- Specialty & Fine Chemicals

- Performance Minerals Additives Market

Performance Minerals Additives Market Size, Share, and Growth Forecast 2026 - 2033

Performance Minerals Additives Market by Product Type (Calcium Carbonate, Talc, Kaolin, Bentonite, Silica, Mica, Others), Additive Type (Antioxidants, Dispersants, Defoamers, Anti-wear Additives, Other), Application (Plastics, Paints & Coatings, Adhesives & Sealants, Rubber, Lubricants, Other), End-use Industry (Automotive, Building & Construction, Packaging, Consumer Goods, Agriculture, Other), and Regional Analysis for 2026 - 2033

Performance Minerals Additives Market Size and Trend Analysis

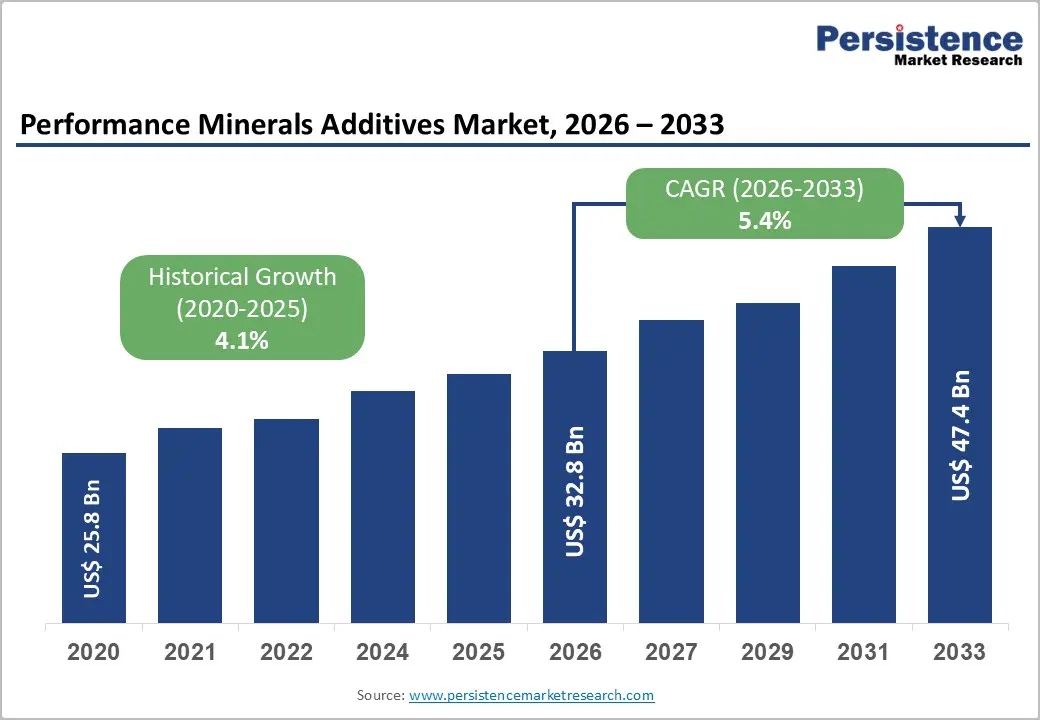

The global Performance Minerals Additives Market size is supposed to be valued at US$ 32.8 billion in 2026 and is projected to reach US$ 47.4 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033. The surging adoption of high-performance mineral fillers across lightweighting initiatives in automotive and sustainable construction applications is driving this expansion. U.S. Geological Survey data confirm that minerals such as talc (32% of U.S. sales directed to plastics) and kaolin (56% used as fillers and extenders) deliver critical functional benefits, including dimensional stability, cost reduction, and enhanced mechanical properties.

These advantages align with global manufacturing shifts toward lighter vehicles and energy-efficient buildings, where mineral additives replace heavier traditional materials while maintaining structural integrity and thermal performance. Regulatory emphasis on reduced emissions further accelerates substitution, positioning mineral-based solutions as essential enablers of next-generation industrial formulations.

Key Industry Highlights:

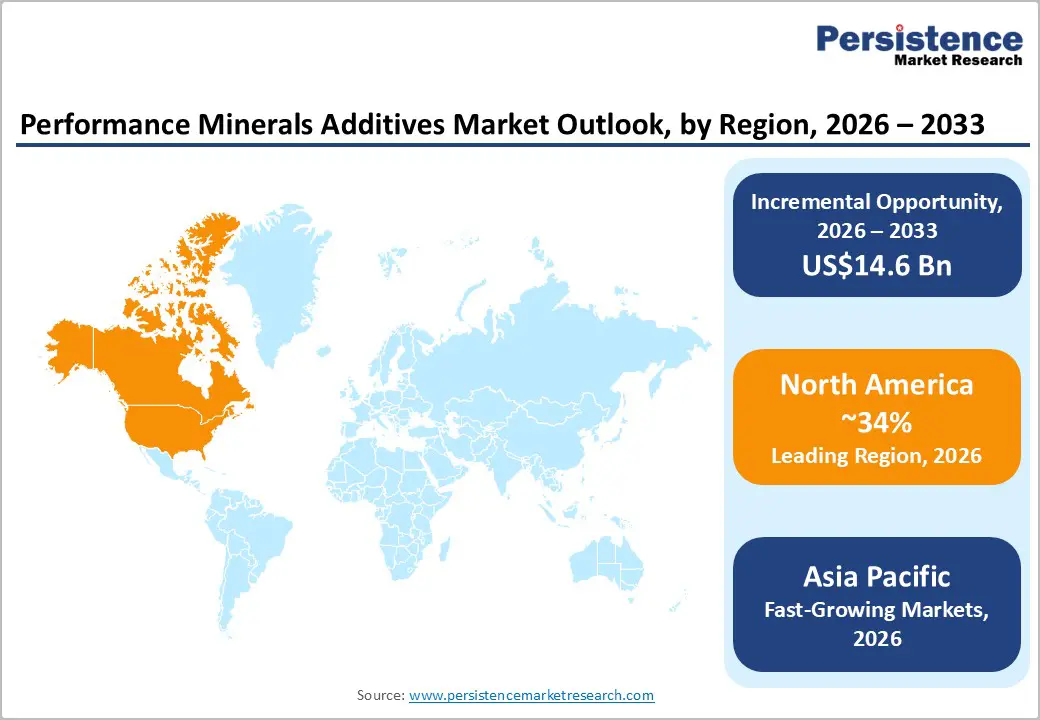

- Leading Region: North America dominates the market, with 34% market share, through domestic production strength and regulatory alignment, supported by U.S. Geological Survey output data and innovation leadership.

- Fastest Growing Region: Asia Pacific advances rapidly via manufacturing scale, local capacity investments, and strong demand from plastics and construction in China, India, and ASEAN.

- Dominant Segment: Calcium Carbonate within Product Type leads with approximately 42% share due to unmatched volume, cost efficiency, and filler versatility.

- Fastest Growing Segment: Plastics application grows quickest, propelled by lightweighting needs and mineral dispersion technologies.

- Key Market Opportunity: Energy-transition applications for thermal management and battery materials offer premium growth through sustainable mineral innovations.

| Key Insights | Details |

|---|---|

|

Performance Minerals Additives Market Size (2026E) |

US$ 32.8 Bn |

|

Market Value Forecast (2033F) |

US$ 47.4 Bn |

|

Projected Growth CAGR (2026–2033) |

5.4% |

|

Historical Market Growth (2020–2025) |

4.1% |

Market Dynamics

Drivers - Rising Demand for Lightweight Materials in Automotive and Plastics Applications

The Performance Minerals Additives Market is experiencing robust growth driven by the automotive sector’s push toward vehicle lightweighting to meet stringent fuel-efficiency and emissions standards. Talc and kaolin, according to U.S. Geological Survey Mineral Commodity Summaries 2026, account for significant shares in plastics compounding, talc at 32% of U.S. consumption for flexural strength improvement and kaolin as a primary filler-extender in rubber and plastic components. These minerals reduce component weight by up to 20% while preserving impact resistance and dimensional stability, directly supporting electric vehicle battery housing and interior parts.

Growing global vehicle production, coupled with OEM mandates for recycled content, amplifies demand for dispersible mineral additives that enhance processing efficiency. This driver not only lowers overall vehicle mass but also improves thermal management in under-hood applications, delivering measurable cost savings and performance gains that convince manufacturers to rapidly scale adoption.

Expansion of Construction and Paints & Coatings Industries Driven by Infrastructure Investments

Infrastructure spending worldwide fuels the Performance Minerals Additives Market through increased consumption in paints, coatings, and construction composites. U.S. Geological Survey reports highlight kaolin’s 56% allocation to fillers and extenders in paint and construction products, while limestone-derived calcium carbonate competes effectively as a cost-effective opacifier and rheology modifier.

Public-private partnerships and green building codes require durable, low-VOC formulations, where mineral additives improve weather resistance, scrubability, and hiding power. In Europe and Asia, large-scale urbanization projects incorporate these additives into sealants and adhesives to build energy-efficient structures. The result is higher throughput in coating lines and extended service life of built assets, providing clear economic justification for wider integration and sustained market momentum.

Restraints - Stringent Environmental Regulations on Mining and Processing

Regulatory frameworks such as EPA air-quality standards and EU REACH compliance impose substantial operational costs on mineral extraction and beneficiation. U.S. Geological Survey 2026 notes reduced import volumes for certain clays due to environmental audits, elevating compliance expenses for producers. Mines must invest in dust suppression and water recycling systems, delaying capacity expansions and squeezing margins. Smaller operators face disproportionate burdens, leading to supply tightness that raises input costs for downstream formulators in the plastics and coatings sectors. These constraints slow market penetration in price-sensitive segments despite strong end-user demand.

Supply Chain Vulnerabilities from Geopolitical Trade Tensions

Dependence on concentrated production, China leading in mica (78% of world output) and talc, exposes the Performance Minerals Additives Market to tariff-induced price volatility. U.S. Geological Survey data indicate high reliance on net imports for several clays, amplifying costs when trade barriers disrupt flows. Geopolitical events, including sanctions affecting Iranian bentonite supplies, further constrain the availability of specialty grades used in drilling muds and absorbents. Downstream industries encounter delayed deliveries and higher logistics expenses, dampening confidence in long-term sourcing and restraining overall volume growth.

Opportunity - Adoption of Sustainable and Recycled Mineral Solutions in Energy Transition Applications

Imerys’ establishment of a dedicated “Solutions for Energy Transition” business area signals strong potential for mineral additives in battery materials, thermal interface compounds, and hydrogen storage. High-purity kaolin and surface-treated calcium carbonate enhance conductivity while reducing ceramic filler loadings in thermal management systems.

U.S. Geological Survey trends toward circular-economy practices support the recycling of process by-products, opening new revenue streams. Policy incentives for net-zero technologies are expected to generate significant demand from the electric vehicle and renewable energy sectors through 2033, offering participants premium pricing and differentiation.

Growth in Agricultural and Consumer Goods Segments via Functional Additives

Rising focus on precision agriculture and eco-friendly packaging creates demand for bentonite and mica-based additives in soil amendments, slow-release fertilizers, and barrier films. U.S. Geological Survey confirms bentonite’s established role in absorbents, now extending to biodegradable mulch films that improve water retention and nutrient delivery.

Consumer goods manufacturers seek mineral-enhanced formulations for personal care and food-contact applications that deliver rheology control without synthetic polymers. These fastest-growing end-uses promise double-digit segment expansion, supported by regulatory approval of natural minerals and brand commitments to sustainable sourcing.

Category-wise Analysis

Product Type Insights

Calcium Carbonate emerges as the leading segment in the Performance Minerals Additives Market, commanding approximately 42% share. U.S. Geological Survey Mineral Commodity Summaries 2026 underscores its dominance through massive limestone resources, with world production exceeding 250 million metric tons, and direct competition with clays in filler-extender roles. Its versatility in plastics, paints, and rubber stems from superior whiteness, low oil absorption, and cost-effectiveness, enabling higher loading levels without compromising flow or mechanical properties.

Surface-treated grades further enhance dispersion and adhesion, meeting stringent automotive and construction specifications. This positions calcium carbonate ahead of talc and kaolin, delivering consistent supply security and performance reliability that drives formulator preference across high-volume applications.

Additive Type Insights

Dispersants hold the leading position within the Additive Type category, accounting for an estimated 35% share. Their effectiveness in uniformly dispersing mineral particles within polymer matrices and liquid systems is essential for achieving consistent performance in plastics and coatings. U.S. Geological Survey data on kaolin and talc processing highlight the critical role of dispersant technologies in preventing particle agglomeration, thereby improving processing efficiency and overall product uniformity.

Specialty dispersants further facilitate higher filler loadings while maintaining optimal viscosity control, supporting lightweighting objectives in automotive applications. This functional advantage over other additive types, such as antioxidants or defoamers, reinforces dispersants’ market dominance and continues to drive innovation in surface-chemistry solutions.

Application Insights

Plastics constitute the leading application segment, accounting for approximately 38% of the market. According to U.S. Geological Survey data, talc directs nearly 32% of its U.S. sales toward plastics to enhance flexural strength, while kaolin serves as a critical filler-extender in both plastic and rubber formulations. The incorporation of mineral additives contributes to reduced material density, improved heat-deflection performance, and superior dimensional stability, attributes essential for automotive interior components, advanced packaging films, and a wide range of consumer durable products.

Furthermore, strong compatibility with recycled resins supports circular-economy initiatives, enabling manufacturers to replace heavier materials without compromising structural performance. This synergy positions plastics as the primary growth driver within the Performance Minerals Additives Market.

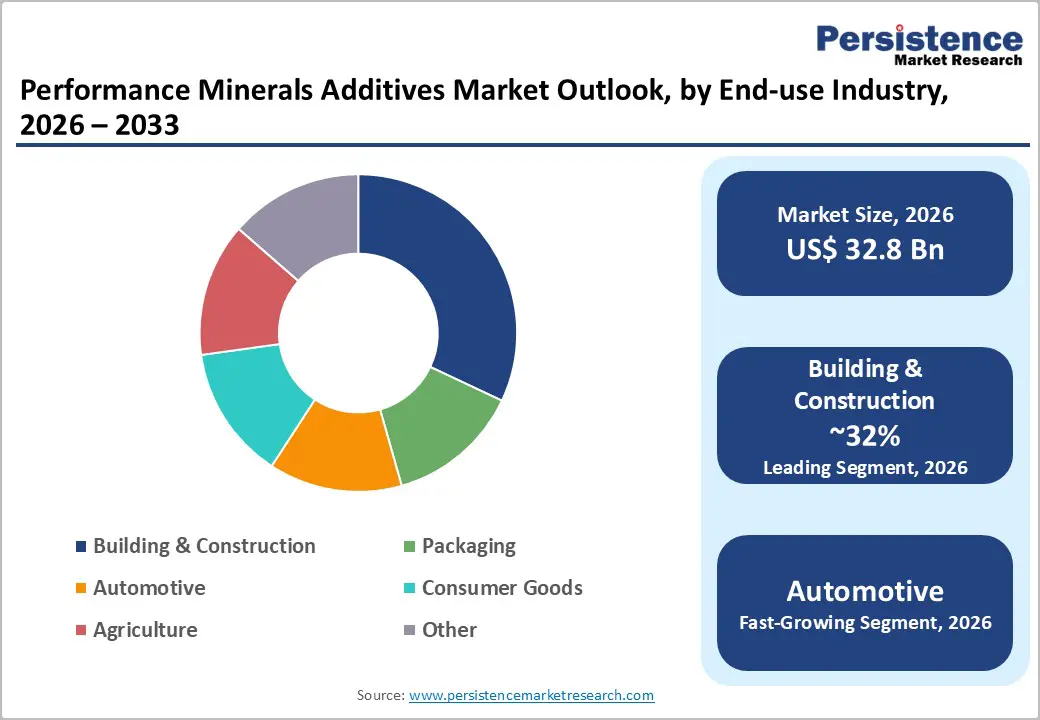

Industry Insights

The Building & Construction sector represents the leading end-use industry, accounting for approximately 32% of total market share. Kaolin, used as a filler and extender in paints and construction materials at 56%, together with calcium carbonate’s critical role in cementitious systems, enhances both structural resilience and aesthetic performance across applications.

According to the U.S. Geological Survey (2026), rising consumption is closely linked to large-scale public infrastructure initiatives and green building mandates that prioritize weather-resistant coatings and advanced sealant technologies. These mineral additives provide long-term durability, reduced maintenance requirements, and compliance with stringent energy-efficiency standards, prompting architects, engineers, and project specifiers to integrate them consistently across residential, commercial, and civil construction projects.

Regional Insights

North America Performance Minerals Additives Market Trends

North America maintains market leadership through robust domestic production and innovation ecosystems. U.S. Geological Survey data confirm strong U.S. output of kaolin (4.8 million tons) and bentonite (4.1 million tons), bolstered by EPA-aligned sustainability programs that favor locally sourced minerals. U.S. trade tensions with China have prompted tariff adjustments on imported fillers, elevating domestic capacity utilization and encouraging vertical integration among producers. Potential supply disruptions from U.S.-Iran geopolitical developments affect bentonite imports, accelerating the adoption of North American alternatives and reinforcing self-sufficiency.

The innovation ecosystem thrives via collaborations between Minerals Technologies Inc. and automotive OEMs, delivering tailored dispersants that support electric vehicle lightweighting targets. Continued regulatory focus on air-quality standards drives investment in low-emission processing technologies, while public infrastructure bills sustain demand in construction coatings. These dynamics collectively position North America as a stable, high-value hub for performance mineral solutions amid global supply uncertainties.

Europe Performance Minerals Additives Market Trends

Europe demonstrates resilient performance across Germany, the U.K., France, and Spain despite external pressures. U.S. Geological Survey import trends indicate reduced reliance on certain Asian clays, offset by intra-EU sourcing and harmonized REACH regulations that streamline approval of surface-treated minerals. Germany’s automotive sector and France’s construction boom drive consumption of talc and kaolin for lightweight components and high-performance coatings. U.S. trade tensions have prompted diversification away from Chinese mica, favoring European mica and calcium carbonate capacities that comply with stringent environmental standards.

Spain’s growing renewable energy projects further integrate mineral additives in thermal management applications. Regulatory harmonization under the European Green Deal accelerates circular models, enabling the recycling of mineral by-products and fostering cross-border supply chain stability. This regulatory and industrial synergy sustains steady growth while mitigating geopolitical risks associated with U.S.-Iran developments.

Asia Pacific Performance Minerals Additives Market Trends

Asia Pacific exhibits dynamic expansion fueled by manufacturing advantages in China, Japan, India, and ASEAN nations. U.S. Geological Survey production figures highlight China’s dominance in mica (78%) and talc, supporting cost-competitive supply for regional plastics and packaging converters. India’s infrastructure push and ASEAN’s growth in electronics assembly drive demand for dispersant-enhanced fillers that improve processing efficiency. U.S. trade tensions have encouraged local capacity build-out and technology upgrades, reducing exposure to tariffs while maintaining export momentum to Europe and North America. Potential U.S.-Iran supply constraints on bentonite are prompting intra-regional sourcing from India and Turkey.

Manufacturing scale, combined with government incentives for sustainable materials, positions the Asia Pacific as the fastest-growing consumer base. Japanese and Chinese R&D in high-purity grades for electronics and automotive further strengthens the region’s competitive edge within the Performance Minerals Additives Market.

Competitive Landscape

The performance minerals additives market remains fragmented, with numerous regional players alongside global leaders pursuing differentiation through vertical integration and sustainability initiatives. Leading companies invest heavily in R&D for surface-modified grades and circular processing technologies, expanding production footprints via targeted acquisitions and greenfield plants. Key differentiators include proprietary dispersion technologies and traceability systems that meet end-user ESG requirements. Emerging business models emphasize co-development partnerships with OEMs and closed-loop recycling of mineral by-products, enabling premium pricing and long-term contracts. Overall concentration is moderate, allowing nimble innovators to capture niche opportunities in energy transition and agricultural segments while established firms leverage scale for cost leadership.

Key Developments:

- March 2026: BASF is increasing prices for products in its antioxidant, process stabilizer and light stabilizer portfolio for plastic applications globally by up to 20 percent. The price adjustment is primarily required due to significant cost increases for essential raw materials, inflationary effects on fixed cost, and increases in freight rates.

- January 2026: Minerals Technologies Inc. announced an expansion of its paper and packaging business in Asia that included the startup of three new satellite plants in 2025, the doubling of capacity at an existing satellite, and the expected commissioning of an additional new satellite in early 2026.

- November 2025: Omya announced the launch of a new business unit specialising in the sales and distribution of specialty materials and ingredients as part of a major reorganisation of the company's business.

Top Companies in Performance Minerals Additives Market

Imerys S.A. (Paris, France) leads through its comprehensive portfolio of engineered minerals and recent focus on energy-transition solutions. The company’s global mine-to-market operations deliver high-purity grades for plastics and coatings, supported by continuous innovation in surface chemistry that enhances compatibility and performance. Strategic expansions and sustainability programs reinforce its position as a preferred supplier to automotive and construction clients worldwide.

Minerals Technologies Inc. (New York, U.S.) excels in specialty additives and consumer applications, leveraging strong North American production assets and Asia-Pacific growth projects. Its focus on functional fillers for packaging and household products, combined with disciplined pricing and operational excellence, drives consistent profitability and market penetration across high-volume segments.

Omya AG (Oftringen, Switzerland) maintains leadership via its expertise in calcium carbonate processing and distribution networks across Europe and beyond. The firm’s emphasis on sustainable sourcing and customized formulations for paints and plastics delivers superior opacity and rheology control, securing long-term relationships with major industrial customers.

Companies Covered in Performance Minerals Additives Market

- Imerys S.A.

- Minerals Technologies Inc.

- Omya AG

- BASF SE

- LKAB Minerals

- EP Minerals

- GLC Minerals, LLC

- The Chemours Company

- Sibelco Group

- KaMin LLC

- Dicalite Management Group, Inc

- Hoffmann Mineral GmbH

- Quarzwerke Group

- Nordkalk Corporation

Frequently Asked Questions

The market is projected to reach US$ 32.8 Bn in 2026 and US$ 47.4 Bn by 2033, expanding at a CAGR of 5.4% during the forecast period.

Light-weighting trends in automotive plastics and infrastructure investments in construction, supported by functional benefits of talc and kaolin fillers, remain the core demand drivers.

Calcium Carbonate leads with approximately 42% share, driven by its high production volume, cost efficiency, and versatility across plastics, paints, and construction applications.

North America maintains leadership through strong domestic production, regulatory alignment, and innovation in sustainable mineral solutions.

Energy-transition applications, including thermal management and battery materials, offer the highest future potential through premium, sustainable mineral innovations.

Leading companies include Imerys S.A., Minerals Technologies Inc., Omya AG, BASF SE, LKAB Minerals, and others profiled for their global reach and technical expertise.