- Clothing, Footwear, & Accessories

- Plano Sunglasses Market

Plano Sunglasses Market Size, Share, and Growth Forecast, 2026 - 2033

Plano Sunglasses Market By Product (Polarized, Non-polarized Sunglasses), Material (CR-39, Polycarbonate, Others), Style (Aviators, Wayfarers, Round, Others), Distribution Channel (Online, Offline Sales Channels), and Regional Analysis for 2026 - 2033

Plano Sunglasses Market Size and Trends Analysis

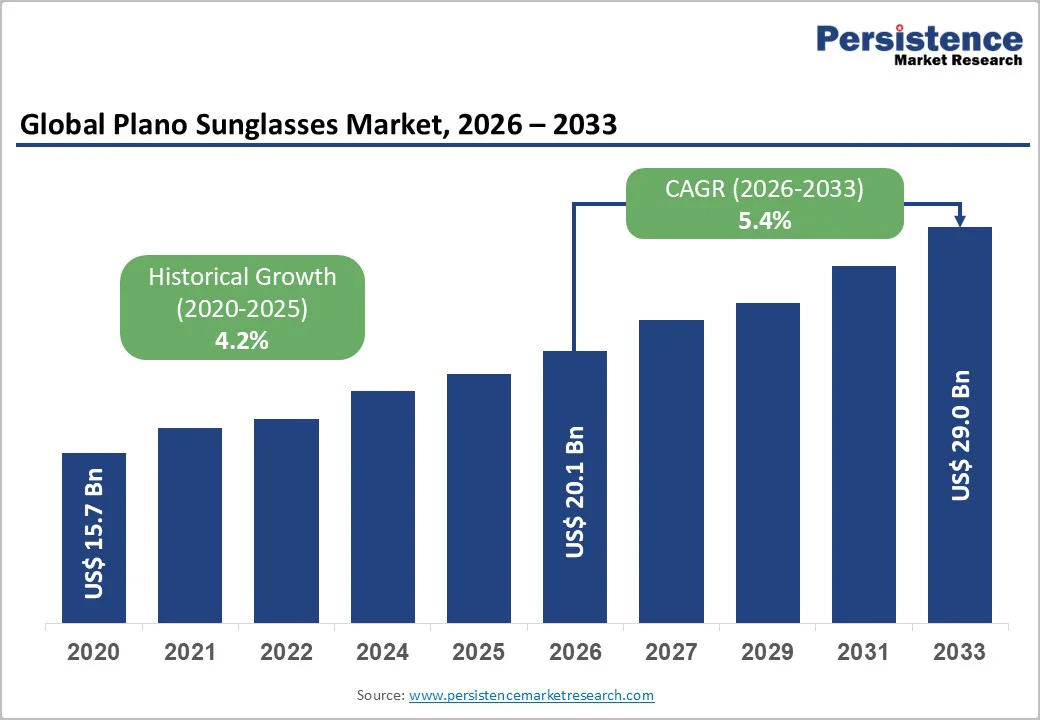

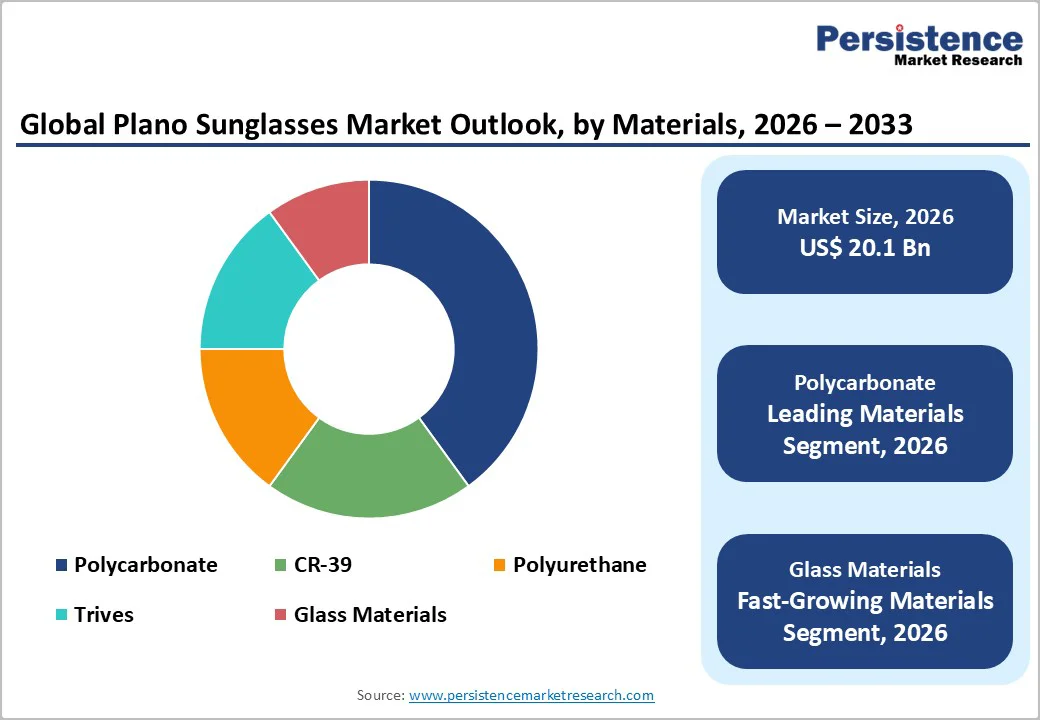

The global plano sunglasses market size is likely to be valued at US$20.1 billion in 2026. It is expected to reach US$29.0 billion by 2033, growing at a CAGR of 5.4% from 2026 to 2033, driven by the increasing prevalence of fashion-forward eyewear, rising demand for UV-protective lenses in polarized and non-polarized sunglasses, and advancements in lightweight materials such as polycarbonate and Trivex.

Demand for stylish, functional plano sunglasses, especially aviators and wayfarers, drives adoption across demographics. Innovations in CR-39 and glass materials meet the needs for durability and clarity, while rising acceptance as everyday style and eye-protection staples boosts growth across online/offline channels.

Key Industry Highlights:

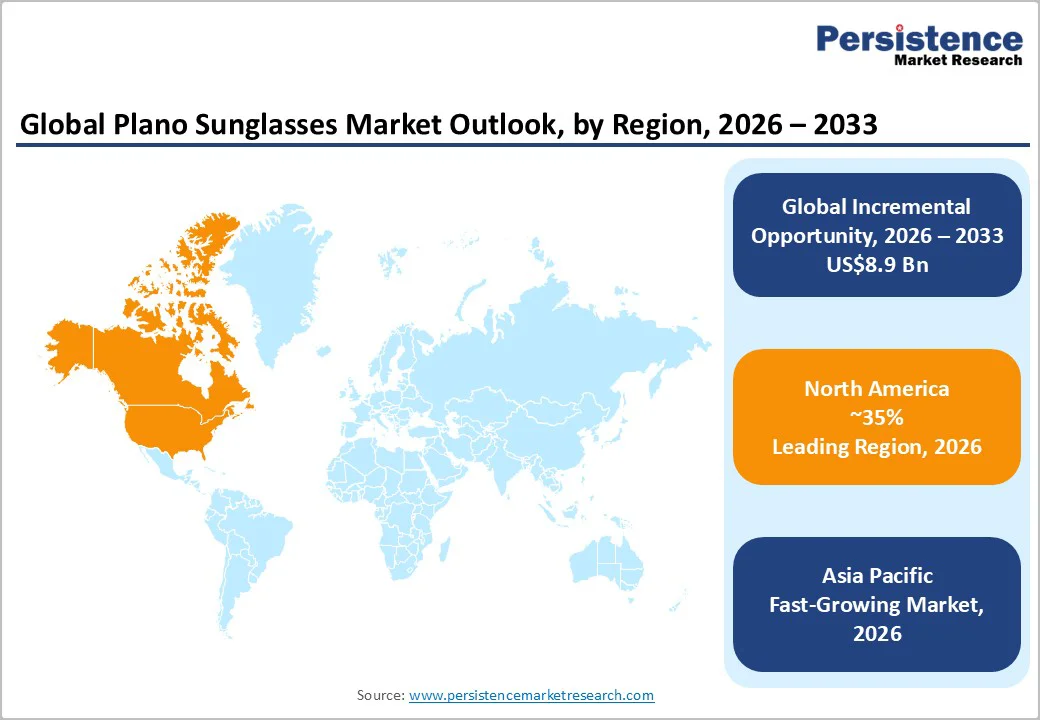

- Leading Region: North America, estimated to account for a 35% market share in 2026, driven by high fashion consciousness, strong prevalence of premium eyewear, and robust retail activities in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by increasing disposable incomes, rising awareness of UV protection, and growing investments in e-commerce sales channels in China and India.

- Dominant Product: Polarized sunglasses, anticipated to hold approximately 55% of the market share, due to they reduce glare, enhance visual clarity, and offer superior eye protection, making them ideal for outdoor activities.

- Leading Material: Polycarbonate, likely to account for over 40% of market revenue, due to it is lightweight, highly impact-resistant, and durable properties, making it ideal for sports, safety, and everyday sunglasses.

- Leading Style: Wayfarers, to contribute nearly 30% of the market revenue in 2026, due to their timeless design, versatile style, and broad appeal across age groups and occasions.

- Leading Distribution Channel: Online sales channels, to dominate with approximately 45% share, due to their convenience, wide accessibility, and seamless shopping experience, allowing consumers to browse, compare, and purchase sunglasses from anywhere.

| Key Insights | Details |

|---|---|

|

Plano Sunglasses Market Size (2026E) |

US$20.1 Bn |

|

Market Value Forecast (2033F) |

US$29.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Fashion-Forward Eyewear and Demand for UV-Protective Lenses

The rising prevalence of fashion-forward eyewear globally is a primary driver of the plano sunglasses market. Eyewear has evolved from being a purely functional accessory to a key fashion statement, with consumers seeking styles that reflect personal identity, lifestyle, and status. Social media influence, celebrity endorsements, and lifestyle trends have significantly amplified the desire for stylish sunglasses, particularly among younger generations and urban populations. As a result, brands are constantly innovating with bold designs, unique frame shapes, color variations, and limited-edition collections to capture attention and cater to evolving fashion preferences.

Heightened awareness of the harmful effects of ultraviolet (UV) radiation has fueled demand for sunglasses that offer reliable eye protection. Consumers are prioritizing lenses that block UVA and UVB rays, reduce glare, and provide clarity, driving the adoption of polarized, photochromic, and high-quality glass or polycarbonate lenses.

High Development and Material Costs

High development and material costs remain a significant challenge in the plano sunglasses market, affecting both established brands and emerging players. The development of high-performance sunglasses requires investment in advanced lens technologies, such as polarized, photochromic, anti-reflective, and scratch-resistant coatings, which involve sophisticated chemical processes and precision manufacturing. Research and development also extend to ergonomic frame designs, lightweight composites, and memory metals, requiring specialized expertise, prototyping, and iterative testing to ensure durability, comfort, and safety.

Material costs further contribute to the overall expense. Premium lenses made from polycarbonate, Trivex, or glass are more expensive than standard plastics, while metal and composite frames, including titanium, carbon fiber, and bio-based polymers, carry higher production costs. The shift toward sustainable materials, such as recycled acetate and biodegradable plastics, also increases costs due to limited supply chains and specialized processing requirements.

Technological Advancements in Lens and Frame Materials

Technological advancements in lens and frame materials are creating major opportunities in the global plano sunglasses market, reshaping product performance, comfort, and consumer appeal. Innovations in lens technology, such as enhanced scratch-resistant coatings, anti-reflective treatments, and high-definition optical lenses, are improving visual clarity and durability.

Polycarbonate and Trivex lenses are increasingly popular for their lightweight properties and superior impact resistance, making them ideal for sports, outdoor activities, and everyday use. Advancements in polarized and photochromic lens formulations are enhancing glare reduction and UV protection, offering consumers more functional and versatile options.

The adoption of advanced composites, memory metals, and bio-based materials is transforming design possibilities. Modern frames made from TR90, titanium alloys, and carbon fiber provide a blend of durability, flexibility, and ultralight comfort. Sustainable materials such as recycled plastics, biodegradable acetate, and plant-derived polymers also align with rising consumer demand for eco-friendly products. 3D printing and digital manufacturing are also opening opportunities for customizable fit, precision shaping, and rapid prototyping.

Category-wise Analysis

Product Insights

Polarized sunglasses are anticipated to dominate the market, accounting for approximately 55% of the market share in 2026. Their leadership is driven by superior glare reduction, enhanced visual clarity, and improved driving safety, making them ideal for outdoor and daily use. Polarized lenses also boost contrast and eye comfort, especially in bright environments. For example, DE RIGO REM’s polarized collections are widely preferred for their advanced UV protection and stylish designs, appealing to both performance-focused and fashion-conscious consumers.

Non-polarized sunglasses are likely to be the fastest-growing segment, due to their affordable pricing, strong fashion appeal, and suitability for everyday casual wear, especially among urban consumers. Lightweight frames, trendy colors, and frequent style updates drive popularity in the Asia Pacific and Europe. Their wide availability across online platforms and retail stores further accelerates adoption. For example, Fast-fashion brands such as H&M and Zara frequently launch non-polarized collections that attract young buyers seeking stylish yet budget-friendly eyewear options.

Material Insights

Polycarbonate leads the market, holding approximately 40% of the share in 2026, driven by its superior impact resistance, lightweight structure, and high durability, making it ideal for sports, outdoor, and safety eyewear. Its built-in UV protection and shatterproof properties make it preferred for active users and children. Wide availability and affordability also strengthen its dominance across both premium and mass-market sunglasses. For example, brands such as Oakley widely use polycarbonate (Plutonite) lenses in their performance eyewear for enhanced protection and clarity.

Glass materials represent the fastest-growing segment, driven by their superior optical clarity, exceptional scratch resistance, and premium feel, making them highly preferred in luxury eyewear. Consumers seeking long-lasting durability and crisp visual performance increasingly choose glass lenses, especially in high-end collections. Their association with craftsmanship and premium aesthetics further accelerates demand. For example, Ray-Ban’s Classic Series uses glass lenses in several models, offering enhanced clarity and a premium experience for discerning buyers.

Style Insights

Wayfarers are expected to dominate the market, accounting for nearly 30% of revenue in 2026, thanks to their timeless design, universal fit, and strong appeal for casual and everyday use. Their versatility appeals to all age groups, while ongoing updates to colors, materials, and sizes keep them trend-relevant. Wide availability across both premium and budget-friendly brands also supports their leadership. For example, Ray-Ban’s iconic Wayfarer series remains one of the most popular and widely adopted eyewear styles globally.

Aviators are representing the fastest-growing segment, due to their iconic teardrop design, lightweight metal frames, and strong association with aviation culture, which continue to attract consumers globally. Increasing adoption by pilots, outdoor enthusiasts, and fashion-forward buyers is boosting demand. Their enduring style, robust construction, and widespread availability across premium and mass-market brands further accelerate growth. For example, Ray-Ban’s Aviator and Randolph Engineering’s military-style aviators remain highly popular among professionals and style-conscious users alike.

Distribution Channel Insights

Online sales channels are likely to dominate the market, with approximately 45% share in 2026, driven by high convenience, easy accessibility, and smooth browsing experiences. Features such as virtual try-ons, fast delivery, competitive pricing, and flexible return policies make e-commerce the preferred option for consumers. Growing digital adoption and strong influencer-driven marketing further boost online purchases. For example, Amazon and Warby Parker’s online platforms attract large customer bases through extensive collections and user-friendly shopping tools.

Offline sales channels are the fastest-growing, as consumers increasingly prefer in-store experiences where they can physically try on frames, assess comfort, and receive personalized fitting support. Optical stores and boutiques provide expert guidance, style recommendations, and immediate purchase options, building trust and satisfaction. The hands-on experience, combined with expanding retail networks, continues to drive strong adoption. For example, LensCrafters and Titan Eye+ stores attract buyers through personalized consultations and extensive on-site eyewear selections.

Regional Insights

North America Plano Sunglasses Market Trends

North America is projected to account for nearly 35% of the market share in 2026, driven by strong consumer awareness of UV protection, rising outdoor recreation culture, and high demand for fashionable yet functional eyewear. The U.S. remains the largest market in the region, supported by a strong preference for premium brands, advanced lens technologies, and durable frame materials. Increasing participation in activities such as hiking, cycling, beach sports, and driving has strengthened the need for polarized and impact-resistant lenses, boosting innovation and adoption.

The region also benefits from a well-established retail ecosystem, with optical stores, specialty eyewear boutiques, and large omnichannel retailers offering a wide range of options. E-commerce has expanded significantly, with virtual try-on tools, influencer-led promotions, and personalized shopping experiences accelerating online purchases. Sustainability is becoming a major trend, with brands introducing recycled plastics, biodegradable materials, and responsibly sourced packaging to meet shifting consumer expectations. Collaborations between eyewear companies and lifestyle or fashion brands are shaping design trends and expanding product visibility.

Europe Plano Sunglasses Market Trends

Europe is projected to lead with a market share of 25% in 2026, supported by a strong fashion culture, high consumer spending on premium eyewear, and increasing awareness of eye protection. Countries such as Italy, France, Germany, and the U.K. remain influential trendsetters in global eyewear design, helping plano sunglasses evolve as both a functional and fashion-driven accessory. Consumers in Europe increasingly prioritize high-quality materials, UV protection, and durability, driving demand for advanced lenses, including scratch-resistant, polarized, and lightweight options.

The region also benefits from a mature retail ecosystem, including optical chains, luxury boutiques, and fast-growing e-commerce channels. European brands are focusing on craftsmanship, minimalistic aesthetics, and sustainable production methods, with growing adoption of recycled acetate, plant-based materials, and eco-friendly packaging. This aligns well with Europe’s strong environmental regulations and rising consumer preference for ethical purchases. Digital transformation is also shaping market trends. The integration of virtual try-on tools, AI-enabled style recommendations, and seamless online buying experiences is expanding reach, especially among younger demographics. Collaborations between eyewear makers and fashion labels continue to boost product visibility.

Asia Pacific Plano Sunglasses Market Trends

Asia Pacific is likely to be the fastest-growing market, driven by rising disposable incomes, rapid urbanization, and the increasing influence of fashion and lifestyle trends across major economies such as China, India, Japan, and South Korea. Consumers in the region are increasingly aware of the importance of UV protection and eye health, significantly boosting demand for high-quality plano sunglasses. Expanding e-commerce channels, aggressive digital marketing, and influencer-led fashion culture are further shaping purchasing behavior, particularly among younger consumers.

Local and global brands are intensifying competition by offering region-specific designs, lightweight materials, and affordable premium options to attract the growing middle-class segment. Sustainability has also become a key trend, with more brands adopting eco-friendly frames, recycled plastics, and bio-based lenses. The expansion of organized retail and optical chains is improving access to premium eyewear across urban and semi-urban areas. Technological integration is another major driver, with AR-powered virtual try-on tools, smart recommendations, and personalized fitting enhancing consumer experience.

Competitive Landscape

The global plano sunglasses market is highly competitive, driven by major international eyewear brands and specialized players focusing on style, lens technology, and materials. In North America and Europe, leaders such as Ray-Ban and DE RIGO REM strengthened their positions through strong retail networks, brand equity, and ongoing R&D investments.

In the Asia Pacific region, Marcolin Eyewear expanded its reach with region-specific designs and competitive pricing. Sustainability further intensified competition, with brands adopting recycled materials and bio-based lenses. Companies also accelerated partnerships, acquisitions, and digital innovations, including AR and virtual try-on tools, to enhance consumer engagement and broaden market presence.

Key Industry Developments

- In September 2025, Marcolin S.p.A. announced that PAI Partners and other minority shareholders had agreed to sell the Marcolin Group to VSP Vision. The acquisition of Marcolin, a global leader in eyewear design, manufacturing, and distribution, marked a significant investment by VSP Vision to deliver enhanced value to its stakeholders.

- In May 2025, Marcolin and adidas advanced their long-term growth strategy by extending their global eyewear licensing agreement for the adidas Sport and adidas Originals labels through 2032, strengthening their collaboration and expanding their joint presence in the performance and lifestyle eyewear market.

Companies Covered in Plano Sunglasses Market

- American Sunglass Manufacturing

- DE RIGO REM

- FGX International (EssilorLuxottica)

- Fossil

- Marcolin Eyewear Modo Eyewear

- Ray-Ban

- Silhouette International

- Vision Ease

- Vogue Eyewear

- Warby Parker

- Zeiss

Frequently Asked Questions

The global plano sunglasses market is projected to reach US$20.1 billion in 2026.

The rising prevalence of fashion-forward eyewear and demand for UV-protective lenses are key drivers.

The plano sunglasses market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Advancements in sustainable materials and AR try-on features are key opportunities.

American Sunglass Manufacturing, DE RIGO REM, Fossil, Ray-Ban, and Warby Parker are the key players.