- Medical Devices

- Overbed Table Market

Overbed Table Market Size, Share, and Growth Forecast, 2026 - 2033

Overbed Table Market by Product Type (Adjustable, Fixed, Rolling), Distribution (Offline, Online), End-user (Hospitals, Homecare, Others), and Regional Analysis 2026 – 2033

Overbed Table Market Size and Trends Analysis

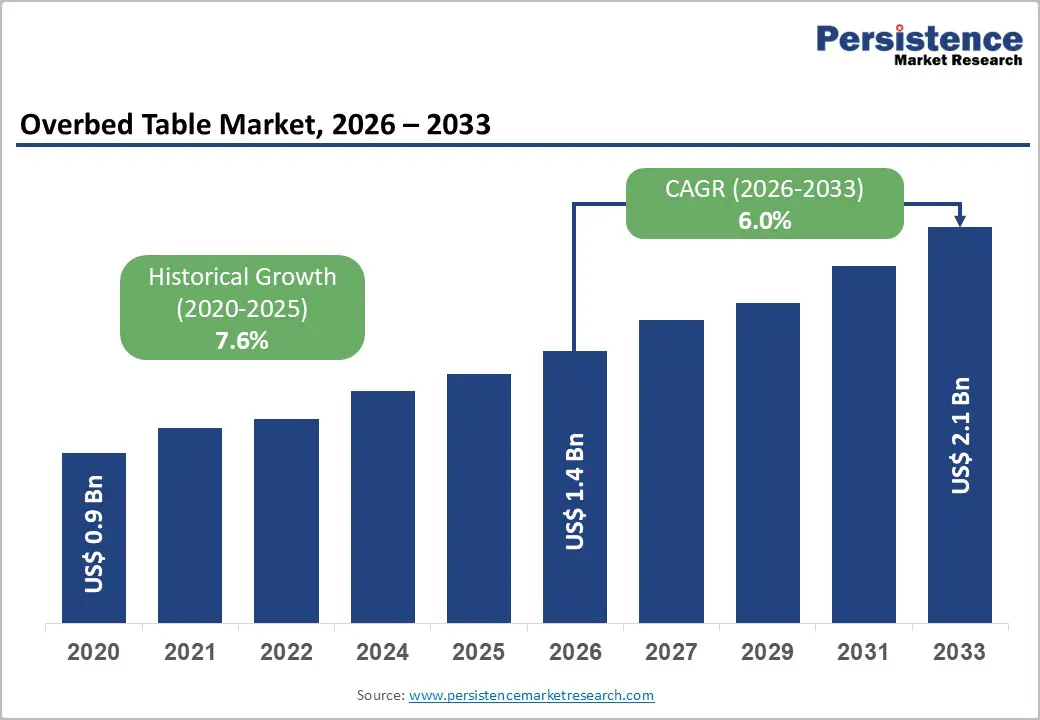

The global overbed table market size is likely to be valued at US$1.4 billion in 2026 and is expected to reach US$2.1 billion by 2033, growing at a CAGR of 6.0% during the forecast period between 2026 and 2033, driven by the aging global population, increasing prevalence of chronic diseases, and the accelerating adoption of home-based care solutions as healthcare systems transition toward cost-effective, patient-centric models. Technological advancements, including height-adjustable mechanisms, antimicrobial surfaces, and smart integrated features, are further enhancing product appeal across diverse healthcare settings. The proliferation of e-commerce distribution channels and the growing focus on ergonomic design standards are broadening market accessibility and creating new revenue opportunities for manufacturers across both developed and emerging economies.

Key Industry Highlights:

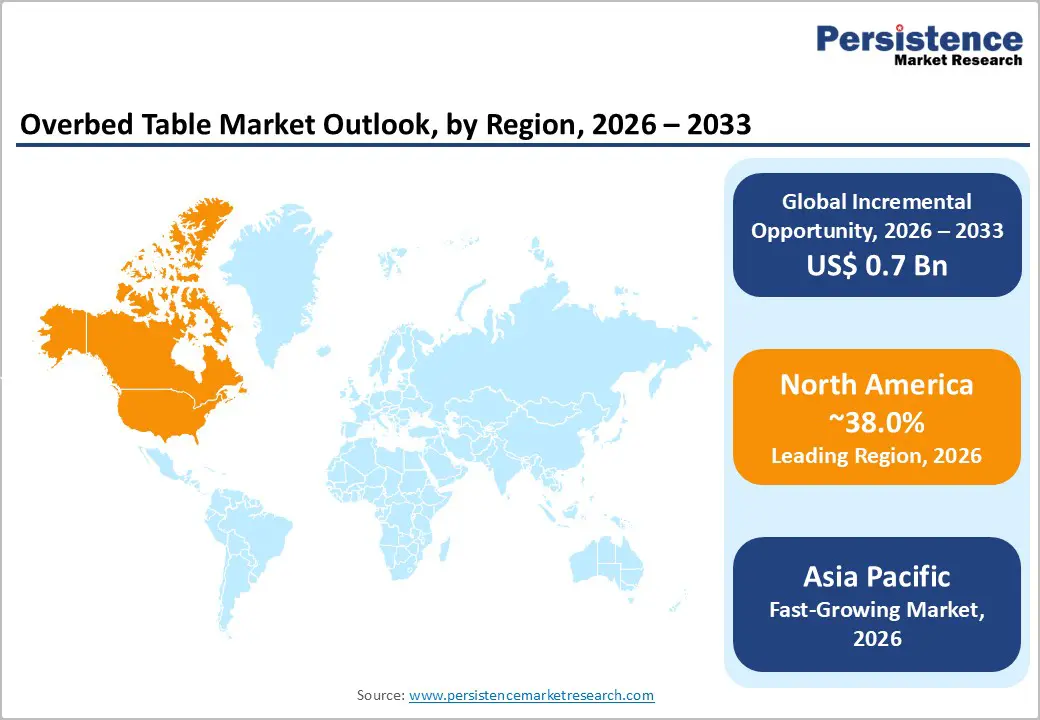

- Leading Market Region: North America is projected to remain the leading region, accounting for approximately 38% share in 2026, supported by advanced healthcare infrastructure, high capital intensity, and mature homecare delivery systems.

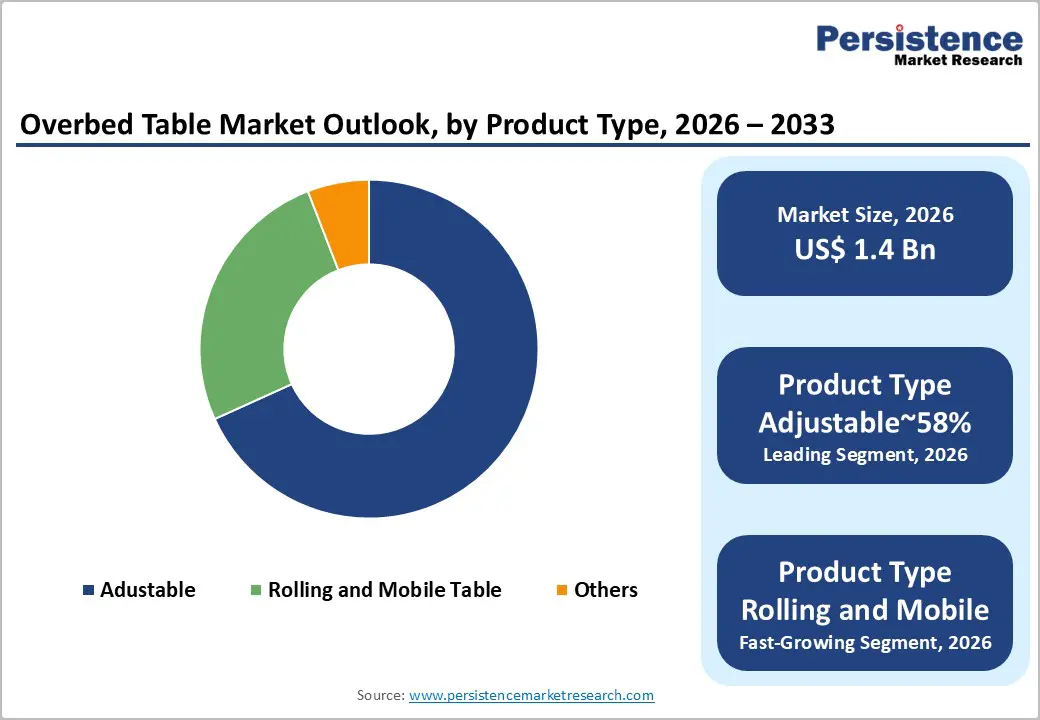

- Leading Product Type: Adjustable overbed tables are expected to lead with 55% share, driven by regulatory compliance, institutional adoption, pneumatic/hydraulic efficiency, and IoT-enabled smart features.

- Leading End-user: Hospitals are projected to lead with 52% share, anchored by acute care demands, regulatory mandates, EHR integration, and high daily usage of clinically optimized tables.

- Key Industry Developments: In May 2023, VieMed acquired Home Medical Products to expand geographically and diversify into mobility, wound care, and complementary equipment.

| Key Insights | Details |

|---|---|

| Overbed Table Market Size (2026E) | US$1.4 Bn |

| Market Value Forecast (2033F) | US$ 2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Demographic Shift

The overbed table market is structurally driven by the accelerating geriatric population, which intensifies demand for functional and ergonomic patient-support solutions. As the global population aged 60 and above approaches 2.1 billion by 2050 (WHO), the prevalence of chronic conditions such as osteoarthritis and cardiovascular disease increases prolonged bed dependency, directly reinforcing the adoption of overbed tables. Healthcare providers and homecare systems prioritize adjustable, multi-acuity furniture that facilitates critical activities of daily living, including feeding, medication management, and personal care, establishing these products as indispensable within patient mobility frameworks.

Adjustable and ergonomically engineered tables dominate the market, as they effectively mitigate physical limitations associated with aging while supporting clinical workflow efficiency. The demographic-driven requirement for accessible, multifunctional furniture sustains volume growth and revenue stability across institutional and residential segments. Market participants leverage these structural dynamics to integrate design innovation, enhance ergonomic functionality, and strengthen competitive positioning, ensuring the segment remains strategically significant within the broader patient care equipment landscape.

Regulatory and Cost-Induced Market Constraints

Complex regulatory frameworks and compliance burdens impose a decisive structural limitation on the medical furniture market, systematically inflating operational costs and constraining innovation. High compliance thresholds disproportionately affect SMEs, compelling many firms to maintain minimal operational scale to avoid regulatory scrutiny, which suppresses the development of advanced patient-centric equipment such as motorized or antimicrobial overbed tables. These structural pressures elevate product pricing, restrict adoption of technologically enhanced solutions, and redirect procurement toward lower-cost, basic alternatives, effectively decoupling functional capability from market penetration. The combined effect of regulatory rigidity and cost escalation directly undermines revenue growth, margin expansion, and long-term strategic positioning for manufacturers operating across institutional and homecare segments.

In the Indian context, the Economic Survey 2024–25 underscores the urgency of regulatory rationalization to unlock market potential. State-level deregulation and streamlined compliance are essential to reduce operational expenditure and incentivize investment in advanced infrastructure. Current budgetary limitations and cost-sensitive procurement frameworks constrain the adoption of high-functionality overbed tables, reflecting a broader global pattern in which value-based healthcare models prioritize expenditure efficiency over integration of premium clinical equipment.

Smart Furniture Integration and Technology-Enabled Patient Care

The overbed table market is increasingly shaped by the integration of artificial intelligence, IoT connectivity, and real-time analytics, which establish functional and operational prerequisites rather than optional enhancements. Furniture equipped with pressure sensors, weight distribution monitoring, and patient positioning algorithms provides quantifiable clinical insights, directly informing care protocols and reducing staff workload. The adoption of such solutions is driven by regulatory expectations for outcome-oriented care and institutional priorities for operational efficiency, positioning technology-enabled tables as a structural requirement within modern patient management frameworks.

From a market perspective, manufacturers capitalize on this functional integration through structured revenue mechanisms, including software licensing, data analytics, and maintenance contracts, reinforcing long-term strategic positioning and predictable cash flow. Telemedicine compatibility and embedded device infrastructure address the increasing reliance on remote monitoring systems, ensuring that technologically advanced tables maintain relevance across institutional and homecare segments. Overall, market adoption aligns with systemic requirements for connectivity, data-driven decision-making, and patient-centric operational efficiency rather than discretionary upgrade cycles.

Category–wise Analysis

Product Type Insights

Adjustable overbed tables are expected to remain the leading product type, holding approximately 55% of the market share in 2026, supported by regulatory compliance, institutional adoption, and ergonomic superiority. This dominance is likely to continue as pneumatic and hydraulic systems enhance caregiver efficiency and patient independence, while maintaining adherence to the FDA, OSHA, and ISO:13485 safety standards. Industrial trends indicate further IoT-enabled integration, with smart tables expected to feature charging ports, ambient documentation sensors, and digital monitoring for clinical workflows. Polymer-based surfaces are projected to strengthen infection control and align with ESG directives across Europe and North America. Split-top designs, exemplified by Godrej Arize, are anticipated to allow multitasking for patients, while Stryker, Hill-Rom, and Wellsure are likely to sustain reliability and reduce maintenance risks. Supply chain consolidation by major players is expected to shorten lead times and reinforce strategic positioning in hospitals and long-term care facilities.

Rolling and mobile overbed tables are anticipated to represent the fastest-growing product type, driven by rising homecare demand, flexible patient environments, and outpatient surgery expansion. Adoption is likely to accelerate as lightweight carbon-fiber and reinforced polymer frames facilitate mobility, while advanced caster systems with automatic braking improve safety and stability. Smart integration of wireless charging, tablet holders, and tool-free assembly, as seen in Stryker Glide-Sensing and Hill-Rom Auto-Leveling models, is expected to optimize clinician workflows and patient engagement. IEC 60601-1-11 standards and infection-control protocols are projected to shape design, requiring stability on inclined surfaces and fully enclosed, cleanable wheels. Biophilic finishes, low-profile bases, and digital-ready interfaces are likely to enhance comfort and operational efficiency. Localized caster production and offset-gravity engineering are anticipated to further expand adoption across homecare, maternity, psychiatric, and small-footprint hospital settings.

End-user Insights

Hospitals are expected to remain the leading end-user segment, holding approximately 52% of the overbed table market share, supported by acute care demands, regulatory mandates, and high daily usage. This dominance is likely to continue as hospitals standardize on pneumatic lift systems, integrate tables with electronic health records (EHR), and adopt no-seam, antimicrobial polymer designs to enhance hygiene and reduce staff injury risks. Bariatric and ICU-specific tables are projected to further reinforce adoption, addressing rising patient weight requirements and critical care needs. Leasing and rental models are anticipated to expand, enabling access to smart, durable tables while minimizing capital expenditure. Brands such as Stryker (Hill-Rom), Invacare, Midmark, and Godrej Interio are expected to maintain leadership by offering clinically optimized, robust furniture that meets ISO 13485, OSHA, and infection-control standards. Supply chain rationalization and smart integration are likely to sustain operational predictability and reinforce strategic positioning across hospital networks.

Homecare settings are anticipated to represent the fastest-growing end-user segment, driven by the shift toward home-based recovery, cost efficiency, and technological enablement. Adoption is likely to accelerate as e-commerce distribution, tool-free assembly, and C-shaped base designs facilitate usability in small residential spaces. Multi-functional, aesthetically integrated tables with USB charging, pneumatic adjustments, and tilting tops are projected to enhance patient independence and comfort, particularly for geriatric users. Regulatory standards emphasizing fall prevention and product safety are expected to shape design and durability, while reimbursement programs incentivize consumer adoption. Brands such as Drive DeVilbiss, Invacare, and Medline are anticipated to expand their presence by offering durable, intuitive tables that align with homecare requirements. Overall, the segment is projected to grow rapidly as healthcare delivery continues shifting from hospitals to patient residences.

Regional Insights

North America Overbed Table Market Trends

North America is expected to maintain its position as the leading region in the overbed table market, accounting for approximately 38% of total revenue in 2026, driven by a mature healthcare infrastructure, widespread adoption of advanced technologies, and a substantial aging population. The region is likely to continue benefiting from strong reimbursement policies under Medicare and private insurance, which incentivize hospitals and homecare providers to acquire premium, feature-rich overbed tables. Rising obesity rates are anticipated to further push demand for standardized bariatric models across hospital wards. Occupational health standards and clinician ergonomics are expected to sustain the adoption of pneumatic and hydraulic systems that reduce nurse fatigue.

Industrial trends are anticipated to focus on smart, IoT-enabled tables that integrate with hospital management systems, track usage metrics, and facilitate remote patient monitoring. The "Hospital-at-Home" model is likely to drive increased demand for portable, home-compatible units, while antimicrobial surfaces and customizable aesthetics are expected to become standard in both hospital and residential settings. Regulatory oversight, including FDA Class I/II device requirements, Joint Commission accreditation, and ADA compliance, is expected to continue shaping product design and market access. Leading brands such as Stryker, Invacare, Drive DeVilbiss, and Leggett & Platt are anticipated to consolidate their positions through innovation, specialized distribution, and integration of smart technologies, reinforcing North America’s market leadership.

Europe Overbed Table Market Trends

Europe remains the second-largest overbed table market, supported by comprehensive public healthcare systems and advanced aging demographics. Demand is shaped by stringent regulatory oversight under CE marking, ISO standards, and MDR compliance, which elevate safety, infection control, and ergonomic requirements across institutional care settings. Germany anchors regional demand through extensive nursing home infrastructure and design-led procurement, while the U.K., France, and Spain contribute stable volumes through long-term care expansion and healthcare modernization initiatives.

The region is characterized by regulatory harmonization and patient-centered care priorities, which favor durable, antimicrobial, and ergonomically optimized furniture solutions. Sustainability directives under EU policy frameworks further influence material selection and manufacturing practices. Europe is therefore positioned as a mature, compliance-driven market, where adoption is guided by regulatory certainty, quality benchmarks, and incremental innovation rather than rapid capacity expansion.

Asia Pacific Overbed Table Market Trends

The Asia Pacific (APAC) region is expected to remain the fastest-growing market for overbed tables, driven by expanding healthcare infrastructure, a rapidly aging population in Japan and South Korea, and rising medical tourism across India, Thailand, and Malaysia. The region is anticipated to continue benefiting from significant local manufacturing upgrades in India and China, where brands such as Godrej Interio and United Poly have scaled production of pneumatic and mechanical tables, reducing costs by up to 30% compared with imports. Public healthcare expenditure in China and India is likely to create a strong baseline demand for both manual and mechanically adjustable tables, while the rise of home nursing and e-commerce platforms is expected to accelerate the retail segment.

Industrial trends in APAC are anticipated to emphasize frugal automation, providing 80% of the functionality of high-end smart tables at a fraction of the cost, along with space-saving collapsible designs suited to dense urban living. Sustainability initiatives are likely to drive the use of bamboo laminates and eco-friendly polymers, while stricter medical device regulations from CDSCO, NMPA, and BIS standards are expected to consolidate the market toward organized manufacturers. Leading regional players, including Godrej Interio, Paramount Bed, United Poly, and Jiangsu Saiik, are anticipated to maintain strong positions, catering simultaneously to premium medical tourism segments and large-scale public hospital projects, reinforcing APAC’s rapid growth trajectory.

Competitive Landscape

The global overbed table market is moderately consolidated, led by established manufacturers such as Hill-Rom Holdings, Stryker Corporation, and Invacare, which collectively exert strong influence through scale, brand recognition, and long-standing relationships with healthcare providers. These players matter as their global distribution networks, manufacturing efficiency, and broad product portfolios shape purchasing standards across hospitals and long-term care facilities. European specialists, including LINET, Favero Health Projects, and Getinge, maintain strong regional positions and are steadily expanding their international footprint through differentiated design and quality-focused offerings.

Beyond the leading group, the market remains competitive and diverse, with numerous mid-sized and regional manufacturers serving specific geographies or facility types. Competitive positioning centers on product innovation, cost-efficient manufacturing, distribution reach, and customer relationship management. Industry behavior increasingly emphasizes technology integration, sustainability initiatives, and omnichannel distribution, signaling gradual competitive evolution rather than aggressive consolidation.

Key Industry Developments:

- In March 2025, Stryker expanded "Smart Room" connectivity by integrating the ProCuity Bed with compatible furniture.

- In February 2025, Stryker launched the ProCeed Bed System with integrated bedside furniture, enhancing safety, maneuverability, and patient-centric efficiency.

- In April 2024, Arjo showcased Caliant Tables, offering flexible height, durability, and easy maintenance for high-traffic healthcare environments.

- In April 2024, Drive DeVilbiss introduced the SuppliTo twinTop Overbed Table with dual surfaces and a tool-free, stable design for homecare use.

- In March 2024, GCX Medical launched a roll stand and overbed tables with ergonomic, telemedicine-ready features, improving bedside patient care.

Companies Covered in Overbed Table Market

- Hill-Rom Holdings, Inc.

- Stryker Corporation

- Invacare Corporation

- LINET spol. S r.o.

- Favero Health

- Getinge Group

- Knightsbridge Furniture

- Paramount Bed Holdings Co. Ltd.

- Savaria Corporation

- Medline Industries, Inc.

- Arjo AB

- Vallitech Móveis Hospitalares

- A.A. Medical

- IMO Medical

- VieMed

- STIEGELMEYER GmbH & Co.KG

Frequently Asked Questions

The global overbed table market is valued at US$1.4 billion in 2026 and is projected to reach US$2.1 billion by 2033.

Demand is increasing due to rapid population aging, rising prevalence of chronic conditions, and the structural shift toward home-based and patient-centric healthcare delivery models.

The overbed table market is expected to grow at a CAGR of 6.0% between 2026 and 2033, supported by ergonomic innovation and expanding homecare adoption.

Opportunities are emerging through height-adjustable designs, antimicrobial surfaces, IoT-enabled smart furniture, and omnichannel distribution targeting residential users.

Key players include Hill-Rom Holdings, Stryker Corporation, Invacare, LINET, Favero Health Projects, Getinge Group, Paramount Bed, Medline Industries, Arjo AB, and Savaria Corporation.