international cement trade flows, creating uncertainty for exporters and producers operating across multiple markets.

Opportunity Analysis - Expansion of Blended Cement and Sustainable Products

Blended cement is emerging as a significant growth opportunity within the Portland cement market. These products combine clinker with supplementary materials such as slag, fly ash, and limestone, reducing carbon emissions during production. Construction companies increasingly prefer blended cement due to its environmental benefits and comparable performance characteristics. Public infrastructure projects and green building certifications are also encouraging the adoption of sustainable construction materials. As a result, manufacturers investing in blended cement technology can expand their product portfolios and improve competitiveness in environmentally regulated markets.

Growth of Integrated Building Solutions

Cement manufacturers are increasingly expanding into broader construction materials and building solutions. By offering prefabricated components, masonry products, and advanced construction materials, companies can capture additional value beyond traditional cement sales. Integrated building solutions improve supply chain coordination and strengthen relationships with construction companies and infrastructure developers. This approach also helps manufacturers reduce revenue volatility by diversifying their product offerings and entering higher-margin construction segments.

Category-wise Analysis

Product Type Analysis

Ordinary Portland Cement (OPC) is anticipated to account for approximately 61.2% of the market share in 2026, maintaining its position as the dominant product type throughout the forecast period. OPC remains widely used in general construction applications, including residential housing, highways, bridges, and commercial structures, due to its strength, reliability, and well-established production processes. Among its variants, OPC Type 1 represents the largest sub-segment, primarily used in general-purpose construction such as buildings, pavements, and precast concrete products. OPC Type 2, which offers moderate sulfate resistance, is commonly used in infrastructure projects where soil and groundwater conditions require improved durability and resistance to chemical exposure.

The widespread availability of OPC, combined with its cost efficiency and compatibility with traditional construction practices, continues to support its leading position in the market. For example, large infrastructure developments such as highway networks, airport runways, and urban housing projects typically rely on OPC-based concrete due to its proven performance and structural strength. Major cement manufacturers continue to expand OPC production capacity to meet consistent demand from large-scale construction projects across Asia Pacific, the Middle East, and Africa. Despite the growing emphasis on sustainable alternatives, OPC is expected to remain the backbone of global cement consumption due to its extensive use across multiple construction sectors.

Blended cement is expected to be the fastest-growing product category during the forecast period, driven by increasing environmental awareness and sustainability requirements within the construction sector. These products incorporate supplementary cementitious materials such as fly ash, granulated blast furnace slag, silica fume, or limestone, which significantly reduce the clinker content and lower carbon emissions during production. As governments and infrastructure developers increasingly adopt environmentally responsible construction practices, the demand for blended cement products is rising steadily.

For instance, blended cement is widely used in large infrastructure and commercial construction projects, where sustainability certifications and carbon reduction targets influence material selection. Many urban infrastructure programs and green building initiatives encourage the use of low-carbon construction materials, which is accelerating the adoption of blended cement across emerging and developed markets. Cement manufacturers are therefore investing in research and development to improve the strength, durability, and curing performance of blended cement formulations. These efforts enable producers to meet sustainability standards while maintaining the structural performance required for modern construction applications.

End-use Industry Insights

The infrastructure sector is anticipated to hold approximately 47.3% of the market share in 2026, making it the largest end-use industry. Infrastructure development requires substantial volumes of cement for concrete production, making it a critical driver of global demand. Major projects such as highways, bridges, rail systems, ports, airports, and power generation facilities rely heavily on cement-based materials to ensure structural stability and long-term durability. Governments around the world are prioritizing infrastructure investments to support economic growth, urban mobility, and industrial expansion.

For example, national highway expansion programs, metro rail developments, and renewable energy infrastructure projects continue to generate strong demand for cement products. Large-scale initiatives such as smart city developments and transportation corridor upgrades also contribute to rising cement consumption. As infrastructure projects typically span several years and require consistent material supply, they provide a stable demand for cement producers and support high capacity utilization across manufacturing facilities.

Commercial construction is projected to be the fastest-growing end-use segment. Rapid urbanization, expanding business districts, and increasing investments in commercial real estate are major factors driving growth in this segment. Demand for office complexes, shopping centers, hotels, healthcare facilities, and logistics hubs is rising across major urban centers worldwide. The rapid expansion of e-commerce and global supply chains has also accelerated the construction of warehouses and distribution centers, further increasing demand for cement-based construction materials. For instance, large logistics parks, data centers, and mixed-use commercial developments require high-performance concrete solutions capable of supporting heavy structural loads and long service life.

Developers are increasingly adopting advanced construction techniques, including precast concrete systems and high-strength cement mixtures, to improve building efficiency and durability. These trends create opportunities for cement manufacturers to supply specialized cement products tailored to commercial construction requirements while supporting the segment’s strong growth trajectory.

Regional Insights

North America Portland Cement Market Trends - Infrastructure Investment and Low-Carbon Cement Innovation

North America represents a mature cement market characterized by stable demand and moderate growth. The U.S. accounts for the largest share of regional cement consumption, supported by infrastructure modernization, residential renovation, and industrial construction activity. Government initiatives such as the U.S. Infrastructure Investment and Jobs Act (IIJA) have allocated hundreds of billions of dollars for transportation networks, bridges, water systems, and public infrastructure upgrades. These investments are expected to sustain long-term demand for Portland cement. Major producers, including Holcim, CEMEX, and Heidelberg Materials, have expanded production and distribution networks across the U.S. to support these projects. For example, Holcim continues to expand its ECOPact low-carbon concrete solutions across North America, supporting contractors seeking sustainable building materials for large infrastructure projects.

Canada also contributes to regional growth through construction activity linked to natural resource development, transportation infrastructure, and urban expansion. Cement demand in Canada is influenced by large-scale projects such as public transit expansions in cities like Toronto and Vancouver, as well as investments in energy infrastructure and residential housing. Companies such as Lafarge Canada (a Holcim company) and Heidelberg Materials North America continue to invest in plant upgrades and logistics networks to improve supply reliability across the country.

For instance, Lafarge Canada has implemented low-carbon cement products and circular construction solutions, aligning with the country’s emissions reduction targets. Environmental regulations across North America are becoming increasingly stringent, encouraging producers to invest in energy-efficient technologies and lower-carbon cement formulations. For example, Heidelberg Materials is developing a carbon capture and storage (CCS) project at its Edmonton cement plant in Canada, designed to significantly reduce CO2 emissions from cement production. Similarly, companies such as CEMEX are introducing lower-clinker cement formulations and expanding the use of alternative fuels at production facilities. These sustainability initiatives are expected to reshape the competitive landscape in the region while helping cement manufacturers comply with environmental regulations and corporate decarbonization commitments.

Europe Portland Cement Market Trends - Carbon Regulations and Sustainable Cement Manufacturing

Europe’s Portland cement market is shaped by strict environmental regulations, advanced manufacturing practices, and a relatively mature construction sector. Countries such as Germany, the U.K., France, and Spain play significant roles in regional cement consumption, supported by infrastructure maintenance, urban redevelopment, and renovation of aging buildings. The European Green Deal and carbon pricing mechanisms under the EU Emissions Trading System (EU ETS) are encouraging cement manufacturers to reduce emissions and adopt cleaner production technologies.

Germany remains one of the most technologically advanced cement markets in Europe, with strong emphasis on sustainable construction practices and industrial efficiency. Companies such as Heidelberg Materials and Dyckerhoff (part of Buzzi Unicem) continue to invest in low-carbon cement production technologies and alternative fuel usage in German cement plants. In the U.K., CEMEX and Holcim subsidiaries are supplying cement and concrete for major infrastructure developments, including rail modernization projects and urban transport expansions. France has also seen investments in sustainable cement technologies, with Lafarge France launching several low-carbon cement products designed to reduce clinker content and improve environmental performance.

Spain has experienced a gradual recovery in construction activity following earlier market slowdowns. Infrastructure upgrades, tourism-related construction projects, and residential development are supporting cement consumption. Companies such as Cementos Molins and Cemex Spain have expanded production capabilities and introduced environmentally friendly cement solutions to meet EU sustainability requirements. Across the region, cement manufacturers are investing in carbon capture technologies, alternative fuels, and blended cement formulations to comply with regulatory standards and reduce environmental impact. These technological investments are expected to influence the long-term evolution of the European cement industry while supporting the transition toward low-carbon construction materials.

Asia Pacific Portland Cement Market Trends - Rapid Urbanization and Large-Scale Infrastructure Demand

Asia Pacific is projected to dominate the market, accounting for approximately 44.6% of market share in 2026, and is also the fastest-growing region. Rapid urbanization, population growth, and large-scale infrastructure development continue to drive strong cement demand across the region. Governments are investing heavily in transportation networks, urban housing, industrial zones, and energy infrastructure, which significantly increases cement consumption. China remains the world’s largest cement producer and consumer, supported by extensive infrastructure projects and urban development programs. Large Chinese cement manufacturers such as Anhui Conch Cement and China National Building Material (CNBM) operate massive production capacities and play a major role in both domestic supply and international exports. The Chinese government’s infrastructure initiatives and urban redevelopment projects continue to support cement demand, although the market is also experiencing consolidation and production efficiency improvements as environmental regulations tighten.

India represents one of the fastest-growing cement markets, driven by expanding housing demand, rapid urbanization, and large government infrastructure programs. Major producers such as UltraTech Cement, ACC Limited, and Shree Cement are expanding production capacity and logistics networks to meet rising demand. For example, UltraTech Cement has announced several capacity expansion projects across India, increasing its production footprint to support the country’s infrastructure development and residential construction growth. Government initiatives such as highway expansion, metro rail projects, and affordable housing programs are expected to further boost cement consumption.

Japan’s cement market is relatively mature but continues to focus on high-performance cement products used in infrastructure maintenance and earthquake-resistant construction. Companies such as Taiheiyo Cement and Sumitomo Osaka Cement invest in advanced cement technologies to support infrastructure durability and resilience. Meanwhile, Southeast Asian countries, including Vietnam, Indonesia, and Thailand, are experiencing strong growth due to expanding urban populations, industrialization, and export-oriented manufacturing sectors.

Cement producers such as Siam Cement Group (SCG) and VICEM are expanding regional production and distribution capabilities to meet rising demand. The availability of raw materials, large domestic markets, and cost-efficient manufacturing capabilities support the region’s dominance in global cement production. As sustainability policies expand across Asia Pacific, producers are increasingly investing in energy-efficient kilns, blended cement products, and lower-carbon production technologies, ensuring the region remains the primary driver of growth in the global Portland cement market.

Competitive Landscape

The global Portland cement market is moderately consolidated at the international level but remains fragmented within many regional markets. Large multinational cement producers dominate global production capacity and distribution networks, while smaller regional manufacturers serve local construction markets. Major companies maintain competitive advantages through integrated supply chains, extensive production facilities, and established distribution systems.

Leading companies focus on sustainability initiatives, operational efficiency, and product diversification. Investments in blended cement technologies, alternative fuels, and energy-efficient manufacturing processes are key priorities. Many companies are also expanding into construction materials and building solutions to improve profitability and strengthen their competitive position.

Key Industry Developments:

- In March 2025, Holcim announced the “NextGen Growth 2030” strategy, focusing on expanding sustainable building materials and scaling up low-carbon cement products such as ECOPlanet, which already accounted for over one-third of Holcim’s cement sales in 2025.

Companies Covered in Portland Cement Market

- Holcim Group

- Heidelberg Materials AG

- CEMEX S.A.B. de C.V.

- China National Building Material Company Limited (CNBM)

- Anhui Conch Cement Company Limited

- UltraTech Cement Limited

- CRH plc

- Buzzi Unicem S.p.A.

- Votorantim Cimentos S.A.

- Taiwan Cement Corporation

- Siam Cement Group (SCG Cement)

- Shree Cement Limited

- Taiheiyo Cement Corporation

- Sumitomo Osaka Cement Co., Ltd.

- Cementos Molins S.A.

- Dangote Cement Plc.

Frequently Asked Questions

The global Portland cement market size is estimated to reach US$215.4 billion in 2026.

The Portland cement market is projected to reach US$299.1 billion by 2033.

Key trends include growing adoption of blended cement for lower carbon emissions, investments in carbon capture and sustainable cement technologies, increasing infrastructure spending, and expansion of cement production capacity in Asia Pacific and emerging markets.

Ordinary Portland Cement (OPC) is the leading product segment, accounting for approximately 61.2% of the global market share, due to its extensive use in residential buildings, roads, bridges, and general construction applications.

The Portland cement market is expected to grow at a CAGR of 4.8% between 2026 and 2033.

Some of the major companies include Holcim Group, Heidelberg Materials AG, CEMEX S.A.B. de C.V., China National Building Material Company (CNBM), and UltraTech Cement Ltd.