- Medical Devices

- North America Orthokeratology Market

North America Orthokeratology Market Size, Share, and Growth Forecast, 2026 – 2033

North America Orthokeratology Market by Indication (Myopia, Astigmatism, Others), Product Type (Overnight lenses, Day-time lenses), Material (Fluorosilicone Acrylate, Silicone Acrylate), and Country Analysis 2026 – 2033

North America Orthokeratology Market Size and Trends Analysis

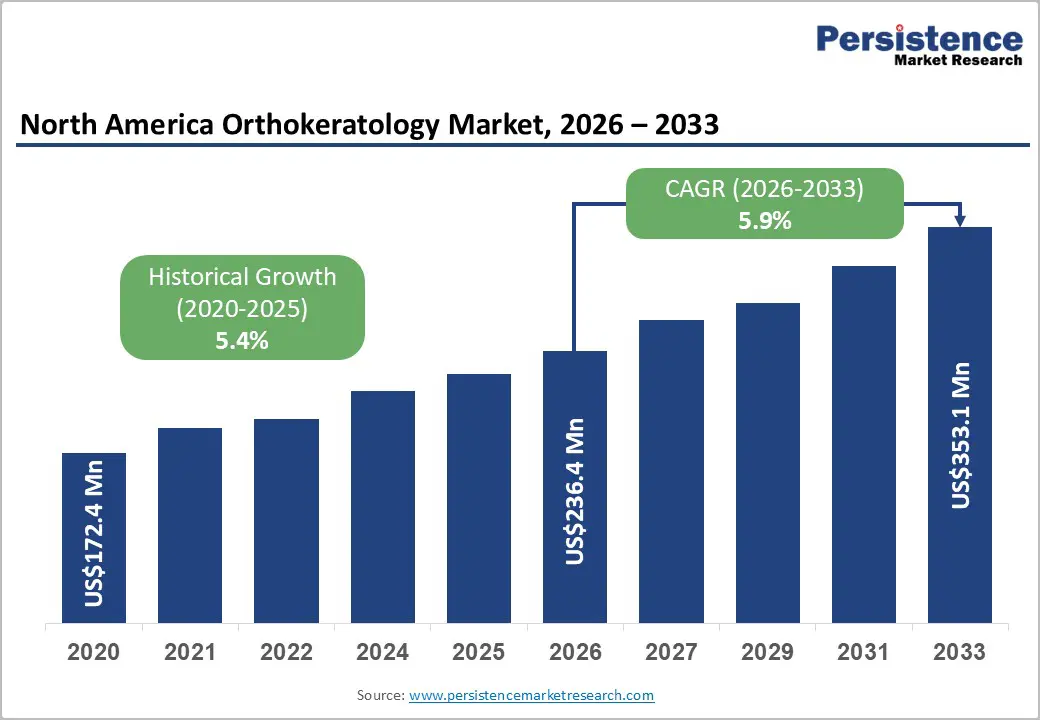

The North America orthokeratology market size is likely to be valued at US$236.4 million in 2026 and is expected to reach US$353.1 million by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033. Growth stems from rising myopia prevalence linked to increased screen time of children exceeding AAP (American Academy of Pediatrics)-recommended limits, driving demand for non-surgical correction.

Advancements in oxygen-permeable lens materials enhance comfort and efficacy, supporting myopia control in pediatrics. Favorable reimbursement and optometric awareness further accelerate adoption. Furthermore, advancements in hyper-Dk gas-permeable materials and cloud-based topography fitting systems have significantly lowered the clinical barrier for entry, allowing more optometrists to offer Ortho-K as a standard of care.

Key Industry Highlights:

- Leading Country: The U.S. is projected to lead due to its established optometry infrastructure, strong practitioner adoption of myopia management protocols, and high pediatric orthokeratology demand, accounting for approximately 80% share in 2026, supported by advanced digital fitting technologies, strong consumer awareness, and a mature clinical ecosystem.

- Fastest-growing Country: Canada is anticipated to grow fastest due to urban population growth, with rising myopia prevalence, evolving medical optometry practices, and adoption of tele-fitting and cloud-based corneal mapping technologies across geographically dispersed regions.

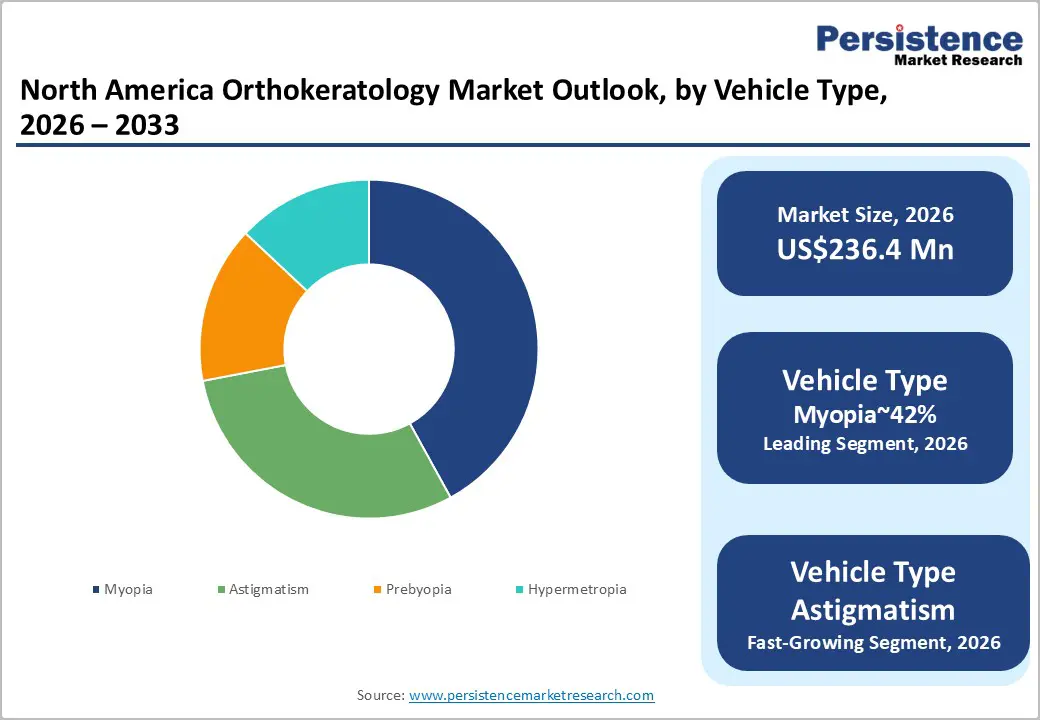

- Leading Indication: Myopia is expected to lead accounting with approximately 42% share in 2026, through strong clinical validation for pediatric myopia control, widespread adoption in structured myopia management programs, and continuous technological improvements in orthokeratology lens materials and corneal mapping systems.

- Leading Product Type: Overnight Ortho-K lenses are projected to dominate for their convenience of overnight wear, ability to deliver clear daytime vision without spectacles, and strong clinical adoption in pediatric myopia management programs, holding approximately 95% share in 2026.

| Key Insights | Details |

|---|---|

| North America Orthokeratology Market Size (2026E) | US$236.4 Mn |

| Market Value Forecast (2033F) | US$353.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Advanced Lens Materials and Digital Fitting Technologies Expanding Orthokeratology Adoption

Continuous innovation in contact lens material engineering is strengthening safety perceptions surrounding orthokeratology therapy. High oxygen permeability fluorosilicone acrylate materials significantly improve corneal oxygen transmission during overnight lens wear. These material advancements mitigate historical concerns regarding corneal hypoxia and epithelial stress under extended usage. Enhanced wettability and surface durability further stabilize tear film interactions, improving overnight comfort for pediatric users. Improved physiological compatibility increases practitioner confidence when prescribing orthokeratology lenses for young myopia patients. Regulatory clearances for advanced material formulations reinforce safety validation across ophthalmic device approval pathways. Such technological progress broadens the clinical eligibility pool for orthokeratology-based vision management approaches. The resulting safety improvements strengthen parental acceptance of overnight corneal reshaping treatments within pediatric eye care.

Parallel digital innovation is transforming orthokeratology fitting workflows across specialized optometry practices. Artificial intelligence-enabled corneal topography platforms deliver precise corneal mapping and predictive lens design recommendations. Cloud-based fitting software reduces manual adjustments and shortens diagnostic chair time during patient consultations. These efficiencies enable practitioners to manage higher patient volumes without compromising clinical precision or treatment outcomes. Integrated digital records also support longitudinal monitoring of corneal response and refractive stability. Streamlined workflows enhance operational productivity within specialty clinics providing orthokeratology services. Technology-driven fitting protocols, therefore, reduce practitioner barriers traditionally associated with complex lens customization. Collectively, these advancements expand service scalability while reinforcing orthokeratology integration into modern myopia management programs.

Rising Pediatric Myopia Burden and Preventive Vision Management Adoption

Escalating pediatric myopia prevalence across North America is intensifying demand for non-surgical refractive management technologies. Lifestyle shifts toward prolonged digital device exposure and limited outdoor activity accelerate early-onset refractive disorders. Pediatric populations increasingly experience progressive axial elongation, prompting clinical concern among ophthalmic and optometric practitioners. Preventive eye care strategies, therefore, gain prominence within pediatric vision management protocols across regional healthcare systems. Orthokeratology lenses offer overnight corneal reshaping that temporarily corrects refractive errors during daytime vision. Such therapeutic positioning encourages early clinical intervention within pediatric ophthalmology and community optometry settings. Growing parental awareness of childhood myopia risks reinforces consistent demand for preventive refractive solutions.

Healthcare providers increasingly transition from episodic refractive correction toward continuous myopia management frameworks. Orthokeratology integrates into longitudinal care pathways where recurring monitoring and lens replacement cycles stabilize revenue. Professional ophthalmology associations increasingly emphasize myopia management education within clinical training and practice guidelines. These developments strengthen practitioner confidence in prescribing orthokeratology lenses for pediatric vision stabilization. Insurance reimbursement dynamics and specialty fitting expertise further differentiate orthokeratology services within optometric practice portfolios. The structural changes collectively reinforce orthokeratology positioning within preventive ophthalmic care delivery models.

Barrier Analysis – High Out-of-Pocket Treatment Costs and Limited Insurance Coverage

Elevated initial treatment costs represent a structural barrier constraining orthokeratology adoption across North America. Orthokeratology therapy requires specialized lens fitting, diagnostic imaging, and practitioner expertise within clinical optometry settings. These service components significantly increase total treatment expenditure compared with conventional spectacles or soft contact lenses. Insurance reimbursement frameworks in the region frequently classify orthokeratology as elective vision correction. This classification restricts financial coverage under standard vision insurance policies across many healthcare plans. Economic sensitivity, therefore, restricts orthokeratology accessibility primarily to higher-income patient demographics.

Recurring maintenance requirements further intensify cost considerations associated with long-term orthokeratology therapy. Periodic lens replacement cycles and routine clinical follow-up visits create continuous financial obligations. These recurring expenditures amplify affordability concerns when household budgets face broader macroeconomic pressures. Patients may discontinue therapy when perceived therapeutic value fails to justify sustained financial commitment. Limited reimbursement integration also reduces incentives for mainstream optometry networks to prioritize orthokeratology services. As a result, adoption remains concentrated within specialty clinics capable of supporting customized lens fitting programs. This uneven service distribution restricts broader penetration across community-level eye care providers. Collectively, these economic constraints slow orthokeratology diffusion despite growing clinical interest in myopia management strategies.

Limited Availability of Specialized Practitioners and Technical Fitting Complexity

Orthokeratology therapy requires specialized clinical expertise supported by advanced corneal imaging and diagnostic infrastructure. Practitioners must interpret detailed corneal topography data to design customized overnight reshaping lens geometries. This technical requirement introduces a steep professional learning curve within routine optometry practice environments. Many general practitioners hesitate to adopt orthokeratology due to training intensity and equipment investment requirements. Corneal topographers and fitting software represent substantial capital expenditure for smaller community clinics. Limited practitioner training capacity, therefore, restricts the number of professionals capable of delivering orthokeratology therapy. This imbalance creates service bottlenecks where clinical supply struggles to match rising pediatric myopia demand. Orthokeratology availability remains concentrated within specialized urban ophthalmic centers possessing advanced diagnostic capabilities.

Operational complexity within orthokeratology fitting protocols further constrains large-scale clinical deployment. Customized lens geometries require iterative adjustments to achieve optimal corneal reshaping outcomes. Initial patient adaptation challenges may create discomfort perceptions during early treatment stages. Such experiences can discourage some patients from continuing therapy despite potential long-term visual benefits. Clinical monitoring protocols also require repeated follow-up consultations to ensure corneal health stability. These procedural demands increase practitioner workload relative to conventional refractive correction methods. Limited specialist distribution therefore restricts access across suburban and rural healthcare environments.

Opportunity Analysis - Expansion of Pediatric Myopia Management Programs

Growing recognition of childhood myopia as a long-term public health concern is expanding opportunities for orthokeratology integration. School-based vision screening initiatives increasingly identify refractive errors at earlier developmental stages. Early diagnosis encourages structured clinical interventions designed to slow myopia progression during critical ocular growth periods. Orthokeratology lenses demonstrate therapeutic relevance within pediatric myopia management frameworks focused on axial elongation control. Clinical research associating overnight corneal reshaping with moderated progression strengthens its credibility among pediatric ophthalmology specialists. Professional medical associations increasingly emphasize early intervention strategies to protect long-term visual health outcomes. Expanding parental awareness further reinforces demand for proactive vision stabilization solutions during childhood development.

Healthcare providers are progressively embedding myopia management protocols into routine pediatric eye care services. Orthokeratology adoption within these programs creates sustained patient engagement across long-term treatment cycles. Pediatric-oriented product design, including simplified packaging and educational materials, supports practitioner consultations with parents. Improved communication tools help clinicians explain therapeutic benefits and long-term vision protection strategies clearly. Manufacturers increasingly collaborate with eye care professionals to develop targeted pediatric education platforms. Collectively, pediatric myopia management integration represents a structurally expanding opportunity within the North America orthokeratology market landscape.

Category–wise Analysis

Indication Insights

Myopia is expected to lead the North America Orthokeratology market, accounting for approximately 42% share in 2026, reflecting its entrenched clinical role in pediatric vision management. Orthokeratology adoption remains anchored by strong clinical validation demonstrating effectiveness in slowing axial elongation among children with progressive nearsightedness. Rising digital device exposure and reduced outdoor activity have accelerated pediatric myopia incidence, strengthening demand for proactive correction strategies.

Eye care professionals increasingly prioritize orthokeratology within structured myopia control programs integrated into pediatric optometry practices. Industry leaders, including Johnson & Johnson Vision Care, CooperVision, and Bausch + Lomb, support this segment through platforms such as Acuvue Abiliti, Paragon CRT, and Vision Shaping Treatment. Continuous advances in fluorosilicone acrylate materials and digital corneal mapping systems further reinforce treatment reliability.

Astigmatism is expected to be the fastest-growing segment, reflecting growing demand for dual refractive correction solutions. Historically, spherical orthokeratology lenses struggled to address higher levels of corneal astigmatism, leaving a large patient population underserved. Recent toric orthokeratology designs now enable precise corneal reshaping while simultaneously managing myopic progression. Manufacturers, including Euclid Systems Corporation, etc., are advancing platforms such as Euclid MAX, Menicon Z Night, and NewVision SC to address these complex refractive profiles.

AI-driven corneal mapping and digital fitting platforms further support customization for irregular corneal geometries. As clinical confidence in Toric orthokeratology expands and diagnostic precision improves, astigmatism correction is gaining traction within advanced myopia management workflows.

Product Type Insights

Overnight Ortho-K Lenses are projected to lead, accounting for approximately 95% share in 2026, reflecting their entrenched role in modern pediatric myopia management workflows. Clinical adoption remains anchored by the convenience of overnight wear, enabling patients to achieve clear daytime vision without spectacles or daytime contact lenses. Technology evolution has reinforced the segment through high oxygen-permeable fluorosilicone acrylate materials and precision reverse-geometry lens manufacturing.

Industry leaders, including Johnson & Johnson Vision Care, CooperVision, and Bausch + Lomb, support adoption through platforms such as ACUVUE Abiliti, Paragon CRT, and Vision Shaping Treatment. The combination of its established clinical protocols, lifestyle compatibility, and mature product ecosystems sustains the segment’s structural dominance.

Overnight Ortho-K Lenses are anticipated to be the fastest-growing segment, driven by escalating pediatric myopia management demand and continuous product innovation. Emerging high oxygen permeability materials have strengthened safety perceptions associated with closed-eye overnight lens wear. Manufacturers, including Euclid Systems Corporation, Menicon, and Johnson & Johnson Vision Care, are advancing next-generation solutions such as Euclid MAX and Menicon Z Night.

The developments collectively reduce operational friction for clinics and strengthen practitioner confidence in overnight orthokeratology therapy. As clinical familiarity expands and material science continues advancing, overnight lenses are positioned to outpace overall North America orthokeratology market growth.

Country Insights

U.S. Orthokeratology Market Trends

U.S. is projected to lead, accounting for approximately 80% share in 2026, reflecting its entrenched clinical infrastructure and strong practitioner adoption. Established myopia management protocols and high professional awareness continue to anchor orthokeratology within mainstream optometry practices. The expanding pediatric myopia burden and strong participation in youth sports reinforce demand for overnight lens solutions, enabling daytime freedom from corrective eyewear.

Market leaders, including The Cooper Companies, Johnson & Johnson Vision Care, and Bausch + Lomb, maintain leadership through platforms such as Paragon CRT, ACUVUE Abiliti, and Vision Shaping Treatment. Digital ecosystem expansion using AI-enabled fitting portals and cloud-based corneal mapping strengthens practitioner efficiency and customization accuracy. This combination of mature clinical networks, technological integration, and strong consumer awareness sustains the U.S. dominant position.

Canada Orthokeratology Market Trends

Canada is anticipated to be the fastest-growing country, supported by demographic shifts and evolving clinical practice models. Urban population growth with higher myopia predisposition is expanding the patient pool requiring early intervention strategies. Canadian optometrists are increasingly transitioning toward medical optometry services, positioning orthokeratology as a specialized revenue-generating offering. Manufacturers, including Johnson & Johnson Vision Care, Euclid Systems Corporation, and CooperVision, are strengthening their presence through programs such as ACUVUE Abiliti and pediatric-focused Euclid MAX platforms.

Tele fitting protocols and cloud-based corneal mapping tools also enable practitioners to manage patients across Canada’s geographically dispersed regions.

Competitive Landscape

The orthokeratology market is moderately consolidated, with leadership concentrated among established suppliers such as CooperVision, Euclid Systems Corporation, Menicon, and Bausch + Lomb. These companies exert significant influence through proprietary lens geometries, advanced oxygen-permeable materials, and established practitioner training ecosystems supporting orthokeratology fitting. Their platforms, including Paragon CRT, Euclid MAX, Menicon Z Night, and Vision Shaping Treatment, anchor long-term clinical workflows across specialty optometry practices.

Leadership is further reinforced by strong partnerships with corneal topography software providers, enabling precision lens customization and data-driven fitting protocols that strengthen practitioner reliance on established technology ecosystems.

Competitive positioning across the sector reflects a mix of vertically integrated manufacturing, niche specialization, and practitioner network expansion. While leading brands dominate premium orthokeratology platforms, a fragmented layer of boutique laboratories continues to serve complex corneal cases through customized lens solutions. Industry behavior increasingly reflects consolidation as major vision care groups acquire specialty labs to secure intellectual property and practitioner relationships.

Platform evolution is also evident through digital fitting portals, automated custom lens manufacturing, and cloud-based patient monitoring tools. These developments are gradually reshaping the competitive landscape toward integrated service ecosystems where product innovation, digital infrastructure, and practitioner support collectively determine long-term market leadership.

Key Industry Developments:

- In February 2026, Health Canada issued updated safety guidance for Myopia Management Devices. This regulatory clarity encourages more Canadian optometrists to adopt Ortho-K, fueling Canada's status as the fastest-growing zone in the region.

- In January 2026, Euclid Vision Corporation officially launched the Be Free® Day Lens, a silicone hydrogel daily disposable lens for myopia. This expands Euclid's portfolio beyond overnight Ortho-K into daytime myopia management, utilizing technology licensed from the Brien Holden Vision Institute.

Companies Covered in North America Orthokeratology Market

- CooperVision

- Bausch + Lomb

- Johnson & Johnson Vision

- Euclid Systems Corporation

- Menicon Co., Ltd.

- Paragon Vision Sciences

- Alcon

- Art Optical Contact Lens, Inc.

- GP Specialists

- Alpha Corporation

- Visionary Optics

- Valley Contax

- TruForm Optics

- Miracorp

- E&E Optics

- Brighten Optix

Frequently Asked Questions

The North America orthokeratology market is projected to be valued at US$236.4 million in 2026 and is expected to reach US$353.1 million by 2033, supported by rising pediatric myopia prevalence and growing demand for non-surgical vision correction.

The increasing prevalence of childhood myopia, linked to prolonged screen exposure and reduced outdoor activity, is driving demand for preventive vision management solutions. Orthokeratology offers overnight corneal reshaping that provides clear daytime vision while helping slow myopia progression, making it an attractive option within structured pediatric myopia management programs.

The North America orthokeratology market is forecast to grow at a CAGR of 5.9% from 2026 to 2033, reflecting steady adoption across pediatric eye care programs and technological improvements in lens materials.

U.S. leads the regional market, accounting for approximately 80% share in 2026. Its dominance is supported by a mature optometry infrastructure, strong practitioner adoption of myopia management protocols, advanced digital fitting technologies, and high consumer awareness of pediatric vision care solutions.

The market is moderately consolidated, with major players including CooperVision, Bausch + Lomb, Johnson & Johnson Vision Care, Euclid Systems Corporation, Menicon Co., Ltd., Paragon Vision Sciences, and Alcon. These companies compete through proprietary lens designs, advanced oxygen-permeable materials, practitioner training programs, and integrated digital fitting platforms.