- Industrial Goods & Service

- O Ring Market

O Ring Market Size, Share, Trends, Growth, Forecasts, 2026 - 2033

O Ring Market By Material Type (EPDM O Ring, Nitrile (NBR) O Ring, PTFE O Ring, Silicone O Ring, Viton O Ring, Metal O Ring, Others), Application (Pneumatic, Hydraulic, Vacuum), Industry (Aerospace & Aviation, Automotive, Chemical & Petrochemical, Oil & Gas, Water & Wastewater Treatment, Electrical & Electronics, Food & Beverages, Medical & Healthcare, Other Industrial), and Regional Analysis from 2026 to 2033

O Ring Market Share and Trends Analysis

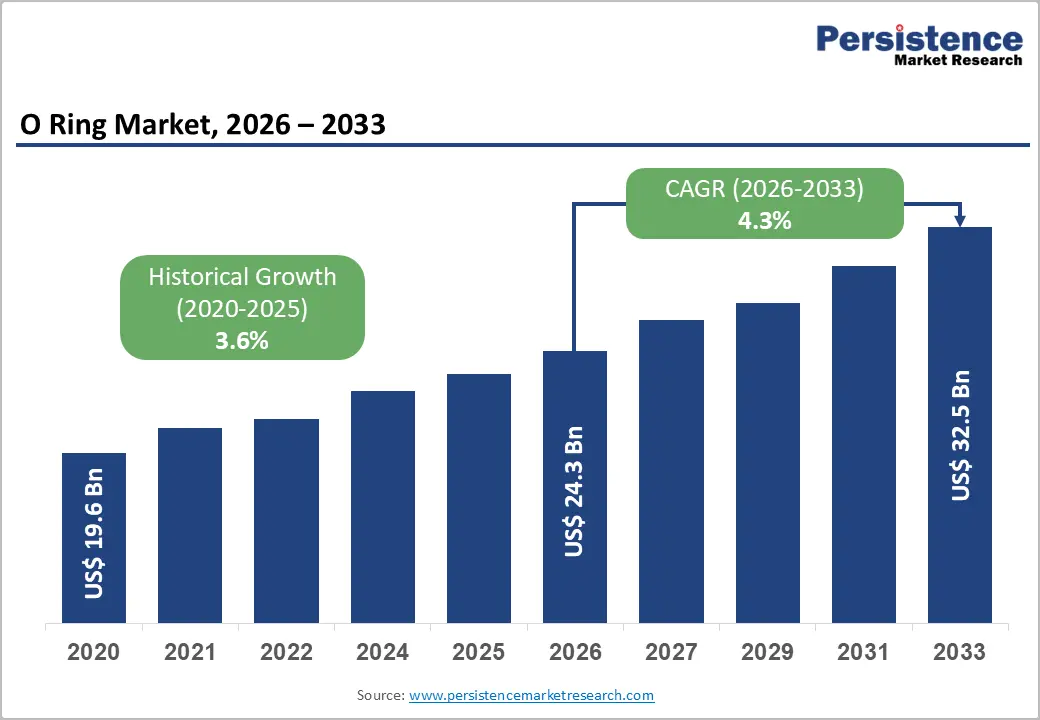

The global O Ring market size anticipated at US$24.3 Billion in 2026 and is projected to reach US$32.5 Billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

Market growth is driven by accelerating automotive electrification requiring advanced EV battery and drivetrain sealing, industrial automation expansion demanding high-performance hydraulic and pneumatic systems, and aerospace growth with aircraft window seals at 7.96% CAGR. Advanced elastomers, self-lubricating rubbers, smart seals, and polymer coatings expand applications, enhance reliability, and establish O-rings as essential sealing infrastructure across industries, transportation, and renewable energy globally.

Key Industry Highlights:

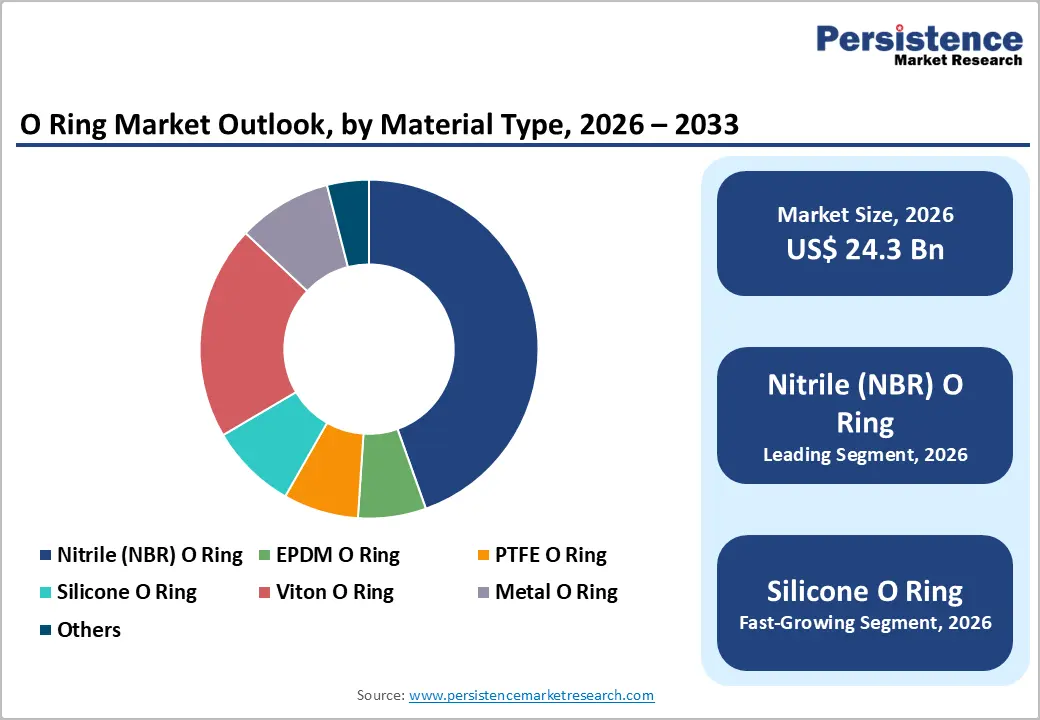

- Nitrile Dominance with Silicone Growth: Nitrile (NBR) maintains 45% market share as cost-effective standard material; silicone O-rings accelerate at 5% CAGR driven by extreme temperature and biocompatibility applications.

- Hydraulic System Leadership with Vacuum Growth: Hydraulic applications command 49% of O-ring demand providing stable revenue foundation; vacuum sealing expands at 4.2% CAGR from semiconductor and laboratory equipment demand.

- Automotive Dominance with Food & Beverage Acceleration: Automotive sector maintains 40% end-use share reflecting vehicle production scale and replacement frequency; food & beverage segment grows fastest at 4.8% CAGR driven by FDA-compliance specialization.

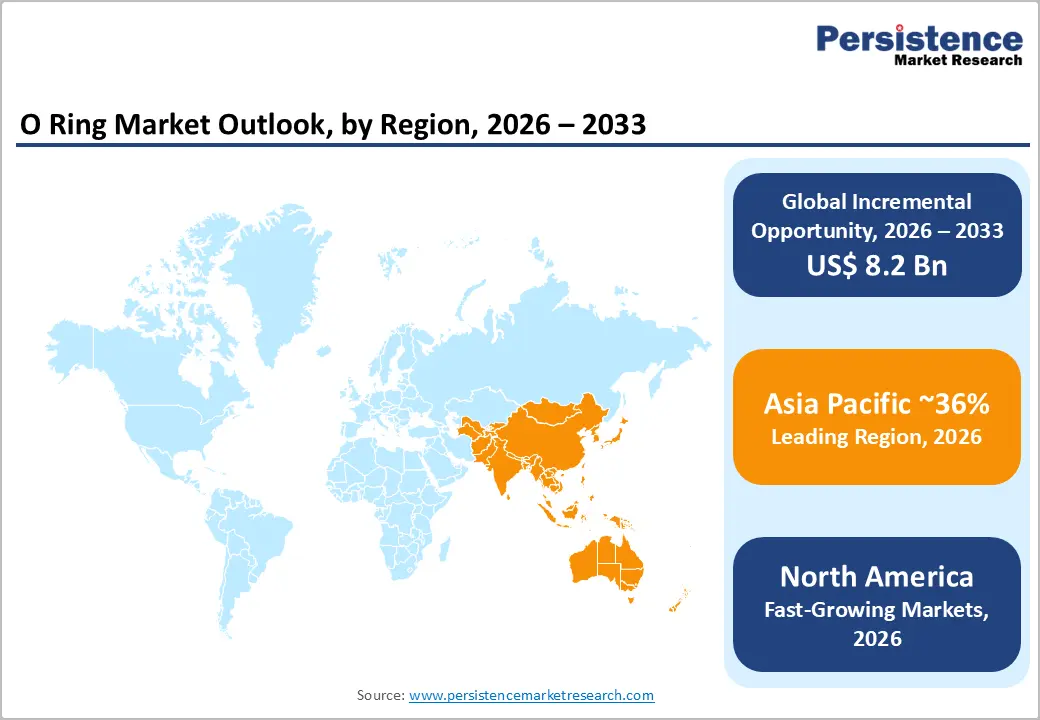

- Asia Pacific Regional Leadership: Asia Pacific dominates with ~36% global market share and 4.6% CAGR; Vietnam facility launch (Trelleborg) and China automotive manufacturing establish regional manufacturing concentration.

- Technology-Driven Performance Innovation: Self-lubricating rubber reducing friction 40% (NOK-ENEOS May 2024), smart seals enabling 40%+ preventive downtime reduction, and aerospace-specialized aircraft window seals (7.96% CAGR) establish competitive differentiation ecosystems.

| Key Insights | Details |

|---|---|

| O Ring Market Size (2026E) | US$ 24.3 billion |

| Market Value Forecast (2033F) | US$ 32.5 billion |

| Projected Growth CAGR (2026 - 2033) | 4.3% |

| Historical Market Growth (2020 - 2025) | 3.6% |

Market Dynamics Analysis

Drivers - Electric Vehicle Adoption and Advanced Automotive Sealing Requirements

The automotive industry accounts for nearly 40% of global O-ring end-use demand and exhibits the strongest growth momentum, driven by electric vehicle proliferation and accelerating electrification shifts. Global EV sales reached 13.6 million units in 2023, representing 18% of new vehicle sales, with penetration projected to approach 50% by 2035. EV powertrains introduce sealing requirements fundamentally different from internal combustion engines, spanning battery cooling systems, high-voltage electrical connections, thermal management circuits, and electric motor drive units, particularly e-axles. These applications demand O-rings with superior thermal stability, electrical insulation, chemical resistance, and low-friction performance. Reflecting this transition, NOK Corporation and ENEOS Corporation jointly developed self-lubricating rubber in May 2024, reducing friction by up to 40% while maintaining sealing integrity in low-viscosity lubricants critical for motor efficiency.

Aerospace Expansion and Aircraft Window Seal Specialization

The aerospace sector demonstrates an exceptional growth trajectory, expanding at a 7.6% CAGR through 2033, with the aircraft O-ring market projected to reach US$4.16 billion by that year. Post-pandemic commercial aviation recovery, fleet modernization, rising air travel demand across Asia Pacific, and aircraft programs including Boeing 737MAX and Airbus A350 production drive sustained manufacturing volumes. Aircraft window seals represent the highest-value application, with Trelleborg Sealing Solutions strengthening leadership through acquisition of major aerospace facilities, including its Seattle aerospace manufacturing campus in 2023, establishing itself as the largest global supplier of aircraft window seals. Aerospace O-rings must perform under extreme conditions, tolerating cabin pressurization up to 8.5 PSI, temperature ranges from -55°C to +200°C, high-altitude ozone exposure, and rigorous AS9100 safety certifications. These requirements enable premium pricing and investment by sealing manufacturers.

Restraint - Raw Material Supply Volatility and Elastomer Cost Fluctuation

O ring manufacturing depends predominantly on crude oil-derived elastomers including nitrile (NBR) comprising 45% market share, EPDM, and specialized polymers including fluorocarbon (FKM) and perfluoroelastomer (FFKM). Crude oil price volatility directly impacts elastomer feedstock costs, creating margin compression during commodity price escalations. Supply chain disruptions exemplified by pandemic-related petrochemical facility shutdowns and subsequent logistics constraints have created extended lead times (6-12 months in specialized applications) and raw material cost inflation 15-25% above historical norms. Additionally, manufacturing capacity constraints in advanced elastomer production (particularly FFKM perfluoroelastomers required for extreme-temperature aerospace applications) limit production velocity and restrict market expansion, particularly in emerging markets with nascent supply chain infrastructure.

Quality Variability Perception and Supply Chain Fragmentation

The O ring market includes numerous regional manufacturers with inconsistent quality control standards, creating a perception risk that lower-cost alternatives may not deliver performance specifications matching premium suppliers. Fragmented manufacturing across multiple facilities, each with distinct production methodologies, material testing protocols, and dimension tolerance management creates standardization challenges, particularly critical for aerospace and high-pressure industrial applications, where seal failure can cause catastrophic equipment damage. This fragmentation particularly affects emerging market adoption where cost-sensitive customers may encounter counterfeit or non-compliant O ring products, damaging overall market credibility.

Opportunity - Hydrogen Technology and Fuel Cell System Sealing

Hydrogen technology emergence as clean energy alternative establishes substantial new market opportunity for specialized O ring solutions addressing hydrogen's unique physical properties. Hydrogen molecules demonstrate permeation characteristics requiring advanced seal materials (particularly PTFE and specialized FFKM compounds), preventing gas escape under high-pressure storage conditions. Global hydrogen capacity is projected to reach 10 million tonnes annually by 2030 (versus current 70 million tonnes), driven by industrial decarbonization objectives and fuel cell vehicle adoption expansion. This emerging opportunity conservatively estimates US$150-250 million incremental O ring market value through 2033 as hydrogen infrastructure scales from pilot programs to commercial deployment. Strategic positioning in hydrogen sealing technology establishes a long-term differentiation advantage for manufacturers investing early in material development and application engineering.

Food & Beverage Industry Expansion and FDA Compliance Specialization

Food and beverage represents the fastest-growing O-ring end-use segment, expanding at a 4.8% CAGR driven by rising food processing automation, stringent sanitary sealing needs, and increasingly strict global food safety regulations. Demand is concentrated around FDA-compliant O-ring materials that prevent chemical leaching and contamination, creating a specialized, high-value segment commanding price premiums of 40-60% over commodity alternatives. The customer base spans small regional food processors to multinational beverage producers, resulting in market fragmentation that favors specialized suppliers with localized regulatory expertise and distribution reach. Incremental market opportunity is conservatively estimated at around US$200-350 million through 2033, supported by rapid modernization of food processing infrastructure across developing economies and increasing adoption of hygienic, high-performance sealing solutions across industrial processing environments globally worldwide.

Category-wise Analysis

Material Type Insights

Nitrile rubber (NBR) O-rings dominate the market with a 45% share, driven by cost-effectiveness, wide operating temperatures (-40°C to +100°C), and excellent resistance to mineral oils, fuels, and hydraulic fluids. With over 50 years of industrial standardization, extensive manufacturer expertise, and commodity pricing, NBR enables broad adoption across price-sensitive segments. Its simple formulation and scalable manufacturing support high global production volumes, meeting industrial automation, automotive, and general industrial demand. This combination of performance, reliability, and affordability reinforces NBR’s sustained market leadership.

Silicone O-rings grow at a 5% CAGR due to superior temperature tolerance (-55°C to +200°C), ozone and UV resistance, and biocompatibility. FDA-compliant for food and medical applications, this premium segment commands 3-4 times the cost of NBR, attracting manufacturers focused on high-performance, differentiation-driven applications in aerospace, medical devices, and food processing.

Application Insights

Hydraulic applications account for 49% of O-ring demand, reflecting the widespread use of fluid power systems in industrial machinery, construction equipment, aviation, and mobile platforms. High system pressures, often exceeding 5,000 PSI in specialized applications, require durable, reliable, and leak-proof sealing solutions. Continuous advancements in hydraulic system sophistication, including tighter tolerances and higher pressure capacities, sustain demand for premium O-rings capable of withstanding mechanical stress, fluid compatibility challenges, and extended operational cycles, reinforcing hydraulic applications as the dominant segment in global O-ring consumption.

Vacuum sealing applications grow at a 4.2% CAGR, driven by semiconductor fabrication, laboratory equipment, and specialized industrial processes requiring hermetic containment. O-rings for these environments must resist outgassing and maintain integrity across pressure differentials, ensuring performance consistency in ultra-low pressure conditions while preventing contamination and preserving vacuum quality.

Industry Insights

Automotive applications account for 40% of O-ring end-use demand, driven by high vehicle production volumes, extensive component counts, and critical sealing requirements across engines, transmissions, braking systems, fuel handling, air conditioning, and hydraulic circuits. This segment benefits from structured OEM procurement networks, standardized part specifications, and frequent replacement cycles in aftermarket maintenance. The combination of large-scale production, recurring service demand, and stringent performance standards ensures sustained O-ring consumption, reinforcing automotive as the dominant end-use sector globally while creating opportunities for manufacturers to supply both OEM and aftermarket channels.

The food and beverage segment grows at a 4.8% CAGR, fueled by processing automation, stringent safety regulations, and FDA-compliant material requirements. Premium pricing attracts specialized suppliers focusing on hygiene, material certifications, and regulatory documentation, enabling safe food contact and creating a differentiated market segment with high-value sealing solutions for global processing operations.

Regional Insights

North America O Ring Market Trends

North America commands approximately 20-22% global O ring market value while demonstrating 4.1% CAGR, reflecting mature market infrastructure combined with aerospace industry concentration and advanced manufacturing capabilities. The United States market specifically, valued at approximately US$5.2-5.8 billion in 2025, drives regional growth through aerospace manufacturing hub status, established automotive supply base, and industrial equipment specialization. Canada contributes 8-10% of regional value, concentrated in automotive component manufacturing and equipment rental segments.

North America's regulatory framework emphasizes safety, environmental protection, and product performance standardization, establishing a foundation for advanced sealing technology investment. NASA and DOD specifications establish extraordinarily stringent sealing requirements for aerospace applications, creating premium-priced markets driving manufacturer innovation. The region hosts approximately 35-40% of global O ring OEM headquarters and significant R&D investment, establishing innovation concentration supporting rapid technology deployment and market differentiation.

Europe O Ring Market Trends

Europe maintains approximately 26% of global O ring market value, reflecting mature manufacturing infrastructure, an established industrial base, and strong automotive heritage. Germany specifically represents 35-40% of European market value through automotive supplier concentration and industrial equipment manufacturing dominance. United Kingdom, France, and Spain collectively represent 25-30% of regional value, with concentration in aerospace, pharmaceutical manufacturing, and food processing applications.

European Union environmental directives emphasize circular economy principles and material sustainability, establishing a competitive advantage for manufacturers offering recyclable materials and eco-friendly production processes. ISO/international standardization originating from European technical leadership establishes quality baselines influencing global O ring specifications. Regional regulatory emphasis on food safety and medical device classification drives premium-priced specialized material segments where margin expansion sustains research investment.

Asia Pacific O Ring Market Trends

Asia Pacific establishes overwhelming market dominance with approximately 36% global market share while demonstrating 4.6% CAGR highest growth trajectory among major regions. China commands 18-22% of global market through automotive manufacturing dominance (28 million vehicles annually), electric vehicle production concentration, and industrial equipment specialization. India represents emerging opportunity through 2033, driven by infrastructure expansion, manufacturing automation acceleration, and automotive industry growth. Japan maintains premium market positioning (3-4% global share) through technology leadership, precision manufacturing capabilities, and EV battery seal specialization.

Asia Pacific hosts approximately 60-65% of global O ring manufacturing capacity, establishing structural cost leadership through labor efficiency, vertical integration, and raw material proximity. Regional manufacturing expansion particularly Trelleborg's Vietnam facility launch and emerging domestic manufacturers is enabling supply chain diversification reducing China-dependent sourcing constraints. Government manufacturing incentives including India's "Make in India" program and Vietnam's preferential trade status are attracting foreign direct investment in sealing solution manufacturing.

Competitive Landscape

Market leaders differentiate through technology innovation, application specialization, and strong OEM relationships. Parker, Freudenberg, and Trelleborg focus on aerospace and medical segments, while NOK excels in EV battery sealing and self-lubricating materials. Cost-competitive Asian manufacturers capture commodity markets, with overall trends including application-specific materials, smart sensor integration for predictive maintenance, certification acquisition, and geographic manufacturing expansion for supply chain resilience.

Strategic Developments

- In May 2024, NOK Corporation and ENEOS Corporation jointly developed a self-lubricating rubber reducing sealing friction by up to 40%, targeting EV motor drive components (e-Axles) and future robotics/hydrogen systems, enhancing energy efficiency, material differentiation, and premium positioning in high-performance applications.

- In December 2023, Trelleborg Sealing Solutions launched its first Southeast Asia manufacturing facility in Vietnam, producing O-rings and custom molded components in FKM and HNBR, achieving cost advantages, supply chain diversification, and proximity to regional automotive OEM platforms for strategic market penetration.

- In October 2025, Trelleborg acquired Masterseals, a specialist in energy sector sealing, expanding its portfolio into renewable energy and oil & gas applications, enhancing high-performance sealing capabilities, differentiation, and positioning in emerging energy transition markets through technology-driven strategic M&A.

Companies Covered in O Ring Market

- Parker Hannifin Corporation

- Freudenberg Sealing Technologies

- Trelleborg Sealing Solutions

- NOK Corporation

- Eaton Corporation

- SKF Group

- Timken Company

- ENEOS Corporation

- Applied Industrial Technologies

- Saint-Gobain

- Hutchinson Group

- Warex

- Quaker Houghton

- SPP Pumps Limited

- Hydraulics International

Frequently Asked Questions

The global O Ring Market was valued at US$19.6 Billion in 2020, reached US$24.3 Billion in 2026, and is projected to reach US$32.5 Billion by 2033.

Market growth is fueled by EV battery and thermal sealing needs, aerospace expansion, industrial automation, renewable energy infrastructure, advanced elastomer innovations, smart predictive seals, and stringent food & water safety regulations.

The O Ring Market is projected to grow at a CAGR of 4.3% between 2026 and 2033.

High-value opportunities exist in hydrogen fuel cell sealing, FDA-compliant food & beverage applications, Asia Pacific localization, aerospace window seals, EV battery systems, and sensor-enabled smart seals.

The market is led by Parker Hannifin, Freudenberg, Trelleborg, and NOK Corporation, supported by players such as Eaton, SKF, Timken, Saint-Gobain, Hutchinson, and fast-growing Asian manufacturers.