- Executive Summary

- Global Plastic Liner Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Other Macro-economic Factors

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Plastic Liner Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Plastic Liner Market Outlook: Material Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Material Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Material Type, 2026-2033

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Others (PLA, etc.)

- Market Attractiveness Analysis: Material Type

- Global Plastic Liner Market Outlook: End-use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by End-use Industry, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food and Beverages

- Fertilizers & Agri Products

- Pharmaceutical

- Industrial Chemicals

- Others

- Market Attractiveness Analysis: End-use Industry

- Global Plastic Liner Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Plastic Liner Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Material Type, 2026-2033

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Others (PLA, etc.)

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food and Beverages

- Fertilizers & Agri Products

- Pharmaceutical

- Industrial Chemicals

- Others

- Europe Plastic Liner Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Material Type, 2026-2033

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Others (PLA, etc.)

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food and Beverages

- Fertilizers & Agri Products

- Pharmaceutical

- Industrial Chemicals

- Others

- East Asia Plastic Liner Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Material Type, 2026-2033

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Others (PLA, etc.)

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food and Beverages

- Fertilizers & Agri Products

- Pharmaceutical

- Industrial Chemicals

- Others

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by , 2026-2033

- South Asia & Oceania Plastic Liner Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Material Type, 2026-2033

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Others (PLA, etc.)

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food and Beverages

- Fertilizers & Agri Products

- Pharmaceutical

- Industrial Chemicals

- Others

- Latin America Plastic Liner Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Material Type, 2026-2033

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Others (PLA, etc.)

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food and Beverages

- Fertilizers & Agri Products

- Pharmaceutical

- Industrial Chemicals

- Others

- Middle East & Africa Plastic Liner Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Material Type, 2026-2033

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Others (PLA, etc.)

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food and Beverages

- Fertilizers & Agri Products

- Pharmaceutical

- Industrial Chemicals

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- RRR Supply, Inc.

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- A-Pac Manufacturing Co., Inc

- Plascon Group International Plastics Inc.

- American Plastics Company

- Shagoon Packaging Pvt. Ltd

- Synpack Avonflex Pvt. Ltd.

- Caltex Plastics Inc.

- Polymer-Synthese-Werk GmbH

- Chiltern Plastics

- NITTEL GmbH

- Bulk Lift International, LLC

- BULK-FLOW (Europe) Ltd.

- Greif, Inc.

- LC Packaging International B.V.

- Junkosha

- Polyzent Trading

- Zeus

- RRR Supply, Inc.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Non-food Packaging

- Plastic Liner Market

Plastic Liner Market Size, Share, and Growth Forecast 2026 - 2033

Plastic Liner Market by Material Type (Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polystyrene (PS), Others), Industry (Food and Beverages, Fertilizers & Agri Products, Pharmaceutical, Industrial Chemicals, Others), by Regional Analysis, 2026 - 2033

Plastic Liner Market Size and Trend Analysis

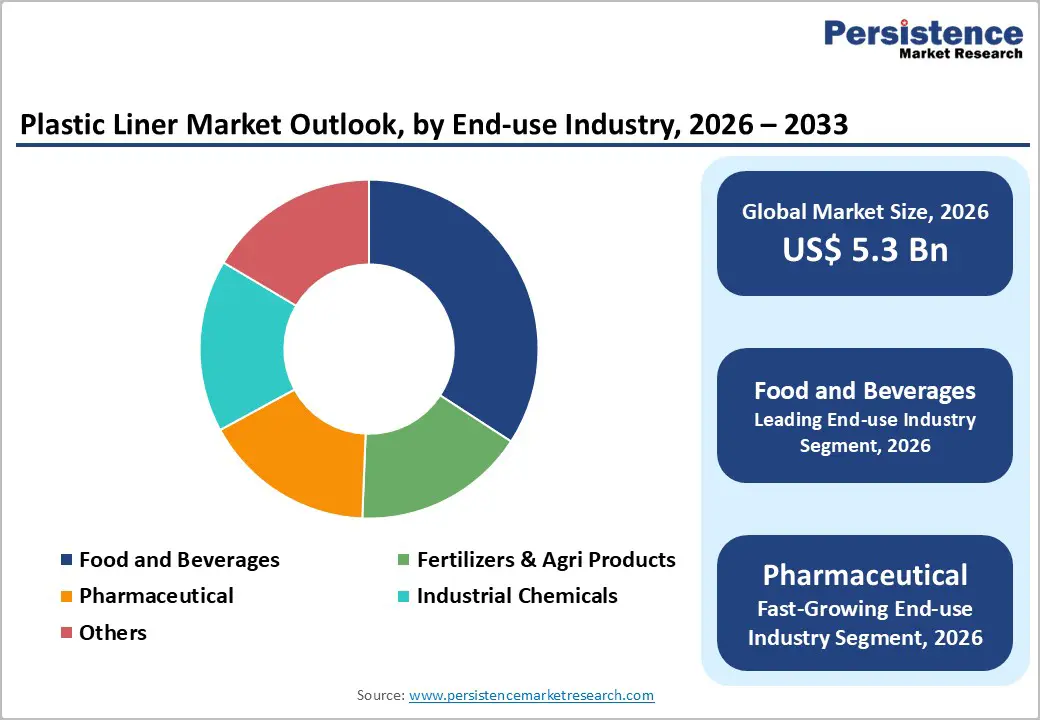

The global plastic liner market size is expected to be valued at US$ 5.3 billion in 2026 and projected to reach US$ 7.4 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033.

The plastic liner market is on a steady and structurally supported growth path, driven by expanding global trade in bulk commodities, rising hygiene and contamination prevention standards across food, pharmaceutical, and agrochemical logistics, and the growing adoption of flexible intermediate bulk container (FIBC) systems in industrial supply chains. As global food production volumes continue to rise to meet the demands of a population projected by the United Nations to reach 9.7 billion by 2050, the requirement for reliable, moisture-resistant, and contamination-proof inner liners for sacks, drums, boxes, and bulk containers is intensifying. Simultaneously, tightening regulatory frameworks on pharmaceutical packaging and chemical containment across the European Union, the United States, and India are elevating quality and traceability standards that favor the use of certified plastic liner solutions over unprotected or substandard alternatives.

Key Industry Highlights:

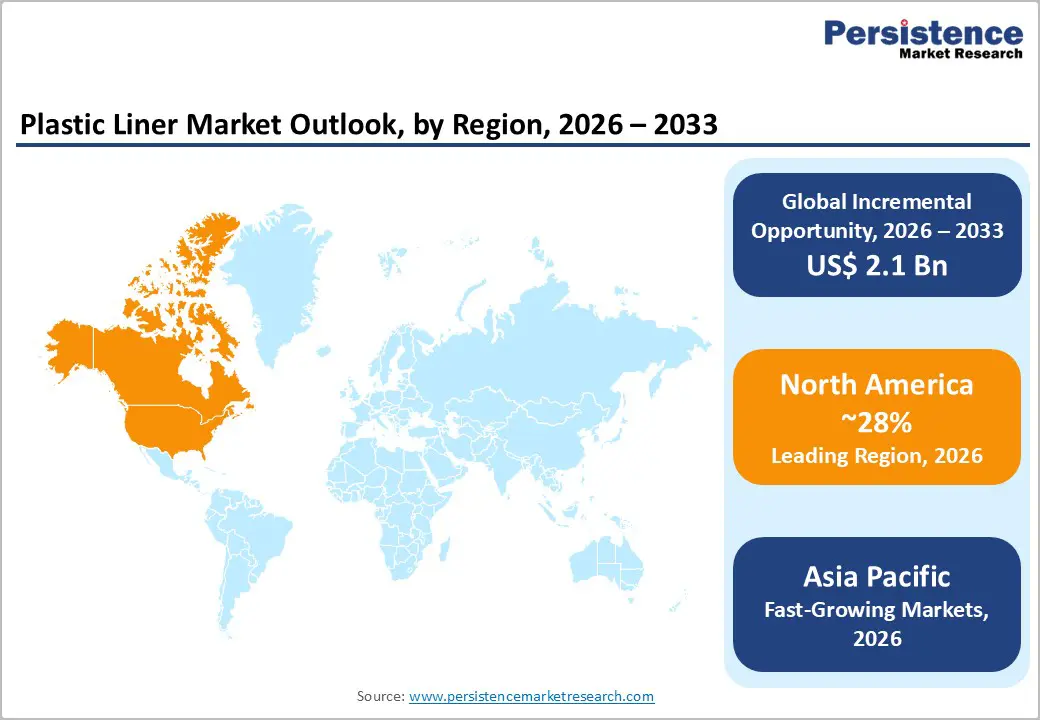

- Leading Region: North America leads the global Plastic Liner market with approximately ~28% revenue share in 2025, driven by the U.S.’s large-scale agricultural export logistics, FDA-regulated pharmaceutical liner procurement, and established domestic manufacturers including RRR Supply, Inc., A-Pac Manufacturing Co., Inc., and Caltex Plastics Inc.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market over 2026 - 2033, propelled by China’s enormous agricultural and chemical bulk packaging demand, India’s rapidly expanding pharmaceutical and food-grain packaging sector exceeding 330 million tonnes of annual food grain output, and ASEAN’s growing industrial and food processing base.

- Dominant Material: Polyethylene (PE) dominates the Material Type segment with approximately ~54% market share in 2025, owing to its unmatched combination of moisture barrier performance, chemical inertness, heat-sealability, and raw material cost competitiveness, making it the universal choice across food-grade, agrochemical, and industrial liner applications.

- Fastest Growing Industry: Pharmaceutical-grade plastic liners represent the fastest growing application segment over 2026 - 2033, as global biologics and API manufacturing expansion, GMP compliance mandates under FDA 21 CFR Part 211, and post-pandemic pharmaceutical supply chain reshoring drive rising demand for premium single-use, validated liner systems.

- Key Opportunity: Sustainable recyclable liner development is the key market opportunity, as the EU Packaging and Packaging Waste Regulation (PPWR) mandates recyclability and recycled content thresholds for all packaging, compelling liner manufacturers to innovate recyclable mono-material PE and PCR-content liner structures that meet both regulatory compliance and corporate ESG commitments.

| Key Insights | Details |

|---|---|

| Plastic Liner Market Size (2026E) | US$ 5.3 Billion |

| Market Value Forecast (2033F) | US$ 7.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 4.8% |

| Historical Market Growth (2020 - 2025) | 4.4% |

Market Dynamics

Drivers - Rising Global Bulk Commodity Trade and FIBC Liner Adoption

The sustained expansion of global bulk commodity trade, encompassing agricultural grains, fertilizers, polymers, minerals, and food ingredients, is a primary structural growth driver for the plastic liner market. Plastic liners, used as inner protective barriers within woven polypropylene bags, FIBC (Flexible Intermediate Bulk Containers), drums, corrugated boxes, and silos, are indispensable for preserving product integrity during transport and storage by providing moisture, oxygen, and contamination barriers. The World Trade Organization (WTO) reported that global merchandise trade volume grew by approximately 2.7% in 2023, with agricultural and chemical commodities representing major share of containerized and bulk shipment volumes. The Flexible Intermediate Bulk Container Association (FIBCA) has noted consistent year-on-year growth in global FIBC production, each unit typically requiring one or more fitted plastic liner to meet food-grade, chemical-grade, or pharmaceutical-grade containment standards, generating sustained incremental liner demand across the global packaging supply chain.

Stringent Food Safety and Pharmaceutical Packaging Regulations Driving Certified Liner Adoption

Regulatory intensification in food safety and pharmaceutical packaging is compelling end users across multiple industries to upgrade from unprotected bulk packaging to certified, compliant plastic liner solutions, directly driving market volume and unit value growth. The U.S. Food and Drug Administration (FDA) enforces comprehensive requirements on food contact materials under 21 CFR Parts 170-199, mandating that plastic liners used in direct food contact applications be manufactured from approved resins and free from prohibited additives. Similarly, the European Food Safety Authority (EFSA) administers Regulation (EC) No. 1935/2004 governing materials and articles intended for food contact, with detailed positive lists for polyethylene and polypropylene food-contact applications. In the pharmaceutical sector, Good Manufacturing Practice (GMP) guidelines enforced under 21 CFR Part 211 in the U.S. and EU GMP Annex 1 require validated, traceable, and often single-use liner systems for drug substance and excipient containment, creating a high-compliance, premium-priced liner demand segment with consistent growth dynamics.

Restraints - Growing Regulatory and Consumer Pressure Against Single-Use Plastics

One of the most significant headwinds facing the plastic liner market is the intensifying global regulatory and consumer sentiment campaign against single-use plastic packaging. The European Union’s Single-Use Plastics Directive (EU) 2019/904 has banned or restricted a range of single-use plastic items, and while industrial liners are not directly targeted, the broader regulatory trajectory is increasing compliance costs for liner manufacturers and creating reputational pressure on end-user companies to demonstrate plastic reduction commitments. Several major multinational food and consumer goods companies have set public pledges to reduce virgin plastic use by 25-50% by 2025-2030, incentivizing the evaluation of alternative liner materials, including paper-based and compostable solutions, that could substitute plastic liners in some applications. This substitution risk, though currently limited, is a structural constraint on premium segment growth.

Raw Material Price Volatility Impacting Manufacturer Margins

Polyethylene (PE) and polypropylene (PP), the dominant raw materials for plastic liner production, are petrochemical derivatives whose pricing is directly correlated with crude oil and natural gas feedstock markets, both of which are subject to significant and sometimes unpredictable price swings. The U.S. Energy Information Administration (EIA) has documented crude oil price fluctuations exceeding 40% within single annual cycles in recent years, creating substantial cost uncertainty for liner manufacturers operating on thin margins. In competitive tender-based procurement environments, particularly in the fertilizer, grain, and industrial chemical segments where buyers are highly price-sensitive, liner producers face difficulty passing raw material cost increases through to customers, compressing profitability during periods of petrochemical price inflation and moderating investment in capacity expansion and product innovation.

Opportunity - Expansion into Pharmaceutical and High-Purity Chemical Liner Applications

The pharmaceutical and high-purity industrial chemicals segments represent high-value and structurally growing opportunity spaces for plastic liner manufacturers capable of meeting demanding regulatory and performance specifications. Pharmaceutical bulk drug substance logistics, covering active pharmaceutical ingredients (APIs), excipients, and granulated intermediates, requires ultra-clean, single-use, gamma-irradiation-compatible liner systems manufactured under ISO 9001 and GMP-certified production environments. The global pharmaceutical industry is undergoing a significant capacity expansion phase: the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA) notes that global pharmaceutical manufacturing output is growing at approximately 5-7% annually, driven by increased biologics production, generic drug manufacturing growth in India and China, and post-pandemic API supply chain reshoring initiatives. Liner suppliers who invest in cleanroom manufacturing infrastructure, FDA-compliant resin traceability systems, and validated single-use pharmaceutical liner product lines are well-positioned to capture premium unit-price revenue streams in this resilient and regulation-protected market segment.

Sustainable and Recyclable Liner Innovation to Meet Circular Economy Mandates

The accelerating transition toward circular economy packaging models presents a transformative product innovation opportunity for plastic liner manufacturers. As the EU Packaging and Packaging Waste Regulation (PPWR), which entered into force in 2024 and mandates minimum recycled content levels and recyclability requirements for all packaging placed on the European market, comes into full implementation, liner manufacturers will be required to demonstrate recycled content integration and recyclability of their products. Manufacturers that proactively develop liners incorporating post-consumer recycled (PCR) polyethylene, monolayer recyclable structures, or certified compostable biopolymers such as PLA (polylactic acid) stand to benefit from both regulatory compliance advantages and growing end-user demand for sustainable packaging. Companies, including Plascon Group and Polymer-Synthese-Werk GmbH are already exploring recyclable liner architectures. The convergence of regulatory mandates, retailer sustainability scorecards, and corporate ESG commitments creates a durable commercial case for sustainable liner innovation investment through 2033.

Category-wise Analysis

Material Type Insights

Polyethylene (PE) Leads the Material Type Segment with ~54% Market Share in 2025

Polyethylene (PE) is the dominant material in the plastic liner market, commanding approximately ~54% of total global revenue in 2025. PE’s market leadership is firmly rooted in its exceptional combination of moisture barrier performance, chemical inertness, flexibility across a wide temperature range, heat-sealability, and low cost of production, properties that make it the material of choice for the broadest range of liner applications spanning food-grade sack liners, FIBC inner bags, drum liners, and pallet cover liners. Both Low-Density Polyethylene (LDPE) and Linear Low-Density Polyethylene (LLDPE) are extensively used in liner manufacturing, with LLDPE increasingly preferred for its superior puncture resistance and tear strength at equivalent or lower gauge. The American Chemistry Council (ACC) reports that polyethylene remains the highest-volume plastic resin produced globally, ensuring raw material availability and competitive pricing that reinforces PE liner’s commercial dominance across all geographic markets.

Industry Insights

The food and beverages end-use segment holds the leading position in the plastic liner market, representing approximately ~36% of total global market revenue in 2025. Plastic liners are a mission-critical component of bulk food packaging systems, used as protective inner barriers in multi-wall paper sacks, woven PP bags, corrugated cartons, and FIBC tote bags for commodities including grains, flour, sugar, coffee, cocoa, dairy powder, spices, and frozen food ingredients. Food safety compliance requirements mandate that food-contact liners meet strict regulatory standards across major markets, including FDA 21 CFR in the United States and EU Regulation (EC) No. 1935/2004, driving procurement toward certified, traceable liner suppliers. The FAO estimates that global food production must increase by approximately 50% by 2050 to meet rising population demand, ensuring that food bulk packaging, and its essential plastic liner component, remains a large, growing, and non-discretionary demand category.

Regional Insights

North America Plastic Liner Market Trends and Insights

North America is the leading regional market for plastic liners, accounting for an estimated ~28% of global revenue share in 2025, underpinned by the United States’ large and technologically sophisticated bulk packaging supply chain serving agricultural, chemical, pharmaceutical, and food processing industries. The U.S. is one of the world’s largest producers and exporters of bulk agricultural commodities. The U.S. Department of Agriculture (USDA) reported total U.S. agricultural exports of approximately US$ 196 billion in fiscal year 2023, generating sustained high-volume demand for grain, fertilizer, and food-ingredient liners throughout the export logistics chain.

The North American regulatory environment, particularly FDA food contact material regulations and EPA chemical packaging containment standards, drives demand for certified, traceable plastic liner products and sustains a premium pricing environment that rewards technically capable manufacturers. Domestic liner producers, including RRR Supply, Inc., A-Pac Manufacturing Co., Inc., American Plastics Company, and Caltex Plastics Inc. benefit from proximity to major agricultural processing hubs and established relationships with FIBC and multi-wall sack producers. The region’s pharmaceutical manufacturing base, concentrated in New Jersey, Pennsylvania, and North Carolina, is also a growing source of premium single-use GMP-compliant liner demand, with the reshoring of API manufacturing post-pandemic further reinforcing this trend.

Europe Plastic Liner Market Trends and Insights

Europe is the most regulatory-driven and sustainability-focused regional market for plastic liners, with the European Union’s comprehensive packaging legislation framework significantly shaping product development and market structure. The EU Packaging and Packaging Waste Regulation (PPWR), alongside the Single-Use Plastics Directive and REACH chemical substance regulations, is creating a complex compliance environment that is accelerating the shift toward mono-material recyclable liner structures and recycled-content PE and PP liner grades. Germany, France, the United Kingdom, and the Netherlands are the most significant national markets, reflecting their large chemical, pharmaceutical, food processing, and bulk commodity trading industries.

Polymer-Synthese-Werk GmbH and NITTEL GmbH, both German-headquartered specialist liner manufacturers, are well-positioned in the European market given their technical expertise in custom-engineered liner solutions for chemical and food-grade applications and their ability to navigate complex EU certification requirements. The UK’s departure from the EU has introduced some supply chain regulatory divergence, though the UK Packaging Recovery Note (PRN) system and forthcoming Extended Producer Responsibility (EPR) reforms are maintaining strong alignment with EU sustainability ambitions. Spain and Italy’s growing agri-food export industries are contributing incremental demand in the region.

Asia Pacific Plastic Liner Market Trends and Insights

Asia Pacific is the fastest growing regional market for plastic liners over the 2026-2033 forecast period, driven by the region’s immense and rapidly modernizing agricultural, chemical, and manufacturing economies. China is the dominant national market, the world’s largest producer of polyethylene and polypropylene resins, and a major manufacturer and consumer of FIBC and bulk packaging systems. China’s agricultural sector, supporting over 1.4 billion people, generates enormous domestic demand for grain, fertilizer, and agrochemical liners, while its expansive chemical and polymer export industry drives demand for industrial-grade drum and container liner solutions. Chinese liner manufacturers benefit from highly competitive raw material costs and scale manufacturing efficiencies that support both domestic supply and export competitiveness.

India is one of the highest-growth individual country markets for plastic liners. The country’s agricultural sector, with total food grain production exceeding 330 million tonnes in 2023-24 according to the Ministry of Agriculture and Farmers’ Welfare, Government of India, generates vast demand for food-grade liners, while the rapidly expanding Indian pharmaceutical industry, the world’s largest supplier of generic medicines by volume, is an increasingly important driver of GMP-certified pharmaceutical liner demand. Companies such as Shagoon Packaging Pvt. Ltd. and Synpack Avonflex Pvt. Ltd. are scaling operations to serve this domestic demand. Japan, South Korea, Vietnam, and Thailand contribute additional demand from their advanced food processing, chemical, and electronics-linked industrial packaging sectors.

Competitive Landscape

The global plastic liner market is highly fragmented, with numerous regional and country-level manufacturers serving localized demand across agriculture, food processing, chemicals, and pharmaceuticals. Competitive positioning is primarily defined by specialization in regulatory compliance, technical customization, and proximity to key industrial clusters rather than global production scale. Manufacturers differentiate through certified food-contact materials, GMP-compliant cleanroom production for pharmaceutical applications, and advanced film extrusion capabilities that ensure precise thickness control and barrier performance consistency.

Strategically, companies are focusing on value-added services such as custom-engineered liner design, rapid prototyping, and application-specific performance optimization to strengthen customer retention. Integrated supply-chain models, including vendor-managed inventory and consignment stocking programs, are increasingly used to secure long-term contracts with bulk commodity exporters and pharmaceutical manufacturers. Sustainability is becoming a central competitive lever, with growing investment in recyclable mono-material structures and reduced-gauge solutions aligned with emerging packaging waste regulations. Selective regional acquisitions are gradually reshaping the mid-tier competitive landscape to expand geographic reach and technical capabilities.

Key Developments

- January, 2025: Zeus announced the upcoming launch of its next-generation StreamLiner NG film-cast PTFE catheter liners featuring improved flexibility, reduced defects, and higher performance to be showcased at MD&M West.

- November, 2025: Polyzent Trading announced it will open its first stretch-film manufacturing facility in Lynchburg, Virginia, investing US $1.1 million to produce industrial stretch film and create about 20 jobs, strengthening local packaging supply chains.

- February 2026: Junkosha unveiled an expanded range of larger-diameter etched PTFE catheter liners supporting up to 5 mm inner diameters for peripheral vascular device delivery systems at MD&M West.

Companies Covered in Plastic Liner Market

- RRR Supply, Inc.

- A-Pac Manufacturing Co., Inc.

- Plascon Group International Plastics Inc.

- American Plastics Company

- Shagoon Packaging Pvt. Ltd.

- Synpack Avonflex Pvt. Ltd.

- Caltex Plastics Inc.

- Polymer-Synthese-Werk GmbH

- Chiltern Plastics

- NITTEL GmbH

- Bulk Lift International, LLC

- BULK-FLOW (Europe) Ltd.

- Greif, Inc.

- LC Packaging International B.V.

- Junkosha

- Polyzent Trading

- Zeus

Frequently Asked Questions

The global Plastic Liner market is valued at US$ 5.3 billion in 2026 and is projected to reach US$ 7.4 billion by 2033 at a CAGR of 4.8%.

Demand is driven by rising bulk commodity trade, stricter food and pharmaceutical packaging regulations, and growing use of certified FIBC liner systems.

North America leads with around 28% revenue share in 2025, supported by strong agricultural exports and a compliance-driven pharmaceutical sector.

The key opportunity lies in recyclable and sustainable liner solutions aligned with evolving packaging waste and recyclability regulations.

Key players include Greif, Inc., LC Packaging International B.V., NITTEL GmbH, Caltex Plastics Inc., and A-Pac Manufacturing Co., Inc., among others, competing through certification and customized liner solutions.